Thinking about getting a personal loan, but unsure how the new rules affect you? You landed in the right place. Staying updated with the latest rules of the RBI on personal loans is crucial before applying, especially with the rise of digital lending.

As of March 2024, fintech NBFCs alone reported an AUM of ₹2,48,006 crore for personal loans, showing just how significant this market is. Fortunately, the RBI’s updated guidelines are designed to protect borrowers, making the process more transparent, fair, and secure.

In this blog, we’ll break down the latest rules, explain their impact, and share tips to manage loans smartly and safely. Let’s get started!

In A Nutshell:

- RBI issued updated 2025 personal loan guidelines to curb mis-selling, hidden fees, and borrower exploitation.

- Digital lending rules mandate transparent disclosures, regulated interest rates, and clear repayment terms for borrowers.

- Guidelines apply to banks, NBFCs, and fintech lenders, ensuring uniform standards across all loan providers.

- Borrowers gain fairer interest rates, better grievance redressal, and more confidence in choosing trusted loan providers.

- To handle new rules smartly, compare lenders, check disclosures, and avoid borrowing beyond actual repayment capacity.

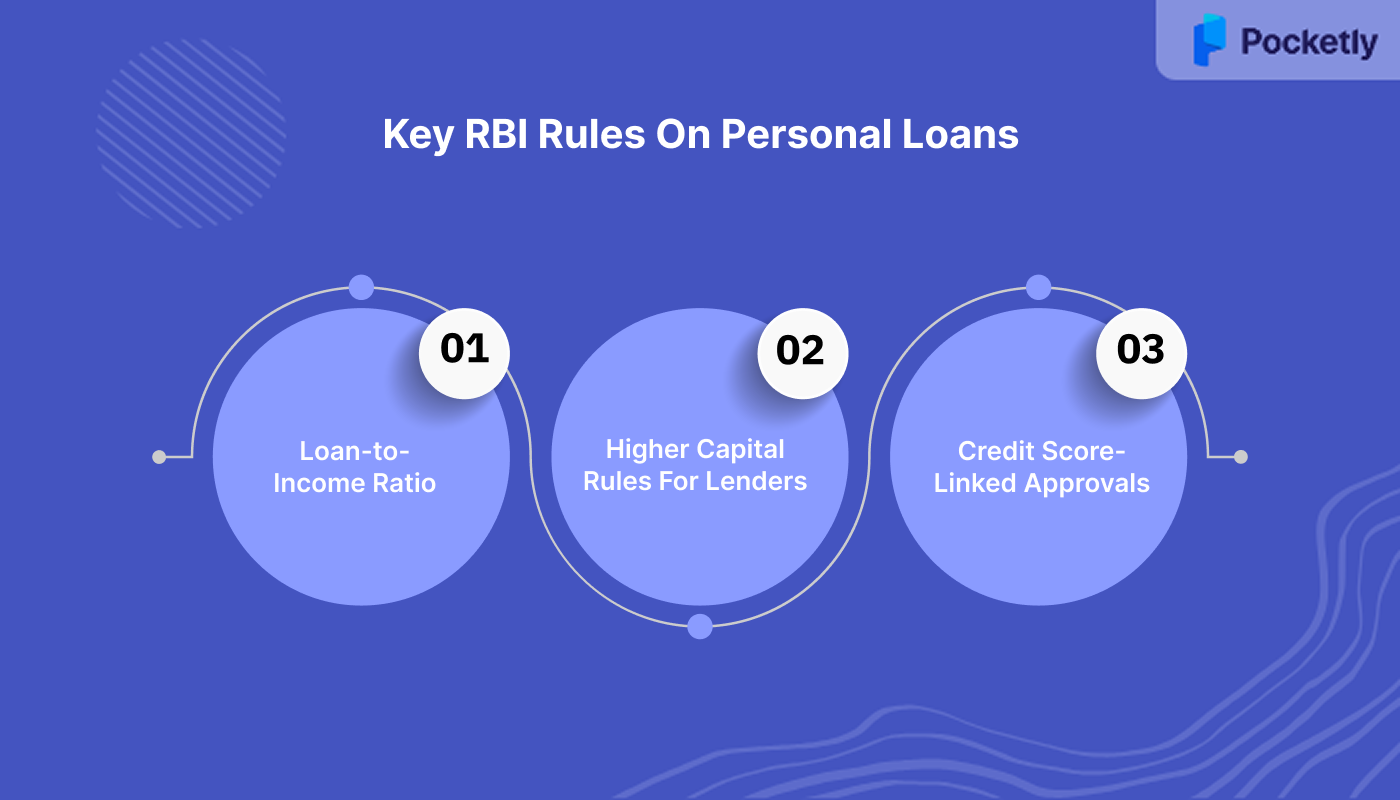

Key RBI Rules On Personal Loans

Before we dive into digital lending, let’s first look at the biggest changes in personal loan regulations. RBI on personal loans laid down strict norms to ensure that borrowing stays responsible and transparent.

Loan-to-Income Ratio

From 2025 onwards, your EMIs cannot exceed 50% of your monthly income. This rule applies to all unsecured personal loans, no matter the amount. Earlier, self-declarations of existing EMIs were enough, but now lenders must verify them properly before approving new credit.

For example, if you earn ₹50,000 a month and already pay ₹10,000 in EMIs, you can only take an additional loan where the new EMI doesn’t cross ₹15,000. This keeps you from over-borrowing and falling into a repayment trap.

Higher Capital Rules For Lenders

The RBI now requires lenders to keep aside larger reserves when they give out unsecured personal loans. Risk weights have increased from 100% to 125%, and for high-risk borrowers, and can even go up to 150%. This makes lenders more cautious in approving new credit.

What does this mean for you? If your profile is strong, you may not feel much difference. But if you have multiple loans or a lower income, lenders may limit your borrowing or charge slightly higher interest to manage their risk.

Credit Score-Linked Approvals

Your credit score has always been important, but under the new guidelines, it has become a deciding factor. Loan eligibility, limits, and interest rates will now be directly linked to your score. Borrowers with strong scores can expect better offers, while weaker scores may lead to tighter restrictions.

For example, someone with a score above 750 may get the full eligible loan amount at attractive rates. On the other hand, scores below 650 might result in reduced approvals or higher costs. Simply put, the better your credit behaviour, the smoother your loan approval process will be.

RBI’s Latest Rules For Digital Lending 2025

As more personal loans are disbursed online, the RBI has introduced clear rules to make digital lending fair for borrowers across India. These rules aim to protect borrowers while keeping digital lending efficient.

- Transparent Loan Offers: Digital platforms must show all matching loan offers, including lender name, interest rate, tenure, EMIs, and charges. This helps you compare options and choose the loan that suits your needs.

- Key Fact Statement (KFS): Every loan must come with a KFS summarising interest, fees, repayment schedule, and penalties. This ensures borrowers are aware of all costs upfront, avoiding surprises later.

- Fair Lending Practices: Digital platforms cannot favour one lender or manipulate how borrowers are matched. This keeps the process fair and consistent for everyone.

- Limited Access to Personal Data: Apps can only access necessary information, like the camera or location, for KYC purposes. They cannot misuse your files, contacts, or call logs without your consent.

- Cooling-Off Period: Borrowers have a set period to exit a loan by repaying the principal and APR without penalties. This provides flexibility if you change your mind shortly after approval.

- Direct Loan Disbursal and Repayment: Loans must be credited directly into the borrower's bank account, and repayments must go straight to the lender. Third parties cannot interfere with the disbursal or repayment process.

- Grievance Redressal and Escalation: Borrowers can raise complaints through the platform if issues arise. If unresolved within 30 days, you can escalate the matter to RBI’s Integrated Ombudsman System.

Also Read: RBI Guidelines for Personal Loan Recovery Process and Rights

Who Do The Latest Rules Apply To?

The updated RBI regulations cover almost every type of lending body. They apply to banks (public and private), NBFCs, microfinance institutions, digital lending apps, and even Lending Service Providers (LSPs). So, whether you borrow from a bank branch or a mobile app, these rules are meant to safeguard your interests.

Key Terms And Conditions In RBI Personal Loan

Before you apply, it’s important to understand the basic conditions attached to personal loans. RBI on personal loans sets clear expectations for both borrowers and lenders, making the borrowing process safer.

Eligibility Criteria: Lenders assess age, income, and employment stability before approval. Most personal loans are available to borrowers aged 21- 57 with a steady income, preferably credited directly to a bank account.

Documentation and Loan Limits: Submitting correct documents, like valid ID, address proof, etc., and avoiding multiple active loans is crucial. Following these conditions helps prevent delays and ensures smooth loan processing.

Credit Score Requirements: A strong credit score, generally above 700, improves your chances of approval and lower interest rates. Borrowers with low scores or fragmented repayment history may face higher rates or rejection.

Also Read: Personal Loans for Students Without Income in India

Impact Of RBI Guidelines On Loan Applicants

The 2025 RBI rules aim to make borrowing safer and clearer for you. Here’s how your experience changes:

- Full Transparency and Safe Disbursal: With the Key Fact Statement, you’ll know all charges, EMIs, interest rates, and tenure upfront. Loans are credited directly to your account, eliminating third-party delays.

- Better Eligibility Assessment: Lenders now review income, employment, existing debts, and credit history thoroughly. This ensures you only take loans you can comfortably repay.

- Fair Charges and Data Protection: Processing fees, late penalties, and other costs must be disclosed upfront. Your data is secured, and apps cannot misuse it without consent.

- Grievance Redressal Support: If any issue arises, lenders or apps must resolve complaints promptly within 30 days, giving you a safer borrowing experience.

Tips To Handle RBI’s Personal Loan Guidelines With Ease

Managing RBI on personal loans rules effectively can improve your approval chances and help you borrow responsibly. Here are practical tips to handle these rules with ease:

Keep Your Credit Profile Healthy

A strong credit score is key under the new RBI guidelines. Regularly check your credit report for errors, pay all EMIs and credit card bills on time, and maintain a credit utilisation ratio below 30%. A healthy profile increases your chances of approval and helps secure lower interest rates.

Maintain A Balanced Debt-to-income Ratio

Lenders now assess your total debt obligations more strictly. Try to keep total EMIs below 40% of your monthly income, prepay high-interest loans, or consolidate debts before applying for a new personal loan. This ensures you stay within the RBI’s recommended repayment limits.

Pick Lenders Wisely

Not all banks and NBFCs interpret the RBI rules the same way. Compare multiple lenders’ eligibility criteria, digital processes, and pre-approved offers. Choosing a lender that aligns with your repayment capacity and offers transparent digital options can save time and avoid rejection.

Plan For Repayment And Foreclosure

Understand the foreclosure process, part-payment options, and associated fees like cheque bounce or processing charges. Planning your repayment strategy in advance helps you avoid unexpected costs and allows you to clear your loan efficiently.

Stay Informed And Use Available Resources

Always read the Key Fact Statement (KFS) carefully, and keep track of any changes in interest rates, penalties, or processing fees. If you encounter issues, the grievance redressal channels can resolve disputes quickly, ensuring a smooth borrowing experience.

Pocketly: A Simple Way to Borrow Within RBI Guidelines

With the new guidelines of the RBI on personal loans, borrowers are now more protected than ever. Pocketly supports this for young Indians by offering short-term loans while staying fully compliant and informed. As a digital lending platform, Pocketly focuses on providing fast, flexible, and hassle-free loans for emergencies and short-term cash needs.

- Transparent Loan Terms: All interest rates start at 2% per month, with processing fees ranging from 1–8%. Every cost is upfront, giving you a clear picture of your loan.

- Quick Access to Funds: Borrow ₹1,000–₹25,000 with fast approval, and get the money directly into your bank account in minutes.

- Flexible Repayments: Adjustable EMIs let you pay at your pace, with options to prepay or close the loan early without stress.

- Simple KYC & Minimal Documentation: Only essential documents are needed to get your loan approved, making the process fast and easy.

- 24/7 Support: Our team is available around the clock to help with any queries or concerns, aligned with RBI’s transparency and grievance rules.

Loan Application Process: Signing up is straightforward. Just register with your mobile number, upload required KYC documents, provide bank account details, select your loan amount and repayment tenure. Once done, the funds are disbursed directly into your account within minutes.

Pocketly puts you in control, delivering quick, transparent short-term loans to handle emergencies without hidden surprises.

Wrapping Up

Understanding the rules of the RBI on personal loans helps you make smarter borrowing decisions. The 2025 guidelines bring more transparency, fair practices, and stronger protections for borrowers. By knowing your rights, eligibility criteria, and the key terms, you can confidently manage personal loans without surprises or hidden charges.

With Pocketly, accessing short-term loans becomes simple and stress-free. Get flexible amounts from ₹1,000 to ₹25,000, quick approvals, and 24/7 support. Download the Pocketly app on iOS or Android to manage emergencies effortlessly.

FAQ’s

What is the new rule of RBI for personal loans?

The latest guidelines issued by the RBI on personal loans focus on transparency, fair lending practices, and borrower protection. Lenders must disclose all charges upfront, verify income and creditworthiness, and ensure borrowers understand the loan terms.

What are the RBI guidelines for personal loan defaulters?

Borrowers have the right to dignity and privacy, meaning no harassment, intimidation, or public disclosure of debt. Lenders must follow fair recovery methods and provide clear communication about outstanding amounts.

What is the punishment for not paying a personal loan?

Non-payment may lead lenders to approach civil courts, potentially resulting in asset seizure or wage garnishment. It can also negatively impact your credit history, making future loans harder to secure.

What are the restrictions on a personal loan?

Some personal loans may restrict usage for certain purposes, like gambling or as a mortgage down payment. Borrowers should review the agreement carefully to avoid violating the terms.