Have you ever applied for a loan through a digital platform and wondered how lenders manage the risk behind the scenes? While the process feels quick and simple, there are structured mechanisms that help make these loans possible.

One such concept is DLG (Default Loss Guarantee), a term often used in the fintech and lending ecosystem in India. It plays an important role in how digital lending platforms and financial institutions work together.

In this blog, you will understand the DLG full form, what it means in the Indian context, how RBI guidelines shape its usage, and real-world examples to make it easy to understand.

Key Takeaways

-

DLG, or Default Loss Guarantee, is a risk-sharing mechanism where fintech platforms cover a small portion of loan defaults, helping lenders offer credit more confidently.

-

It enables digital lending partnerships between fintech platforms and banks or NBFCs, especially for first-time or underserved borrowers.

-

DLG improves access, but not cost or responsibility, with lenders still bearing most of the risk and making independent decisions.

-

For you, the key is choosing loans with clear terms and repayment structures that match your financial situation.

What Is Default Loss Guarantee (DLG)?

DLG or Default Loss Guarantee is a risk-sharing arrangement where one party, usually a fintech platform, agrees to absorb part of the potential losses if borrowers fail to repay their loans.

In simple terms, DLG acts as a safety layer for lenders, encouraging them to offer loans more confidently, especially in digital lending models.

Default Loss Guarantee is commonly used in partnerships between fintech platforms and lenders such as banks or NBFCs in India's digital lending ecosystem.

In this arrangement, the roles are clearly defined:

-

The lender (bank or NBFC) provides the actual loan.

-

The fintech platform helps acquire and onboard customers.

-

The fintech may agree to cover a portion of the loss if a borrower defaults.

This structure allows lenders to expand credit access while managing risk in a more controlled way, especially when lending to new or underserved borrowers.

How DLG Works in India

To understand how Default Loss Guarantee works in practice, it helps to look at the full flow of a loan and where risk-sharing comes into play.

-

Step 1: A borrower applies for a loan through a digital platform: The process generally begins with an online application in which the borrower submits basic details such as income, employment, and identity verification.

-

Step 2: The platform assesses the application and connects with a lender: The fintech platform uses its risk models and data insights to assess the borrower and forwards the application to a partner bank or NBFC.

-

Step 3: The lender makes the final decision and disburses the loan: Even with DLG in place, the lender is responsible for approving and issuing the loan based on its own credit policies.

-

Step 4: Repayment begins as per the agreed terms: If the borrower repays on time, the transaction is completed normally, and the DLG arrangement is not triggered.

-

Step 5: If the borrower defaults, the DLG mechanism is activated: In case of non-repayment, the fintech platform covers a pre-agreed portion of the loss, as defined in its agreement with the lender.

-

Step 6: The remaining risk stays with the lender: The DLG only covers a limited percentage of the total loss, which means the lender still bears the majority of the risk.

This structure does not eliminate risk, but distributes it more efficiently, allowing lenders to expand credit access while maintaining control over potential losses.

RBI Guidelines on DLG

The Reserve Bank of India has issued specific guidelines to regulate Default Loss Guarantee (DLG) arrangements in digital lending. These rules are designed to make sure that risk-sharing does not lead to excessive or uncontrolled lending.

Here are the key aspects defined by RBI:

1. DLG Exposure Is Capped

RBI has placed a limit on how much risk can be covered under DLG arrangements.

-

The total DLG cover is capped at 5% of the loan portfolio.

-

This makes sure that lenders retain the majority of the risk.

This prevents over-reliance on guarantees and keeps lending decisions balanced.

2. Mandatory Formal Agreements

All DLG arrangements must be backed by legally enforceable agreements between the fintech platform and the regulated lender.

-

Terms of risk coverage must be clearly defined.

-

The extent of loss sharing must be documented.

This reduces ambiguity and guarantees accountability between parties.

3. Transparency and Disclosure Requirements

RBI mandates clear transparency in DLG structures.

-

All terms must be disclosed between the fintech and the lender.

-

Proper reporting and documentation must be maintained.

This makes sure that risk is visible and traceable within the system.

4. Lender Responsibility Cannot Be Transferred

Even with DLG in place:

-

Banks and NBFCs remain fully responsible for loan underwriting.

-

Credit decisions must be based on their own risk assessment.

DLG does not replace the lender's responsibility; it only supplements it.

5. DLG Must Be Backed by Valid Forms of Guarantee

RBI allows DLG to be provided only through approved forms, such as:

-

Cash deposits

-

Fixed deposits

-

Bank guarantees

This confirms that the guarantee is real and enforceable, not just a theoretical promise.

These guidelines make sure that DLG remains a risk-sharing tool rather than a way to shift risk entirely. They help maintain financial stability, prevent aggressive or reckless lending, and ensure accountability across fintech and lender partnerships.

Why DLG Matters in Digital Lending

DLG plays a key role in shaping how digital lending works in India by enabling a balance between wider credit access and responsible risk management.

-

Expands access to formal credit: By partially sharing default risk, DLG makes it easier for lenders to serve borrowers who may not have a long credit history. This helps bring more individuals into the formal financial system.

-

Enables fintech-lender collaboration at scale: It allows digital platforms and regulated lenders to work together more effectively, combining technology-driven customer acquisition with established lending frameworks.

-

Improves confidence in new borrower segments: In segments where data is limited or risk is uncertain, DLG provides an additional layer of assurance, encouraging lenders to make more inclusive credit decisions.

-

Supports faster and more efficient lending models: With structured risk-sharing in place, digital platforms can streamline processes, making loan access quicker without completely compromising on risk control.

-

Encourages disciplined underwriting despite risk-sharing: Even with DLG, lenders are required to evaluate borrowers independently. This guarantees that credit decisions remain based on actual risk assessment, not just the presence of a guarantee.

At the same time, regulatory oversight ensures that DLG continues to function as a support mechanism rather than a substitute for responsible lending practices.

Also Read: Applying for an Instant Personal Credit Line Online

Where You Actually See DLG in Real Life

Understanding Default Loss Guarantee becomes much clearer when you look at how it works in situations that reflect real borrowing behaviour.

Example 1: Fintech-NBFC Partnership (Portfolio Level)

A fintech platform partners with an NBFC to offer small personal loans to young professionals.

-

Total loan portfolio: ₹1 crore.

-

DLG agreement: 5%.

Now, assume borrowers default on ₹10 lakh:

-

The fintech covers up to ₹5 lakh (as per the DLG agreement).

-

The remaining ₹5 lakh loss is borne by the NBFC.

This reduces the lender's overall risk, making it more comfortable to offer loans at scale, especially to new-to-credit users.

Example 2: First-Time Borrower (Young Professional)

A salaried individual with limited credit history applies for a ₹20,000 loan through a digital lending app.

-

The lender has limited past data to assess risk.

-

Normally, this could lead to rejection or stricter conditions.

However, with a DLG arrangement in place:

-

The fintech shares part of the potential default risk.

-

The lender gains additional confidence to approve the loan.

For the borrower, this means access to credit that may not have been possible otherwise, even without a strong credit history.

Example 3: Irregular Income (Gig Worker or Freelancer)

A freelancer or gig worker applies for a ₹15,000 loan to manage a short-term cash gap.

-

Income may be inconsistent.

-

Traditional lenders may view this as higher risk.

With DLG:

-

The fintech helps bridge the trust gap.

-

The lender is more willing to approve the loan despite income variability.

This allows individuals with non-traditional income streams to access formal credit instead of relying on informal sources.

Example 4: Higher-Risk Borrower Segment

In segments where default risk is naturally higher:

-

Lenders may hesitate to expand lending.

-

Growth becomes limited due to risk concerns.

With DLG:

-

A portion of the potential loss is covered.

-

Lenders can cautiously expand into these segments.

Result:

-

More borrowers get access to credit.

-

Risk remains controlled and distributed.

Across all these scenarios, DLG does not eliminate risk; it redistributes it in a more structured and manageable way. This enables more inclusive lending decisions, expanding access to formal credit for underserved borrowers while supporting controlled growth within the lending ecosystem.

Exploring structured lending platforms like Pocketly can help you understand and access such credit options with greater clarity and confidence.

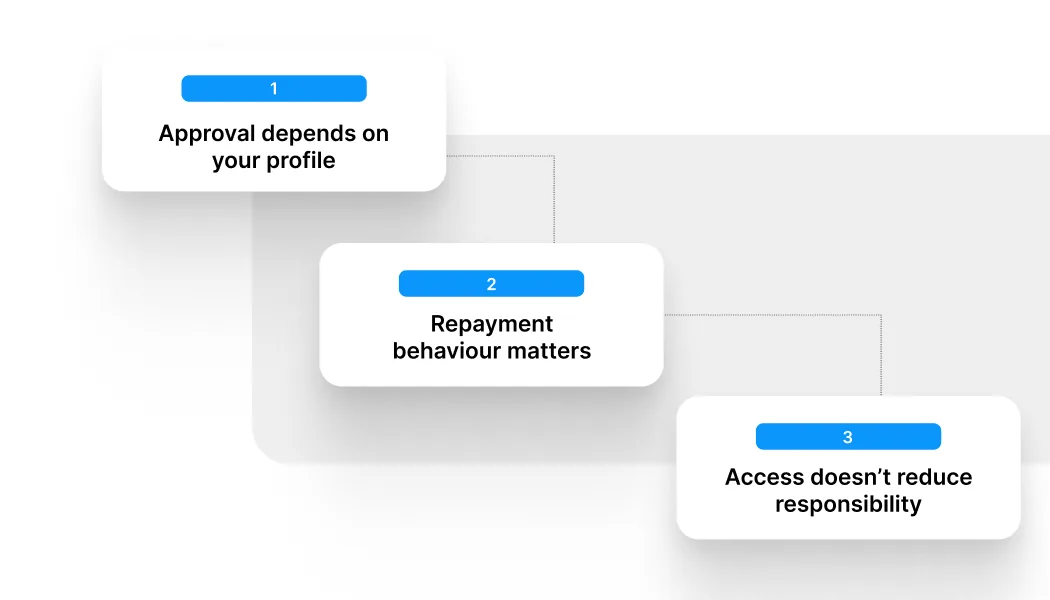

What This Means for Your Borrowing Decisions

While DLG helps lenders manage a portion of the risk, it does not eliminate it. The lender still bears the majority of the potential loss, and DLG only covers a limited share, which means lending decisions remain cautious and structured.

For borrowers, especially young professionals, students, and individuals with irregular income, this has a direct implication. Even if a loan is approved more easily due to backend risk-sharing, repayment responsibility does not change. Missed or delayed payments can still affect your credit profile and reduce your chances of accessing credit in the future.

In practical terms, this means that while DLG may improve access to loans, it does not reduce the cost of borrowing or the importance of repayment discipline. Poor borrowing behaviour can still create financial pressure and limit future opportunities.

Also Read: The Ultimate Guide to Small Business Loans in India (2026)

What DLG Does Not Change for You as a Borrower

While DLG supports digital lending in the background, it does not directly reduce the cost or responsibility for borrowers. For students, young professionals, and individuals managing tight or irregular cash flows, understanding these limitations is important before relying on any short-term credit option.

What This Means in Real Borrowing Situations

While DLG works in the background, its limitations can directly influence how your loan is approved, priced, and managed in real-life situations.

|

DLG Limitation |

What It Means for You |

Why It Matters |

|

Limited coverage |

Only a small portion of the loss is covered by the fintech |

Lenders still remain cautious when approving loans |

|

Not visible to borrowers |

You may not know if a loan has a DLG arrangement |

Approval does not mean reduced responsibility |

|

Regulatory dependency |

DLG operates under strict RBI guidelines |

Lending remains controlled and structured |

|

No direct benefit in pricing |

Interest rates and charges remain unchanged |

Your repayment cost does not reduce |

|

Risk still exists |

The lender bears most of the risk |

Your repayment behaviour still impacts future access |

In simple terms, while DLG may improve access to credit, it does not reduce your repayment responsibility or the overall cost of borrowing.

How This Connects to Your Borrowing Decisions

Even though DLG operates behind the scenes, it influences how lenders evaluate and offer loans. What matters most is how you approach borrowing decisions in real situations.

-

Lenders still assess your profile independently: This means approval depends on your income, credit history, and repayment capacity, not just the presence of a guarantee.

-

Your repayment behaviour remains critical: Consistent, on-time repayment strengthens your credit profile, while delays can limit future access to credit.

-

Access to credit does not reduce responsibility: Easier approval does not mean lower cost or lower obligation. Borrowing should still be aligned with your ability to repay.

In practical terms, this means taking a moment to assess whether the amount, repayment timeline, and overall cost fit your financial situation before borrowing.

Managing Short-Term Credit with Pocketly

Not every short-term financial need requires a complex setup. What matters is clarity in how you borrow and repay, especially when dealing with urgent expenses.

Platforms like Pocketly, which is not an NBFC itself, is a fintech startup dedicated to addressing the financial needs of young Indians, offering simple and transparent access to small, short-term credit. It works within regulated frameworks, partnering with RBI-registered NBFCs (Fairassets Technologies India Private Limited, NDX Financial Services Private Limited and Speel Finance Company Private Limited) to offer structured short-term credit options with transparent terms and clear repayment plans.

Here's how Pocketly supports better short-term borrowing:

-

Borrow between ₹1,000 and ₹25,000 based on your need.

-

No collateral or guarantor required.

-

Quick digital KYC process with 24/7 customer support.

-

Direct transfer to your bank account.

-

Flexible repayment options.

-

Transparent pricing with no hidden charges.

-

Interest starts from 2% per month, with processing fees between 1% and 8%.

-

24/7 access through the app.

This ensures that while systems like DLG support lending in the background, your borrowing experience remains simple, predictable, and easier to manage.

If you are exploring short-term credit, reviewing structured options like Pocketly can help you make more informed and controlled borrowing decisions.

Conclusion

As digital lending expands in India, systems like DLG will quietly shape how quickly and widely credit becomes available, especially for younger and first-time borrowers. The real shift is not just in access, but in how borrowing is designed to fit faster, more flexible financial needs.

For individuals managing dynamic income cycles or short-term cash gaps, the focus will increasingly move toward choosing options that offer clarity, flexibility, and predictable repayment structures.

Over time, the ability to assess not just whether you can borrow, but how well a loan fits your financial situation, will become more important than access alone.

Exploring structured borrowing options like Pocketly can help you approach short-term credit with more clarity and confidence. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. What is the full form of DLG in finance?

DLG stands for Default Loss Guarantee, a mechanism where a fintech platform agrees to cover a portion of potential loan losses for the lender.

2. Who provides DLG in India?

DLG is typically provided by fintech platforms, while regulated entities like banks or NBFCs remain responsible for issuing the loans.

3. Is DLG regulated by RBI?

Yes, the Reserve Bank of India has issued guidelines to ensure DLG arrangements are transparent, limited in scope, and used responsibly.

4. Does DLG improve your chances of getting a loan?

In some cases, yes. DLG can give lenders additional confidence, especially when evaluating first-time borrowers or those with limited credit history.

5. Does DLG affect your interest rate or loan cost?

No, DLG does not directly reduce interest rates or charges. It mainly impacts how risk is shared between the lender and the fintech platform.

6. Is DLG risky for borrowers?

DLG does not increase risk for borrowers directly, but it also does not reduce their responsibility. Timely repayment remains essential regardless of backend arrangements.