Ever wondered why half of your friends still haven’t bothered to check their credit score, even when applying for loans or credit cards feels like a monthly ritual? Nearly 50% of Indian consumers have never checked their credit score, leaving many unaware of how their financial behaviour shows up on official credit reports.

That lack of awareness creates a silent pain point: past defaults, settled accounts, or unresolved dues can sit on your report and silently influence loan approvals, interest rates, and borrowing opportunities, often without you even realising it.

The good news? There’s a lesser‑known credit report update called the CIBIL masking amount that can help make your credit profile cleaner and more appealing to lenders.

In this blog, you’ll learn what CIBIL masking amount really is, how it works in India, and how it can change the way banks see your credit history, without rewriting your entire financial past.

Key Takeaways

-

CIBIL Masking hides old mistakes on your credit report so lenders focus on your current repayment behaviour without deleting any history.

-

Settling past dues or written-off loans can improve loan approvals, interest rates, and access to credit.

-

Only your bank can update your CIBIL report; middlemen or credit repair agents cannot legally make changes.

-

NOCs confirm you’ve paid, but don’t automatically improve your credit score; always get official documentation.

-

Understanding the difference between masking and actively improving your credit helps you make smarter financial decisions.

What Is CIBIL Masking?

CIBIL masking is a technique to hide old or negative entries on your credit report so they don’t affect your chances of getting a loan or credit card. It doesn’t delete anything; it just marks some details as not important for lenders.

Think of it like this: if you had a small loan late payment three years ago, it may still show on your report. With masking, lenders can see your report but focus on your current financial behaviour, not old mistakes.

Here’s how it works:

-

Masked items stay on your report, but they are less visible to lenders.

-

It is not the same as deleting; transparency is still maintained.

-

Helps you improve your chances for new loans or cards.

-

Useful if you want to rebuild your credit history while showing your responsible money habits now.

In short, CIBIL masking helps your current credit picture look better without hiding the truth.

CIBIL Masking Benefits: How Settling Old Debts Boosts Your Borrowing Power

Fixing past debts can feel overwhelming, but CIBIL Masking makes it easier to clean up your credit history and regain control of your finances. Here’s what improving your credit report can do for you:

-

Remove Past Mistakes: Old defaults or unpaid debts no longer weigh down your credit report. By settling these, you can start fresh financially, making it easier to plan your future borrowing.

-

Boost Your Credit Score: Paying off old debts removes negative marks like “Settled” or “Written Off". A higher score shows lenders you are trustworthy, which can help in getting loans approved faster.

-

Faster Loan Processing: Banks are more confident in borrowers with a clean credit history. This means your home loan, car loan, or personal loan applications can be processed more quickly than before.

-

Better Deals on Loans: With a positive report, you can negotiate lower interest rates, smaller fees, and better repayment terms because lenders see you as less risky.

-

Higher Chances of Approval: Lenders are more likely to approve your loans or credit cards. This is particularly helpful for larger loans or urgent funding needs, reducing the stress of rejections.

-

Easier Access to Credit: A higher CIBIL score opens doors to more credit options, like credit cards, personal loans, or small business funding, often at more favourable terms.

-

Secure Your Financial Future: Over time, a higher score improves your overall financial credibility, giving you the confidence to plan bigger investments or borrow for important milestones without being held back by past mistakes.

-

Show Lenders You’re Responsible: Clearing past debts proves you manage money responsibly, which builds trust with banks and improves your reputation for future financial interactions.

Also Read: Meaning and Differences between CRIF and CIBIL Score

10 Steps to Successfully Apply for CIBIL Masking in India

Masking loans or credit card accounts on your CIBIL report can be tricky if not done correctly. Following a clear, step-by-step process ensures your request is handled smoothly. Use this easy process to avoid delays and mistakes.

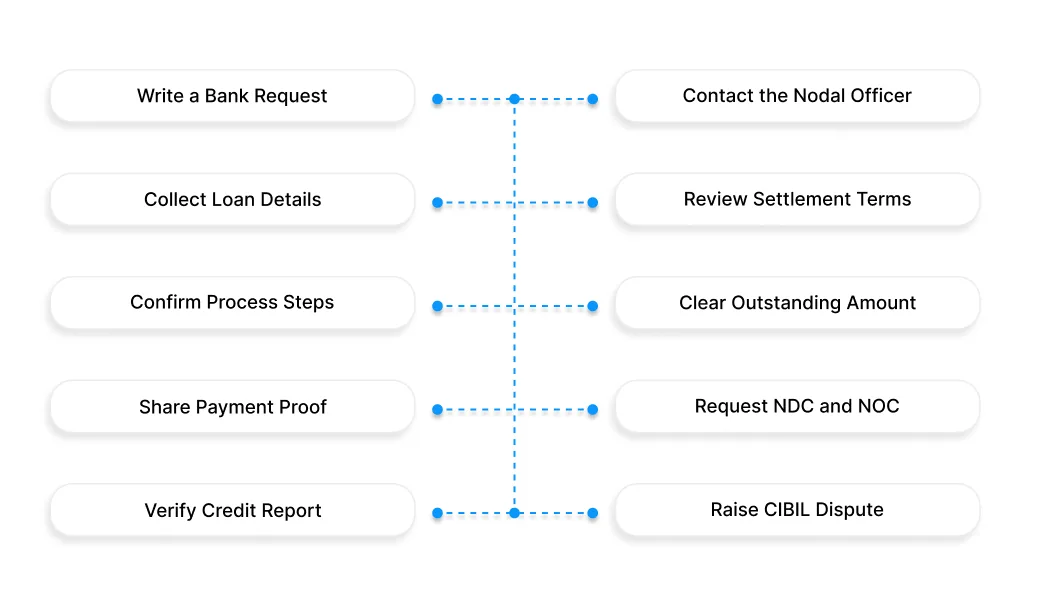

Step 1: Write a Precise Request to Your Bank

-

Draft a formal application mentioning the exact loan or credit account.

-

Include account numbers, dates, and a clear request for rectification.

-

Quick Tip: The more precise your details, the faster your bank can process them.

Step 2: Contact the Bank’s Nodal Officer

-

Reach out directly to the Nodal Officer or Nodal Office Desk.

-

They handle specialised requests like CIBIL Masking efficiently.

Step 3: Collect Loan and Outstanding Details

-

The bank provides loan history, outstanding balance, and payment schedule.

-

Note the due date to avoid delays in processing your masking request.

Step 4: Review Settlement Terms Carefully

-

Some banks waive penalties or revise settlements to cover only interest.

-

Check if the terms match your financial situation.

-

Ask questions if anything is unclear.

Step 5: Confirm Agreement and Clarify the Process

-

Reply to the bank with consent. Confirm:

-

Exact steps of the masking process

-

Expected timeline for update

-

How the account will appear post-masking

-

Step 6: Clear the Outstanding Amount

-

Make the payment as agreed.

-

Obtain an official receipt as proof.

Step 7: Share Payment Proof and Request Processing

-

Send the receipt to the Nodal Officer.

-

Formally request them to initiate the CIBIL Masking process.

Step 8: Request No Dues Certificate (NDC) and NOC

-

Ensure the NOC clearly states the bank’s consent for masking.

-

Avoid disclaimers like “CIBIL Masking not guaranteed.”

Step 9: Follow Up and Verify Your Credit Report

-

Stay in touch with the bank until confirmation.

-

Download your CIBIL report and check that the masked account shows correctly.

Step 10: Raise a Dispute with CIBIL if Needed

-

If updates are delayed or incorrect, file a dispute on CIBIL’s official website.

-

CIBIL will coordinate with your bank to resolve the issue.

Avoid messing up your CIBIL score due to late payments. Pocketly gives ₹1,000–₹25,000 instantly to cover urgent EMIs or bills, helping you stay on top of your credit. Apply in minutes and protect your financial reputation.

Masking Your CIBIL Report vs Actively Improving Your Score: What You Must Know

CIBIL masking and credit score improvement are often mentioned together, but they serve very different purposes. Knowing how each works helps you take the right steps toward healthier credit. Here’s how they differ:

|

Feature |

CIBIL Masking |

Credit Score Improvement |

|

Purpose |

Temporarily hides negative entries from your CIBIL report |

Improves your actual creditworthiness over time |

|

Effect on Credit Score |

No real impact; score remains the same |

Gradually increases score by showing responsible credit behaviour |

|

Duration |

Usually 6–12 months, depending on lender/bureau policies |

Permanent, as long as you maintain good credit habits |

|

Eligibility |

Can be requested if you have recent negative marks or errors |

Anyone with a CIBIL report; improvement depends on behaviour |

|

Impact on Loan Approvals |

May help get short-term approvals, but not guaranteed |

Strongly increases chances of loan/credit approvals |

|

Cost |

May involve a small fee via a bureau or service provider |

Free, as it relies on timely payments, EMIs, and low credit utilisation |

|

Limitations |

Only hides information; doesn’t remove errors or debts |

Requires time and consistent effort; results are gradual |

Also Read: 7 Smart Tips to Increase Your CIBIL Score Immediately

CIBIL Masking Mistakes Indians Often Make And How to Fix Them

Many people in India get misled by paying middlemen, trusting verbal promises, or thinking an NOC fixes their credit, only to lose money or harm their CIBIL score. Here’s what you must know:

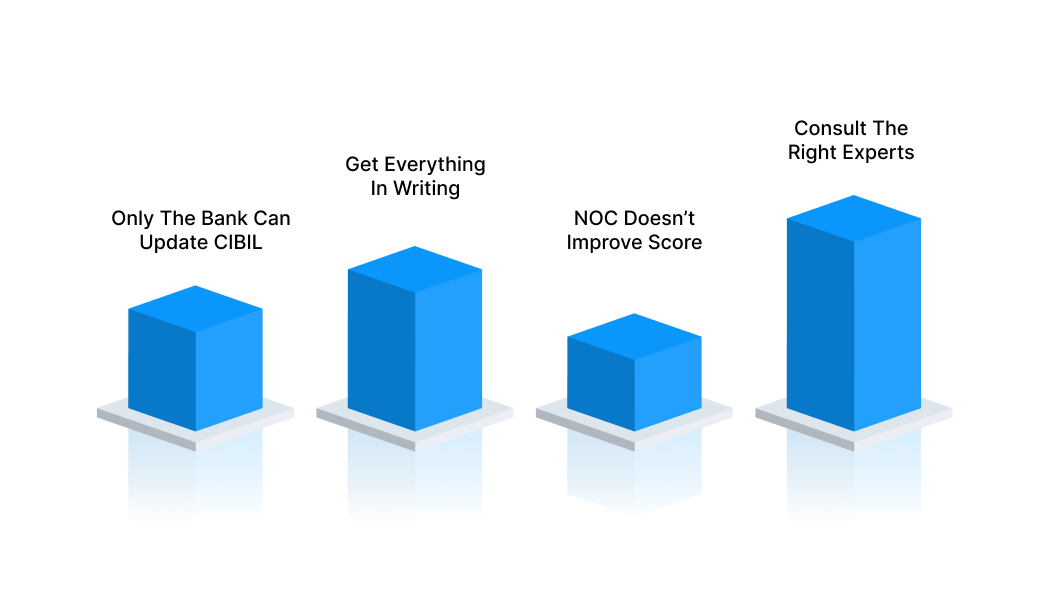

1. Only Your Bank Can Update Your Credit Report

Your original lender is the only legal authority to mask or correct entries on your CIBIL report.

Common mistakes to avoid:

-

Paying third-party agents, recovery firms, or law offices for “fast fixes".

-

Assuming extra payments guarantee a higher credit score.

Why does it happen?

-

Recovery agencies often buy written-off loans at a discount (e.g., ₹45,000 for ₹12,000). Any extra you pay is their profit, not a credit improvement.

-

No one besides your bank can directly update your CIBIL report.

Pro Tip: Skip middlemen. Always deal with your lender directly and ask exactly what they can legally update.

2. Get Everything in Writing

Verbal promises, even from bank staff, aren’t legally binding. Without proper documentation, you risk:

-

Paying money without receiving credit improvements.

-

Losing proof in case of disputes or delays.

Best practices:

-

Request confirmation on official letterhead or a verified email from a senior officer (nodal officer or credit resolution team).

-

Avoid relying on branch-level verbal commitments.

Pro Tip: No written confirmation? Don’t pay. Protect yourself with formal documentation.

3. NOC Doesn’t Mean Better Credit Score

Many borrowers think a No Objection Certificate (NOC) will automatically improve their CIBIL score. This is false.

What you need to know:

-

An NOC only confirms that you no longer owe money; it doesn’t guarantee account status updates on CIBIL.

-

Settled or written-off accounts may remain marked as such even after a payment.

-

Paying third parties for an NOC without checking reporting details can lead to no improvement in your score.

Actionable tip:

-

Confirm exactly how the account will be reported to CIBIL post-settlement.

-

Get this clarification in writing before making any payments.

Pro Tip: Treat NOCs as proof of payment, not a score booster.

4. Consult the Right Experts Before Acting

Your credit score affects loans, credit cards, and future financial opportunities. Misguided advice can cause serious setbacks.

Mistakes borrowers often make:

-

Following advice from recovery agents, online ads, or unverified “credit repair” services.

-

Negotiating settlements without understanding CIBIL reporting rules.

Safe approach:

-

Discuss directly with your bank about your credit reporting post-settlement.

-

Consult a certified financial advisor if unsure.

-

Ask clear questions: Will the account be marked ‘settled’ or ‘paid in full’? How long before it reflects on CIBIL?

Pro Tip: Treat your credit score like a valuable asset and handle it carefully with expert guidance.

Stay on Top of Payments Even During Tight Months with Pocketly

Even when you plan carefully, unexpected bills, EMIs, or timing gaps in your salary can throw your finances off balance. Missing a payment can hurt your credit score or delay your journey to a better financial profile.

Pocketly acts as a smart, fast, and flexible financial cushion to help you manage short-term cash gaps without stress.

Here’s how Pocketly makes life easier for you:

-

Pay on time, every time: Avoid late fees, penalties, or a hit to your CIBIL score, even if your salary comes late or an expense pops up unexpectedly.

-

Borrow just what you need: Access ₹1,000–₹25,000 instantly, enough to cover urgent bills or EMIs without taking on extra debt.

-

Lightning-fast digital process: Apply and get money transferred directly to your bank account in minutes, with no long forms or paperwork.

-

No strict credit requirements: You don’t need a perfect credit history, collateral, or a guarantor to get started. Pocketly is built for real-world emergencies.

-

Flexible repayment options: Choose a schedule that aligns with your income cycle, so repayments are easy and stress-free.

-

Transparent costs upfront: Interest starts at 2%/month, and processing fees range from 1%–8%. No hidden charges or surprises.

-

All-in-one convenience: Track, manage, and repay directly from the app, keeping your finances organised and under control.

With Pocketly, you get a reliable partner to handle urgent payments, protect your credit health, and reduce financial stress without breaking your savings or monthly planning.

Get Pocketly on iOS or Android and stay in control; never let sudden cash needs affect your budget or loan payments.

FAQs

1. What is a CIBIL Masking Amount?

It’s the portion of a settled or written-off loan that the lender marks as masked on your credit report. The account stays, but the masked amount stops affecting your credit score, giving lenders a clearer view of your current financial health.

2. Who can request masking?

Only your bank or lender can request it. You can ask them to initiate, but CIBIL does not accept requests directly from borrowers.

3. How does masking affect my score?

Masking doesn’t instantly raise your score. It simply removes the negative impact of settled dues, letting your active accounts and timely repayments weigh more positively over time.

4. How long does masking take?

Usually, 2–8 weeks after the lender submits the request. Delays happen if documents are missing or the lender doesn’t follow up.

5. Can freelancers or irregular earners benefit?

Yes. Masking clears past negatives, making it easier to get loans or credit cards, even with inconsistent income.

6. Why is masking important in India?

Even small settled defaults can impact approvals and interest rates. Masking ensures cleared debts don’t overshadow your responsible credit behaviour, boosting your chances for loans and better terms.