Finding it hard to build a credit history in India? Even with a steady income, getting approved for loans or premium cards can feel impossible when your credit score is low or nonexistent. Every declined application only adds to the stress, making you feel stuck financially.

This struggle isn’t just inconvenient; it can slow down your financial growth and limit opportunities for better interest rates or bigger purchases in the future.

The solution is simpler than you think. By choosing the right credit cards designed for beginners, you can start building your credit history, improve your score, and unlock a world of financial flexibility.

In this blog, we’ll break down the best credit cards in India that help newcomers and young professionals establish a strong credit profile while managing spending responsibly.

Key Takeaways

-

No credit history? Secured and beginner-friendly credit cards can help you start building your CIBIL score from scratch.

-

The best cards in India, especially FD-backed options, offer easy approval and low-risk entry for first-time users.

-

Your credit score improves with simple habits: pay on time, keep usage below 30%, and stay consistent.

-

Avoid common mistakes like late payments, high utilisation, or applying for multiple cards at once

-

If you’re not eligible for cards yet, tools like Pocketly can help you build financial discipline and bridge gaps while starting your credit journey.

What is a Credit Score and How Does it Work in India?

A credit score is a three-digit number that reflects how well you manage borrowing and repayment. Banks and lenders use it to decide whether to approve loans, credit cards, or even offer better interest rates.

Here’s what it looks like in practice:

-

You take a ₹10,000 personal loan and repay it on time → your score improves

-

You miss a credit card payment of ₹1,000 → your score drops

-

You keep your credit utilisation below 30% → lenders see you as responsible

In India, scores usually range from 300 to 900. A score above 750 is considered excellent, while a score below 600 may make approvals harder.

In simple terms, your credit score is like a financial report card. The better your behaviour, the easier it is to access credit and financial opportunities.

The Real Benefits of a Credit Builder Card for First-Time Users

Starting your credit journey in India can feel tricky, but a credit builder card is designed to make it simple. These cards focus on helping you establish a positive credit history rather than offering fancy rewards.

What Makes a Card Ideal for Building Credit

Look for these features when picking a card:

-

Beginner-Friendly Approval: Low eligibility barriers make it easier for first-time credit users to get approved.

-

Secured with Fixed Deposit: Many banks offer secured cards backed by an FD, which ensures faster approval and lower risk.

-

Manageable Credit Limits: Modest limits let you use the card responsibly, proving your repayment reliability to credit bureaus.

Secured vs Unsecured Cards

Knowing the difference helps you choose wisely:

|

Type |

How It Works |

Who It’s Best For |

Key Advantage |

|

Secured |

Backed by your fixed deposit |

First-time credit users |

Easier approval and a safer way to build credit |

|

Unsecured |

No collateral, relies on income/credit history |

Users with some credit history |

Higher limits, rewards, and perks once approved |

Using the right card responsibly, paying bills on time and keeping utilisation low can steadily improve your CIBIL score, opening doors to better cards and loans in the future.

Top 5 Credit Cards to Build Credit in India

Not all cards are created equal when it comes to building your credit score. Here’s a curated list of some of the best options available for beginners in India, including both secured and beginner-friendly unsecured cards:

1. SBM ZET Credit Card

SBM ZET is a secured, FD-backed credit card designed for first-time credit users. With a low fixed deposit requirement of around ₹5,000 and a lifetime fee waiver, it’s ideal for beginners who want to start building credit without a big upfront investment.

For example, you can use this card for small monthly expenses like groceries or online subscriptions. Paying the full statement on time ensures your activity is reported to credit bureaus, gradually improving your score from zero.

Best for: beginners looking to start a credit history with minimal FD

Features

-

FD-backed with low entry requirement (~₹5,000)

-

Lifetime free with no annual fee

-

Digital onboarding and instant card issuance

-

Basic rewards on select spends

Pros

-

Very low investment to start a credit

-

Simple and fast digital application

-

Helps build a credit score from scratch

Cons

-

Limited rewards and perks

-

Low credit limit

Tips for building credit:

-

Use for predictable monthly payments only

-

Always pay full dues on time

-

Keep utilisation under 30% to maximise credit score growth

2. SBI Unnati Credit Card

SBI Unnati is a secured card backed by a fixed deposit of around ₹25,000. It has no annual fee and is widely accepted across India, making it a solid choice for beginners who want to start their credit journey responsibly.

For example, using this card for recurring bills like electricity, mobile recharge, or groceries while paying in full each month helps create a strong payment history.

Best for: first-time users who want a widely accepted starter card

Features

-

Secured against FD (~₹25,000)

-

No annual fee

-

Easy eligibility and broad acceptance

-

Basic rewards on select categories

Pros

-

Builds credit history safely

-

Low-risk entry for first-time users

-

Simple application process

Cons

-

Credit limit depends on the FD amount

-

Minimal reward program

Tips for building credit:

-

Use for regular, recurring payments

-

Pay full bill each month to avoid interest

-

Monitor statements to ensure timely payments

3. Kotak 811 #DreamDifferent Credit Card

Kotak 811 #DreamDifferent is an FD-backed secured card that comes with rewards and wide merchant acceptance. Its flexible usage makes it suitable for users without prior credit history, while also incentivising spending responsibly.

For example, using this card for online shopping or utility bills and paying in full helps establish your credit profile while also earning cashback or reward points.

Best for: users starting credit with the benefit of rewards

Features

-

FD-backed secured credit card

-

Cashback and reward points

-

Widely accepted across India

-

Easy online management

Pros

-

Rewards incentivise responsible usage

-

Helps build credit from zero

-

Flexible online management

Cons

-

FD requirements can be higher than entry-level cards

-

Limited high-value perks

Tips for building credit:

-

Focus on regular monthly payments

-

Avoid overspending to maximise score benefits

-

Track rewards as an additional incentive to maintain usage

4. IDFC FIRST WoW / FIRST EA₹N Cards

These are beginner-friendly FD-backed secured cards with very low FD entry (~₹5,000) and zero or low fees. They also offer cashback or reward programmes, which encourage regular usage and help build a positive credit history.

For example, using the card for grocery shopping or subscriptions and clearing the dues every month improves your credit record and helps you maintain a disciplined spending pattern.

Best for: beginners wanting low FD, minimal fees, and rewards

Features

-

Secured with low FD (~₹5,000)

-

Zero or low annual fees

-

Cashback or reward options

-

Easy online tracking and statement management

Pros

-

Low barrier to entry

-

Encourages responsible spending

-

A rewards programme motivates consistent usage

Cons

-

Limited credit limit due to the FD cap

-

Rewards may be modest

Tips for building credit:

-

Set automated payments to avoid missed bills

-

Use for recurring essentials

-

Keep credit utilisation low for faster score growth

5. OneCard Secured Variant

OneCard Secured is an app-first, FD-backed card with flexible FD tiers and instant virtual issuance. Perfect for digital-first users, it allows you to start building credit quickly and manage the card entirely via a mobile app.

For example, depositing ₹10,000 as an FD gives you a matching credit limit. Using it for online subscriptions or grocery shopping while paying in full ensures your positive payment history is recorded.

Best for: tech-savvy beginners wanting a digital-first credit experience

Features

-

App-driven, instant virtual card issuance

-

FD-backed with flexible tiers

-

Full mobile app management

-

Track spending and payments in real-time

Pros

-

Quick setup and instant virtual card

-

Flexible FD requirement

-

Fully app-based, convenient for digital users

Cons

-

Requires smartphone and app familiarity

-

Limited offline rewards

Tips for building credit:

-

Treat it like cash: spend only what you can repay

-

Always pay in full to avoid interest

-

Regularly monitor statements through the app

6. Other FD-Backed Beginner Cards (Top Picks)

Other options include the PhonePe Wish Card and DCB Niyo Global, which are secured cards with low FD entry and basic rewards. These cards are ideal if you want simple, low-risk credit-building options with minimal investment.

For example, a ₹5,000 FD can give you access to a credit card for essential monthly expenses. By paying in full and consistently, you gradually build a positive credit history and improve your CIBIL score.

Best for: first-time credit users seeking minimal investment options

Features

-

Low FD entry (~₹5,000)

-

Beginner-focused secured cards

-

Basic rewards or cashback

-

Easy digital management

Pros

-

Very low barrier to entry

-

Helps build credit without heavy risk

-

Suitable for small, consistent expenses

Cons

-

Limited perks and reward options

-

Credit limit capped by FD

Tips for building credit:

-

Focus on recurring, manageable expenses

-

Pay full dues monthly

-

Monitor credit reports periodically

A credit score is a three-digit number that reflects how reliably you borrow and repay money

How to Use Credit Builder Cards to Boost Your Score

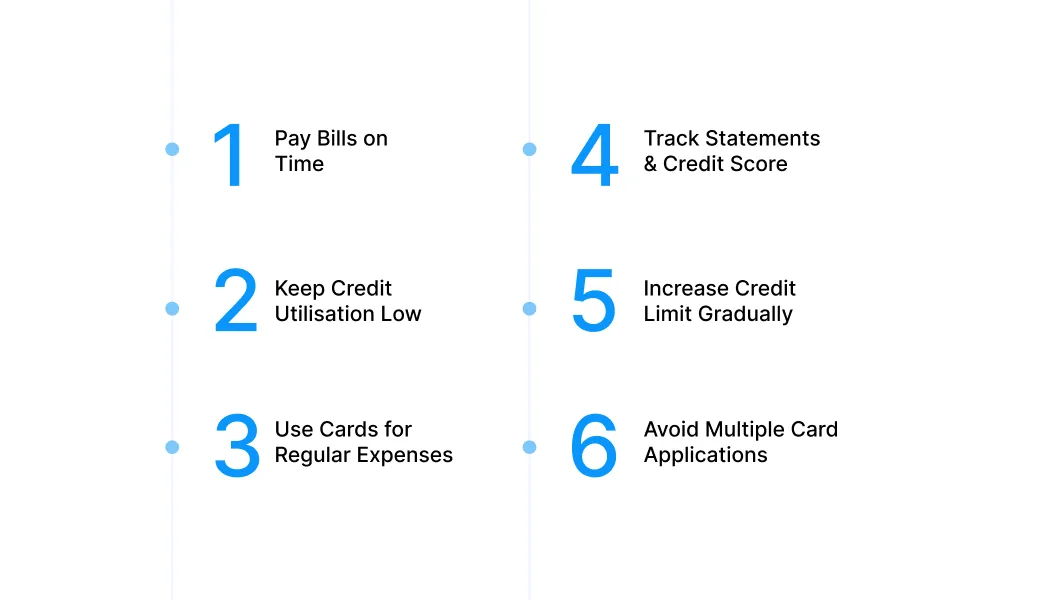

Building a strong credit score requires responsible card usage, not just ownership. Even secured or beginner-friendly cards can improve your score when you pay bills on time, keep utilisation low, and maintain consistent activity. Here’s how:

1. Pay Your Bills on Time, Every Time

Late payments are the fastest way to hurt your credit score. Even if you spend responsibly, a single missed payment can take months to recover from.

For example, if your SBI Unnati Credit Card bill of ₹2,500 is due on the 5th of every month, setting up an automated payment or a calendar reminder ensures you never miss it. Over time, this consistent track record of on-time payments builds your CIBIL score steadily and shows lenders you are reliable.

2. Keep Credit Utilisation Low

Credit utilisation, the percentage of your available limit you use, is a major factor in your score. Staying below 30% of your limit signals that you’re in control of your finances.

For instance, with a Kotak 811 #DreamDifferent Credit Card limit of ₹10,000, aim to spend no more than ₹3,000 before the billing cycle ends. Even if you pay in full every month, keeping utilisation low demonstrates discipline and reduces the risk perceived by lenders.

3. Use the Card for Regular, Predictable Expenses

Using your card for small, recurring bills creates a steady record of responsible usage. This helps you build a positive payment history without overspending.

For example, put monthly subscriptions like Netflix, mobile bills, or electricity payments on your IDFC FIRST WoW card. This consistent activity is reported to credit bureaus, gradually improving your credit score over time.

4. Monitor Statements and Track Your Credit Score

Keeping an eye on your statements ensures there are no mistakes or fraudulent charges, and tracking your credit score helps measure progress.

For example, if your OneCard Secured variant shows an unexpected transaction, you can resolve it immediately instead of letting it hurt your credit history. Check your CIBIL or Experian score every few months to stay on top of your progress.

5. Gradually Increase Your Credit Limit

A higher credit limit, combined with disciplined spending, can lower your utilisation ratio and improve your score. But only request increases after showing consistent on-time payments.

For example, after using SBM ZET responsibly for 8–12 months, you may be eligible for a higher limit. Spending the same amount now represents a lower utilisation, which looks better to lenders and helps your credit score.

6. Avoid Applying for Multiple Cards at Once

Every new card application triggers a hard inquiry, which can temporarily reduce your score. Focus on one or two cards first and build a solid history before applying for more.

For instance, start with SBI Unnati or Kotak 811 #DreamDifferent. Use it responsibly for a year before considering another card. Spacing out applications by 6–12 months protects your score from unnecessary drops.

Mistakes That Can Hurt Your Credit Building Efforts

Building a strong credit score is less about having a credit card and more about using it correctly over time. Small missteps, especially in the early stages, can slow down your progress significantly.

Here are the key mistakes to watch out for:

1. Missing Payments or Paying Late

Risk: Payment history carries the highest weight in your credit score. Even one delayed payment can stay on your credit report for months and reduce your credibility in the eyes of lenders.

How to Avoid: Pay your total amount due whenever possible, not just the minimum. Setting up auto-debit or payment reminders ensures consistency, especially if you’re new to managing credit.

2. High Credit Utilisation

Risk: Regularly using a large portion of your credit limit indicates dependency on credit, which lenders may interpret as financial risk. This can lower your score even if you pay on time.

How to Avoid: Try to keep your usage below 30% of your total limit. If your limit is low, consider making multiple payments within a billing cycle to maintain a lower reported balance.

3. Applying for Multiple Cards in a Short Time

Risk: Every application triggers a hard inquiry on your credit report. Too many inquiries within a short span can signal credit-hungry behaviour and temporarily reduce your score.

How to Avoid: Space out applications and only apply for cards you are likely to qualify for. Focus on building a solid history with one card before expanding.

4. Closing Your First Credit Card Too Early

Risk: The length of your credit history is an important factor in your score. Closing your oldest card shortens your credit history and can negatively impact your score.

How to Avoid: Keep your first card active, even if you don’t use it frequently. Small, occasional transactions can help maintain the account without unnecessary spending.

5. Ignoring Your Credit Report

Risk: Errors such as incorrect late payments or unrecognised accounts can go unnoticed and damage your score over time if not addressed.

How to Avoid: Check your credit report periodically through CIBIL or Experian. Early detection of discrepancies allows you to raise disputes and protect your score.

6. Treating Credit Limit as Extra Income

Risk: Spending based on your credit limit rather than your actual income can lead to repayment pressure and growing debt, which directly affects your credit profile.

How to Avoid: Use your credit card as a payment tool, not a borrowing tool. Only spend what you can comfortably repay within the billing cycle.

Tip: Credit building is driven by consistency. A single card used responsibly over time is far more effective than multiple cards used without discipline.

Also Read: Top 10 Tips to Spend and Save Money Wisely

New to Credit Cards? Pocketly Can Help You Get Started

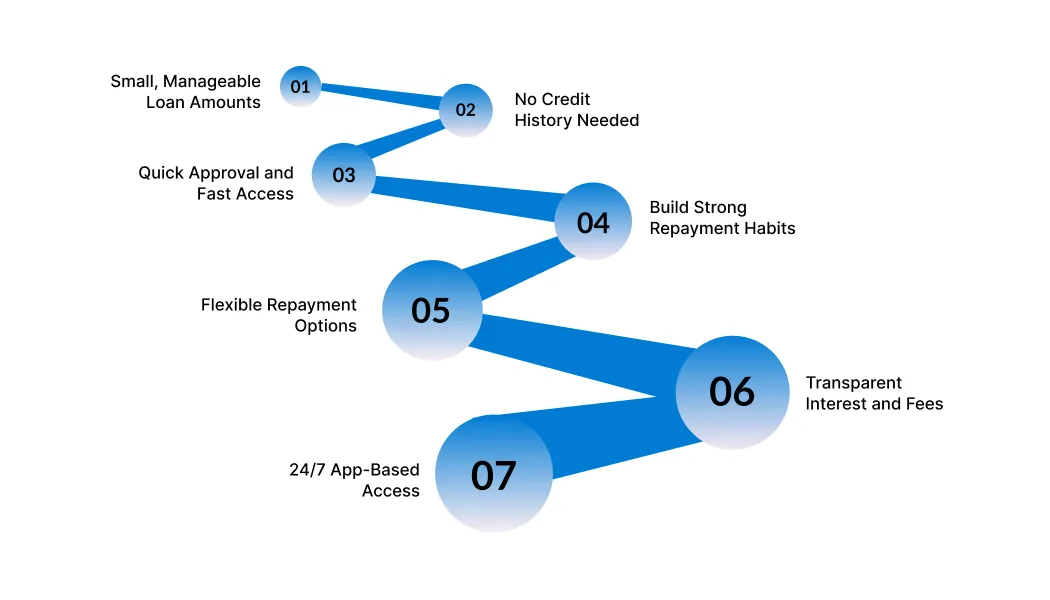

Building a credit score from scratch can feel confusing, especially when most credit cards require an existing history to get approved. If you are just starting out or facing rejections, Pocketly offers a simple way to begin your credit journey while managing short-term financial needs responsibly.

Here’s why Pocketly works for first-time credit users in India:

-

Borrow small and stay in control: Loan amounts range from ₹1,000 to ₹25,000, helping you start with manageable credit and avoid unnecessary debt.

-

No credit history required: You don’t need an existing credit score, collateral, or guarantor to get started, making it ideal for beginners.

-

Quick approval and instant access: A fast KYC-based process ensures quick decisions, with funds transferred directly to your bank account.

-

Build disciplined repayment habits: Regular, on-time repayments help you develop the financial behaviour needed to improve your credit profile over time.

-

Flexible repayment options: Choose a plan that fits your monthly budget so you can stay consistent without added pressure.

-

Transparent pricing: Interest starts from 2% per month, with processing fees between 1% and 8%, with no hidden charges.

-

24/7 app-based access: Apply, track, and manage everything directly through the Pocketly app, anytime and anywhere.

Pocketly helps you take the first step toward building financial credibility, giving you a practical foundation before moving on to credit cards and larger financial products.

Download Pocketly on iOS or Android to manage short-term financial gaps and stay on track with both your credit and financial goals.

FAQs

1. Which is the best credit card to build credit in India?

The best credit card to build credit in India is usually a secured (FD-backed) card like SBI Unnati or IDFC FIRST WoW, as they have easier approval and help establish a credit history quickly.

2. Can I get a credit card with no credit history in India?

Yes, you can get a credit card without any credit history by applying for a secured credit card against a fixed deposit. These cards are designed for beginners and first-time users.

3. How do credit cards help build your credit score?

Credit cards help build your score by creating a repayment history. Paying your bills on time, keeping usage low, and using the card regularly improve your credit profile over time.

4. What is a secured credit card and how does it work?

A secured credit card is issued against a fixed deposit. Your credit limit is usually equal to or a percentage of the FD amount, reducing risk for the lender while helping you build credit.

5. How long does it take to build a good credit score in India?

It typically takes 3 to 6 months to start building a credit score and around 6 to 12 months of consistent usage to see significant improvement.