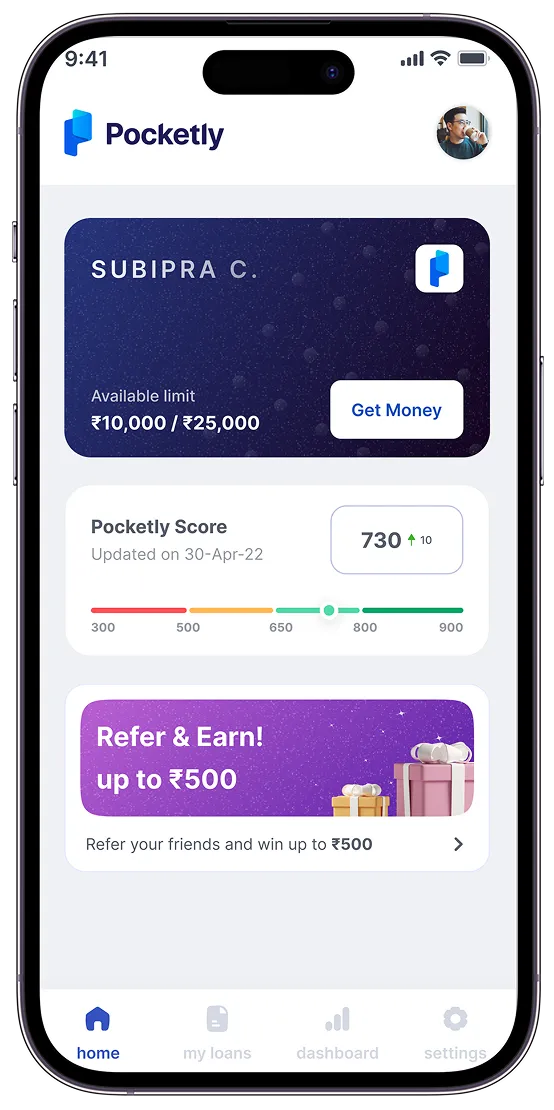

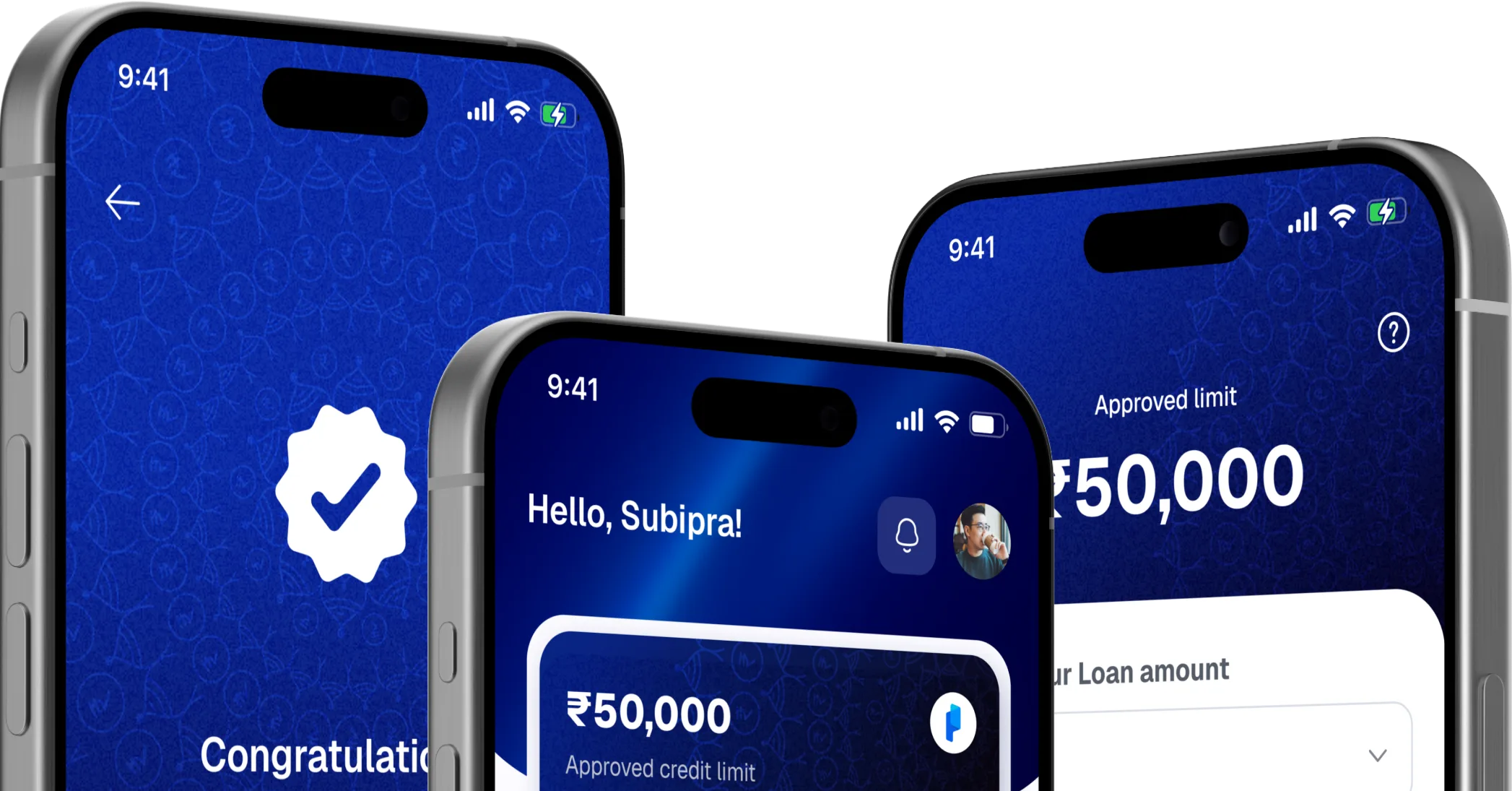

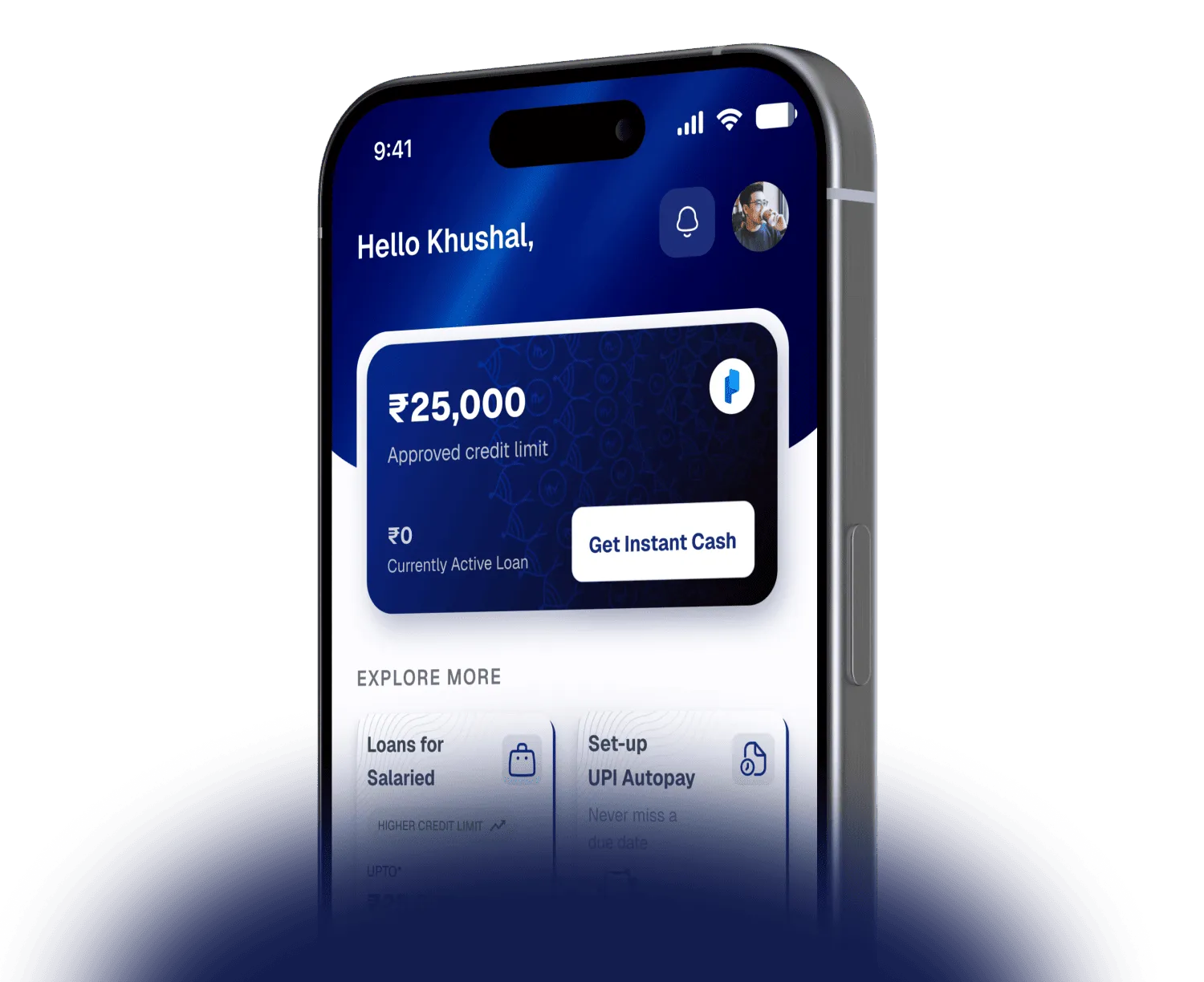

Get funds of up to

₹50,000 in just

few

minutes

100% Digital Journey

Minimum KYC

Direct Bank Transfer

Help Us With Your Details

Download Pocketly App now!