The Indian personal loan market is booming, with a CAGR of 15.83% annually from FY2025 to FY2032. However, even as opportunities expand, one key factor that continues to influence personal loan approvals is your credit score.

But here’s the catch: a lot of young Indians don’t fully understand what a credit score is until they’re turned down for a loan. It’s frustrating to find out that your score is the reason you didn’t get approved. If you’re just starting to build your financial history, it can feel even more confusing.

What if you could get the hang of how credit scores work and learn how to improve yours? Knowing the minimum credit score for a personal loan and exploring options even if you’re new to credit can make a big difference.

In this blog, we’ll break down everything you need to know about the minimum credit score for personal loans in India, how to improve your score, and what alternatives you have. By the end, you’ll have a clearer idea of how to take the next step in managing your finances.

What Is a Credit Score?

In India, your credit score is a three-digit number, typically ranging from 300 to 900 that reflects how likely you are to repay borrowed money on time. It acts as a quick summary of your creditworthiness, helping lenders decide whether to approve your loan or credit card application and what terms to offer you.

Credit Score vs. CIBIL Score

Many people tend to use "CIBIL Score" and "Credit Score" interchangeably, but there’s actually a key difference between the two. A "Credit Score" is a general term for any number that reflects your creditworthiness. It’s a broad concept, and it can be generated by any of the major credit bureaus.

On the other hand, the "CIBIL Score" refers to the specific credit score provided by TransUnion CIBIL, one of the major credit rating agencies in India. So, while every CIBIL Score is a credit score, not every credit score is a CIBIL Score. Other agencies, like Experian, Equifax, and CRIF High Mark, also issue their own credit scores, each based on its own unique approach and analysis.

How are Credit Scores Calculated?

Credit scores are determined based on the information provided in your credit report. This includes:

- Your repayment history,

- Total outstanding debt,

- Types and number of credit accounts,

- Length of your credit history

- Credit utilization

- Recent applications for new credit

Suppose you have the following credit profile:

- Repayment History: You’ve always paid your EMIs and credit card bills on time, and you never missed a payment.

- Credit Utilization: Your total credit card limit is ₹1,00,000, but you typically keep your outstanding balance around ₹20,000. That’s just 20% utilization.

- Length of Credit History: Your oldest credit account has been active for 5 years.

- Types of Credit: You have one credit card and one personal loan, giving you a good mix of credit.

- Recent Credit Inquiries: You applied for a new credit card once in the past year.

Now, let’s see how these factors add up using the typical weightage system:

| Factor | Weightage | Your Status | Contribution to Score |

|---|---|---|---|

| Repayment History | 35% | No missed payments | 35/35 |

| Credit Utilization | 30% | 20% utilization | 28/30 |

| Length of Credit History | 15% | 5 years | 12/15 |

| Types of Credit | 10% | Mix of card & loan | 9/10 |

| Recent Inquiries | 10% | 1 inquiry in the last year | 9/10 |

| Total | 93/100 |

In India, credit scores usually range from 300 to 900. Here’s how you can estimate your score:

- The lowest possible score is 300.

- The highest is 900.

- That’s a difference of 600 points.

So, your estimated score would be:

Score = 300 + (93% of 600)

= 300 + (0.93 × 600)

= 300 + 558

= 858

That means, with these healthy credit habits, your credit score would likely be around 858, which is considered excellent!

Lenders also consider your income, employment stability, existing debts, and other financial details before making a decision. A higher score generally improves your chances of getting a loan with favorable terms, but a strong overall financial profile is equally important.

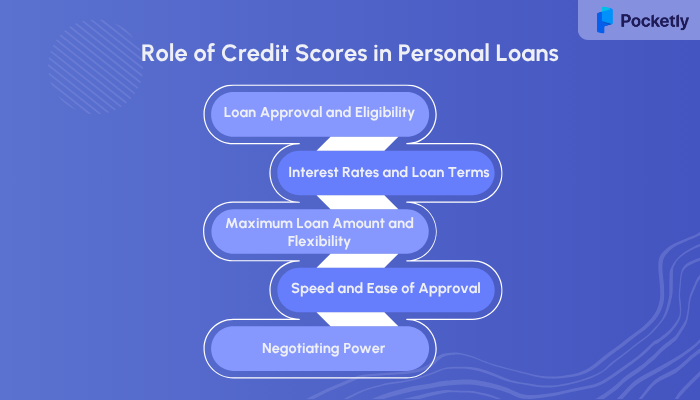

What is the Role of Credit Scores in Personal Loans

Credit scores help to assess the risk involved in lending money to an individual. Let’s break down the significance of credit scores in the loan process:

1. Loan Approval and Eligibility

Your credit score acts as a primary filter to decide whether to approve your personal loan application. A higher score signals your responsible credit behavior and makes you a more attractive candidate for approval.

Banks and NBFCs set a minimum credit score threshold for personal loan eligibility. If your score falls below this range, your chances of approval drop significantly, and you may need to seek alternative lenders or provide additional documentation.

2. Interest Rates and Loan Terms

Your credit score doesn’t just determine if you get approved, but it also directly impacts the interest rate and terms you’re offered. Borrowers with high credit scores are rewarded with lower interest rates, reduced processing fees, and sometimes even longer repayment tenures.

This indicates that a good credit score can save you a significant amount of money throughout the life of your loan. Conversely, a lower score often results in higher rates and stricter terms, reflecting the increased risk to the lender.

3. Maximum Loan Amount and Flexibility

A strong credit score can also increase the maximum loan amount you’re eligible for. You can be offered larger sums if you have demonstrated responsible credit management over time. Additionally, you may enjoy greater flexibility in choosing your loan tenure and repayment options.

4. Speed and Ease of Approval

With a high credit score, the loan approval process is often faster and smoother. Lenders may require less documentation and conduct fewer background checks, expediting the disbursal of funds when you need them most. On the other hand, a lower score can lead to a more cumbersome application process and additional scrutiny.

5. Negotiating Power

A satisfactory credit score gives you the power to negotiate better terms with lenders. You can demand lower interest rates or reduced fees, knowing that your strong credit profile makes you a desirable customer.

Credit scores are a critical factor in the personal loan approval process. A lower score may lead to high interest rates or limited credit access.

However, the minimum credit score for a personal loan varies from bank to bank. NBFCs and other digital lenders often have their own credit score requirements for offering a personal loan to you. Let’s discuss the minimum credit scores for a personal loan in India.

Minimum Credit Score for a Personal Loan in India

In India, most major credit bureaus have a similar standard for what’s considered a good credit score. TransUnion CIBIL, Experian, and CRIF Highmark typically view scores above 700 as favourable, while Equifax considers a score of around 670 to be good.

Attaining a score within this range significantly enhances your prospects for loan approval and positions you to secure the most advantageous interest rates and repayment terms available.

Minimum Credit Score for a Personal Loan: Banks vs. NBFCs

The minimum credit score required to get a loan can vary depending on the lender. This reflects the growing diversity in India’s lending market. Banks usually prefer lower-risk borrowers and offer better terms, while NBFCs are more flexible and cater to a wider range of applicants.

Traditional Banks

In India, most public and private banks require a minimum CIBIL score between 700 and 750 for personal loan applications. While some may consider loans for applicants with scores as low as 650, it’s often accompanied by higher interest rates or stricter loan conditions. The reason for this is simple: a lower score signals more risk for the bank. Banks are generally more cautious and tend to follow stricter eligibility rules.

If you have a low credit score, lenders see you as a higher risk, and that’s why they may offer loans with higher costs attached. Simply put, the higher the risk, the more it costs to borrow. So, if your credit score isn’t in the “ideal” range, you could face more expensive loan terms. This is how your credit score directly impacts how much you’ll pay for a personal loan.

NBFCs (Non-Banking Financial Companies) & Fintech Lenders

NBFCs and fintech lenders are usually more flexible in terms of credit score requirements than traditional banks. Many of them are open to approving loans for people with scores under 700, and some may even accept scores as low as 650 or lower.

Instead of focusing solely on the credit score, they often look at other factors, like your income, job or business stability, the reputation of your employer, and a closer look at your bank statements. This flexibility makes NBFCs and fintech lenders a great option for those who need quick access to funds or who might not meet the stricter criteria of traditional banks.

The following table provides a comprehensive overview of how lenders in India generally perceive different credit score ranges and their corresponding implications for personal loan approval and terms.

| Credit Score Range | Status | Loan Approval Chances | Typical Interest Rates/Terms | Lender Preference |

|---|---|---|---|---|

| 800 and above | Excellent | Highest | Best rates & most flexible terms | All lenders |

| 750 - 799 | Very Good | Very High | Favorable rates & terms | Most banks, all NBFCs |

| 701 - 749 | Good | Good | Standard rates, reasonable terms | Some banks, most NBFCs |

| 651 - 700 | Average | Moderate | Higher rates & stricter terms | NBFCs/Fintech lenders |

| 300 - 650 | Poor | Challenging/Low | Very high rates or difficult to obtain | Limited options (NBFCs/Fintech) |

Knowing the minimum requirements and why they matter can help you find the right lender and increase your chances of approval.

Even if you have little or no credit history, NBFCs and fintech lenders can still be options. This brings to the question of why the requirements of credit scores differ between banks and other NBFCs and Fintech lenders.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

Why Banks and NBFCs Have Different Credit Score Requirements for Personal Loans

The reason banks and NBFCs have different credit score requirements comes down to their different approaches to business, risk, and who they’re willing to lend to. Here are the key reasons:

1. Risk and Target Market

Banks are careful with their lending. They prefer borrowers with a strong credit history and usually require a CIBIL score of 700 or more. In return, they offer better rates and terms. NBFCs, however, are more flexible.

They’re open to lending to a wider range of people, even those with little or no credit history. Since there’s more risk, they may approve loans for people with scores as low as 650.

2. How They Assess You

Banks mainly look at your credit score when deciding whether to approve your loan. NBFCs take a more holistic approach. If your score is low, they’ll consider other things, like your income, job stability, and the reputation of your employer.

They might also look at your bank statements to understand your finances better. This way, they get a clearer picture of your ability to repay.

3. Regulatory Differences

Banks have to follow strict rules set by the Reserve Bank of India (RBI), including how they set interest rates. NBFCs have a bit more flexibility in setting rates because they have their internal benchmarking systems. This means they can create loan products that fit a wider range of borrowers.

4. Speed and Digitalization

NBFCs are known for quick loan processing and disbursal times, with a priority on digital application processes and minimal paperwork compared to traditional banks. This is great for people who need funds quickly or those who struggle with the extensive paperwork that banks require.

However, if you don’t meet the strict credit score requirements of banks or you have little to no credit history, Pocketly could be a great option. Pocketly offers loans ranging from ₹1,000 to ₹25,000, with interest rates from 2% per month. Processing fees are between 1% and 8% of the loan amount. The best part is that you can apply online and get approved in minutes.

Steps to Improve Your Credit Score

Creating a good credit score takes discipline. It’s all about creating good financial habits and sticking to them. Your credit score reflects how competently you handle your money, rewarding responsible actions and penalizing careless ones. Here’s how to improve your score:

- Timely Payments: This is the most important thing you can do. Always ensure timely payments for your loans and credit card bills. A single missed or late payment can negatively impact your score.

- Manage the Utilisation of Credits: If you’re using too much of your available credit, it can negatively affect your score. Aim to keep your credit usage below 30%. A smart move is to ask for a higher credit limit while keeping your spending the same. This lowers your credit utilization ratio and can help your score.

- Credit Mix and History: Having a mix of different types of credit, like home loans, auto loans, and credit cards, shows you can handle various forms of debt. Also, the longer you’ve had credit and have managed it well, the better it is for your score.

- Limit the Applications for Credit Cards: When you apply for credit, authorities can make a “hard inquiry”, which can slightly lower your credit score. You should avoid applying for many credit cards in a short period. It can make lenders think you’re relying too much on credit.

- Avoid Being a Guarantor (Unless You're Sure): Being a guarantor for someone else’s loan can hurt your credit if they fail to make payments. Only agree to be a guarantor if you're confident the person can repay their loan.

Improving your credit score doesn’t happen overnight. It takes time to see real improvement, usually between 4 to 12 months. It might take longer if you’ve had serious issues like defaults or bankruptcies. Stick with good habits, and over time, your score will improve.

Read More: How to Achieve a Perfect 900 CIBIL Score?

When it comes to personal loans, many young Indians worry that a limited or low credit score will automatically disqualify them from getting the funds they need. This is where digital lending platforms like Pocketly come to the rescue.

How Pocketly Makes Borrowing Easy for Young People

Pocketly is a fintech platform designed specifically to support the financial needs of young Indians, including students, new professionals, and entrepreneurs, who may not have an extensive credit history. Unlike traditional banks that typically require a high credit score and collateral, Pocketly offers short-term personal loans with a simple, digital-first approach.

Pocketly Supports Borrowers with Limited Credit History with:

- Low Entry Barriers: Pocketly’s easy-to-follow KYC process and minimal documentation requirements make it accessible for those with little or no credit history.

- No Collateral: You don’t need to pledge any assets, making it ideal for students and young professionals just starting out.

- Small Loan Amounts: Borrowers can access amounts from ₹1,000 up to ₹25,000, perfect for handling month-end crunches, education expenses, or small business needs.

- Quick Disbursal: Once approved, funds are transferred directly to your bank account, often within minutes, addressing urgent financial needs without the long wait.

- Transparent Costs: Interest rates start at 2% per month, with a clear processing fee structure and no hidden charges.

If you’re concerned about meeting the minimum credit score for a personal loan, Pocketly offers a practical, transparent, and accessible solution. It not only helps you meet immediate financial needs but also supports your journey toward a stronger credit profile and greater financial independence.

Final Words!

In India, securing a personal loan can be tough, especially if you're just starting to build your credit. However, understanding the minimum credit score required for loan approval and taking the necessary steps to improve your score can significantly improve your chances of getting favorable terms.

Fortunately, Pocketly is here to make it easier. If you're struggling to meet traditional banks' strict credit score requirements, Pocketly offers a flexible, quick, and transparent solution.

Pocketly offers a way to secure emergency funds or finance your goals without worrying about a perfect credit score. Best of all, you can apply online, and the funds are often in your account within minutes.

If you’re in need of financial flexibility, download the Pocketly app to apply for a loan today!

FAQs

Q: Can I get a personal loan with no credit history?

A: Yes, it's possible to get a personal loan without a credit history. Some lenders, like non-banking financial companies (NBFCs) and online lenders, may be open to applicants who don't have a credit record. They usually look at other factors, such as your income, job stability, and banking history, to decide if you're able to repay the loan.

Q: Does a higher credit score guarantee approval?

A: A high credit score definitely improves your chances of getting approved, but it doesn't guarantee it. Lenders will also consider things like your income, job history, and current debts when making their decision. With a good score, you’re more likely to get better terms, such as lower interest rates and larger loan amounts.

Q: How can I improve my credit score?

A: You can see some improvement in your credit score within a few months if you focus on paying bills on time, cutting down debt, and avoiding new loans. However, building a solid credit score takes time and consistent effort. Negative marks can remain on your account for years, but positive actions are usually reflected in your score more quickly.