Students completing their studies, professionals switching jobs, or borrowers facing temporary cash shortages often look for ways to manage loan repayments more comfortably. This is where understanding a moratorium period becomes important.

India’s education loan portfolio recently grew by 15% to ₹8.58 lakh crore, increasing the number of borrowers navigating repayment concepts such as moratorium periods. As more young Indians rely on loans for education and financial needs, confusion around repayment pauses, interest charges, and EMI timelines has also increased.

Many borrowers assume a moratorium period means repayments stop completely, but loan terms may work differently depending on the lender and loan type. This guide explains what a moratorium period means, how it works, how interest is charged, and what borrowers should check before choosing one.

Key Takeaways

-

A moratorium period is a temporary lender-approved pause on loan repayments, commonly offered with education loans and certain financial hardship situations.

-

During a moratorium period, EMI payments may pause temporarily, but interest often continues accumulating on the outstanding loan amount.

-

Moratorium periods can help borrowers manage temporary income gaps during studies, job transitions, or short-term financial difficulty.

-

Borrowers should review revised EMIs, repayment tenure, and total repayment costs carefully before accepting a moratorium period.

-

Pocketly provides structured short-term borrowing options from ₹1,000 to ₹25,000 for eligible borrowers managing temporary financial gaps.

What Is a Moratorium Period? Everything You Need to Know

A moratorium period is a temporary pause on loan repayments approved by the lender for a specific period. During this time, borrowers may not need to pay full EMIs immediately, depending on the loan terms and lender policy.

Moratorium periods are commonly offered with education loans and may also apply in certain personal or business loan situations.

Many borrowers misunderstand moratorium periods as a complete break from loan obligations. However, in most cases, the repayment responsibility does not disappear. Interest may continue to accumulate during the moratorium period, which can increase the total repayment amount later.

In India, moratorium periods are often used during situations such as:

-

Students completing their studies before starting repayment

-

Borrowers facing temporary financial difficulty

-

Job transitions or temporary income gaps

-

Short-term repayment restructuring situations

For example, an education loan borrower may receive a moratorium period covering the course duration and a few additional months after graduation. During this period, the borrower gets time to secure employment before regular EMI payments begin.

Understanding how repayment pauses work can help borrowers avoid unexpected repayment pressure later.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

How Does a Moratorium Period Work?

A moratorium period temporarily postpones loan repayments for a specific duration approved by the lender. While this can reduce immediate repayment pressure, the exact repayment structure depends on the loan agreement and lender policy.

During the Moratorium Period

In most cases, borrowers receive a temporary break from full EMI payments. However, this does not always mean the loan becomes interest-free during that period.

Depending on the lender and loan type:

-

Full EMI payments may pause temporarily

-

Interest may continue to accumulate

-

Partial interest payments may still apply

-

The repayment schedule gets postponed

This is why borrowers should carefully check the loan terms before assuming repayment costs will remain unchanged.

After the Moratorium Period Ends

Once the moratorium period ends, regular repayments usually begin again. Depending on how interest accumulated during the pause, lenders may:

-

Increase the EMI amount

-

Extend the loan tenure

-

Revise the repayment schedule

-

Restructure the remaining balance

These changes vary across lenders and loan categories. Some lenders may also offer repayment restructuring options if the borrower continues to face temporary financial difficulty after the moratorium period.

For example, a salaried employee changing jobs may request a temporary repayment pause during the transition period. Once a stable income resumes, the borrower continues EMI payments based on the revised repayment schedule shared by the lender.

Before accepting any repayment pause, borrowers should review how interest accumulation and future EMIs may be affected.

Read More: How to Achieve a Perfect 900 CIBIL Score?

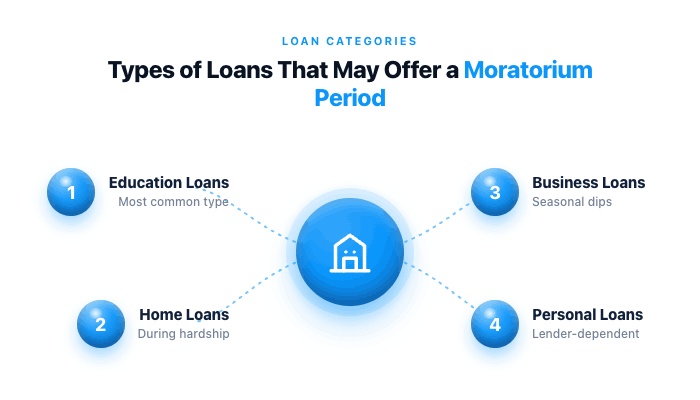

Types of Loans That May Offer Moratorium Periods

Moratorium periods are not limited to one type of borrowing. Different loan categories may offer repayment pauses depending on the lender’s policy, borrower profile, and repayment situation. However, the duration and conditions can vary significantly across loan types.

Education Loans

Moratorium periods are most commonly associated with education loans in India. Borrowers usually receive a repayment pause during:

-

The course duration

-

A specified period after course completion

-

The initial job-search phase

This allows students time to secure employment before regular EMI payments begin. However, interest may still accumulate during this period depending on the loan terms.

Home Loans

Some lenders may offer temporary repayment relief on home loans during situations such as:

-

Medical emergencies

-

Temporary job loss

-

Financial hardship

-

Economic disruptions

In these cases, lenders may restructure repayments or temporarily postpone EMIs based on the borrower’s repayment history and eligibility.

Business Loans

Business owners may seek moratorium support during periods of:

-

Seasonal revenue decline

-

Cash-flow disruptions

-

Operational slowdowns

-

Unexpected business expenses

Lenders may evaluate the business’s repayment capacity before approving any temporary repayment pause or restructuring request.

Personal Loans

Moratorium availability for personal loans depends heavily on lender-specific policies. Some lenders may offer temporary repayment flexibility during exceptional financial situations, while others may not provide formal moratorium options at all.

Borrowers should carefully review:

-

Interest treatment during the pause

-

Revised EMI structure

-

Additional charges or penalties

-

Updated repayment tenure

Short-term borrowing products may follow different repayment structures, so borrowers should review lender terms carefully before applying.

Also Read: Personal Loan vs Cash Advance Cost Comparison: What You’ll Actually Pay

Does Interest Continue During a Moratorium Period?

One of the most common misunderstandings about moratorium periods is that an EMI pause means the borrower does not pay anything extra later. In reality, most lenders continue charging interest during the moratorium period even if EMI payments are temporarily paused.

This means the outstanding loan amount may continue to grow during the repayment break. Once the moratorium period ends, the lender may:

-

Increase the EMI amount

-

Extend the repayment tenure

-

Adjust the repayment schedule

-

Add the accumulated interest to the remaining balance

The exact structure depends on the lender’s policy and loan agreement.

How This Usually Works

During the Moratorium Period:

-

EMI payments may pause temporarily

-

Interest may continue accumulating

-

Outstanding balance may increase

After the Moratorium Period:

-

Regular EMI payments resume

-

Total repayment amount may become higher

-

Loan tenure or EMI amount may change

For example, an education loan borrower may not need to pay full EMIs during the study period. However, interest may continue accumulating on the outstanding loan amount throughout the moratorium duration. Once repayment starts, the borrower may face higher EMIs or a longer repayment tenure depending on the accumulated interest.

Reviewing the total repayment amount before accepting a moratorium can help borrowers avoid larger repayment pressure later.

Also Read: Personal Loan Prepayment Charges Guide: Save or Lose Money?

Benefits and Drawbacks of a Moratorium Period

A moratorium period can provide temporary repayment relief during financially challenging situations. However, borrowers should also understand how it may affect the overall loan cost and repayment timeline later.

|

Benefits |

Considerations |

|

Temporary relief from immediate EMI payments |

Interest may continue accumulating during the pause |

|

Helps borrowers manage temporary income gaps |

Total repayment amount may increase later |

|

Supports short-term financial flexibility |

Loan tenure may become longer |

|

Useful during study periods or job transitions |

Future EMI amounts may change |

|

Can reduce immediate repayment stress |

Revised repayment schedules may affect budgeting |

A moratorium period can help borrowers manage temporary financial situations more comfortably, especially during education, job transitions, or short-term income disruptions.

However, borrowers should also plan for the revised repayment structure later, since accumulated interest and extended repayment periods may increase the overall loan burden.

Also Read: Payday Loans vs Personal Loans in India: Borrow Smartly in 2026

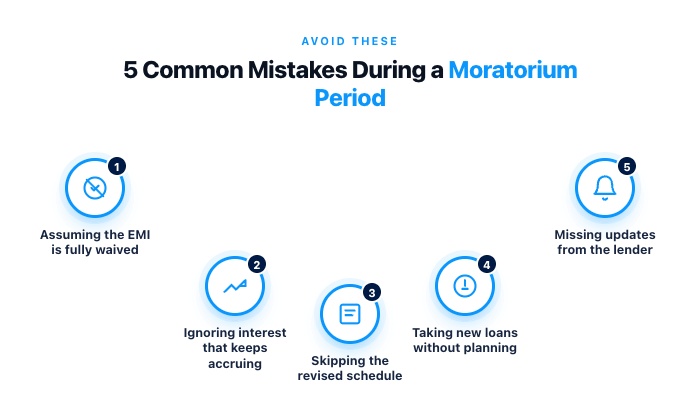

Common Mistakes Borrowers Make During Moratorium Periods

A moratorium period can reduce immediate repayment pressure, but misunderstanding how it works may create larger financial challenges later. Many borrowers focus on the short-term relief without fully reviewing the repayment impact after the pause ends.

1. Assuming the EMI Is Completely Waived: Many borrowers believe they no longer owe the EMI amount during the moratorium period. In reality, repayments are usually postponed, not cancelled permanently. The loan obligation typically continues under revised repayment terms.

2. Ignoring Interest Accumulation: A temporary EMI pause does not always stop interest charges. In many cases, interest continues accumulating on the outstanding balance during the moratorium period, which can increase the total repayment amount later.

3. Not Checking the Revised Repayment Schedule: Some borrowers accept the moratorium offer without reviewing the updated repayment structure. Depending on the lender’s policy, this may result in:

-

Higher future EMIs

-

Longer repayment tenure

-

Additional interest burden

Understanding these changes early helps borrowers prepare for future repayments more realistically.

4. Taking Additional Loans Without Proper Planning: Borrowers facing temporary financial pressure sometimes take new loans during the moratorium period without evaluating their future repayment capacity. Once all repayments resume together, managing multiple EMIs may become difficult.

5. Missing Communication From the Lender: Some borrowers fail to check updated lender notifications, revised schedules, or repayment instructions during the moratorium period. Missing these updates can create confusion around due dates, revised EMIs, or outstanding balances later.

Borrowers managing temporary financial gaps should evaluate repayment affordability carefully before taking additional short-term credit.

A Structured Way to Handle Short-Term Financial Gaps with Pocketly

Temporary repayment pressure during a moratorium period can sometimes create additional cash flow challenges, especially when borrowers still need to manage daily expenses alongside future EMI obligations. In such situations, structured short-term borrowing may help address urgent financial needs more responsibly.

Pocketly is a digital lending platform and not an NBFC. It works with RBI-registered NBFC partners to provide short-term borrowing options for young Indians, including students, salaried professionals, and self-employed individuals managing temporary financial gaps.

Instead of relying on unplanned borrowing, structured short-term credit may help borrowers manage situations such as:

-

Emergency medical expenses

-

Temporary rent gaps

-

Urgent utility bill payments

-

Emergency travel costs

-

Short-term cash flow shortages

Pocketly helps eligible borrowers access short-term personal loans ranging from ₹1,000 to ₹25,000 through a fully digital process. Key features include:

-

Interest rates starting from 2% per month

-

Processing fees ranging between 1% and 8%

-

Digital KYC verification

-

No collateral requirement

-

Direct transfer to eligible borrowers’ bank accounts

-

Short-term repayment structure

-

Fully digital application and repayment process

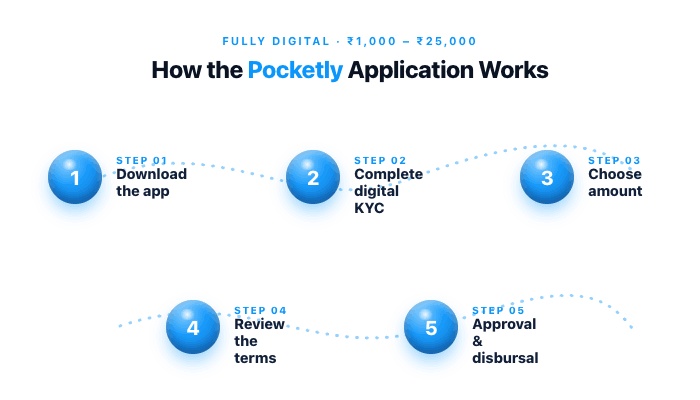

How the Application Process Works

-

Download the app or visit the website.

-

Complete the digital KYC process.

-

Select the required loan amount.

-

Review the repayment terms carefully.

-

Receive approval and disbursal for eligible applications.

If you need a small amount for an urgent expense, you can check your eligibility on Pocketly in a few minutes.

Before taking any short-term loan, borrowers should review the repayment timeline, total borrowing cost, and future EMI obligations carefully to avoid additional financial pressure later.

What to Check Before Accepting a Moratorium Period

Before choosing a moratorium period, borrowers should review how the repayment pause may affect future EMIs and total loan costs.

Check the following carefully:

-

Whether interest continues during the pause

-

Revised EMI or repayment tenure

-

Total repayment amount after restructuring

-

Existing monthly financial obligations

-

Future repayment affordability

A temporary EMI pause can reduce immediate pressure, but repayment planning remains important once the moratorium period ends.

If you need a small amount for an urgent expense during a temporary cash flow gap, you can check your eligibility on Pocketly in a few minutes. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

Frequently Asked Questions (FAQs)

1. Is interest charged during a moratorium period?

In most cases, yes. Even if EMI payments are temporarily paused, interest may continue accumulating on the outstanding loan amount during the moratorium period.

2. Does a moratorium period affect your credit score?

A lender-approved moratorium period generally does not affect the credit score negatively if the borrower follows the agreed repayment terms. However, missing payments outside the approved structure may impact credit history.

3. What happens after the moratorium period ends?

Once the moratorium period ends, regular repayments usually resume. Depending on the lender’s policy, the EMI amount, repayment tenure, or total repayment cost may change.

4. Is a moratorium period available for personal loans?

Some lenders may offer moratorium periods for personal loans during temporary financial hardship or exceptional situations. However, availability and repayment terms depend on the lender’s policy.

5. What is the difference between a grace period and a moratorium period?

A grace period usually refers to a short payment window before penalties apply, while a moratorium period is a temporary pause on scheduled loan repayments approved by the lender.