Getting a personal loan rejected can feel like a sudden roadblock, especially when you need the funds for emergencies, travel, or important life goals. It leaves you frustrated, stressed, and unsure about what went wrong.

Most rejections aren’t random; they usually happen because of gaps in your credit history, income, documentation, or eligibility. Without knowing the exact reasons, you might keep applying blindly, which can hurt your credit score and waste both time and effort.

Understanding why lenders deny personal loans is the first step to turning a rejection into approval. By identifying the common pitfalls and learning how to address them, you can strengthen your application, avoid repeated denials, and secure the funds you need with confidence.

In this blog, we break down the most frequent personal loan rejection reasons and share practical steps to increase your chances of getting approved.

TL;DR

- Personal loan rejections usually happen due to low credit scores, high debt-to-income ratios, unstable income, or incomplete documents, not randomly.

- Lenders assess your repayment ability through credit history, income stability, debt obligations, and employment continuity.

- Common pitfalls include recent defaults, multiple simultaneous applications, and missing or inaccurate paperwork.

- To improve approval chances: boost credit score, reduce debt, maintain a stable income, organise documents, and space out applications.

- Short-term solutions like Pocketly provide quick funds while you strengthen your profile, helping manage urgent expenses without repeated rejections.

How Personal Loan Applications Are Evaluated?

When you apply for a personal loan, lenders follow a structured process to assess your repayment ability. Understanding this can help you avoid common pitfalls and improve your chances of approval.

- Credit Score: Indicates your repayment history. A high score shows reliability, while a low score signals risk.

- Income & Employment: Lenders check if your income is stable and sufficient to cover EMIs alongside existing expenses. Permanent jobs or long-term contracts strengthen your profile.

- Debt-to-Income Ratio: Shows how much of your income is already committed to debt. A high ratio suggests over-leverage and increases rejection risk.

- Financial Track Record: Past defaults, late payments, or ongoing loans are red flags. Lenders prefer consistent financial responsibility.

Why Applications Get Rejected: Lenders aim to minimise risk. Even a single weak factor, such as a low credit score, high debt, or unstable income, can lead to rejection.

Typical Approval Workflow

- Submit the application with personal, income, and document details.

- The lender conducts automated/manual credit assessments using bureau scores and internal criteria.

- Income and employment verification.

- Risk assessment: weighing credit history, existing obligations, and repayment capacity.

- Decision: approved, approved with modifications, or rejected.

Understanding this evaluation process helps you strengthen your profile, like improving your credit score, lowering debt, or documenting stable income, before applying.

Also Read: Get Debt Consolidation Loan Online: How it Works

7 Common Reasons for Personal Loan Rejection

Understanding why lenders reject personal loan applications helps you address weak points in advance. Here are the most frequent reasons:

Understanding why lenders reject personal loan applications helps you address weak points in advance. Here are the most frequent reasons:

1. Low Credit Score

A credit score is a numerical snapshot of your financial reliability, reflecting how consistently you’ve repaid past loans or credit. Lenders use this score to predict your likelihood of timely repayment. A low score signals a higher risk, often resulting in rejection.

For example, if your credit score is 580 while the lender’s minimum is 700, your application may be denied even with a steady income. Beyond just numbers, lenders also consider your credit mix: having only credit cards or only small loans can be a negative indicator.

To improve your score, pay off outstanding dues, maintain timely EMIs, and avoid maxing out credit cards. Over a few months, these steps can significantly enhance your approval chances.

2. High Debt-to-Income Ratio

Lenders carefully examine how much of your income is already committed to loan repayments. A high debt-to-income (DTI) ratio suggests limited capacity to take on new debt.

For instance, if your monthly income is ₹50,000 and ₹35,000 goes toward EMIs, adding another personal loan may be considered risky. This not only affects approval chances but may also limit the loan amount offered.

To improve your DTI ratio, consider paying down existing loans, consolidating debts, or applying for smaller loan amounts that better align with your repayment capacity.

3. Irregular or Unstable Income

A steady and predictable income reassures lenders of your repayment ability. Freelancers, contractual employees, or people with seasonal income may face rejection because lenders cannot reliably forecast their cash flow.

For example, a freelancer earning ₹60,000 in one month but only ₹25,000 in another may be flagged as high-risk. Lenders may request additional documentation such as tax returns, bank statements, or proof of consistent contracts.

Demonstrating multiple income streams or maintaining a buffer in your bank account can help lenders feel confident about your ability to repay.

4. Incomplete or Incorrect Documentation

Even if you meet all eligibility criteria, errors in your documentation can lead to rejection. Lenders need accurate proof of income, identity, residence, and employment.

For example, submitting a rent agreement instead of a utility bill for address proof, or missing recent salary slips, can cause unnecessary delays or outright rejection. To avoid this, double-check document requirements, ensure all forms are legible, and keep digital copies ready for smooth submission.

Proper documentation can often be the difference between approval and rejection, especially for first-time borrowers.

5. Recent Defaults or Missed Payments

Your repayment history is a key factor in lenders’ risk assessment. Defaults, late payments, or unpaid loans reduce trust and signal potential future risk.

For example, missing an EMI six months ago may appear as a warning sign even if your current finances are stable. Lenders also look at how recently the default occurred, the amount, and whether it was a one-time lapse or repeated behaviour.

Addressing past defaults by clearing dues and maintaining consistent payments over several months demonstrates reliability and can improve future loan approval chances.

6. Multiple Recent Loan Applications

Applying for multiple loans within a short timeframe can signal financial distress. Lenders may interpret this as desperation or excessive borrowing and reject new applications accordingly.

For example, submitting three personal loan applications in one month could indicate that you are struggling to manage finances, even if your income and credit score are good. To mitigate this, space out applications and avoid simultaneous submissions.

Also, maintain a clean credit inquiry history, as frequent enquiries negatively impact lenders’ perception of risk.

7. Age or Employment Criteria Not Met

Many lenders have strict eligibility rules based on age and employment tenure. Applications outside these parameters are often rejected regardless of income or creditworthiness.

For example, a candidate who just started a new job last week may be denied, even with a high salary. Lenders prefer borrowers with at least a few months of stable employment to ensure repayment capability.

Checking eligibility criteria before applying and waiting until you meet the minimum employment period can prevent unnecessary rejection and save time.

Also Read: How to Pay Off Loans Quickly and Easily

How to Improve Your Chances of Personal Loan Approval?

If your personal loan application has been rejected before, understanding why it happens and taking strategic steps can make all the difference. Here’s a detailed, step-by-step approach to strengthen your application and increase your chances of approval.

If your personal loan application has been rejected before, understanding why it happens and taking strategic steps can make all the difference. Here’s a detailed, step-by-step approach to strengthen your application and increase your chances of approval.

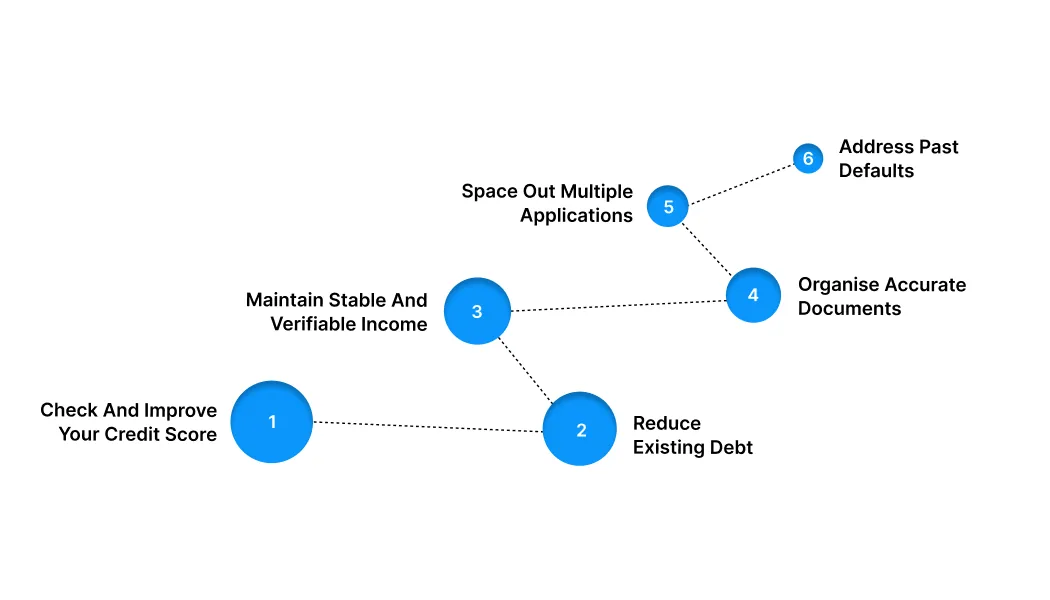

Step 1: Check and Improve Your Credit Score

Your credit score is the most crucial factor lenders look at. It reflects your past repayment behaviour and financial discipline. A higher score signals lower risk, making your application more appealing.

- Pay off overdue bills and EMIs: Even small unpaid amounts can drag your score down. Prioritise clearing them to demonstrate responsibility.

- Maintain low credit utilisation: Keep your credit card usage below 30% of your limit. High utilisation suggests you rely heavily on borrowed money.

- Avoid multiple credit enquiries: Each hard inquiry slightly lowers your score. Apply strategically to maintain stability.

- Monitor regularly: Use free apps or bank dashboards to track your score and spot discrepancies.

Example: If your score is 650, paying off pending dues and maintaining on-time payments for 3–4 months could raise it above 700. This immediately improves your approval chances and may also reduce interest rates.

Outcome: A strong credit score reassures lenders of your reliability and boosts your approval probability.

Step 2: Reduce Existing Debt

Lenders consider your debt-to-income (DTI) ratio to see how much of your income is already committed. A lower DTI shows that you can comfortably manage new loan repayments.

- Pay off smaller loans first: Reducing outstanding balances quickly improves your DTI.

- Consolidate multiple EMIs: This lowers monthly obligations and simplifies repayment.

- Avoid new debts: Taking on additional loans or credit cards increases your DTI and reduces approval chances.

Example: Suppose your monthly income is ₹50,000, and your EMIs total ₹25,000. Your DTI is 50%, which is high for most lenders. Paying off one EMI of ₹5,000 reduces your DTI to 40%, making you more eligible.

Outcome: Lowering debt levels signals financial stability and makes lenders confident in approving your personal loan.

Step 3: Maintain Stable and Verifiable Income

Lenders want assurance that you can repay the loan consistently. Documented income stability reduces perceived risk.

- Salaried individuals: Keep salary slips, Form 16, and bank statements updated and accessible.

- Freelancers/self-employed: Maintain IT returns, invoices, and bank statements to demonstrate consistent earnings.

- Track all income sources: Side hustles, freelance work, or rental income can boost eligibility if documented properly.

Example: A freelancer earning ₹40,000 per month can show six months of consistent bank deposits and invoices. This reassures lenders even without a formal salary.

Outcome: A stable and documented income strengthens your profile and increases the likelihood of approval.

Step 4: Organise Accurate Documents

Even minor errors in documentation can lead to automatic rejection. Lenders want clear, consistent, and valid proofs.

- Verify personal information: Ensure PAN, Aadhaar, and bank account details match perfectly.

- Update documents: Expired proofs or outdated statements may trigger delays or rejection.

- Scan or photograph clearly: Blurry images in digital submissions can cause application denial.

Example: Submitting only two months of bank statements may appear insufficient. Providing six months of well-organised statements proves consistent income and financial stability.

Outcome: Accurate and complete documents accelerate approval and demonstrate professionalism.

Step 5: Space Out Multiple Applications

Applying to multiple lenders simultaneously can signal financial stress. Each hard inquiry may slightly reduce your credit score.

- Wait between applications: Leave at least 3–4 weeks before reapplying.

- Target the right lenders: Only approach banks or NBFCs where you meet eligibility criteria.

- Monitor credit reports: Ensure past applications haven’t negatively affected your score.

Example: Applying for three loans in the same week can lower your score and make lenders cautious. Spacing applications protects your credit profile.

Outcome: Timely and strategic applications reduce perceived risk and increase approval chances.

Step 6: Address Past Defaults

Past payment issues or defaults often trigger rejections. Showing that you’ve resolved past issues and maintained responsible behaviour can change a lender’s decision.

- Clear overdue amounts: Prioritise unpaid EMIs or credit card bills.

- Demonstrate consistent repayments: Maintain on-time payments for 3–6 months post-default.

- Provide context if needed: Explain unavoidable financial hardships like emergencies to reassure lenders.

Example: Missing a ₹5,000 EMI six months ago may have lowered your credibility. Showing six months of perfect repayment afterwards demonstrates responsibility and rebuilds trust.

Outcome: Addressing past defaults effectively reassures lenders and increases the likelihood of approval.

Common Myths About Loan Rejection

Many applicants assume their personal loan will be rejected for reasons that aren’t always true. Believing these myths can cause unnecessary worry or even stop you from applying. Let’s bust the most common misconceptions:

Myth 1: I’ll get rejected if my salary is low

Reality: Lenders evaluate your overall financial profile, not just your salary. Factors like existing debts, credit history, and repayment capacity are equally important. Even moderate earners can get approved with a strong financial record.

Myth 2: Only perfect credit scores get approved

Reality: Credit score matters, but lenders also consider income stability, employment history, and outstanding obligations. A slightly lower score does not automatically mean rejection if other criteria are solid.

Myth 3: Applying online reduces my chances

Reality: The method of application (online or offline) does not affect approval. Rejections usually happen due to eligibility issues, incorrect details, or missing documents, not because of the application channel.

Myth 4: Once rejected, I’ll never get a loan

Reality: Each application is assessed independently. By improving credit health, clearing outstanding debts, and providing complete documentation, you can increase your chances in future applications.

Myth 5: Small loans are easier to get

Reality: Loan amount alone doesn’t guarantee approval. Lenders focus on your risk profile, so even small loans can be rejected if your financial behaviour or documentation is weak.

Worried About Loan Rejection? Pocketly Lets You Borrow with Confidence

Needing extra cash but fearing a personal loan rejection can be stressful. Pocketly makes borrowing simple, fast, and accessible, even if traditional loans feel out of reach.

Why Pocketly stands out:

- Borrow exactly what you need: Loan amounts from ₹1,000 to ₹25,000—no more, no less.

- No collateral or guarantor: Skip assets and co-signers, so common rejection reasons don’t apply.

- Easy eligibility: Minimal criteria make it accessible for students, freelancers, and first-time borrowers.

- Quick approval: Fast KYC verification and instant decisions, without long paperwork or waiting.

- Instant fund transfer: Get approved funds directly in your bank account within minutes.

- Flexible repayment: Pick a plan that suits your budget, reducing stress and repayment issues.

- Transparent pricing: Interest from 2% per month, processing fees 1%–8%, no hidden charges.

- Available anytime: Apply, track, and manage your loan 24/7 via Pocketly’s mobile app.

With Pocketly, regulated NBFC partnerships ensure secure loans with clear terms. Even if other lenders say “no,” you can access funds confidently and bridge your financial gap without hassle.

Conclusion

Getting a personal loan rejected can be frustrating, but it’s not the end of the road. Most rejections stem from issues you can fix, such as missing documents, a low credit score, or high debt. Understanding why your loan was denied helps you take smart steps to improve your chances next time.

It’s all about being prepared. Check your credit health, organise your paperwork, and apply to lenders that suit your profile. This way, when you really need a loan, you’re ready and more likely to get approved.

If unexpected expenses come up while you’re working on your financial profile, short-term solutions like Pocketly can help you bridge the gap. With quick approvals, flexible repayment, and transparent pricing, you can manage urgent costs without stress.

Download the Pocketly app today on [Android] or [iOS] to access funds instantly and keep your finances steady, no matter what comes your way.

FAQs

1. Why was my personal loan rejected even though I have a steady income?

Even with a steady income, lenders consider multiple factors such as credit score, existing debt, employment stability, and repayment history. Any one of these can lead to rejection.

2. Can I apply again immediately after a loan rejection?

You can reapply, but it’s better to first address the reason for rejection. Reapplying without fixing issues like a low credit score or high debt may lead to repeated rejections.

3. How long should I wait before reapplying for a personal loan?

It depends on the rejection reason. For credit-related issues, wait 2–3 months after improving your score. For documentation errors, you can reapply immediately once corrected.

4. Does a personal loan rejection affect my credit score?

Yes, multiple loan applications in a short period can slightly impact your credit score. Each rejection due to a hard inquiry is noted, so it’s wise to space out applications.

5. Are online personal loans easier to get approved for than bank loans?

Online lenders may have faster processing and more flexible eligibility criteria, but they still check income, credit score, and repayment capacity. Approval is not guaranteed.

6. Can having a co-applicant improve my chances of loan approval?

Yes, adding a co-applicant with a strong credit profile or higher income can improve eligibility and increase approval chances.