Keeping track of money sounds simple until your salary hits your account and slowly disappears into rent, UPI payments, subscriptions, and everyday expenses. You’re earning consistently, yet it never quite feels like you’re in control. The real problem isn’t how much you make, but how your money flows without visibility.

This is becoming more common. According to stats, India saw over 164 billion digital payment transactions in FY 2024, highlighting how effortless and frequent spending has become. When money moves this quickly, it’s easy to lose track and end up with a month-end cash crunch.

A cash flow budget solves this by giving you a clear view of your income and expenses in real time. In this blog, we will explore what a cash flow budget is, why it matters in the Indian context, and how you can create one step by step to manage your money better.

Key Takeaways

-

A cash flow budget helps track when money comes in and goes out, not just totals, so you can manage timing gaps in expenses.

-

It focuses on cash inflows, outflows, and net cash flow to highlight potential shortages or surpluses.

-

Categorising expenses into fixed, variable, and occasional makes it easier to plan for all types of spending.

-

Regular monitoring and adjusting the timing of payments ensures you avoid financial stress and reliance on credit.

-

Solutions like Pocketly can help cover short-term cash gaps, keeping your budget smooth and uninterrupted.

What is a Cash Flow Budget?

A cash flow budget is a simple way to track how money moves in and out of your life over a specific period, usually monthly. It focuses on two key elements:

-

Cash inflows: the money you earn (salary, freelance income, side income)

-

Cash outflows: the money you spend (rent, bills, food, shopping)

Unlike a regular budget that only lists expenses, a cash flow budget goes a step further. It helps you understand the timing and movement of your money, not just where it should go, but where it actually goes.

For example, you might earn ₹50,000 a month. But if most of your expenses happen in the first two weeks, you may still feel broke by the end of the month.

A cash flow budget highlights these gaps so you can plan better and avoid unnecessary stress.

Why Cash Flow Matters More Than Your Salary in India

Most advice around budgeting focuses on how much you spend. What often gets ignored is when you spend, and that’s where most financial stress actually comes from.

In India, this timing mismatch is more visible because of how our financial habits are structured. Salaries are usually credited once a month, but expenses don’t follow a schedule. They’re clustered, uneven, and often front-loaded.

Here’s what makes cash flow budgeting uniquely important:

-

It exposes “invisible stress points” in your month: You might not be overspending overall, but if too many expenses hit at the same time, your account balance dips sharply. This creates a temporary shortage, which often leads to borrowing or dipping into savings.

-

It helps you redesign your expense timing, not just reduce it: Instead of cutting down on spending, you can shift it to better align your cash flow. Moving certain payments or spreading expenses across the month can improve your financial comfort without changing your lifestyle.

-

It separates affordability from liquidity: Just because you can afford something on paper doesn’t mean you can pay for it at that moment. Cash flow budgeting helps you avoid situations where you’re technically “fine” but practically broke.

-

It reduces dependence on short-term fixes: Many people rely on credit, borrowing, or delaying payments not because they lack money, but because of poor timing. Fixing cash flow often removes the need for these quick fixes.

-

It gives you decision-making clarity in real time: Instead of guessing, "Can I afford this? You know exactly where you stand in that moment in the month. This changes how you spend, save, and plan.

A cash flow budget doesn’t just organise your money; it changes how you experience it. Instead of reacting to shortages, you start anticipating them and quietly staying ahead.

Projects often fail not because of work, but because money runs out at the wrong time. Cash flow shows you when money comes in and goes out, so you can plan better. Learn how to manage project cash flow easily, even as a beginner.

The Key Parts of a Cash Flow Budget Explained

A cash flow budget may sound technical, but at its core, it answers a very simple question: How much money is coming in, how much is going out, and do you have enough left when you need it?

To understand this clearly, break it into three parts:

1. Cash Inflows (Money You Receive)

This includes all the money that comes into your account during the month:

-

Salary

-

Pocket money or allowance

-

Freelance or side income

-

Bonuses or any extra income

The important thing here is to focus on actual income, not expected income. For example, if you might get freelance work or a bonus, don’t include it until you actually receive it. This keeps your budget realistic and avoids overconfidence in spending.

2. Cash Outflows (Money You Spend)

This is where most confusion happens, because not all expenses look the same. To make sense of it, divide your spending into three simple categories:

-

Fixed expenses (same every month): These are payments you cannot avoid and usually stay constant. Examples: rent, EMIs, subscriptions.

-

Variable expenses (change every month): These depend on your lifestyle and choices.

Examples: food, travel, shopping, eating out. -

Occasional expenses (not monthly, but unavoidable): These don’t happen every month, but they are still part of your life. Examples: festivals, trips, medical needs, repairs.

Most beginners ignore this third category. That’s why even a “planned” budget fails. These expenses feel sudden, but in reality, they are just not planned in advance.

3. Net Cash Flow (What You Have Left)

This is the most important part of your cash flow budget.

Simple formula: Money In – Money Out = Money Left

-

If you have money left over, you have positive cash flow. This is what you can use for savings or investments.

-

If you have nothing left or go below zero, it means your spending is too high or not timed well.

One important thing to understand here is that having money left on paper is not enough. If most of your expenses happen early in the month, you can still feel broke later, even with a positive balance overall.

Make short-term cash gaps easy to manage. Pocketly gives ₹1,000–₹25,000 instantly, helping you pay on time. Apply in minutes and cover urgent payments without hassle.

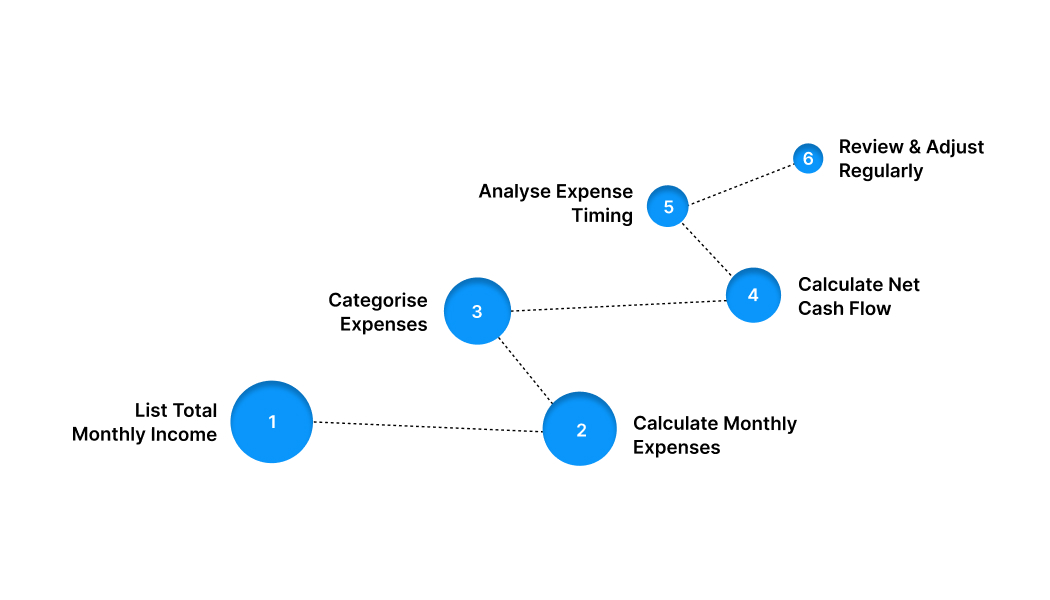

How to Create a Cash Flow Budget (Step by Step)

Most people think budgeting fails because they lack discipline. In reality, it fails because they try to plan money in totals, not in flow.

You don’t run out of money because you didn’t earn enough. You run out because your money didn’t last at the right time. The steps below are not just about listing income and expenses.

Step 1: Start by Listing Your Total Monthly Income

Begin by identifying how much money you actually receive in a month. This should include your salary (after deductions), any side income, freelance work, or fixed allowances.

It’s important to consider only reliable and consistent income. Avoid including uncertain amounts like expected bonuses or irregular earnings, as this can lead to overestimating your budget.

For example, if your monthly salary is ₹40,000 and you earn an additional ₹5,000 from freelance work, your total inflow would be ₹45,000.

Step 2: Calculate Your Monthly Expenses

Next, list down all your expenses to understand where your money is going. Start with essential and fixed costs such as rent, EMIs, and utility bills, then include everyday spending like food, travel, and subscriptions.

To make this easier, you can review your bank statements or UPI transaction history. This helps you capture even small expenses that are often overlooked but add up over time.

For instance, if you spend ₹15,000 on rent, ₹5,000 on groceries, and ₹3,000 on transport, your total expenses begin to take shape more clearly.

Step 3: Categorise Your Expenses for Better Clarity

Once you have your list, group your expenses into categories such as fixed, variable, and occasional.

Fixed expenses remain the same every month, while variable expenses change based on your lifestyle. Occasional expenses, like travel or festivals, may not occur monthly but still need to be planned for.

This step helps you understand which expenses are unavoidable and which ones can be adjusted if needed.

Step 4: Calculate Your Net Cash Flow

Now subtract your total expenses from your total income to find out how much money you have left.

Net Cash Flow = Total Income – Total Expenses

If the result is positive, you have surplus money that can be saved or invested. If it is negative, it indicates that your expenses are higher than your income and need to be adjusted.

This step gives you a clear picture of your financial position.

Step 5: Analyse the Timing of Your Expenses

Beyond totals, it is important to observe when your money is being spent during the month.

For example, if most of your expenses are paid within the first 10 days, you may feel financially stretched later, even if your overall budget is balanced.

By identifying this pattern, you can try to shift or spread certain expenses to maintain a smoother cash flow throughout the month.

Step 6: Review and Adjust Regularly

A cash flow budget is not something you create once and forget. Your income, expenses, and priorities can change over time.

Set aside some time at the end of each month to review your budget, identify any gaps, and make necessary adjustments. This ensures your budget stays relevant and continues to work for you.

Planning your cash doesn’t have to be confusing or scary. With the right approach, you can see what’s coming in, what’s going out, and stay ahead. Learn how with our beginner-friendly cash planning guide 2026.

How a Cash Flow Budget Looks: Indian Example

Most cash flow examples stop at “income minus expenses.” But what actually matters is when money comes in vs when it goes out, especially in India, where salary dates and bill cycles rarely align.

Monthly Cash Flow Breakdown

|

Category |

Amount (₹) |

|

Salary |

50,000 |

|

Freelance/Side Income |

5,000 |

|

Total Inflow |

55,000 |

Monthly Expenses

|

Category |

Amount (₹) |

|

Rent |

15,000 |

|

Groceries & Food |

6,000 |

|

Travel & Fuel |

4,000 |

|

Utility Bills |

3,500 |

|

EMIs |

5,000 |

|

Entertainment & Shopping |

4,000 |

|

SIP/Investments |

3,000 |

|

Miscellaneous |

4,500 |

|

Total Outflow |

45,000 |

Also Read: Financial Planning in Your 30s: Smart Money Guide (2025)

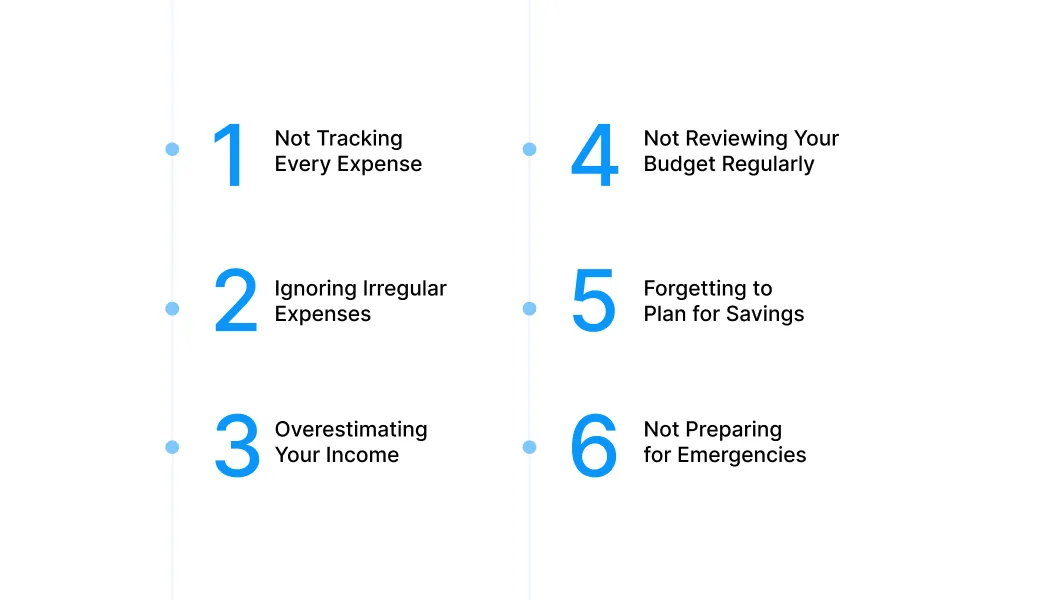

Common Cash Flow Budgeting Mistakes and How to Avoid Them

Even with the right intentions, small mistakes can throw your entire cash flow off track. Here are some common ones to avoid:

1. Not Tracking Every Expense

Risk: Missing out on small or irregular expenses can create a mismatch between your planned and actual cash flow, leading to overspending without realising it.

Mitigation: Track every expense consistently, big or small. Use UPI history, bank statements, or a budgeting app to ensure nothing slips through the cracks.

2. Ignoring Irregular Expenses

Risk: Expenses like festivals, travel, insurance premiums, or yearly subscriptions can disrupt your budget when they suddenly arise.

Mitigation: Identify all non-monthly expenses and spread them across the year. Set aside a small amount each month to prepare for these costs in advance.

3. Overestimating Your Income

Risk: Relying on uncertain income like bonuses, incentives, or freelance payments can make your budget unrealistic and lead to shortfalls.

Mitigation: Base your budget on fixed and predictable income. Treat variable earnings as extra and allocate them only after they are received.

4. Not Reviewing Your Budget Regularly

Risk: A static budget can quickly become outdated due to changes in income, lifestyle, or expenses, reducing its effectiveness.

Mitigation: Review your cash flow budget monthly. Adjust categories and allocations based on your current financial situation.

5. Forgetting to Plan for Savings

Risk: Treating savings as optional often results in little to no money being set aside, impacting long-term financial stability.

Mitigation: Make savings a fixed part of your outflow. Allocate a specific percentage of your income toward savings before spending on non-essentials.

6. Not Preparing for Emergencies

Risk: Unexpected expenses like medical emergencies or urgent repairs can disrupt your cash flow and force you into debt.

Mitigation: Build an emergency fund gradually. Aim to save at least 3–6 months’ worth of essential expenses to handle unforeseen situations.

Finding It Hard to Stick to Your Cash Flow Budget? Pocketly Can Help You Stay Balanced

Even with a well-planned cash flow budget, there are moments when things don’t line up. A bill might be due today, while your salary is still a few days away. Or an unexpected expense can show up right when your budget is already tight.

In such situations, the problem isn’t your planning; it’s the timing of your cash flow.

Pocketly is built to support you during these short gaps. It gives you quick access to small amounts of money so you can manage immediate expenses without disturbing your savings or long-term financial plans.

Here’s how it helps:

-

Manages short-term cash gaps smoothly: Whether it’s rent, utilities, or an urgent payment, you can handle it on time without stretching your budget or delaying expenses.

-

Borrow only what’s necessary: With access to ₹1,000 to ₹25,000, you can cover specific needs instead of taking on a larger, unnecessary loan.

-

Fast access when you need it most: A simple digital process ensures quick approval and direct transfer to your bank account, saving you from delays and last-minute stress.

-

No complicated eligibility barriers: You don’t need a strong credit history, collateral, or a guarantor, making it easier for students and first-time earners to access funds.

-

Repay in a way that fits your income cycle: Flexible repayment options help you plan your EMIs around your salary, so your monthly cash flow remains stable.

-

Clear, upfront costs: Interest starts from 2% per month, with processing fees between 1% and 8%, so you know the total cost before you borrow.

-

Helps you avoid financial disruptions: Paying bills on time means no late fees, no service interruptions, and better control over your overall budget.

-

Simple, app-based experience: From applying to tracking repayments, everything is managed in one place, making it easy to stay organised.

Pocketly works best as a short-term financial cushion, not something to rely on regularly. When used carefully, it helps you handle timing mismatches without losing control of your cash flow budget.

With quick access to small loan amounts, instant approvals, and flexible repayment options, you can handle urgent expenses without disrupting your overall financial flow.

Download Pocketly on iOS or Android to manage short-term cash needs easily and stay in control of your finances.

FAQs

1. What is a cash flow budget in simple terms?

A cash flow budget tracks all money coming in (income, salary, side earnings) and going out (bills, groceries, EMIs, discretionary spending) over a period, usually monthly. It helps you see the timing of money, anticipate shortages, and ensure essentials are covered before spending on non-essentials.

2. How is a cash flow budget different from a regular budget?

A regular budget sets spending limits for categories, while a cash flow budget maps when money enters and leaves your account, helping avoid gaps between due payments and income, especially useful for managing EMIs, salary cycles, and festival expenses.

3. Why is a cash flow budget important in India?

Expenses like festival shopping, school fees, or travel can vary monthly. Cash flow budgeting helps prioritise essentials, savings, and goals, preventing overspending early in the month and ensuring funds are available when needed.

4. How can I create a cash flow budget easily?

List all income sources: salary, freelance payments, and passive income. Track all expenses, categorise them, calculate net cash flow (income minus expenses), and adjust spending to avoid negative flow. Tools like Excel, Google Sheets, or Indian budgeting apps make this simpler.

5. What is a positive vs a negative cash flow?

Positive cash flow occurs when income exceeds expenses, allowing for savings or investments. Negative cash flow happens when expenses exceed income, highlighting areas to reduce spending before it impacts financial health.

6. How often should I update my cash flow budget?

Monthly reviews are ideal, or weekly for freelancers/self-employed individuals. Regular updates help accommodate unexpected expenses and adjust allocations for payments like festival shopping or travel.