Ever swiped a credit card or considered a personal loan and wondered, 'Am I making the right choice?' Many of us do. Using credit or taking a loan without understanding the differences can lead to surprise charges, high interest, or lingering debt.

The stress of mismanaged borrowing can quickly outweigh the convenience it promises. Unplanned credit use or loans can trap you in cycles of repayments that feel impossible to break.

But it doesn’t have to be that way. Knowing when to use credit and when to take a loan gives you clarity, control, and confidence over your finances. The right choice can help you cover urgent expenses, manage large purchases, or grow your financial stability without unnecessary strain.

In this blog, we’ll break down credit and loans, compare their pros and cons, and show you how to make smarter borrowing decisions that actually work for you.

TL;DR

- Credit and loans may look similar, but they work differently. Credit offers flexible, reusable access to funds, while a loan provides a fixed amount with a defined repayment schedule.

- Your decision should depend on purpose and repayment capacity. Credit works better for short-term expenses you can clear quickly. Loans are more suitable for larger, planned costs that require structured repayments.

- Instead of focusing only on interest rates, evaluate the total repayment amount, fees, tenure, and how comfortably the repayment fits into your monthly budget.

- Smart borrowing is about clarity and control. When used wisely, credit adds flexibility and loans provide structure.

- If you need short-term financial support without long-term pressure, solutions like Pocketly can help you manage the gap responsibly.

What Is Credit and How Does It Work?

Credit allows you to use money now and repay it later. It’s a flexible way to manage purchases without needing cash up front.

Key points about credit:

- Comes in forms like credit cards, store credit, and lines of credit

- Has a preset borrowing limit set by the lender

- Timely repayments help build your credit score

- Missed or late payments can negatively affect your creditworthiness

How it works:

- You make a purchase, and the lender pays immediately

- You repay the borrowed amount over time

- Your credit history influences future borrowing limits and interest rates

Example: Swiping a credit card for a ₹5,000 electronics purchase lets you pay later. Clearing the bill on time strengthens your credit history and opens doors to higher limits and better financial options.

What Is a Loan and How Does It Work?

A loan is a fixed amount of money borrowed from a lender that you repay over an agreed period, usually with interest. Unlike credit, loans are structured and often meant for specific purposes.

Key points about loans:

- Can be secured (with collateral) or unsecured (no collateral)

- Fixed repayment schedule with monthly EMIs

- Interest rates may be fixed or variable

- Late payments can lead to penalties or legal action

How it works:

- You apply for a loan, and the lender approves a specific amount

- Funds are disbursed to your account

- You repay in instalments until the loan is fully cleared

Example: Taking a ₹1,00,000 personal loan for home renovation allows you to pay it back in 12 months through fixed EMIs.

Timely payments keep your financial record healthy and avoid extra charges.

Credit vs Loan: A Side-by-Side Comparison for Smart Borrowing

When managing finances, knowing whether to use credit or a loan can make a huge difference. Both allow you to borrow money, but they work in different ways, with unique repayment rules, flexibility, and costs. Understanding these differences helps you make smarter financial choices and avoid unnecessary interest or debt.

Below is a clear comparison to guide your decision:

| Feature | Credit | Loan |

| Definition | A flexible borrowing limit you can use repeatedly | A fixed amount borrowed for a specific purpose |

| Access | Revolving; borrow, repay, and borrow again | One-time disbursement; repaid in fixed instalments |

| Interest | Charged only on the amount used | Charged on the full loan amount from day one |

| Repayment | Flexible, minimum monthly payments possible | Fixed EMIs over the loan tenure |

| Collateral | Usually unsecured (except for credit lines) | Can be secured or unsecured |

| Purpose | General use: shopping, emergencies, daily expenses | Specific use: home, education, car, business |

| Flexibility | High; borrow as needed within the limit | Low amount and a fixed schedule |

| Impact on Credit Score | Usage and timely repayment affect the score | Timely repayment builds credit history; defaults hurt |

Also Read: Different NBFC Types in India: A Guide For 2026

When Credit Makes Sense and When a Loan Is Better

Understanding when to use credit and when to opt for a loan can save you money, reduce stress, and make your finances more predictable. Both serve the purpose of providing funds, but they do so in very different ways. The choice depends on your borrowing needs, repayment flexibility, and the goal behind the money.

When Credit Works Best

- Provides flexible access to funds for day-to-day or unpredictable expenses.

- Interest is charged only on the amount used, not the full limit.

- Ideal for short-term cash flow gaps or recurring needs.

Example: A freelance designer in Bengaluru can use a credit line to cover fluctuating monthly costs like software subscriptions, utilities, or supplies, paying only for what they actually use each month.

When a Loan Is Better

- Gives a fixed sum upfront for a specific purpose.

- Repayment is structured through fixed EMIs, making budgeting easier.

- Suitable for larger, planned expenses like buying a car, funding education, or home renovations.

Example: A working professional taking a personal loan to renovate their apartment can plan repayments over 12–24 months with predictable interest, avoiding surprise costs.

Choosing the right option ensures you pay only what you need, avoid unnecessary debt, and stay in control of your financial decisions.

Key Factors to Consider Before Choosing a Credit or a Loan

Before you decide, several factors can influence which option works best for your situation. Evaluating these carefully can prevent unnecessary costs and financial stress.

Before you decide, several factors can influence which option works best for your situation. Evaluating these carefully can prevent unnecessary costs and financial stress.

1. Purpose of Borrowing: Match Your Money to Your Goal

Knowing why you need money is the first step in deciding between credit and a loan. Credit works best for short-term, variable needs like sudden medical bills, urgent travel, or small home repairs. Loans are better suited for planned, larger expenses such as buying a car, funding higher education, or home renovations.

For example, a sudden medical bill of ₹15,000 can be handled with a credit card or digital line of credit, offering fast access without complex approvals. Planning a ₹5 lakh home renovation, however, calls for a personal loan with structured repayment and predictable interest.

Choosing the right tool for your purpose ensures financial discipline and avoids unnecessary stress.

2. Repayment Flexibility: Balance Control and Responsibility

Repayment flexibility differs significantly between credit and loans. Credit allows revolving borrowing where you can borrow, repay, and reuse up to your limit, often with minimum monthly payments. Loans require fixed EMIs over a set tenure, providing structure but less flexibility.

For instance, a ₹10,000 grocery expense on a credit card allows you to spread repayment across the month. A personal loan for the same amount commits you to fixed payments that could strain your budget if unexpected costs arise.

Understanding these differences helps you maintain liquidity while staying responsible.

3. Interest Rates and Overall Cost: Predictability versus Convenience

Loans usually offer predictable interest rates, often lower than credit, making it easier to plan your finances. Credit provides convenience but often comes with higher and variable interest rates. Carrying balances without paying in full can make credit substantially more expensive.

A ₹1 lakh personal loan at 12% per annum results in predictable EMIs over the tenure. Borrowing the same amount on a credit card at 36% annualised interest can double your debt in a few months if only minimum payments are made.

Knowing the cost structure helps you borrow wisely and avoid expensive debt traps.

4. Loan Amount and Credit Limits: Access versus Practicality

Loans provide higher sums, suitable for big, planned purchases. Credit limits are smaller and intended for short-term or emergency expenses.

A ₹5 lakh personal loan can fund a new car or an extensive home renovation. A credit card with a limit of ₹1–2 lakh may cover multiple small expenses but cannot support major purchases.

Using each option based on the amount needed prevents overleveraging and preserves financial health.

5. Application Process and Speed: Convenience versus Due Diligence

Credit is designed for speed. Pre-approved cards, digital lines of credit, and instant KYC approvals provide quick access to funds. Loans require more documentation, longer processing, and formal approvals.

A hospital bill of ₹20,000 can be paid immediately using a pre-approved credit card, while a personal loan might take one to three business days. Speed offers convenience, but loans provide a structured assessment, reducing the risk of borrowing beyond your means.

6. Risk and Debt Management: Discipline and Awareness

Every borrowing option carries risks. Loans’ fixed EMIs enforce discipline, but missing payments can hurt your credit score and incur penalties. Credit is flexible but can lead to overspending and high-interest debt if mismanaged.

Maxing out a credit card for multiple small purchases without planning can spiral into ₹50,000 debt with high interest. Missing one EMI on a ₹2 lakh personal loan impacts credit as well but is more predictable and easier to manage. Borrow within your repayment capacity to protect your financial health.

Also Read: 10 Smart Spending Tips For Financial Wellness

Common Mistakes People Make When Choosing Credit vs Loan

Even financially responsible people make avoidable mistakes when deciding between credit and a loan. The problem is rarely a lack of options. It is a lack of clarity. Here are the most common errors and how to avoid them.

Even financially responsible people make avoidable mistakes when deciding between credit and a loan. The problem is rarely a lack of options. It is a lack of clarity. Here are the most common errors and how to avoid them.

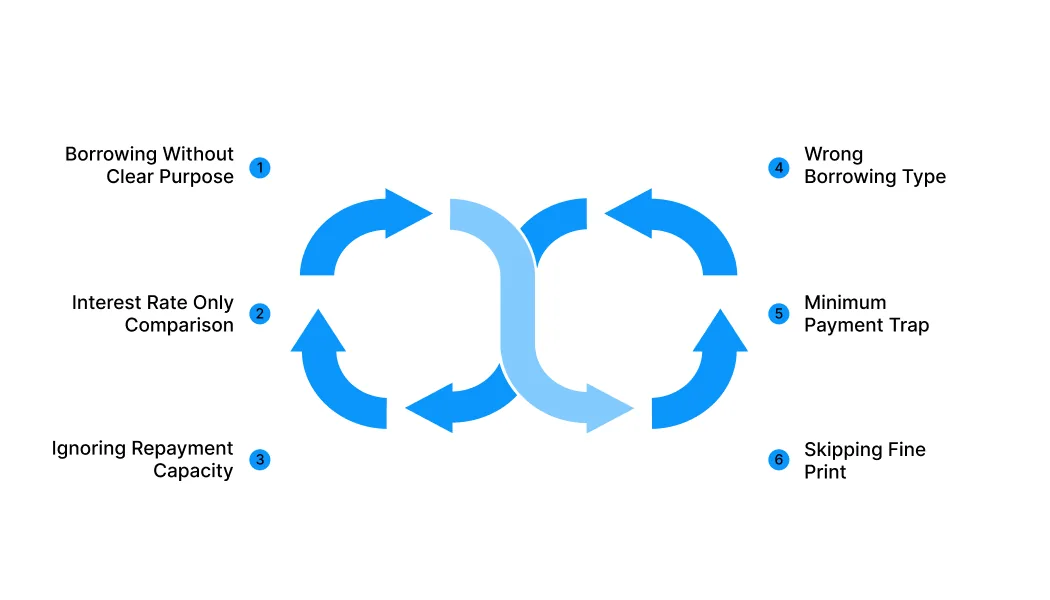

1. Borrowing Without a Clear Purpose

Risk: Taking credit or a loan simply because it is easily available can lead to unnecessary debt. Without a defined purpose, borrowed money often gets spent on non-essential expenses, making repayment feel heavier later.

Mitigation: Define the exact reason before borrowing. Ask yourself what problem this money is solving and whether the expense is urgent or value-creating. If the purpose is unclear, delay the decision.

2. Comparing Only Interest Rates

Risk: Many borrowers focus only on the interest rate and ignore processing fees, tenure length, penalties, and compounding structure. This can result in paying more than expected.

Mitigation: Calculate the total repayment amount, not just the monthly EMI. Review processing fees, late charges, and prepayment terms to understand the real cost of borrowing.

3. Ignoring Repayment Capacity

Risk: Choosing an EMI that stretches your monthly budget leaves little room for unexpected expenses. Even a small income disruption can create repayment stress.

Mitigation: Select a repayment amount that fits comfortably within your income after essentials and savings. Leave a buffer so your budget remains stable even if something changes.

4. Using the Wrong Type for the Timeline

Risk: Taking a long-term loan for a short-term expense increases total interest unnecessarily. Similarly, using high-interest revolving credit for long-term needs can become expensive.

Mitigation: Match the borrowing option to the duration of your need. Short-term gaps require short-tenure solutions, while structured long-term goals are better suited to fixed loans.

5. Relying on Minimum Payments in Credit

Risk: Paying only the minimum amount due on a credit line or card allows interest to accumulate on the remaining balance. Over time, this significantly increases the total repayment.

Mitigation: Create a fixed repayment schedule for yourself and aim to clear the outstanding balance as early as possible. Treat revolving credit as temporary support, not ongoing financing.

6. Skipping the Fine Print

Risk: Overlooking terms related to penalties, prepayment charges, or interest calculation methods can lead to unexpected costs.

Mitigation: Review all terms carefully before accepting. If something is unclear, clarify it first. Transparency at the beginning prevents financial stress later.

Need Flexible Credit Without the Hassle? Pocketly Makes It Simple

When you are stuck choosing between using a credit card or applying for a traditional loan, neither option may feel ideal. Credit cards can carry high interest if unpaid, while bank loans often require larger amounts, strict eligibility, and longer approval timelines.

For short-term needs, what you really need is flexibility, speed, and clarity.

Pocketly is built for exactly that. It offers small, short-term digital loans that help you manage urgent expenses without locking yourself into long-term debt.

Here is how Pocketly supports smarter borrowing:

- Borrow only what you need: With loan amounts ranging from ₹1,000 to ₹25,000, you stay in control of how much you take. This prevents unnecessary debt and keeps repayments manageable.

- Completely collateral-free: No assets, no guarantor, and no complicated paperwork. The process is designed to be simple and accessible, especially for students and young professionals.

- Quick approval with minimal documentation: A fast KYC-based verification system ensures that your application is processed rapidly without traditional banking delays.

- Instant transfer to your bank account: Once approved, the funds are credited directly to your account, making it useful for medical bills, travel needs, urgent payments, or unexpected expenses.

- Flexible repayment options: You can choose a repayment tenure that aligns with your cash flow, so EMIs fit comfortably into your monthly budget.

- Transparent and clear pricing: Interest rates start from 2% per month, with processing fees typically between 1% and 8% depending on your profile and loan amount. There are no hidden charges or surprise costs.

- 24/7 access through the mobile app: You can apply, monitor, and manage your loan anytime through the Pocketly app, giving you complete control over your borrowing.

Conclusion

Understanding the difference between credit and a loan gives you more than financial knowledge. It gives you control. In 2026, with so many borrowing options available, the real advantage lies in knowing when to use flexibility and when to choose structure.

Credit works best when you need short-term access and can repay quickly. Loans are better suited for planned, larger expenses that require predictable EMIs. The smarter move is not choosing one blindly, but matching the right tool to the right need.

Financial confidence comes from borrowing with intention, reviewing the true cost, and ensuring repayments fit comfortably within your budget.

And when life throws an unexpected expense your way, flexible digital options like Pocketly can help you bridge the gap without long-term disruption.

Ready to make smarter borrowing decisions? Download the Pocketly app today on [Android] or [iOS] and access short-term credit designed to keep you in control.

FAQs

1. What is the main difference between a credit and a loan?

Credit allows you to borrow up to a set limit and repay flexibly, and you can reuse the amount once it is repaid. A loan gives you a fixed lump sum with a structured repayment schedule over a specific period.

2. Is credit more expensive than a loan?

Credit, especially credit cards, often has higher interest rates if you carry forward balances. Loans usually have lower interest rates compared to revolving credit, but they come with fixed EMIs and longer commitments.

3. When should I choose credit instead of a loan?

Credit is suitable for short-term needs, smaller expenses, or temporary cash flow gaps when you can repay quickly and avoid high interest accumulation.

4. When is a loan a better option than credit?

A loan is better for large, planned expenses such as buying a car, funding education, or managing high medical costs, where you need a structured repayment plan.

5. Does using credit affect my credit score differently from a loan?

Yes. Credit impacts your credit utilisation ratio, while loans impact your repayment history and overall debt profile.

Responsible repayment in both cases can improve your credit score.

6. Can I use both credit and a loan at the same time?

Yes, but only if your income comfortably supports all repayments. It is important to ensure that your total monthly obligations remain manageable.