Struggling to manage expenses before your next salary hits? For many young Indians, the problem isn’t just borrowing money; it’s figuring out how to repay it without disrupting their monthly budget. What feels manageable at the moment can quickly turn stressful when EMIs start stacking up.

This isn’t an isolated issue. According to stats, household debt reached 41.3% of GDP by March 2025, with a growing share driven by consumption-led borrowing.

In simple terms, more people are relying on credit for everyday needs, but not always choosing the right repayment structure.

In this blog, we’ll break down different EMI options, how they work, and how to choose one that fits your income, not just your loan amount.

Key Takeaways

-

EMI is not just a monthly deduction; it is a repayment structure that decides how your debt is reduced over time.

-

In most loans, early payments primarily cover interest, so principal reduction starts slower than expected.

-

A lower EMI usually comes from extending tenure, which can quietly increase total repayment even if the monthly burden feels easy.

-

EMI decisions are less about affordability today and more about how long your money stays locked in repayment cycles.

-

The right EMI is the one that stays sustainable even when income or expenses don’t go as planned.

What Are EMI Options?

EMI options refer to the different ways you can structure your monthly loan repayments, not just the act of paying them.

At its core, an EMI (Equated Monthly Instalment) is a fixed monthly payment made towards repaying a loan, which includes both the principal amount and the interest charged by the lender.

But here’s what most people miss: while the EMI amount may look simple, how it is structured can vary significantly.

Depending on the lender and loan type, you may get options to:

-

Adjust your repayment tenure

-

Choose lower or higher monthly instalments

-

Start with smaller payments and increase later

-

Opt for flexible or customised repayment plans

In simple terms, EMI options decide how your repayment fits into your monthly life, not just how much you repay.

And that’s exactly why choosing the right EMI option matters more than most borrowers realise.

Why Do EMI Options Decide How Fast You Get Out of Debt?

An EMI may look like a fixed monthly number, but what actually changes over time is what you’re paying for.

In the early months of a loan, a larger portion of your EMI goes toward interest, not the principal. Over time, this gradually shifts, and more of your payment starts reducing the actual loan amount.

This has a direct implication most borrowers overlook:

Your repayment structure decides how quickly you actually get out of debt—not just how much you pay each month.

For example:

-

A longer tenure lowers your EMI but keeps you paying interest for longer

-

A flexible EMI may reduce pressure now, but delay principal repayment

-

A poorly chosen structure can make you feel like you’re “paying regularly” without significantly reducing what you owe

So EMI options aren’t just about affordability; they control the pace at which your debt shrinks.

And that’s the real decision most borrowers don’t realise they’re making.

Also read: Interest Rates in India 2026: How They Affect Loans & Savings

5 Types of EMI Options You Should Actually Understand

Different EMI options tweak the pattern, shifting how quickly your payments start impacting the principal.

Here are the following EMI options you should understand:

1. Standard EMI (Reducing Balance EMI)

This is the most widely used EMI structure where you pay a fixed monthly instalment, but interest is calculated on the remaining loan balance, not the original amount. This means the interest portion is higher in the beginning and gradually reduces as you repay the principal.

For example, on a ₹1,00,000 loan at 12% for 12 months, early EMIs mostly go toward interest, while later EMIs contribute more toward reducing the actual loan amount.

This structure works best for salaried individuals with stable income who can commit to regular repayments. However, the loan feels slower to reduce in the initial months, even though you are paying consistently.

2. No-Cost EMI

No-cost EMI allows you to break a purchase into monthly instalments without showing explicit interest. However, the cost is usually adjusted through discounts or pricing changes by the seller, meaning the interest is not truly eliminated.

For example, a ₹12,000 product on 6-month no-cost EMI may appear as ₹2,000 per month, but the final price structure already accounts for the financing cost.

This option is useful for short-term product purchases like electronics or appliances. The trade-off is that the “no-cost” benefit is often indirect rather than absolute.

3. Low-Cost EMI

Low-cost EMI reduces your overall interest burden through partial subsidies offered by lenders or merchants. This makes monthly payments more affordable compared to standard EMI structures.

For example, on a ₹50,000 purchase, part of the interest may be waived or reduced, resulting in slightly lower monthly instalments.

It works well for budget-conscious borrowers, but you are still paying interest—just at a reduced rate, so it is not completely free.

4. Credit Card EMI

Credit card EMI converts a purchase made on your credit card into fixed monthly repayments. The tenure and interest rate depend on the card issuer and selected plan.

For example, a ₹20,000 purchase can be split into 3, 6, or 12-month EMIs, where interest is added based on the bank’s terms.

This is useful for urgent, short-term purchases, but it can increase credit utilisation and affect your overall credit behaviour if not managed carefully.

5. Flexible / Step-Up EMI

Step-up EMIs start with lower monthly payments in the early stage and increase gradually over time, based on the expectation that your income will grow.

For example, you might begin with a ₹3,000 EMI that increases to ₹5,000 later in the tenure.

This structure is suitable for early-career professionals, but it can become stressful later if income does not grow as expected, since repayment pressure increases over time.

Quick Overview

|

EMI Type |

How It Works |

Interest Structure |

Best For |

Key Trade-Off |

|

Standard EMI (Reducing Balance) |

Fixed monthly payment across tenure |

Interest calculated on outstanding balance; the higher interest portion is paid early, reducing over time |

Most borrowers with stable income |

Slower principal reduction in the early months |

|

No-Cost EMI |

Equal instalments with no visible interest |

Interest is adjusted via pricing/discounts |

Short-term purchases |

Not truly “free”; cost is hidden |

|

Low-Cost EMI |

EMI with reduced interest |

Part of the interest is subsidised |

Cost-conscious borrowers |

Still pays interest, just lower |

|

Credit Card EMI |

Converts purchase into EMIs via credit limit |

Interest depends on the issuer and tenure |

Quick, short-term financing |

Impacts credit utilisation |

|

Flexible / Step-Up EMI |

Lower EMIs initially, higher later |

Interest applies normally, structure shifts timing |

Income expected to grow |

Higher future repayment pressure |

If you are exploring short-term financial support, understanding repayment structure can help you choose a smaller, more manageable loan that fits your cash flow through platforms like Pocketly. Apply now for quick, flexible credit.

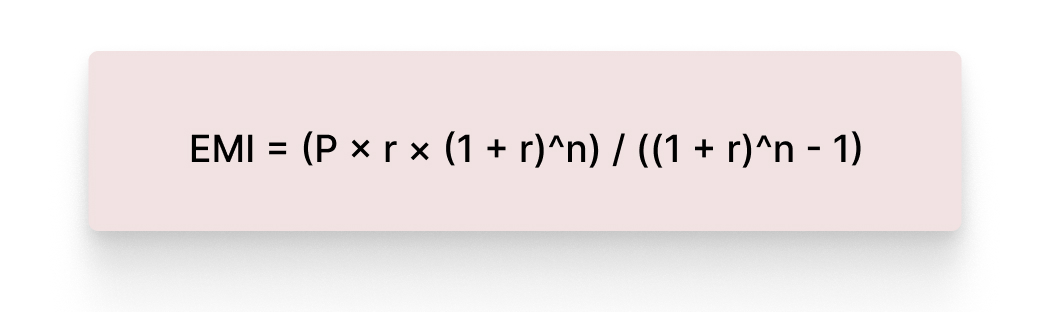

What EMI Calculation Looks Like in a Real Loan?

EMI is calculated using a standard formula based on three factors: loan amount, interest rate, and repayment tenure.

EMI = (P × r × (1 + r)^n) / ((1 + r)^n - 1)

Here, P is the principal, r is the monthly interest rate, and n is the number of monthly payments.

Let’s take a simple scenario to see how EMI behaves beyond just the number.

Assume you borrow ₹1,00,000 at 12% annual interest for 12 months. Your EMI comes out to roughly ₹8,885 using the standard reducing-balance method.

At first glance, this looks straightforward, but the breakdown tells a different story.

In the first month, a significant portion of that ₹8,885 goes toward interest because it’s calculated on the full loan amount. As you continue paying, the outstanding balance reduces, and so does the interest portion. Over time, more of your EMI starts going toward the principal instead.

This shift is what most borrowers don’t see. Even though the EMI stays constant, the effectiveness of each payment improves over time, which is why early repayments or better EMI structures can significantly reduce your total interest.

Also read: Credit vs Loan in India: Key Differences & Smart Choice (2026)

How to Choose an EMI Option That Fits Your Cash Flow?

Picking an EMI option isn’t about finding the lowest monthly number; it’s about choosing a structure you won’t regret three months later. The real decision is how much pressure you’re willing to carry consistently, not temporarily.

|

Factor |

What to Check |

Why It Matters |

|

Income stability |

Choose EMI based on your lowest earning month |

EMIs are fixed, income isn’t |

|

Tenure vs cost |

Longer tenure = lower EMI but higher total interest |

Extending tenure increases total repayment |

|

EMI size |

Keep total EMIs within ~30–40% of income |

Higher ratios increase financial stress |

|

Total repayment |

Check the total amount paid, not just EMI |

A lower EMI can hide a higher interest cost |

|

Existing EMIs |

Consider all current obligations together |

Multiple EMIs can strain cash flow |

|

Flexibility |

Look for prepayment or adjustment options |

Helps if income or expenses change |

|

Future uncertainty |

Plan for unexpected expenses |

EMIs continue regardless of the situation |

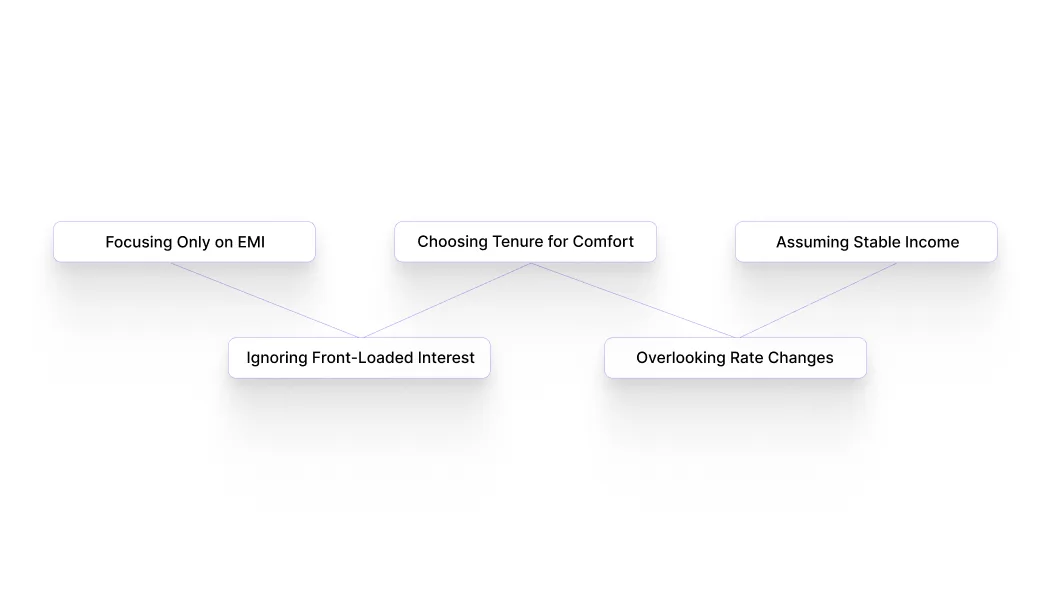

5 Typical EMI Mistakes That Quietly Increase Your Loan Cost

Most EMI mistakes aren’t obvious. They don’t show up in your monthly payment—they show up in how long you stay in debt and how much extra you end up paying.

1. Focusing Only on the EMI Amount

Risk: A lower EMI often comes from a longer tenure, which increases total interest paid over time, even if the monthly amount feels manageable.

Mitigation: Always check the total repayment amount, not just the EMI. A slightly higher EMI with a shorter tenure can reduce your overall cost significantly.

2. Ignoring How Interest Is Front-Loaded

Risk: In most loans, early EMIs are dominated by interest, so your principal reduces slowly at the beginning.

Mitigation: Review the principal vs interest split or amortisation schedule to understand how quickly your loan balance will actually reduce.

3. Choosing Tenure Based on Comfort Alone

Risk: Longer tenures reduce monthly burden but extend your debt cycle and increase total interest outgo.

Mitigation: Choose a tenure that balances affordability with faster principal repayment, not just immediate comfort.

4. Overlooking the Impact of Interest Rate Changes

Risk: In floating-rate loans, EMIs or tenure can change when interest rates are revised, increasing your repayment burden unexpectedly.

Mitigation: Factor in rate fluctuations and maintain a buffer so your EMI remains manageable even if rates increase.

5. Assuming Consistent Financial Stability

Risk: EMI plans are built on stable income assumptions, but real-life expenses and income often fluctuate.

Mitigation: Choose an EMI that remains manageable even during low-income or high-expense months, not just ideal conditions.

How Pocketly Fits When the Need Is Small and Time-Sensitive

Borrowing decisions aren’t just about getting money quickly; they’re about how efficiently that money is repaid after you take it. The same loan components (amount, interest, and tenure) determine whether credit stays manageable or becomes unnecessarily expensive.

That’s why short-term borrowing works best when it stays tightly aligned with the actual need, without extending repayment beyond what is required.

Pocketly is built for such situations where the requirement is small, urgent, and time-bound.

It helps by:

-

Offering smaller loan amounts, so you borrow only what you actually need

-

Keeping repayment cycles short helps avoid long interest accumulation

-

Starting interest from around 2% per month, with processing fees typically between 1%–8%, based on profile and loan amount

-

Showing costs upfront, so you know the repayment impact before you decide

Download the Pocketly app today on [Android] or [iOS] to access funds quickly and keep your finances steady, no matter what comes your way.

FAQs

1. What is the difference between EMI and loan repayment?

EMI is a structured way of repaying a loan in fixed monthly instalments, while loan repayment is the overall process of clearing the borrowed amount with interest.

2. How many EMI options are available in personal loans?

Most lenders offer multiple EMI structures, such as fixed EMI, flexible EMI, step-up EMI, and reducing balance EMI, depending on borrower eligibility.

3. Which EMI option reduces total interest cost the fastest?

Reducing balance EMIs with shorter tenure reduces total interest cost faster because more of your payment goes toward principal repayment early on.

4. What happens if I choose a longer EMI tenure?

A longer tenure reduces your monthly EMI but increases the total interest paid over the loan period, making the loan more expensive overall.

5. Are EMI options the same for all lenders in India?

No, EMI options vary across banks, NBFCs, and digital lending platforms depending on their interest structure and repayment policies.

6. Can EMI options impact my credit score?

Yes, timely repayment of EMIs improves your credit score, while missed or delayed EMIs can negatively impact your credit history.

7. What is the safest EMI option for salaried individuals?

A fixed or reducing balance EMI with a moderate tenure is usually safest for salaried individuals as it balances affordability and total interest cost.