When it comes to managing loans, understanding how interest works is important to making smart financial decisions. Simple interest is a common method used to calculate interest on the original amount borrowed or invested, giving you a clear view of what you'll owe over time. It’s easy to understand, making it ideal for short-term loans and investments.

But here's something that can impact your finances significantly: personal loan interest rates in India range from 10.00% to 44% per annum. This means the amount of interest you pay can vary greatly depending on the rate you're offered.

Knowing how to calculate simple interest and EMIs can give you more control over your financial future, helping you avoid surprises and manage your repayments efficiently. Let’s dive into the simple interest formula and explore how it can guide your financial decisions.

Key Takeaways:

- Simple Interest: A straightforward method for calculating interest on loans or investments based on the original principal amount.

- Calculation Process: Simple interest is calculated using the formula SI = (P × R × T) / 100, with key variables being principal, rate, and time.

- Loan Tenure Impact: Shorter loan tenures lead to higher EMIs but lower total interest, while longer tenures reduce EMIs but increase total interest paid.

- Amortisation vs Simple Interest: Amortisation reduces the principal over time, whereas simple interest is calculated only on the original principal throughout the loan term.

- Loan Calculators: Simple interest calculators provide quick and accurate results, helping you estimate interest and total amounts for better financial planning.

What is Simple Interest?

Simple Interest (SI) is a method of calculating interest on a loan or investment based on the initial principal amount. Unlike compound interest, which is calculated on both the principal and accumulated interest, simple interest is calculated only on the original principal for the entire duration of the loan or investment.

Formula: The formula for calculating SI is:

SI = (P × R × T) / 100

Where:

- P = Principal amount (the original amount of money borrowed or invested)

- R = Rate of interest per annum (expressed as a percentage)

- T = Time period (in years) for which the money is borrowed or invested

When Should You Use the Simple Interest Formula?

Simple Interest is typically used in situations where the loan or investment does not compound over time. Here are some common scenarios where the Simple Interest formula is applied:

- Personal loans: Ideal for short-term loans, such as those for students or salaried individuals, where the interest is calculated only on the principal amount throughout the loan term.

- Fixed-Term Deposits: Used for investments with a set duration, where interest is calculated on the initial principal, and there are no periodic interest reinvestments.

- Short-Term Investments: When investing for a short period, such as 1-2 years, Simple Interest can be used to determine the interest accrued on the initial amount.

- Education Loans: Often structured using simple interest, especially when repayment is expected to start after a few years, with interest calculated only on the original loan amount.

Whether you're managing a personal loan or handling unexpected expenses, Pocketly offers a simple solution. With short-term loans from ₹1,000 to ₹25,000, Pocketly ensures instant disbursal and flexible repayment options, all with minimal documentation and no collateral required.

How to Calculate Simple Interest (Step-by-Step Process)

To calculate simple interest, you need three key inputs: the principal amount (P), the interest rate (R), and the time period (T). Once you have those, the formula is straightforward, and the process is easy to follow.

- Gather your values: First, identify the principal (how much money you borrowed or invested), the interest rate (usually a percentage), and the time period (typically in years) for the loan or investment. For example, let’s say you have ₹10,000 at 5% for 3 years.

- Plug the values into the formula: Using our example of ₹10,000, 5%, and 3 years, you would multiply these values with the simple interest formula:

SI = (10,000 × 5 × 3) / 100. This gives you ₹1,500 as the interest over the 3 years.

- Check your units: If your interest rate is given monthly or for partial years, you’ll need to adjust the time period or rate. For instance, if the interest rate is 5% per month, you would multiply it by 12 to convert it to an annual rate. Similarly, for a loan period of 6 months, the time factor should be represented as 0.5 years in the formula.

Also Read: Calculating Personal Loan Amount Based on Salary

What Is the Total Amount Using the Simple Interest Formula?

When calculating simple interest, it's important to determine the total amount or maturity amount, which is the sum of the principal and the interest.

The formula for the Total Amount (A) is:

Total Amount = Principal + Interest

Where:

- The principal refers to the initial money that is borrowed or invested.

- Interest is the simple interest calculated using the formula discussed earlier.

Example Calculation:

For example, let’s say you have ₹10,000 invested at an interest rate of 5% for 3 years:

- Interest: Interest = (10,000 × 5 × 3) / 100 = ₹1,500

- Total Amount: Total Amount = ₹10,000 + ₹1,500 = ₹11,500

So, after 3 years, the total amount will be ₹11,500, which includes your original principal of ₹10,000 and ₹1,500 interest.

How Can a Simple Interest Calculator Help You?

Being an online tool, a Simple Interest Calculator helps you instantly calculate the interest and total amount for loans or investments. It uses three key variables, principal, rate, and time, to give you an accurate calculation of both the interest and the maturity amount.

Benefits of Using a Simple Interest Calculator:

- Speed and Accuracy: It provides fast and accurate calculations. This further eliminates the need for manual computation and reduces the risk of errors.

- Quick Estimation: Get an instant estimation of the interest amount, allowing you to make quick financial decisions.

- Versatile: It can be used for different types of loans and investments, including personal loans, education loans, and business loans.

Also Read: Getting Personal Loans for Young Students in India Without Parents

How It Works:

- Simply input the required values, Principal, Rate, and Time, into the calculator, and you’ll get the results immediately. The tool calculates both the interest and the total maturity amount, helping you stay on top of your financial planning.

Example Calculations Using a Simple Interest Calculator

To better understand how a Simple Interest Calculator works, let's look at some practical examples. These examples will help illustrate how the calculator can be used to determine both the interest and the total amount.

Case 1: ₹5,00,000 at 7% for 1 year

In this scenario, you’ve invested ₹5,00,000 for 1 year at an interest rate of 7%. The calculation process would look like this:

- Interest: Interest = (5,00,000 × 7 × 1) / 100 = ₹35,000

- Total Amount: Total Amount = Principal + Interest = ₹5,00,000 + ₹35,000 = ₹5,35,000

So, after 1 year, the total amount will be ₹5,35,000, which includes the original principal of ₹5,00,000 and the ₹35,000 interest earned.

Case 2: ₹10,00,000 at 15% for 5 years

Now, let’s take a larger investment of ₹10,00,000 for 5 years at an interest rate of 15%. Here’s the breakdown:

- Interest: Interest = (10,00,000 × 15 × 5) / 100 = ₹7,50,000

- Total Amount: Total Amount = Principal + Interest = ₹10,00,000 + ₹7,50,000 = ₹17,50,000

So, after 5 years, the total amount due would be ₹17,50,000, which includes the original ₹10,00,000 principal and the ₹7,50,000 interest.

Understanding the Relationship Between Loan Tenure and Simple Interest

Loan tenure, or the duration of time over which a loan is repaid, has a significant impact on both the total interest amount and the EMIs (Equated Monthly Instalments) you will need to pay.

In the case of simple interest loans, the interest is calculated on the principal amount, the rate of interest, and the time period. Therefore, any changes in the loan tenure directly affect the total interest and the size of your monthly payments.

Impact of Loan Tenure on Total Interest and EMIs

- Shorter Loan Tenure: When the loan tenure is short, the EMIs will be higher because you are repaying the loan over a smaller period. However, the total interest you pay over the life of the loan will be lower since the interest is calculated for a shorter time.

- Longer Loan Tenure: Extending the loan tenure reduces the size of the EMIs, making monthly repayments more manageable. However, this results in a higher total interest because the loan is repaid over a longer period, and interest continues to accumulate on the principal amount for a longer time.

What is Amortisation?

Amortisation is the process of gradually repaying a loan over a set period through equal, regularly scheduled payments. These payments typically cover both the principal (the amount borrowed) and the interest. As you make each payment, the principal reduces. Additionally, a portion of your payment goes towards paying off the interest. Over time, the interest reduces while the principal portion increases, until the entire loan is paid off.

Difference Between Amortisation and Simple Interest

- Simple Interest: Interest is calculated on the original principal amount throughout the loan term, with no reduction in principal over time.

- Amortisation: Payments reduce the principal over time, so interest is recalculated on the remaining balance after each payment.

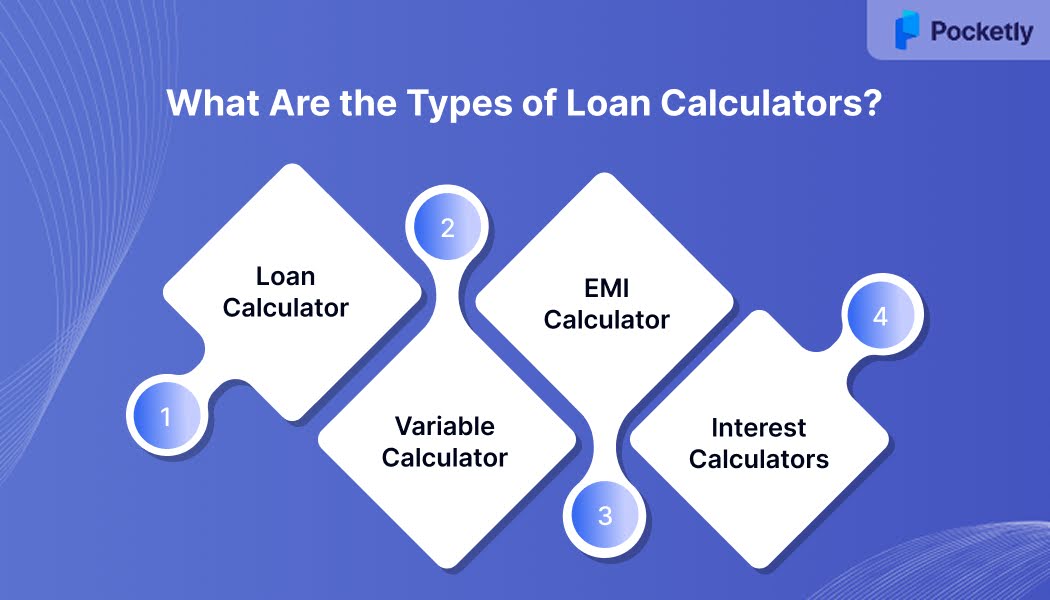

What Are the Types of Loan Calculators?

When it comes to managing loans, there are several types of calculators available, each serving a unique purpose. These tools help you better understand your loan terms and repayments. Below are the most common types of loan calculators:

1. Fixed-Rate Loan Calculator

A Fixed-Rate Loan Calculator is designed for loans that have a constant interest rate throughout the loan term. This type of calculator is ideal for calculating monthly repayments (EMIs) when the rate doesn’t change over time. It gives borrowers a clear understanding of their fixed monthly payment amounts, making budgeting easier.

2. Variable-Rate Loan Calculator

For loans where the interest rate changes over time, a Variable-Rate Loan Calculator comes into play. This tool allows you to determine how changes in interest rates will impact your monthly payments and the total cost of the loan, especially for loans that are tied to market rates.

3. EMI Calculator

An EMI Calculator calculates the Equated Monthly Instalments (EMIs) for any loan. It takes into account not just the principal amount, but also the interest rate and loan tenure to provide an estimate of the monthly payments. This is particularly useful for budgeting and understanding how your loan repayment schedule will look.

4. Simple Interest vs Compound Interest Calculators

When dealing with loans or investments, understanding the type of interest applied can significantly impact your repayment strategy. Simple Interest Calculators are used for loans where interest is calculated only on the principal amount, while Compound Interest Calculators account for interest on both the principal and any accumulated interest.

How Pocketly Can Support Your Financial Journey?

Managing loans and understanding the impact of simple interest can be overwhelming, especially when unexpected expenses arise. Whether you're dealing with a personal loan, an education loan, or short-term financial needs, keeping track of your payments is essential for maintaining a healthy financial status.

However, sometimes managing these payments, especially during financial emergencies, can become difficult. Pocketly offers a practical solution to help you manage your cash flow. It also assists you in staying on track with your loan repayments.

With instant loan disbursal and flexible repayment options, Pocketly provides small, short-term loans from ₹1,000 to ₹25,000, perfect for covering emergencies or smoothing over financial gaps.

Key features include:

- Instant Loan Disbursal: Apply and receive funds directly in your bank account within minutes.

- Flexible Repayment Options: Choose repayment tenures ranging from 2 to 6 months, with the ability to restructure or refinance loans as needed.

- Minimal Documentation: A hassle-free application process with minimal KYC requirements.

- 24/7 Customer Support: Access dedicated assistance anytime to address your queries and concerns.

By integrating Pocketly into your financial strategy, you can manage your loan repayments more effectively. Quickly download the app for a smooth experience!

Conclusion

Simple Interest is a straightforward formula, ideal for calculating interest on short-term loans and investments. It simplifies the process of determining how much interest you’ll pay or earn over a set period.

While the concept is simple, knowing when and how to apply the simple interest formula is equally important for effective financial planning. For quick, accurate financial calculations, a Simple Interest Calculator is an invaluable tool. It provides immediate insights, helping you make sound financial decisions.

In an emergency situation or to cover unexpected expenses, reach out to Pocketly. Get quick, short-term loans with minimal documentation, instant disbursal, and flexible repayment options to manage your finances effortlessly.

Frequently Asked Questions

How is EMI calculated in simple interest?

EMI in simple interest loans is calculated by dividing the total repayment amount (principal + interest) into equal monthly payments. Simple interest is calculated only on the principal, not accumulated interest. The formula is: EMI = (P + (P × R × T) / 100) / N.

What is EMI in simple words?

EMI (Equated Monthly Installment) is the fixed monthly amount paid to repay a loan. It covers both the interest and principal, making loan repayment more manageable.

What is the major difference between EMI and simple interest and compound interest in practical?

EMI is a fixed monthly payment that includes both principal and interest, while simple interest is calculated only on the original principal. Compound interest, on the other hand, adds interest to both principal and accumulated interest, making it more expensive over time.

How do you calculate the loan EMI and interest rate?

The formula for EMI is EMI = (P × R × (1 + R)^T) / ((1 + R)^T - 1). The interest rate can be derived based on the loan amount, tenure, and EMI amount using a reverse calculation.