An urgent expense rarely gives you time to compare options. A medical bill, a repair, or a last-minute payment can force a quick decision between a personal loan and a credit cash advance.

At first glance, both seem similar. You get access to money and plan to repay it soon. The difference becomes clear only when you look at the cost. Interest, fees, and repayment structure can vary significantly, and the wrong choice can increase your total repayment more than expected.

This is where most people get caught off guard.

In this blog, we break down the cost comparison between a personal loan and a credit cash advance, explain how each option works, and help you choose the one that fits your situation without adding unnecessary financial pressure.

Key Takeaways

-

A personal loan usually offers more predictable borrowing costs because repayment is structured through fixed EMIs and known tenure.

-

A credit cash advance may feel faster in the moment, but immediate interest and upfront fees can make it much more expensive very quickly.

-

The smartest comparison is not speed alone, but total repayment, including interest, fees, and how long the amount remains unpaid.

-

The right option depends on urgency, amount needed, and repayment certainty, not just which one is easier to access.

-

For smaller short-term gaps, choosing a proportionate borrowing option can help you avoid both long-term loan pressure and high cash advance costs.

What Is a Personal Loan vs Credit Cash Advance

Both options provide access to funds, but they work very differently in terms of structure, cost, and repayment.

A personal loan is a structured borrowing option where you receive a fixed amount and repay it over time through EMIs. It is typically used for planned or slightly larger expenses where repayment needs to be spread out.

A credit cash advance, on the other hand, allows you to withdraw cash directly using your credit card limit. It is designed for immediate, short-term needs where speed matters more than cost.

Here is the key difference:

-

Personal loan works as a structured plan: You borrow a fixed amount, know your EMI in advance, and repay over a defined period.

-

Cash advance works as instant access to credit: You withdraw money quickly, but the cost starts building immediately without a structured repayment plan.

For example, if you need ₹5,000 urgently, a cash advance may give you instant access. But if you need a larger amount and want a predictable repayment, a personal loan may be more suitable.

Understanding this basic difference is important before comparing the actual cost, which is where the real impact shows.

Also Read: Personal Loan Rejection Reasons: 7 Common Causes & Fixes in 2026

How Personal Loan and Cash Advance Costs Build Differently

The biggest difference between a personal loan and a credit cash advance is not how quickly you get the money, but how the cost builds over time.

Even for the same amount, the total repayment can vary depending on how interest and fees are applied.

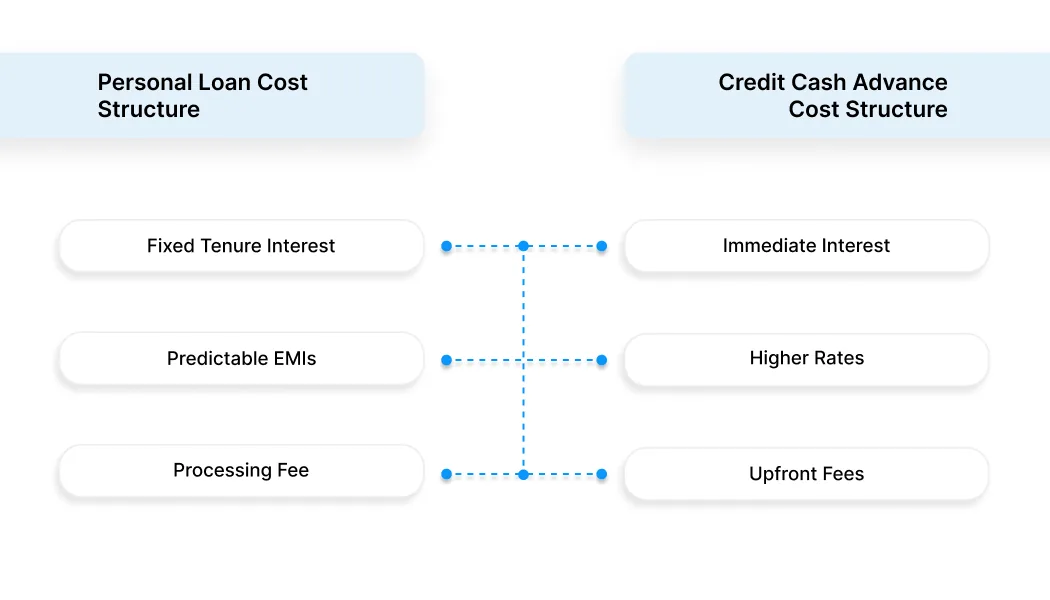

Personal Loan Cost Structure

-

Interest is spread across a fixed tenure: You repay the loan through EMIs, where interest is calculated over the loan period and divided into monthly payments.

-

Costs are more predictable: The EMI, tenure, and total repayment are usually known upfront, which makes planning easier.

-

One-time processing fee may apply: A small fee is charged at the start, which is either deducted from the loan amount or added to the total cost.

Result: The cost builds gradually, and repayment remains structured.

Credit Cash Advance Cost Structure

-

Interest starts immediately: Unlike regular credit card usage, there is usually no grace period. Interest begins from the day you withdraw cash.

-

Higher interest rates apply: Cash advances often carry higher rates compared to personal loans, increasing the cost quickly.

-

Additional upfront fees: A percentage of the withdrawn amount is charged as a cash advance fee.

Result: The cost builds faster and becomes expensive if not repaid quickly.

Key Difference

-

Personal loan → structured, predictable cost over time

-

Cash advance → immediate, fast-growing cost from day one

This difference is what makes cost comparison critical before choosing between the two.

Also Read: Student Loan vs Personal Loan: Which One Should You Choose?

Why Credit Cash Advances Become Expensive So Quickly

A credit cash advance is designed for speed, not cost efficiency. While it solves an immediate need, the way charges are applied can make it one of the most expensive borrowing options if not handled carefully.

Here is why the cost increases quickly:

-

Interest starts from day one: There is usually no interest-free period. Charges begin as soon as the cash is withdrawn, increasing the total cost even for short usage.

-

Higher interest rates compared to loans: Cash advances often carry higher rates than personal loans, which makes the cost build faster over time.

-

Upfront withdrawal fees: A percentage of the amount is charged as a fee at the time of withdrawal, reducing the actual amount you receive or increasing the total payable.

-

No structured repayment plan: Without fixed EMIs, it becomes easier to delay repayment, which adds more interest and increases the overall burden.

-

Compounding effect of delays: Even small delays in repayment can lead to a noticeable increase in total cost because interest continues to accumulate.

For example, a borrower may take a small cash advance expecting to repay it quickly. However, if repayment is delayed by even a few weeks, the combined impact of interest and fees can make the final amount higher than expected.

This is why cash advances should be used with a clear repayment timeline, not as a flexible or long-term borrowing option.

If the cost of a cash advance feels too high for a small expense, a short-term option like Pocketly can help you manage the gap without daily interest building up.

When a Personal Loan Makes More Sense Than a Cash Advance

Choosing between a personal loan and a credit cash advance depends on your situation, not just availability. The right option is the one that aligns with your urgency, amount required, and repayment clarity.

Choose a Personal Loan when:

-

The amount required is relatively higher: Personal loans are better suited for larger expenses where repayment needs to be spread over time.

-

You need predictable repayment: Fixed EMIs and defined tenure make it easier to plan your monthly budget.

-

You want better control over total cost: Compared to cash advances, personal loans generally offer more structured and manageable costs.

-

You have time for approval and processing: If the expense is not immediate, waiting for a structured loan may be more practical.

Choose a Cash Advance when:

-

The need is urgent and immediate: Cash advances provide quick access to funds when timing is critical.

-

The amount required is small: They are typically used for short-term, limited needs.

-

You have clear repayment visibility: If you can repay within a very short period, the impact of high cost may be limited.

-

You cannot wait for loan approval: In situations where delay creates additional problems, speed becomes the priority.

Key takeaway: A personal loan is better for structured, planned borrowing, while a cash advance works only for immediate, short-term needs where repayment is certain.

Making the right choice depends on balancing urgency with total cost.

If your requirement is small and time-sensitive, choosing a proportionate option like Pocketly may be more practical than either a full personal loan or a high-cost cash advance.

Also Read: RBI Guidelines For Personal Loan Lending In India

Hidden Cost Risks in Personal Loan vs Cash Advance

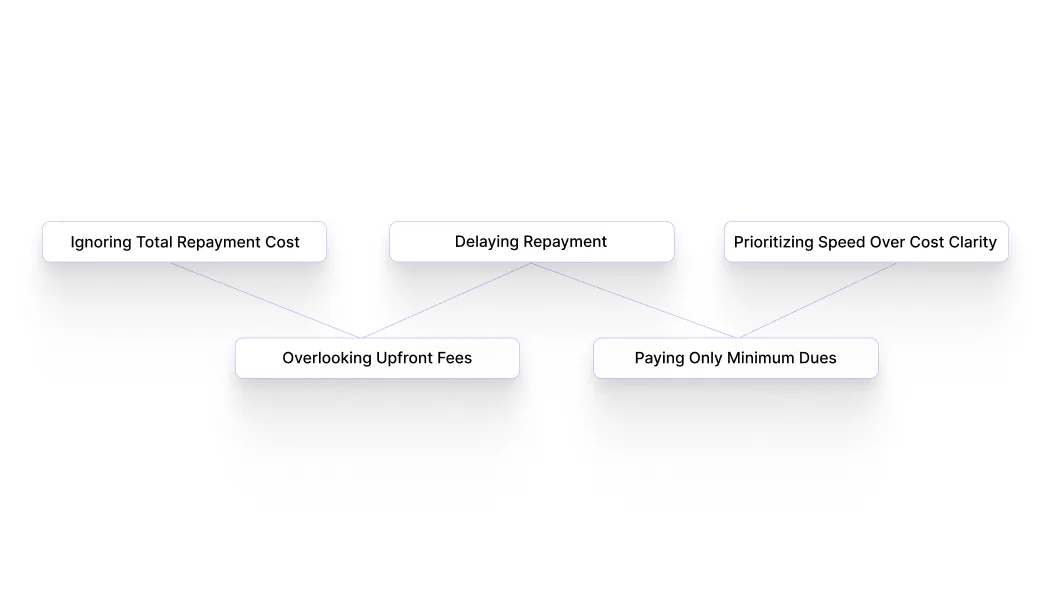

The biggest mistake in choosing between a personal loan and a cash advance is focusing only on access to money, not the total cost. Many charges are either overlooked or misunderstood, which increases the repayment burden later.

Here are the most common risks:

-

Looking only at interest rate, not total repayment: A lower rate may still lead to higher overall cost if fees and tenure are not considered.

-

Ignoring upfront and service fees: Cash advance fees and loan processing charges can increase the effective cost beyond what is expected.

-

Delaying repayment without realising the impact: In cash advances, even a short delay can significantly increase interest. In loans, longer tenure increases total payable.

-

Paying only partial amounts or minimum dues: This can extend the repayment cycle and increase the total cost due to continued interest accumulation.

-

Choosing speed over cost clarity: Urgent decisions often lead to selecting the quickest option without understanding the financial impact.

For example, a borrower may choose a cash advance for speed without checking how interest is applied. If repayment is delayed, the final amount can be much higher than expected.

Avoiding these risks starts with one simple step: always check the full repayment amount before choosing any borrowing option.

Also Read: Getting Instant Small Personal Loans Online With Loan Apps in India

What Matters More Than Choosing the Cheapest Option

The decision between a personal loan and a cash advance is not only about which one has a lower cost on paper. The better choice depends on how well it fits your situation and repayment ability.

Focusing only on “cheapest” can lead to the wrong decision.

Here are the factors that matter more:

-

Urgency of the expense: If the need is immediate, speed may matter more than comparing minor cost differences.

-

Clarity of repayment timeline: Knowing exactly when and how you will repay is more important than choosing a slightly lower rate.

-

Total cost over time: The full repayment amount, including fees and interest, gives a clearer picture than just the headline rate.

-

Impact on monthly cash flow: The option you choose should not disrupt essential expenses or create additional financial stress.

-

Size of the requirement: Smaller needs may not require a structured loan, while larger amounts may not be suitable for high-cost short-term borrowing.

For example, choosing a cheaper option without considering repayment ability can still lead to higher financial pressure. On the other hand, selecting a slightly higher-cost option that fits your timeline may be more manageable.

The right choice is not just the cheapest one, but the one that keeps your finances stable and predictable.

Also Read: How Long Does it Take to Build Credit Using a Credit Card?

Get Speed Without Cash Advance-Level Cost with Pocketly

The real problem in this comparison is that both options can feel imperfect. A personal loan gives more structure, but it may not always match the urgency of a short-term expense. A credit cash advance is faster, but the cost can rise quickly from the moment the money is withdrawn.

That leaves a gap in the middle. Sometimes, you do not need a long repayment cycle. You also do not want the immediate cost pressure that comes with a cash advance.

This is where Pocketly fits more naturally.

Pocketly is a digital lending platform working with RBI-registered NBFCs. It is suited to short-term borrowing needs where the amount is smaller, the requirement is urgent, and cost visibility matters before you proceed.

Why it can work better in this situation:

-

It gives a middle-ground option: If a personal loan feels too large and a cash advance feels too expensive, a smaller short-term borrowing option can be more proportionate.

-

It helps you borrow for the actual gap, not beyond it: Loan amounts range from ₹1,000 to ₹25,000, which can make more sense for urgent but limited expenses.

-

The cost can be reviewed upfront: Interest starts from 2% per month, with processing fees between 1% and 8%, depending on your profile and loan amount.

-

It avoids collateral and branch-heavy processes: The application is digital, which helps when the need is immediate, and you want fewer steps.

-

It is better suited to short-term repayment thinking: Instead of treating the expense like a long-term loan decision, it helps address a smaller financial gap with a clearer borrowing frame.

If a short-term gap is stretching your budget, Pocketly offers small-ticket loans with transparent pricing, no collateral, and a fully digital process. You can check your eligibility and get started by downloading the Pocketly app on Android or iOS.

FAQs

Q: Is a personal loan cheaper than a credit card cash advance?

A: In most cases, a personal loan is cheaper because it has lower interest rates and structured repayment. Cash advances carry higher rates and start charging interest immediately.

Q: How much interest is charged on a credit card cash advance?

A: Interest rates on cash advances are usually higher than regular card purchases and apply from day one. The exact rate depends on the card issuer and your profile.

Q: Do cash advances have additional fees apart from interest?

A: Yes, most cash advances include a withdrawal fee charged as a percentage of the amount. These fees increase the total cost along with interest.

Q: Why do cash advances become expensive so quickly?

A: Interest starts immediately and is charged at a higher rate than regular borrowing. Combined with fees, even short delays can increase the total repayment significantly.

Q: Does taking a personal loan affect my credit score?

A: Yes, it can impact your credit score depending on how you manage repayments. Timely EMI payments can improve your score, while missed payments can lower it.