Interest rates may seem like just another number attached to a loan or savings account, but they quietly influence how much you pay, how much you earn, and how quickly you reach your financial goals. From home loans and credit cards to fixed deposits and personal loans, this single percentage can reshape your entire financial plan.

The problem is that many people focus only on the EMI or short-term return without understanding the bigger picture. Even a small change in interest rates can increase your total repayment significantly or reduce the growth of your savings over time. Left unchecked, this can slow your progress and create avoidable financial pressure.

In this blog, we will break down what interest rates really mean, the different types you should know, how they are decided, and how they affect your loans and investments so you can make smarter, more confident financial decisions.

TL;DR

- Interest rates determine the cost of borrowing and the return on savings, directly affecting EMIs, total repayments, and investment growth.

- Understanding fixed, floating, simple, compound, and other types of interest rates helps you make smarter loan and investment choices.

- In India, rates are influenced by RBI policies, inflation, market liquidity, and your personal credit profile.

- Small changes in interest rates can significantly impact long-term finances, so evaluating total cost, compounding, and loan tenure is crucial.

- Tools like Pocketly provide short-term financial support, helping you manage cash gaps responsibly without disrupting your budget.

What Are Interest Rates?

An interest rate is the percentage charged on borrowed money or earned on saved money. It represents the cost of using someone else’s funds or the reward for allowing a bank or institution to use yours.

In simple terms, it answers one key question: how much extra will you pay or earn over time?

Here is what interest rates mean in practical terms:

- For borrowers, it is the additional amount paid on top of the principal.

- For savers, it is the income earned on deposits or investments.

- It is usually expressed as an annual percentage.

- It directly affects EMIs, total repayment, and investment returns.

- Even small rate changes can significantly impact long-term finances.

Whether you are taking a loan or building savings, understanding interest rates helps you calculate the real cost and real return of your money.

Why Understanding Interest Rates Can Save You Thousands

Interest rates influence almost every part of your financial life. They determine how expensive it is to borrow, how rewarding it is to save, and how quickly you can move toward your goals. Even small changes can create a noticeable difference over time.

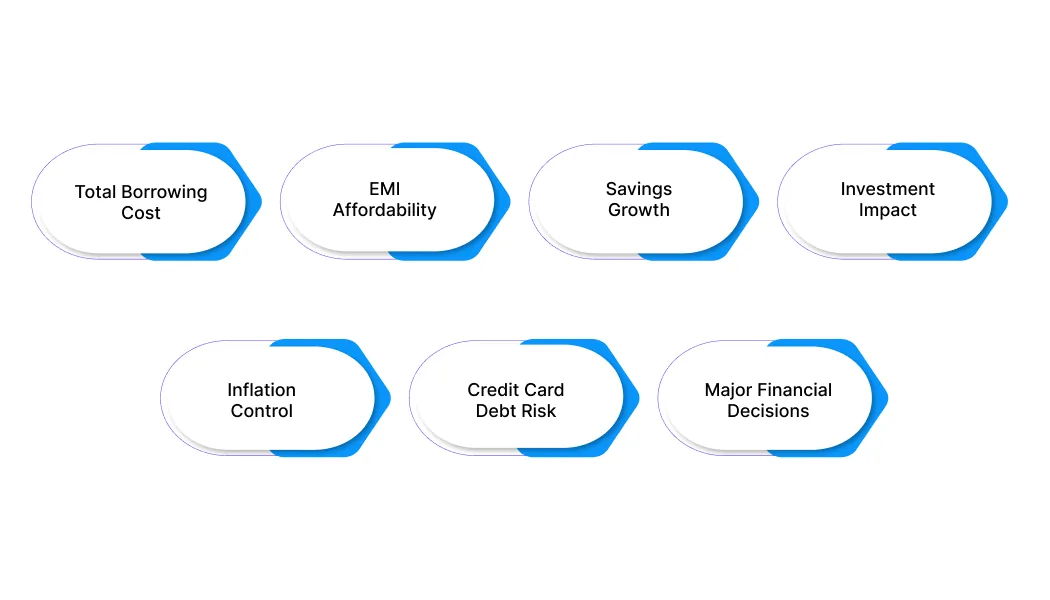

Here is why interest rates deserve serious attention:

Here is why interest rates deserve serious attention:

- Total cost of borrowing: A higher rate increases not just your EMI but the overall amount repaid across the loan tenure.

- EMI affordability: When rates rise, monthly payments increase, putting pressure on your cash flow and budget.

- Growth of savings: Better rates on fixed deposits or savings instruments help your money compound faster.

- Impact on investments: Interest rate movements influence bond returns, stock market trends, and overall investor sentiment.

- Inflation control: Central banks adjust interest rates to manage inflation, which affects purchasing power and daily expenses.

- Credit card debt risk: High credit card interest can quickly multiply unpaid balances, making short-term borrowing very expensive.

- Major life decisions: Rate levels often influence when people buy homes, upgrade vehicles, or expand businesses.

Types of Interest Rates You Should Know

Not all interest rates work the same way. The structure of the rate determines how much you ultimately pay or earn and how predictable your financial commitment will be.

Here is a clear comparison of the most common types:

| Type of Interest Rate | How It Works | Financial Impact | Commonly Used For |

| Fixed Interest Rate | Remains the same throughout the loan or deposit tenure | EMI and returns stay predictable | Home loans, car loans, fixed deposits |

| Floating Interest Rate | Changes based on market benchmarks or policy rates | EMI may increase or decrease over time | Home loans, business loans |

| Simple Interest | Calculated only on the principal amount | Lower total interest compared to compounding | Short-term loans |

| Compound Interest | Calculated on principal plus accumulated interest | Higher overall cost or return over time | Long-term loans, savings, investments |

| Reducing Balance Interest | Interest is calculated on the outstanding loan balance | The interest amount reduces as you repay the principal | Most bank loans |

| Flat Interest Rate | Calculated on the entire principal for the full tenure | Higher effective cost compared to the reducing balance | Some personal or consumer loans |

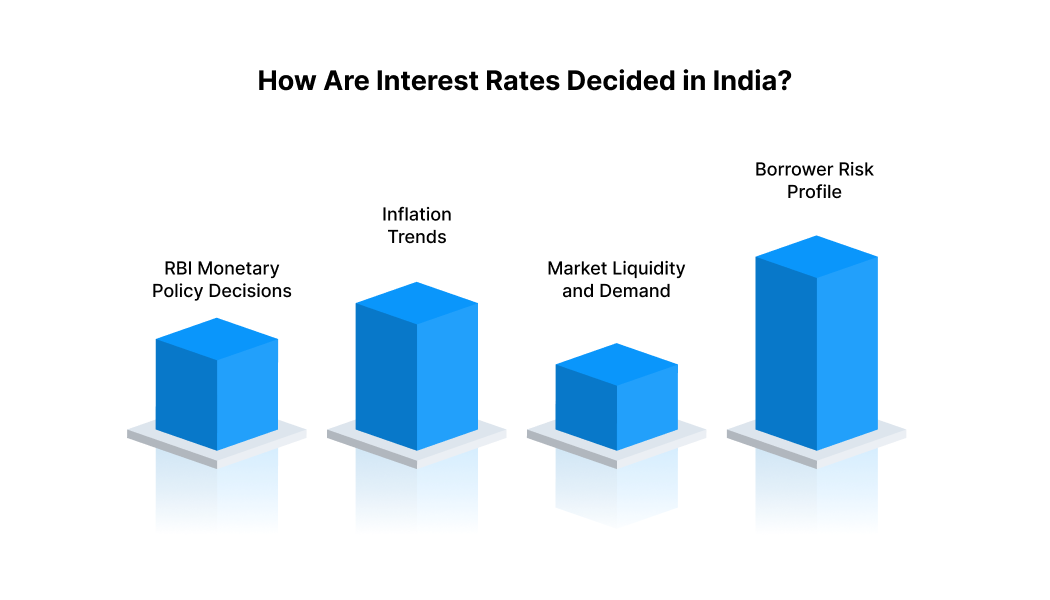

How Are Interest Rates Decided in India?

Interest rates are not set randomly. They are influenced by economic conditions, central bank policies, and your personal credit profile. Understanding these factors helps you anticipate rate changes and negotiate better loan terms.

Here are the key drivers:

Here are the key drivers:

1. RBI Monetary Policy Decisions

The Reserve Bank of India plays a central role in shaping interest rates across the country. Through its monetary policy reviews, it adjusts key rates to manage inflation, control liquidity, and support economic growth. When policy rates move, banks typically revise their lending and deposit rates accordingly.

For instance, if the RBI increases the repo rate to control rising inflation, banks may raise home loan and personal loan interest rates within weeks. As a result, borrowers could see their EMIs increase even if their loan amount remains the same.

2. Inflation Trends

Inflation directly impacts interest rate decisions. When prices rise rapidly, central banks often increase rates to slow down spending and stabilise the economy. Conversely, during low inflation or economic slowdown, rates may be reduced to encourage borrowing and investment.

For example, during periods of high inflation, you may notice loan rates increasing while fixed deposit returns also improve. This adjustment is aimed at balancing purchasing power and economic activity.

3. Market Liquidity and Demand

The availability of funds in the banking system influences how aggressively banks lend. When liquidity is tight or loan demand is high, interest rates may rise. When liquidity is abundant, banks may lower rates to attract borrowers.

For instance, during festive seasons when loan demand surges, certain lending rates may inch upward due to higher borrowing activity.

4. Borrower Risk Profile

Beyond economic factors, your personal financial profile plays a key role. Banks assess your credit score, income stability, repayment history, and existing debt before deciding your interest rate. Lower perceived risk usually means better rates.

For example, a borrower with a strong credit score and stable income may receive a home loan at a lower rate compared to someone with irregular income or missed repayments.

How Interest Rates Affect Different Loan Types

Interest rates do not impact every loan in the same way. The effect depends on the loan structure, tenure, and whether the rate is fixed or floating. When rates rise, some loans become immediately expensive, while others create slower but long-term financial pressure.

Here is a clearer breakdown:

| Loan Type | Interest Rate Impact | What Changes for You | Risk Level if Rates Rise |

| Home Loan | Highly sensitive due to long tenure and large principal | EMI may increase, or tenure may extend, raising total repayment | High |

| Personal Loan | Generally, higher base rates are associated with unsecured loans | Higher EMI burden and greater total interest paid | Medium to High |

| Credit Card | Very high interest, usually compounding monthly | The outstanding balance grows quickly if it is unpaid | Very High |

| Car Loan | Moderate sensitivity depending on rate structure | EMI may rise slightly, affecting the monthly budget | Medium |

| Business Loan | Impacts working capital and expansion costs | Higher borrowing costs reduce cash flow flexibility | High |

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

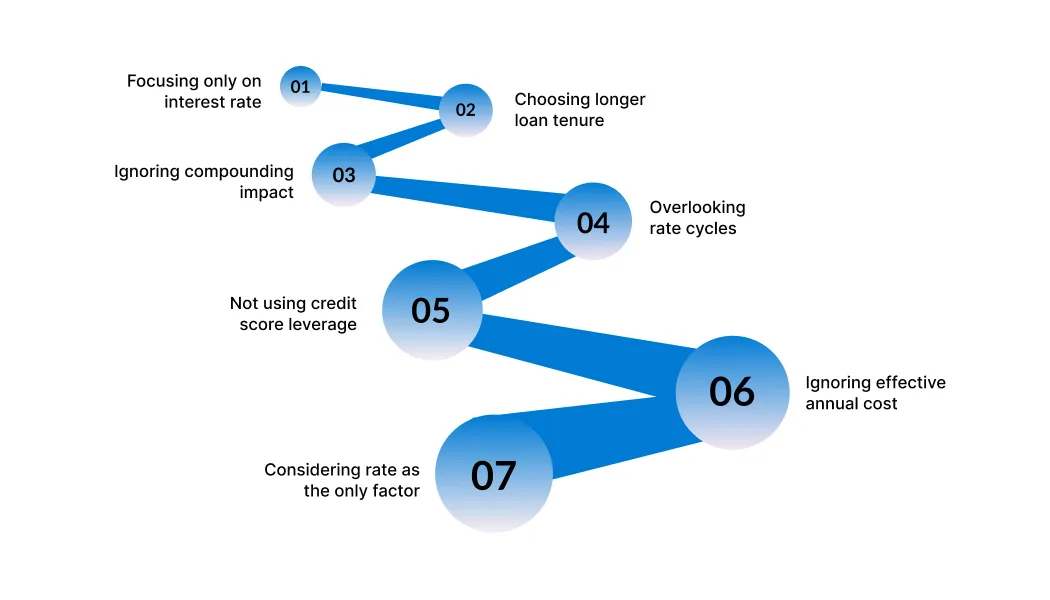

Common Mistakes People Make About Interest Rates

Interest rates influence far more than your EMI. They shape your cash flow, long-term wealth creation, and even financial stress levels. The problem is not that people ignore interest rates. The problem is that they misunderstand how deeply they affect total cost, timing, and flexibility.

Here are the most financially damaging mistakes, explained with deeper context.

Here are the most financially damaging mistakes, explained with deeper context.

1. Looking at the Rate Instead of the Total Cost

Risk: A 10% loan and an 11% loan may not be dramatically different on paper. But when fees, compounding frequency, tenure, and repayment structure are added, the actual repayment gap can become substantial.

Many borrowers compare only the interest percentage without calculating the total repayment across the full tenure. Over longer loans, such as home loans, even a small difference of 0.5% can translate into lakhs over time.

Mitigation: Always calculate the total repayment amount, not just EMI. Ask for an amortisation schedule and compare the full loan costs across lenders.

2. Choosing Longer Tenure for Comfort, Not Strategy

Risk: Lower EMI feels safer in the short term, especially for salaried professionals managing monthly commitments. However, extending tenure increases the number of interest cycles, which significantly raises total interest paid.

This trade-off is often emotional rather than strategic. People optimise for short-term comfort instead of long-term cost efficiency.

Mitigation: Select the shortest tenure that keeps your EMI within 30 to 40% of your monthly income. If income increases later, consider partial prepayments to reduce total interest.

3. Underestimating the Power of Compounding

Risk: In investments, compounding builds wealth. In debt, it accelerates liability. Many borrowers assume interest is calculated only on principal, but with compounding, unpaid interest gets added to the outstanding balance.

This is especially dangerous with credit cards and short-term high-interest loans, where carrying a balance multiplies the cost quickly.

Mitigation: Avoid revolving balances. Pay dues in full whenever possible. Understand whether interest is compounded monthly, quarterly, or annually.

4. Ignoring Interest Rate Cycles

Risk: Interest rates move in cycles depending on inflation, economic growth, and central bank policies. Borrowers often choose floating rates without understanding whether rates are likely to rise or fall.

In a rising rate environment, floating rate borrowers may see EMIs increase or tenure extend automatically.

Mitigation: Evaluate the broader economic environment before selecting fixed or floating rates. If stability is a priority, fixed rates provide predictability. If rates are expected to decline, floating rates may offer savings.

5. Overlooking Credit Score Negotiation Power

Risk: Many borrowers accept the first interest rate offered, unaware that their credit score directly influences pricing. A strong credit profile gives you leverage to negotiate better terms.

Even a small improvement in the credit score category can reduce interest costs meaningfully over long tenures.

Mitigation: Check your credit score before applying. Reduce credit utilisation, clear overdue balances, and avoid multiple hard enquiries before major loan applications.

6. Ignoring the Effective Annual Cost

Risk: Some lenders quote monthly interest rates, which appear lower when seen in isolation. A 2% monthly rate may sound manageable, but annualised, it represents a significantly higher cost.

Without converting to annual terms, borrowers may underestimate the real financial burden.

Mitigation: Always convert monthly rates into annual percentage terms. Compare offers on the same annual basis for clarity.

7. Assuming Interest Rate Is the Only Decision Factor

Risk: Interest rate is important, but flexibility, prepayment terms, processing time, and repayment structure also affect overall value. A slightly higher rate with flexible repayment may be more practical for someone with a variable income.

Mitigation: Evaluate interest rate alongside tenure flexibility, prepayment options, transparency, and lender credibility.

Read More: How to Achieve a Perfect 900 CIBIL Score?

Short on Cash? How Pocketly Supports Smart, Short-Term Borrowing

Short-term credit exists to solve a very specific problem in personal finance: timing gaps. Income comes on a fixed date, but expenses rarely wait. Medical bills, utility payments, urgent travel, or unexpected repairs can create pressure even when your overall finances are stable.

Pocketly operates within this short-term lending space by offering structured, transparent access to small-ticket loans designed for temporary liquidity needs, not long-term debt.

As a digital lending platform, Pocketly supports users by:

- Offering controlled loan amounts between ₹1,000 and ₹25,000, helping borrowers address immediate cash gaps without taking on unnecessary financial exposure.

- Providing a fully digital experience with quick KYC-based verification, eliminating branch visits and reducing processing delays.

- Maintaining clear pricing, with interest starting from 2% per month and processing fees generally ranging from 1% to 8%, so borrowers understand the cost upfront.

- Enabling fast bank transfers after approval, which is especially useful for time-sensitive expenses such as EMIs, bills, or urgent payments

- Allowing flexible repayment structures, making it easier to align instalments with existing monthly commitments

By prioritising accessibility, transparency, and controlled borrowing limits, Pocketly fits into the financial services ecosystem as a practical liquidity tool. It is structured to support responsible short-term borrowing rather than encourage prolonged dependency on credit.

Conclusion

Understanding interest rates is one of the smartest steps you can take to strengthen your financial decisions in 2026. By knowing how rates affect loans, savings, and investments, you can make informed choices that save money, reduce stress, and grow your wealth over time.

Interest rate awareness isn’t about fear; it’s about control. It helps you borrow responsibly, invest wisely, and plan your financial future with confidence.

When you face financial decisions affected by fluctuating rates, tools and calculators can help you compare options and make choices that align with your goals.

Stay ahead of your finances. Keep an eye on interest rates, plan strategically, and make every rupee work smarter for you. Download the Pocketly app today on [Android] or [iOS] to access funds instantly and keep your finances steady, no matter what comes your way.

FAQs

1. What are interest rates?

Interest rates represent the cost of borrowing money or the return you earn on savings and investments, usually expressed as a percentage of the principal amount.

2. How do interest rates affect my loans?

Higher interest rates increase your monthly repayments and the total amount you pay back over time, while lower rates reduce borrowing costs. This applies to personal loans, home loans, and credit cards.

3. What is the difference between fixed and floating interest rates?

A fixed rate stays the same throughout the loan tenure, offering predictability, while a floating rate changes based on market conditions, which can make your repayments higher or lower over time.

4. How are interest rates decided in India?

The Reserve Bank of India (RBI) sets key rates like the repo and reverse repo, and interest rates are also influenced by inflation, economic growth, market demand, and the borrower’s credit profile.

5. How do interest rates impact my savings and investments?

Higher interest rates mean better returns on fixed deposits, savings accounts, and bonds. Lower rates reduce the growth of interest-based investments.