Even with a steady income, financial gaps can show up at the worst possible time. A bill due before payday, an unexpected medical expense, or an urgent payment can quickly disrupt your plans. When there is no immediate access to funds, it often leads to stress, delayed payments, or using savings meant for more important goals.

The problem is not just about how much you earn, but how easily you can access money when timing does not work in your favour. Without a reliable fallback, even short-term disruptions can create unnecessary financial pressure.

Advance loans, commonly known as salary advance loans in India, are designed to solve this exact problem. They give you quick access to funds before your next paycheck, helping you manage urgent needs without long-term financial impact. In this blog, you will understand how they work, their benefits, risks, and when to use them.

Key Takeaways

-

Advance loans (or salary advance loans) are short-term loans to cover urgent expenses like bills, rent, medical emergencies, or unexpected repairs before your next salary.

-

The process is fast and digital: apply online, complete basic KYC, get approved within minutes, and receive funds directly in your bank account.

-

Loan amounts are small, and repayment is short-term, usually via your next salary or a fixed short tenure, with interest starting around 2% per month.

-

Use advance loans only for urgent, necessary expenses; avoid borrowing for shopping, lifestyle upgrades, or non-essential spending.

-

Responsible use helps manage short-term gaps safely, protect your credit score, and build disciplined repayment habits.

What Are Advance Loans (Salary Advance Loans)?

Advance loans are short-term loans that help you get money quickly before your next salary arrives. They are ideal for urgent expenses like bills, rent, or unexpected medical costs, especially for people who don’t want to wait for payday or dip into their savings.

In India, these loans are most commonly offered as salary advance loans, designed specifically for salaried individuals who sometimes face cash gaps between pay cycles.

Key Features:

-

Quick repayment: Usually repaid with your next salary or over a short few-week period.

-

Small amounts: Enough to cover urgent needs, not big-ticket purchases.

-

Fast approval: Apply online with basic personal and income details; funds are sent directly to your bank account.

-

Minimal documentation: Typically requires PAN, Aadhaar, and bank account info only.

How It Works in Real Life:

-

You have a ₹5,000 bill due a week before payday → take an advance loan and repay after your salary.

-

Rent is due, but your salary is delayed → borrow a small amount to avoid late fees.

-

Unexpected medical expenses arise mid-month → use an advance loan instead of breaking your savings.

In simple words, an advance loan is like borrowing a small sum today to cover urgent needs, with repayment planned when your next paycheck arrives. It’s designed to be fast, convenient, and safe when used responsibly.

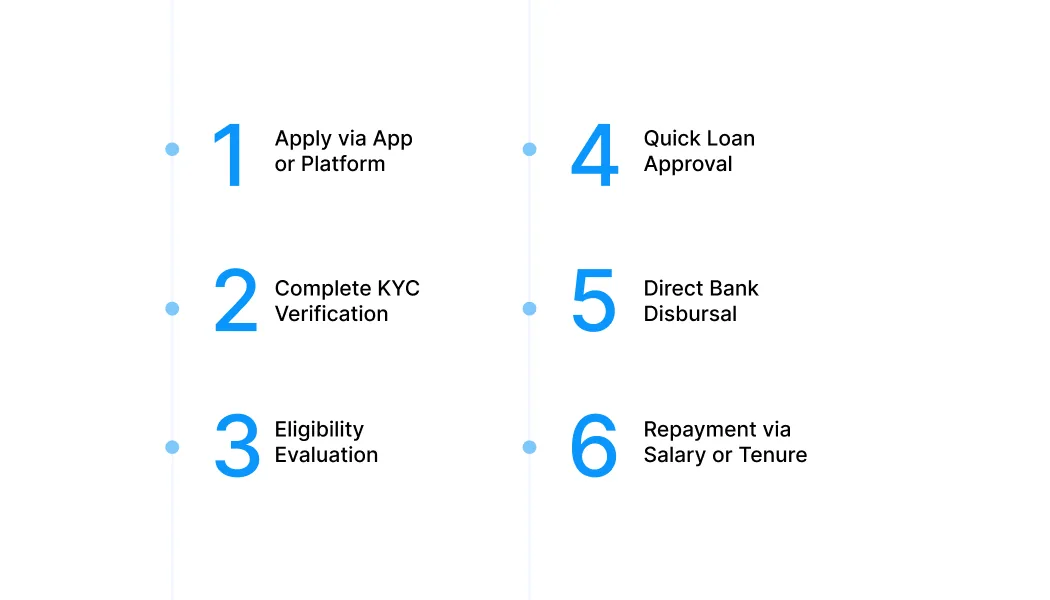

How Do Advance Loans Work? Step-by-Step Process

Advance loans are built around a fast and predictable process, where you apply, get approved, receive funds, and repay within a short cycle. Each step is designed to minimise delays and give you quick access to money.

Step-by-Step Process

-

Apply through a mobile app or lender platform: You start by entering basic details like your name, job, income, and bank account. This helps the lender understand your profile.

-

Complete KYC and submit basic details: KYC means verifying your identity. You usually need to upload documents like your PAN card and Aadhaar card so the lender knows you are a genuine user.

-

Lender evaluates income and eligibility: The lender checks how much you earn and whether you will be able to repay the loan on time. Based on this, they decide how much money you can borrow.

-

Loan gets approved within minutes or hours: If everything looks good, your loan is approved quickly. You don’t have to wait for days like traditional bank loans.

-

Funds are credited directly to your bank account: Once approved, the money is sent straight to your bank account, so you can use it immediately for your needs.

-

Repayment happens via your next salary or a fixed tenure: You repay the loan after your salary is credited or in small instalments over a short period, depending on what you choose.

Cover unexpected costs without worry. Get ₹1,000–₹25,000 instantly through Pocketly and keep payments on track. Apply in minutes and handle urgent bills stress-free.

Also Read: How to Manage Monthly Expenses Smartly in 2025

Key Features of Advance Loans That Make Them Suitable for Short-Term Needs

Advance loans are defined by a few key factors, such as quick access, small amounts, and short repayment cycles. Here’s a clear breakdown.

|

Feature |

What It Means |

|

Quick access to funds |

The loan is approved and credited within a short time, often within minutes or hours. |

|

Small loan amounts |

Borrow a limited amount based on your income, suitable for short-term needs. |

|

Short repayment period |

Repayment is usually done by the next salary or within a few weeks to months. |

|

No collateral required |

No need to pledge assets like gold, property, or investments. |

|

Minimal documentation |

Only basic documents like PAN, Aadhaar, and bank details are required. |

|

Fully digital process |

Application, approval, and tracking are done online without branch visits. |

When Advance Loans Make Sense and When You Should Avoid Them

Advance loans are useful when you need money immediately but know you can repay it soon, usually from your next salary. They are meant to handle short-term gaps, not ongoing financial needs.

Best Used For

-

Medical emergencies: Health-related expenses often cannot wait, even if the amount is small. An advance loan helps you access treatment or medicines immediately without delaying care.

-

Urgent bills or rent: Fixed payments like rent, electricity, or EMIs come with strict due dates. If your salary is delayed or a few days away, an advance loan helps you avoid penalties and maintain a clean payment record.

-

Temporary cash flow shortages: Some months bring extra expenses that go beyond your usual budget. An advance loan can help you manage this one-time gap without disturbing your savings or routine spending.

-

Unexpected travel or essential repairs: Situations like urgent travel or fixing a phone, laptop, or vehicle can affect your daily life or work. Advance loans provide quick support so these disruptions don’t impact your routine.

Avoid Using For

-

Shopping or lifestyle upgrades: Buying things on impulse or during sales may feel justified, but repayment can reduce your next month’s financial flexibility.

-

Non-essential spending: If the expense can be delayed without consequences, it’s better to wait and pay from your own income instead of borrowing.

Quick Rule to Remember: If the expense is urgent, necessary, and repayable from your next income, an advance loan can make sense. If not, it’s better to avoid borrowing.

Wondering how to manage your loan payments without stress? A repayment schedule shows exactly when and how much you need to pay. Learn why it’s important and how to calculate it easily, even as a beginner.

5 Common Advance Loan Mistakes That Increase Your Repayment Burden

Advance loans can be helpful in urgent situations, but using them without planning can lead to financial pressure. Since these loans are short-term and quick to access, small mistakes can create bigger problems over time.

Here are the key risks to be aware of:

1. Borrowing Without a Repayment Plan

Risk: Quick approvals can make borrowing feel effortless, but without a clear repayment plan, it can disrupt your entire salary cycle. When repayment is due, you may struggle to manage regular expenses like rent, food, or bills.

How to Avoid: Before taking a loan, mentally allocate your next salary. Ensure that after repayment, you still have enough left for essential expenses.

2. Short Repayment Timelines

Risk: Advance loans are designed to be repaid quickly, often by your next salary. This short window can create pressure, especially if multiple expenses are already lined up for that month.

How to Avoid: Check your upcoming expenses before borrowing. If your next salary is already committed, consider reducing the loan amount or avoiding borrowing altogether.

3. Falling Into a Borrowing Cycle

Risk: If you start relying on advance loans for regular expenses, it can turn into a cycle where each month’s salary is partly used to repay the previous loan. Over time, this reduces your financial flexibility.

How to Avoid: Use advance loans only for unexpected or urgent situations. For recurring gaps, focus on budgeting better or building a small emergency buffer.

4. Underestimating the Total Cost

Risk: While the loan amount may seem small, interest rates and processing fees can increase the total repayment. Ignoring these costs can lead to paying more than expected for a short-term loan.

How to Avoid: Always look at the total amount you need to repay, not just the amount you receive. This helps you make a more informed decision.

5. Choosing the Wrong Platform

Risk: Some apps may have unclear terms, hidden charges, or poor customer support. This can create issues during repayment or lead to unexpected costs.

How to Avoid: Choose platforms that clearly mention interest rates, fees, and repayment terms. Check user reviews and ensure the app is secure and reliable.

Also Read: Top 10 Tips to Spend and Save Money Wisely

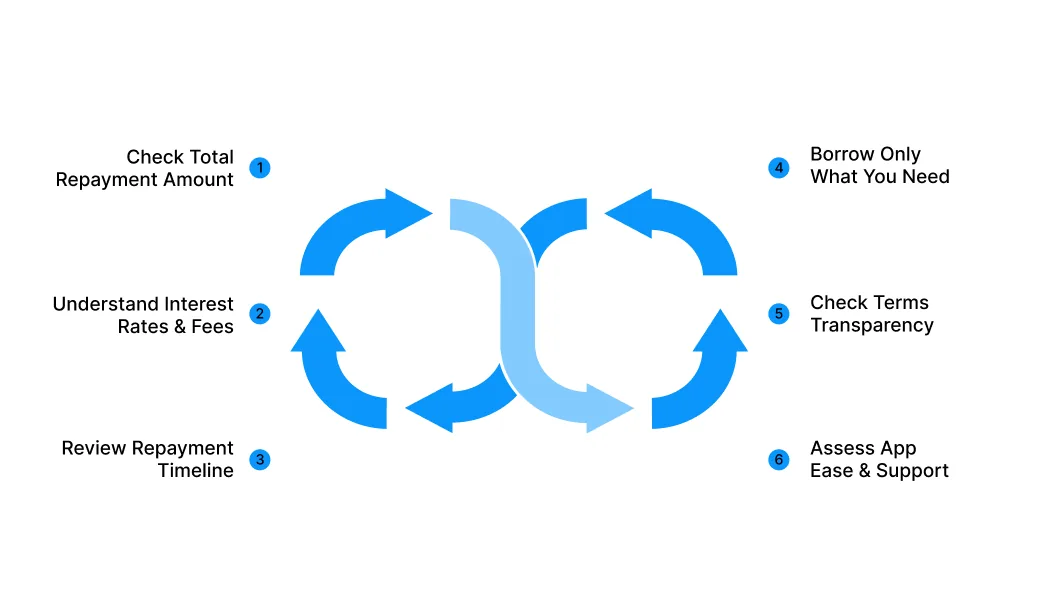

How to Choose the Right Advance Loan Without Overpaying or Over-Borrowing

Not all advance loans are the same. Choosing the right one can save you money and reduce repayment stress, especially if you’re applying for the first time.

1. Salary Advance Loans

If you need a small amount quickly, salary advance loans are usually the fastest option. They let you borrow a portion of your next salary, often with minimal paperwork.

For example, if you need ₹5,000 for an urgent bill, a salary advance could cover it instantly. Just make sure your employer or the platform doesn’t charge extra hidden fees, so you’re not paying more than you need.

2. Personal Advance Loans

Banks and NBFCs offer personal loans that can cover larger expenses, like medical emergencies or travel. The amount is higher than a salary advance, but interest rates can vary.

For instance, borrowing ₹20,000 for a medical bill from Bank A may cost you ₹22,000 in a month, while Bank B charges only ₹21,000. Always compare the total repayment before choosing a lender.

3. Digital App-Based Loans

Fintech apps give quick access to money with minimal paperwork. Funds can appear in your account the same day, making it convenient for sudden needs.

For example, if you forgot to pay a utility bill and the due date is today, an app-based loan can save you from late fees. Just check the interest rate and any hidden charges first.

4. Overdraft or Credit Line Loans

Some banks let you borrow from a pre-approved overdraft or credit line linked to your account. You pay interest only on what you use, which makes it flexible.

For example, if your overdraft limit is ₹10,000 and you only use ₹3,000, you’re charged interest on ₹3,000, not ₹10,000. It’s great for occasional urgent expenses, but avoid using the full limit unless necessary.

Want to close your loan but not sure how to start? A loan closure application is a simple request to pay off your loan completely. Learn the easy steps to write and submit one without any confusion.

New to Advance Loans? Pocketly Makes It Simple

Managing unexpected expenses can be stressful, especially if you’re new to loans. Pocketly offers a simple, beginner-friendly way to get small, short-term loans without confusing processes or hidden charges.

Here’s why Pocketly works well for first-time users in India:

-

Borrow small and stay in control: Loan amounts range from ₹1,000 to ₹25,000, letting you cover urgent needs without taking on too much debt.

-

No credit history needed: You don’t need a credit score, collateral, or guarantor. Pocketly is ideal for students, employees, or anyone new to borrowing.

-

Fast approval and instant transfer: A quick KYC-based process ensures speedy approval, with funds credited directly to your bank account.

-

Build responsible repayment habits: Repaying on time helps you develop financial discipline, preparing you for bigger loans or credit products in the future.

-

Flexible repayment options: Choose a plan that fits your monthly income so you can repay comfortably without stress.

-

Transparent pricing: Interest starts from 2% per month, with processing fees between 1% and 8%. Everything is clear upfront—no hidden charges.

-

24/7 app access: Apply, track, and manage your loan anytime from the Pocketly app, giving you complete control and convenience.

In emergencies, Pocketly serves as a reliable safety net. Loan amounts from ₹1,000 to ₹25,000, instant approvals, and flexible repayment options ensure you can manage urgent expenses without disrupting your broader financial goals.

Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. What are advance loans in India?

Advance loans are short-term loans that help you cover urgent expenses when cash is tight. They are meant for temporary needs like paying bills, handling medical emergencies, or fixing unexpected problems.

2. Are advance loans the same as salary advance loans?

Not always. Salary advance loans are a type of advance loan where repayment is automatically deducted from your next salary. Other advance loans may have different repayment options and are available to a wider range of borrowers.

3. How fast can I get an advance loan?

Advance loans are designed to be fast. With online applications and basic KYC verification, approval can happen within minutes or a few hours, and the funds are usually credited directly to your bank account.

4. What interest rates can I expect?

Rates vary by lender, but small, short-term loans typically start at around 2% per month. Always check for processing fees or additional charges before borrowing.

5. Will taking an advance loan affect my credit score?

Yes, it can. Paying on time helps maintain or improve your credit score, while missed or late payments can hurt it. Borrow only what you can repay to stay safe.