Running a small business is challenging enough without the added stress of managing cash flow gaps or needing extra funds for expansion. Whether it’s covering operational costs, upgrading equipment, or handling unexpected expenses, the financial strain can quickly become overwhelming. Without access to the right resources, businesses often find themselves juggling bills or delaying growth opportunities, leading to missed chances and increased stress.

But what if there was a way to get the funds you need, quickly and easily, without the hassle of paperwork and long approval processes? Small business loans can offer a viable solution, providing the financial flexibility to fuel growth and manage day-to-day expenses.

In this blog, we’ll explore the different types of small business loans, how they work, and how to choose the right one for your business needs.

Key Takeaways

- Small business loans provide financial support for entrepreneurs, helping them manage cash flow, fund growth, or purchase essential equipment.

- These loans come in various forms, such as term loans, working capital loans, and lines of credit, each designed for different business needs.

- Eligibility for small business loans typically depends on the business’s financial health, credit score, and years of operation.

- Costs include interest rates, processing fees, and potential penalties for early repayment, which can impact your total cost of borrowing.

- Carefully evaluate loan terms, including repayment flexibility, interest rates, and fees, to choose the best option that aligns with your business goals.

What Are Small Business Loans?

A small business loan is a financial product designed to provide funding for businesses to cover operational costs, fuel growth, or manage cash flow gaps. These loans can be used for a variety of needs, including buying inventory, upgrading equipment, expanding operations, or even covering emergency expenses.

Unlike personal loans, small business loans are tailored to meet the unique needs of business owners, offering a variety of repayment terms and interest rates. With small business loans, business owners can access the capital they need without depleting personal savings or seeking external investments.

These loans are often easier to get than traditional bank loans, with more flexible terms and quicker approval processes, especially through digital lenders.

Why Small Business Loans Matter for Entrepreneurs

For entrepreneurs and small business owners, having access to the right loan can be a game-changer. Here’s why small business loans are crucial:

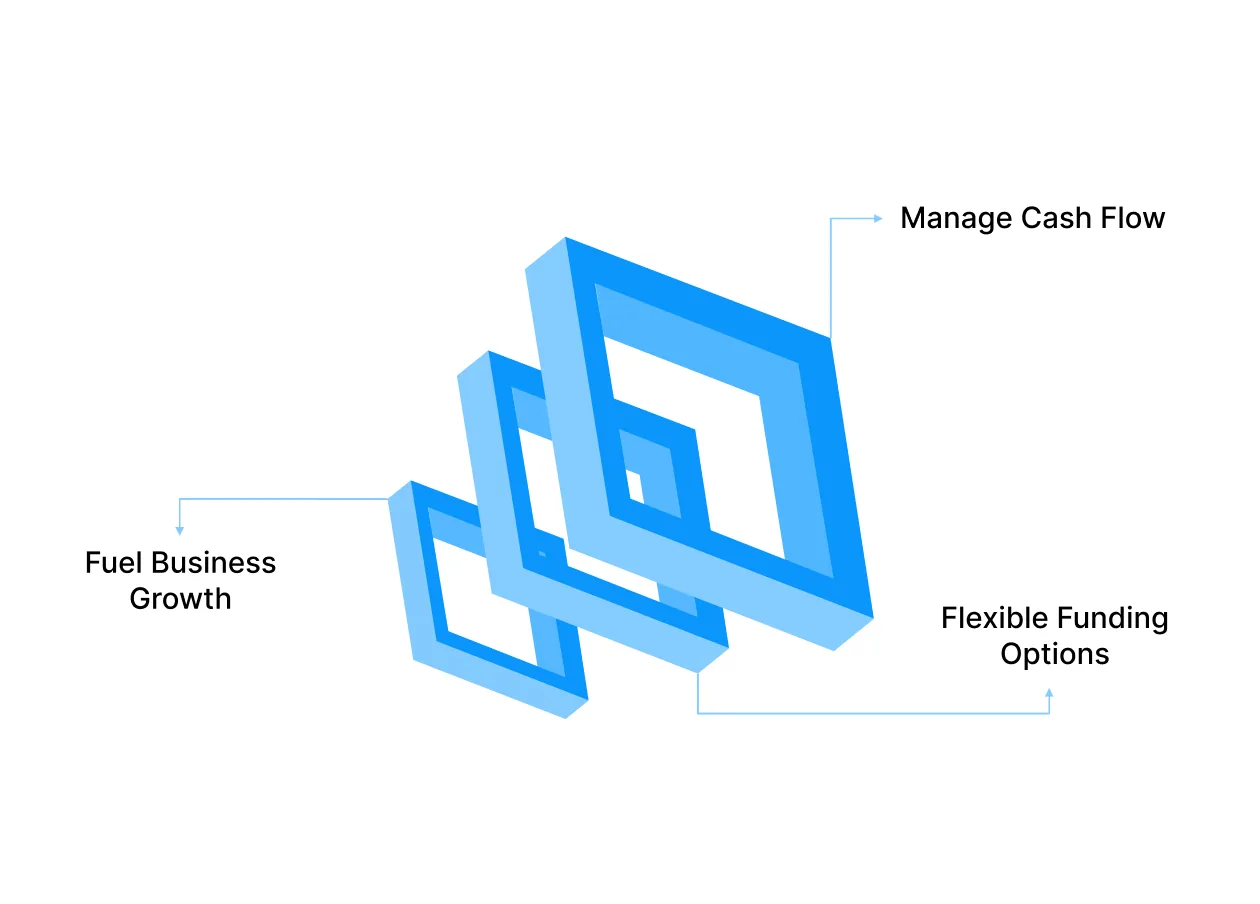

- Fuel Business Growth: Small business loans provide the funding necessary to expand, whether that means hiring new employees, entering new markets, or upgrading your technology. This can make all the difference in a competitive market.

- Manage Cash Flow: Seasonal dips, unexpected expenses, or delayed payments can leave a business struggling to cover operational costs. A small business loan can bridge these gaps, allowing you to maintain operations without disruption.

- Flexible Funding Options: From short-term working capital loans to longer-term growth loans, small business loans offer a range of options. With these loans, you can modify your repayment schedule to your cash flow and financial goals.

By securing a small business loan, you’re not only ensuring your business remains operational but also setting it up for future success and stability.

Now, let's take a closer look at the different types of small business loans available and how they can benefit your business.

Types of Small Business Loans Available

When it comes to financing your business, there isn’t a one-size-fits-all solution. Small business loans come in various forms, each designed to meet distinct needs and offer different terms. Understanding the various types can help you choose the best loan for your business goals.

1. Term Loans

Term loans are one of the simplest and most widely used types of small business loans. They provide a lump sum amount of capital that is repaid over a fixed period, normally with regular monthly payments. This type of loan is often used for significant, long-term investments like expanding your business, purchasing equipment, or even refinancing other debt.

For example, if your business wants to expand into a new location or purchase machinery, a term loan could provide the upfront capital needed, with predictable payments over the course of several years.

The fixed nature of the repayment schedule helps businesses plan their finances, making it a reliable option for those with well-defined growth strategies.

2. Working Capital Loans

Working capital loans are created to help businesses cover their day-to-day operational expenses. Whether it’s managing payroll, buying inventory, or paying bills, these loans offer short-term relief without the long-term commitment of traditional loans. Unlike term loans, working capital loans typically do not require collateral, making them more accessible for smaller businesses that may not have significant assets to pledge.

For example, a retail business might use a working capital loan to manage the fluctuating costs of inventory or seasonal variations in sales. This short-term funding allows businesses to maintain operations smoothly without getting bogged down by cash flow issues.

3. Business Lines of Credit

A business line of credit provides businesses with access to a fixed amount of credit, which they can borrow from, repay, and borrow again as needed. It offers much more flexibility than a traditional loan, as businesses can draw funds at any time within the approved credit limit. Interest is only billed on the amount borrowed, making it an ideal option for businesses with fluctuating financial needs.

For example, a business experiencing inconsistent monthly cash flow could use a business line of credit to cover expenses during slow months and repay the balance when revenue picks up. This flexibility can be particularly beneficial for small businesses or startups that face frequent cash flow fluctuations.

4. Invoice Financing

Invoice financing is a prominent option for businesses that deal with long payment cycles. It allows businesses to borrow against unpaid invoices, freeing up cash that would usually be tied up until customers pay. This type of financing helps businesses bridge the gap between issuing invoices and receiving payment, improving cash flow without taking on significant debt.

For example, a freelance graphic design company may have several large projects with 30–60 day payment terms. By using invoice financing, they can get immediate access to the majority of the invoice amount, ensuring they have enough capital to pay their employees and manage other expenses while waiting for client payments to come through.

5. Equipment Financing

Equipment financing is a specialised loan designed for businesses looking to purchase or lease equipment. This type of loan relies on the equipment itself as collateral, making it easier to secure financing for businesses that don’t have major assets or established credit histories. These loans are typically offered with flexible repayment options and lower interest rates since the equipment acts as a guarantee for the loan.

For example, a construction company might use equipment financing to purchase a new crane or bulldozer. The equipment would serve as collateral, allowing the company to secure the necessary funding without putting other assets or personal guarantees on the line.

6. Merchant Cash Advance

A merchant cash advance (MCA) is a type of funding where businesses receive a lump sum payment in return for a percentage of their future sales. Unlike traditional loans, the repayment is tied directly to your business's daily credit card transactions, meaning repayments fluctuate based on your sales volume.

For example, a restaurant with high but fluctuating sales might opt for a merchant cash advance to cover unexpected expenses. During busy periods, the repayments would be higher, and during slow periods, the repayments would naturally adjust, providing a flexible repayment structure suited to variable income streams.

Also Read: Minimum Credit Score Required For Personal Loan

How to Choose the Right Small Business Loan for Your Needs

Choosing the right small business loan is critical to meeting your specific financial goals. Here’s a step-by-step guide to help you navigate the process and select the best loan option for your business:

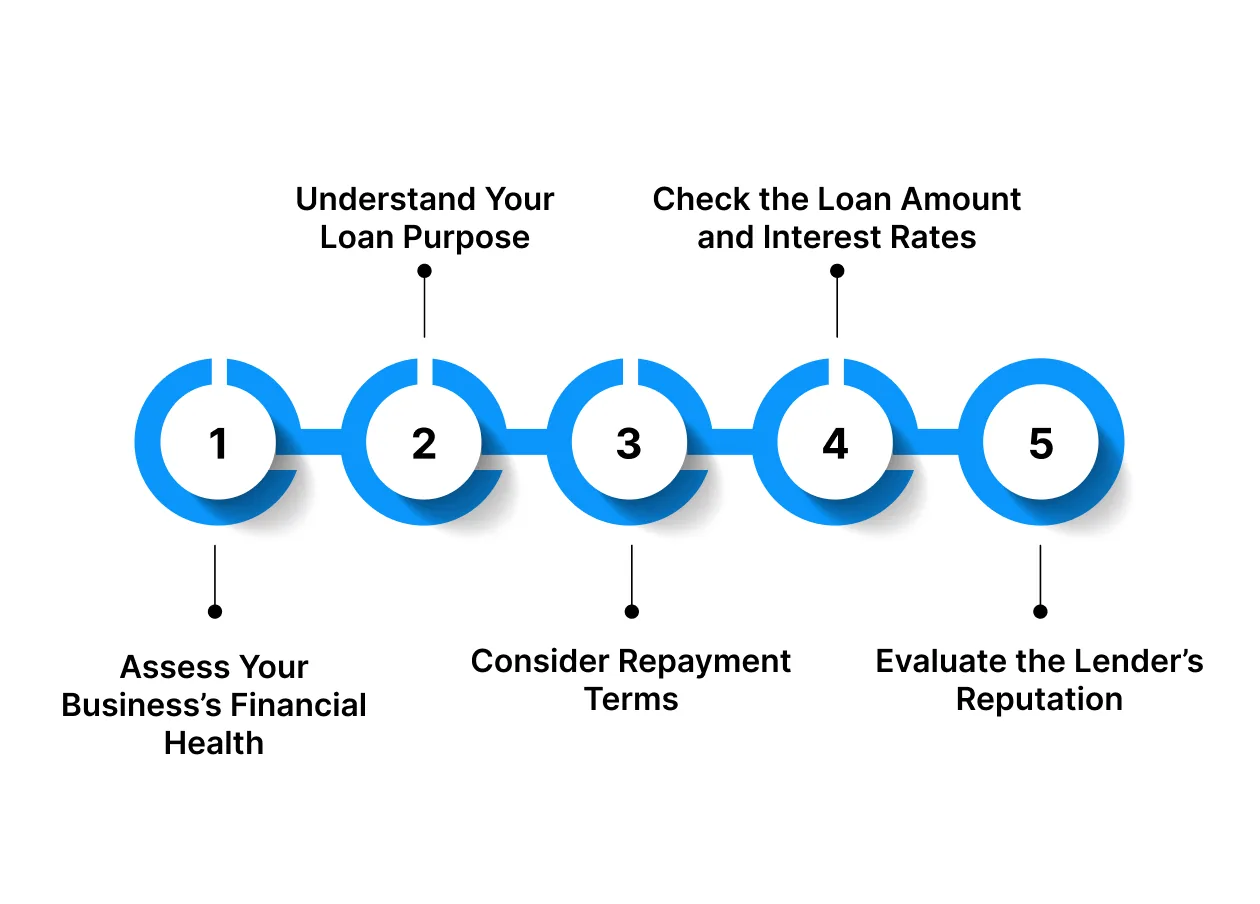

1. Assess Your Business’s Financial Health

To choose the right loan, you first need to understand your business's financial position. Start by reviewing:

- Cash flow: How much money is coming in vs. going out?

- Current debt: Do you have existing liabilities that might affect your ability to take on new debt?

- Profit margins: Are your margins stable enough to manage loan repayments?

Having a clear picture of your financial health will help you choose between short-term loans and long-term financing.

2. Understand Your Loan Purpose

Each loan type is created for a specific purpose. Know your business’s needs before selecting a loan:

- Working Capital Loan: For covering daily operational expenses.

- Term Loan: Ideal for long-term investments like expansion or equipment purchase.

- Business Line of Credit: Flexible funding to manage cash flow fluctuations.

Identifying the purpose behind the loan will help you choose the right loan product that best fits your business.

3. Consider Repayment Terms

Repayment terms vary greatly depending on the loan type. You should consider how the repayment schedule will align with your business cash flow:

- Fixed Terms (Term Loans): Set monthly repayments that work well for predictable income.

- Flexible Terms (Business Lines of Credit): Repay as you go, with more flexibility for fluctuating revenues.

Choose the loan with terms that match your business's ability to repay, without straining your cash flow.

4. Check the Loan Amount and Interest Rates

Make sure the loan amount aligns with your needs. Also, compare interest rates and fees:

- Loan Amount: Borrow only what you require to avoid unnecessary debt.

- Interest Rates: Lower interest rates reduce overall costs. Compare rates from different lenders to get the best deal.

- Fees: Look for any hidden fees like processing charges or prepayment penalties.

Carefully evaluate loan amounts, rates, and fees to ensure you’re not overpaying for the funds you need.

5. Evaluate the Lender’s Reputation

A reputable lender will provide clear terms, good customer support, and transparent processes. When choosing a lender, consider:

- Customer Reviews: Look for online feedback and testimonials to gauge the lender’s credibility.

- Support: Look for a lender who offers helpful customer support and transparent communication.

- Reputation: Choose a lender with a solid track record of helping small businesses succeed.

Evaluating lenders based on their reputation ensures you are working with a trustworthy partner who will guide you through the loan process.

Also Read: Understanding the Process And Meaning of Credit Control

Eligibility Criteria for Small Business Loans: A Checklist

When applying for a small business loan, it's essential to meet certain eligibility criteria. Here’s a checklist to help you understand the key requirements:

1. Business Age

- Minimum Requirement: 6 months to 2 years of operation.

- Why it Matters: Lenders want to ensure your business is stable enough to repay the loan.

2. Annual Revenue

- Minimum Requirement: ₹1,00,000 to ₹10,00,000 per year (varies by lender and loan type).

- Why it Matters: Your business needs a steady cash flow to handle loan repayments.

3. Credit Score

- Minimum Requirement: Typically above 650 for favourable loan terms.

- Why it Matters: A good credit score indicates to lenders that you can manage credit responsibly.

4. Business Type

- Consideration: Certain industries (e.g., IT, retail) are preferred by some lenders.

- Why it Matters: Lenders assess the stability and predictability of cash flow in different industries.

5. Collateral

- Requirement: May be required for secured loans (e.g., property, equipment).

- Why it Matters: Collateral lowers the risk for lenders by ensuring they have an asset to claim if you default.

6. Debt-to-Income Ratio (DTI)

- Target: A low DTI ratio is favourable.

- Why it Matters: A low DTI indicates that your business isn’t overburdened with debt, making it more likely you can handle additional loan repayments.

Costs and Fees Associated with Small Business Loans

Before taking out a small business loan, it’s crucial to recognise the costs and fees involved, as they can significantly impact your business’s financial health. Here’s a breakdown of the typical costs and fees associated with small business loans:

1. Interest Rates

Interest rates are one of the most important factors when considering a small business loan. They directly affect how much you'll pay over the life of the loan. Understanding interest rates can help you make a more informed decision, and a business loan platform can assist by:

- Comparing rates from multiple lenders: Get access to competitive rates by comparing offers from different financial institutions.

- Providing a clear breakdown of costs: Platforms often offer easy-to-read breakdowns of interest rates, helping you understand the total cost of borrowing.

For businesses, these tools are essential in helping you select a loan that fits within your budget and avoids overpaying.

2. Processing Fees

Processing fees can quickly add up and increase the cost of your loan. Understanding how they work can prevent surprises and unnecessary expenses. A loan management platform helps by:

- Estimating total loan costs: With a clear summary of fees upfront, you’ll know exactly how much the loan will cost after all charges are included.

- Making fee comparison simple: The platform consolidates various fee structures, so you can choose the most affordable option for your business needs.

These platforms ensure that you’re aware of all additional costs before committing to a loan, giving you full control over your financial decisions.

3. Prepayment Penalties

Paying off your loan early might seem like a good idea, but prepayment penalties can reduce the financial benefit of doing so. A loan platform helps by:

- Alerting you to prepayment terms: Stay informed about potential penalties before making extra payments.

- Offering flexible repayment options: Some platforms provide alternatives that allow for early repayments without penalties.

Understanding these penalties and avoiding them can help your business save money in the long run.

4. Late Payment Fees

Late payments on business loans can incur additional charges and negatively affect your financial stability. Loan management platforms help by:

- Setting up reminders for payment due dates: Stay on top of your loan payments with automated reminders.

- Tracking missed payments: Easily track when payments are due, reducing the risk of missed deadlines.

By using these tools, you can prevent late fees, maintain a good payment history, and avoid unnecessary costs.

5. Collateral Costs (For Secured Loans)

If your loan requires collateral, you need to understand the risks involved in pledging assets. Loan platforms assist by:

- Providing collateral requirements upfront: Know what assets are needed before you apply for a loan.

- Helping assess collateral value: Some platforms offer tools to evaluate whether your assets are worth the loan amount.

For businesses, being aware of collateral requirements ensures you’re prepared and able to secure the loan without jeopardising valuable assets.

Risks of Small Business Loans and How to Mitigate Them

While small business loans can be a great tool for growth and financial management, they do come with certain risks. It’s essential to know these risks and take proactive steps to mitigate them to ensure your business remains financially stable.

1. High-Interest Rates

Risk: High-interest rates can significantly increase the total cost of borrowing, especially for unsecured loans or loans from non-traditional lenders. These higher rates can lead to larger repayments and financial strain on your business.

Mitigation: Compare rates from multiple lenders before choosing a loan, ensuring you find the most competitive option. Opt for loans with fixed interest rates, which can provide stability and help you plan your finances more effectively.

2. Impact on Cash Flow

Risk: Loan repayments, especially with larger sums, can create a cash flow burden, particularly if your business experiences seasonal revenue fluctuations. This can restrict your capacity to invest in day-to-day operations and growth opportunities.

Mitigation: Borrow only the amount you need, and ensure the loan terms align with your business’s cash flow. Choose flexible repayment schedules, and if possible, opt for a loan with a grace period during slow revenue months.

3. Collateral Risk (For Secured Loans)

Risk: When you pledge assets as collateral for a secured loan, you are at risk of losing them if the loan isn’t repaid, potentially disrupting business operations and causing long-term financial damage.

Mitigation: Carefully assess the collateral requirements before committing. Opt for unsecured loans when possible to protect your business assets, or use only low-risk assets if collateral is a necessity.

4. Debt Overload

Risk: Taking on multiple loans or large amounts of debt can lead to a debt overload, where your business struggles to make repayments, resulting in a damaged credit score and fewer options for future financing.

Mitigation: Limit the number of loans you take and focus on repaying existing debts before taking on new ones. Use debt management strategies, such as consolidating loans or prioritising high-interest debts first, to reduce financial pressure.

5. Missed Repayments and Late Fees

Risk: Missing loan payments or making late payments can result in late fees, penalties, and a negative impact on your credit score, which can restrict future access to financing and increase the overall cost of your loan.

Mitigation: Set up reminders or automate payments to ensure that your payments are made on time. Regularly monitor your loan schedule and make sure you have enough funds to cover your repayments.

How to Apply for a Small Business Loan: A Step-by-Step Guide

Applying for a small business loan can be a straightforward process if you approach it with the right steps in mind. Here’s a step-by-step guide to help you through the application process, ensuring you increase your chances of success.

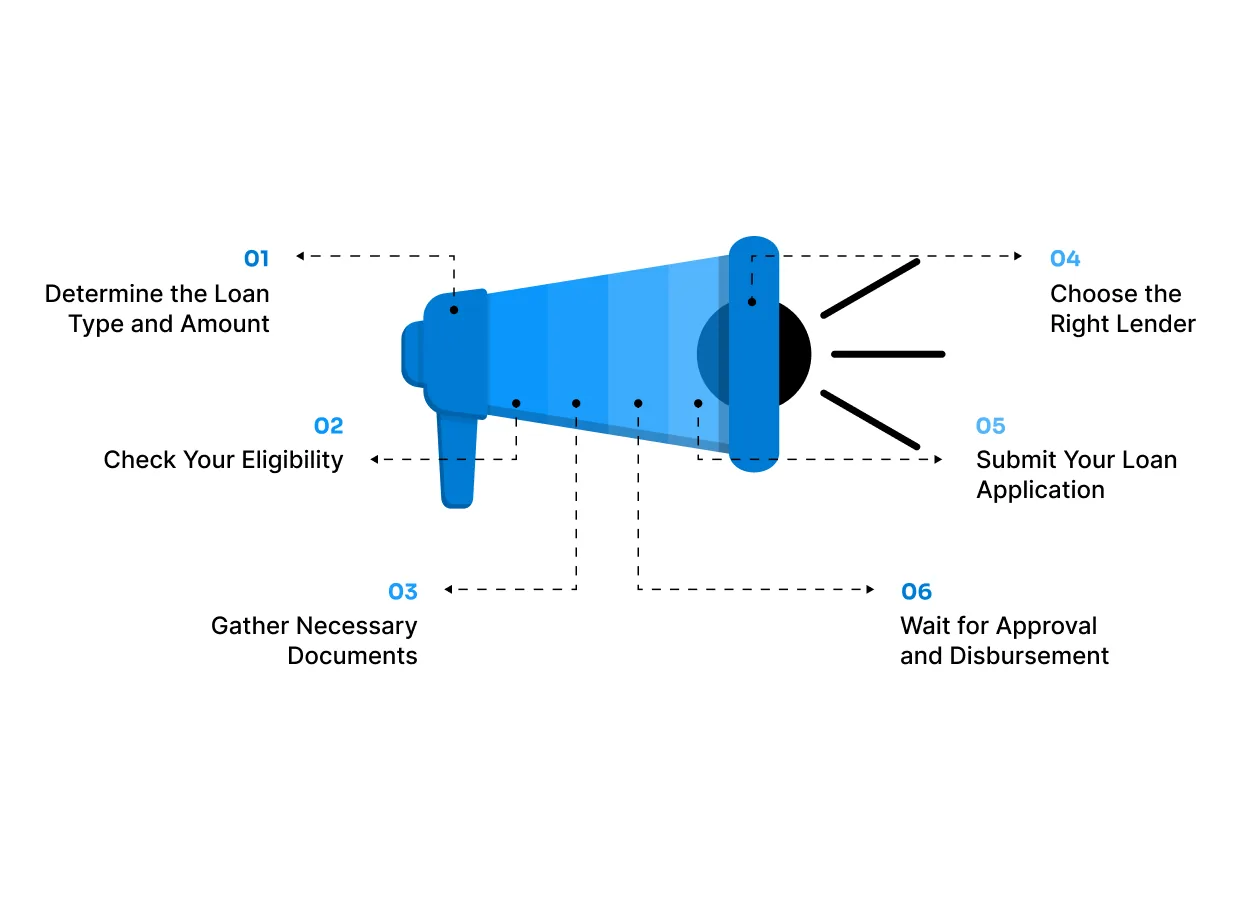

Step 1: Determine the Loan Type and Amount

- Identify the Loan Purpose: Clearly define what you need the loan for (e.g., working capital, equipment purchase, expansion).

- Calculate the Loan Amount: Be realistic about how much money you need, ensuring you don’t borrow more than necessary.

Step 2: Check Your Eligibility

- Review Lender’s Criteria: Ensure your business meets the eligibility requirements, such as:

- Minimum operational history (e.g., 6 months to 2 years).

- Annual revenue requirements.

- Credit score thresholds.

- Availability of collateral for secured loans.

Step 3: Gather Necessary Documents

Prepare the following paperwork for your loan application:

- Financial Documents: Gain and loss statements, balance sheets, tax returns.

- Business Plan: A clear outline of your business goals and how the loan will be used.

- Bank Statements: To demonstrate your business's financial health.

- Identification Documents: PAN card, Aadhaar card, address proof, etc.

Step 4: Choose the Right Lender

- Compare Lenders: Consider whether you want to apply through a bank, a financial organisation, or an online lender.

- Traditional Banks: Often provide longer loan terms but may have strict eligibility criteria.

- Online Lenders (Fintech): Offer quicker approvals and more flexible requirements but may come with higher interest rates.

Step 5: Submit Your Loan Application

- Fill Out the Application: Submit your loan application online or in person, depending on the lender. Ensure all information is accurate to prevent delays.

- Review Loan Terms: Make sure you comprehend the loan terms, such as interest rates, repayment dates, and any fees.

Step 6: Wait for Approval and Disbursement

- Loan Approval: The lender will scrutinise your application, verify the provided documents, and make a decision.

- Receive Funds: Once approved, the lender shall send the loan amount to your business account as per the agreed terms.

By following these steps, you can navigate the loan application process more efficiently, ensuring you have the necessary documents and meet the criteria for approval.

Tips to Improve Your Chances of Loan Approval

Securing a small business loan may be difficult, but with the right steps, you can increase your chances of approval. Here are some key tips to help you strengthen your application and get the funding your business needs:

Maintain a Strong Credit Score

A good credit score is one of the most important factors in securing a small business loan. By keeping your credit score above 650, you improve your likelihood of approval and receiving better loan terms. Staying on the forefront of your credit score will help you avoid:

- Higher interest rates due to poor credit history.

- Limited loan options, as lenders may be hesitant to approve loans with a low score.

- Consistently managing your credit and making timely payments will enhance your financial reputation and increase your borrowing potential.

Prepare Financial Statements

Having up-to-date and accurate financial statements is crucial for loan approval. Lenders rely on these papers to assess the financial health of your business. By keeping complete and precise records, you can avoid:

- Delays in approvalare caused by incomplete or unclear financial data.

- Rejection of the loan if your business’s financial health is unclear.

- Clear and well-maintained financial documents reassure lenders that your business is stable and able to handle loan repayments.

Have a Clear Business Plan

A well-structured business plan helps lenders understand your business goals and how you plan to use the loan. A detailed plan demonstrates that you’ve thought about the future of your business. Without a solid plan, you risk:

- Uncertainty in the loan purpose may cause lenders to hesitate.

- Missed opportunities for growth that the loan could help finance.

- Having a clear and realistic business plan will show lenders your business's potential for success and help you secure funding for growth.

Show Consistent Cash Flow

Lenders want to see that your business has consistent revenue and cash flow, which assures them that you can handle the loan repayments. A strong cash flow helps prevent:

- Loan denial due to concerns about your ability to repay.

- Financial stress from being unable to manage monthly payments.

- Tracking your cash flow regularly will give you the financial insight needed to prove your ability to manage business expenses and repay loans.

Offer Collateral (If Possible)

Offering collateral for a secured loan can increase your chances of approval, as it reduces the lender's risk. By providing valuable assets, you can avoid:

- Higher interest rates are due to the perceived risk of an unsecured loan.

- Rejection of your loan application if your business doesn’t meet all the eligibility criteria.

- Offering collateral provides security for the lender and can improve your chances of receiving favourable loan terms.

How Pocketly Supports Your Small Business Loan Journey

Managing the process of securing a small business loan can be complex, but sometimes businesses face unexpected cash flow gaps even after securing financing. This is where Pocketly adds value, providing quick and flexible short-term loans that complement your long-term financing strategy.

Here’s how Pocketly supports your business needs:

- Quick Access to Funds: Pocketly offers small loans ranging from ₹1,000 to ₹25,000 to help businesses bridge temporary financial gaps. Whether you’re dealing with late invoices, unexpected bills, or seasonal revenue fluctuations, Pocketly ensures you have the cash to keep things running smoothly.

- Fast Digital Application Process: Pocketly’s user-friendly app allows you to apply for loans quickly with a simple KYC and approval process. You can get approved and have funds transferred into your business account in just a few minutes—no long waits or complicated paperwork.

- Transparent Terms and Fees: Pocketly offers clear and upfront terms, with interest rates starting at 2% per month and processing fees between 1% and 8% of the loan amount. With no hidden charges, you know exactly what to expect before you take the loan.

- Prevent Cash Flow Disruptions: If your business needs immediate capital for inventory or operational costs, Pocketly helps you avoid disruptions. The flexibility to cover urgent expenses ensures you can maintain smooth operations without the stress of cash flow issues.

Download the Pocketly App today and access the short-term financial support your business needs to grow and thrive.

Conclusion

Navigating the world of small business loans may seem overwhelming, but with the right knowledge and planning, it becomes an invaluable tool for growth. From securing working capital to funding business expansions, the right loan can unlock new opportunities and drive success.

As small business owners continue to explore financing options, the focus will shift towards choosing the right loan type based on specific needs, understanding costs, and planning for repayment. With so many options available, it’s crucial to choose wisely to ensure long-term financial health.

For businesses seeking quick, flexible funding, Pocketly offers a solution. With minimal documentation, fast approvals, and no collateral required, Pocketly ensures that you can cover short-term cash flow gaps without stress. Ready to take the next step in your business journey?

Download the Pocketly app on iOS or Android to access quick, hassle-free loans and keep your business moving forward.

FAQs

1. What is a small business loan?

A small business loan is a financial product intended to help small enterprises access funding for business expenses such as working capital, equipment, or growth initiatives. These loans can be unsecured or secured and are provided by banks, NBFCs, and online lenders.

2. How much can I borrow with a small business loan?

Loan sums vary depending on the lender and the type of loan. Small businesses can typically borrow amounts ranging from ₹10,000 to ₹50,00,000 or more, depending on their needs, creditworthiness, and the lender’s policies.

3. Do I need collateral to get a business loan?

It depends on the type of loan. Some loans, such as term loans, may require collateral, while others, like working capital loans or unsecured loans, may not require any collateral. Lenders assess the loan amount and risk factors when deciding on collateral requirements.

4. How long does approval take for a small business loan?

Approval procedures can differ based on the lender. Traditional banks may take a few weeks, while online lenders or platforms like Pocketly can offer approval in just a few hours to a few days, especially for smaller, short-term loans.

5. Can new businesses get small business loans?

Yes, new businesses can qualify for small business loans, though they may face higher scrutiny and more stringent eligibility criteria. Lenders typically look for a solid business plan, personal credit score, and potential for future cash flow before approving loans for new ventures.