Unexpected expenses can hit hard, such as a sudden medical bill, an urgent car repair, or a surprise travel need. Without a financial buffer, these moments can derail your month, force you into debt, and leave you stressed. The constant worry of “what if something happens?” can quietly affect every financial decision you make.

An emergency fund solves this problem. It’s a dedicated stash of money designed to cover life’s surprises, giving you freedom and confidence to handle the unexpected without panic. With the right strategy, you can build a fund that protects you, keeps you on track with your goals, and turns financial uncertainty into peace of mind.

This blog will show you how to calculate the right amount, start saving smartly, and grow your emergency fund so that when life throws curveballs, you’re prepared, secure, and stress-free.

TL;DR

- Life is unpredictable, and unexpected expenses like medical bills, urgent repairs, or sudden travel can disrupt your budget.

- An emergency fund acts as a safety net, ideally covering 3–6 months of essential expenses, protecting you from debt and financial stress.

- Build your fund gradually: calculate essentials, automate monthly savings, and channel bonuses or extra income into it.

- Store your emergency fund in liquid, low-risk accounts such as high-yield savings or liquid mutual funds, separate from daily spending.

- For short-term gaps beyond your fund, solutions like Pocketly provide quick, responsible loans, letting your emergency savings stay intact.

What Is an Emergency Fund?

An emergency fund is money set aside specifically to handle unexpected financial situations. It is different from regular savings or investments because its sole purpose is to provide a safety net, not to fund planned goals.

Examples of situations where an emergency fund comes in handy include:

- Sudden medical expenses

- Urgent car or home repairs

- Job loss or sudden drop in income

- Unexpected travel or family emergencies

For young professionals in India, the amount needed in an emergency fund usually covers 3–6 months of essential expenses, giving you a buffer to manage life’s surprises without relying on loans or credit cards.

Note: Building an emergency fund creates financial stability and peace of mind, ensuring that unexpected costs don’t derail your long-term plans.

Why You Absolutely Need an Emergency Fund?

An emergency fund is your financial safety net, a stash of money set aside exclusively to handle unexpected expenses. Life is unpredictable, and without a dedicated fund, even small surprises can upset your budget, increase stress, or push you into high-interest debt.

An emergency fund is your financial safety net, a stash of money set aside exclusively to handle unexpected expenses. Life is unpredictable, and without a dedicated fund, even small surprises can upset your budget, increase stress, or push you into high-interest debt.

Here’s why every young professional in India should prioritise building an emergency fund:

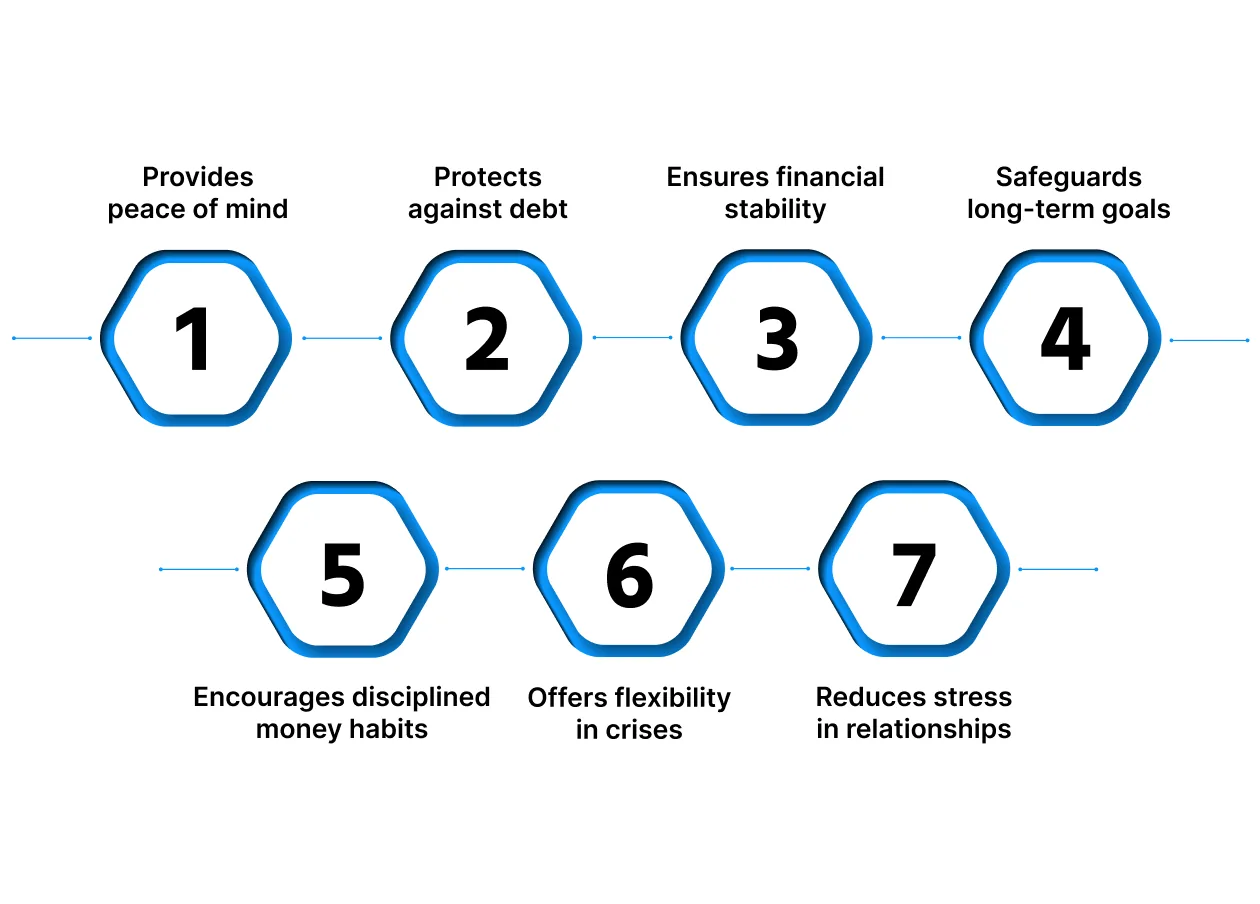

- Provides peace of mind: Knowing that you have money reserved for emergencies reduces anxiety and allows you to focus on your work, studies, or personal goals without constant financial worry.

- Protects against debt: Unplanned expenses, like medical emergencies, car repairs, or sudden travel, won’t force you to rely on credit cards or loans with high interest rates.

- Ensures financial stability: Life events such as job loss, delayed freelance payments, or unexpected bills can disrupt your monthly budget. An emergency fund helps you cover essentials like rent, groceries, and utilities without compromising your lifestyle.

- Safeguards long-term goals: By handling short-term crises, your emergency fund prevents you from dipping into savings meant for investments, buying a house, or funding further education.

- Encourages disciplined money habits: Regularly contributing to an emergency fund builds savings discipline, encourages prioritisation, and strengthens your overall financial planning skills.

- Offers flexibility in crises: Emergencies aren’t only financial urgent travel, relocation, or sudden family needs can be managed smoothly when you have cash ready.

- Reduces stress in relationships: Money stress is one of the top causes of conflict in households. A ready emergency fund allows you to handle surprises without putting pressure on your partner or family.

Real-life example: Your motorbike suddenly breaks down, requiring a ₹10,000 repair. Without an emergency fund, you might put it on a credit card or borrow from friends, adding stress and interest. With a dedicated fund, you can pay immediately, keep your budget intact, and stay worry-free.

How Much Should You Save in Your Emergency Fund?

Determining the right size of your emergency fund depends on your lifestyle, income stability, and monthly expenses. The goal is to have enough to cover essential costs for a period when income is disrupted, without overcommitting money you might need for other goals.

Cover 3 to 6 Months of Basic Expenses

Your emergency fund should ideally cover three to six months of essential living costs such as rent, groceries, utilities, EMIs, and healthcare. This ensures that even if your income stops suddenly, you can continue living without financial stress.

For example, if your monthly essentials total ₹25,000, a 3-month buffer would be ₹75,000, while a 6-month buffer would be ₹1,50,000. This cushion is especially important for young professionals in metro cities like Bengaluru or Mumbai, where living costs are high and sudden expenses like medical emergencies or urgent travel can quickly derail finances.

Factor in Job Security and Income Stability

How stable your income is should determine the size of your emergency fund. Full-time employees with predictable salaries may need a smaller buffer, while freelancers, gig workers, or those with variable income should aim for a larger fund to cover periods without earnings.

For instance, a freelancer earning ₹40,000 one month and ₹60,000 the next should aim for at least six months of expenses in their fund, while someone in a secure corporate job may start with three months. Understanding your risk exposure helps you prepare for income gaps more realistically.

Include Irregular and Annual Expenses

Many expenses don’t occur monthly but can significantly affect your budget if unplanned. These include insurance premiums, festival shopping, annual subscription fees, property taxes, and travel costs. Incorporating these into your emergency fund ensures you’re not caught off guard.

For example, if your annual health insurance premium is ₹12,000, you can allocate ₹1,000 monthly to your emergency fund, ensuring you have the money ready when it’s due. Breaking down irregular costs into monthly contributions prevents these from becoming sudden financial shocks.

Account for Dependents

If you financially support family members, adjust your emergency fund to cover their essential expenses as well. Your fund should reflect the total household costs, not just your personal living expenses.

For example, if you support a parent and a sibling with ₹15,000 in monthly essentials combined, and your own essentials are ₹25,000, your emergency fund should cover ₹40,000 per month. This ensures your family remains financially secure even during income disruptions.

Consider City and Lifestyle Factors

Emergency fund needs vary based on city-specific costs and lifestyle choices. Metro cities like Delhi, Mumbai, and Bengaluru have higher rents, transport, and healthcare costs compared to smaller towns, so your fund should reflect that reality.

For instance, someone renting a ₹20,000 apartment with ₹10,000 in groceries and transport should aim for at least ₹90,000–₹1,80,000 to cover three to six months. Similarly, lifestyle choices such as eating out, fitness memberships, or private healthcare subscriptions should be factored into your essentials if they are non-negotiable.

Start Small and Build Consistently

Building a full emergency fund may seem daunting, but starting small is better than waiting for the “perfect” amount. Even a modest fund offers protection and helps develop the habit of disciplined saving.

For example, start with ₹10,000–₹15,000 and add ₹5,000–₹10,000 each month until you reach your target. Automating monthly transfers into a separate account can make this process easier, and seeing your fund grow steadily can motivate you to maintain it consistently.

Reassess and Adjust Regularly

An emergency fund is not a “set it and forget it” tool. As your expenses, income, or responsibilities change, your target fund should also be recalculated. Life events such as marriage, moving to a new city, or having children can increase monthly expenses.

For example, after moving to Bengaluru for work, rent might increase from ₹12,000 to ₹20,000. Recalculating your fund ensures it still covers three to six months of your new essential expenses. Regular reviews keep your safety net relevant and effective.

Also Read: Can Paying Bills Help Build a Credit Score?

Where to Save Your Emergency Fund for Easy Access

Choosing the ideal place to park your emergency fund is crucial. You want it safe, easily accessible, and ideally earning a bit of interest. Here’s how to approach it:

| Option | Key Features | Liquidity | Risk Level | Notes |

| High-Interest Savings Account | Earns interest while keeping funds accessible | Instant | Very Low | Choose accounts with low fees and decent interest rates |

| Short-Term Fixed Deposits | Higher interest than savings accounts | 3–6 months | Very Low | Check premature withdrawal rules |

| Liquid Mutual Funds | Invests in short-term debt instruments | 24 hours | Low | Choose funds with low exit loads and reliable fund houses |

| Avoid Risky Investments | Stocks, crypto, or long-term equity funds | Variable | High | Not suitable for emergency funds |

| Separate Account | Dedicated account separate from regular funds | Instant | Very Low | Prevents accidental spending |

| Annual Review | Reassess interest rates and accessibility | N/A | N/A | Adjust storage method as your needs change |

How to Build Your Emergency Fund Quickly?

Creating an emergency fund can feel like a slow process, but with clear planning and consistent effort, you can reach your goal faster than you expect. A strong emergency fund protects you from unexpected financial shocks such as sudden medical expenses, urgent repairs, or temporary income loss, giving you peace of mind and financial stability.

Creating an emergency fund can feel like a slow process, but with clear planning and consistent effort, you can reach your goal faster than you expect. A strong emergency fund protects you from unexpected financial shocks such as sudden medical expenses, urgent repairs, or temporary income loss, giving you peace of mind and financial stability.

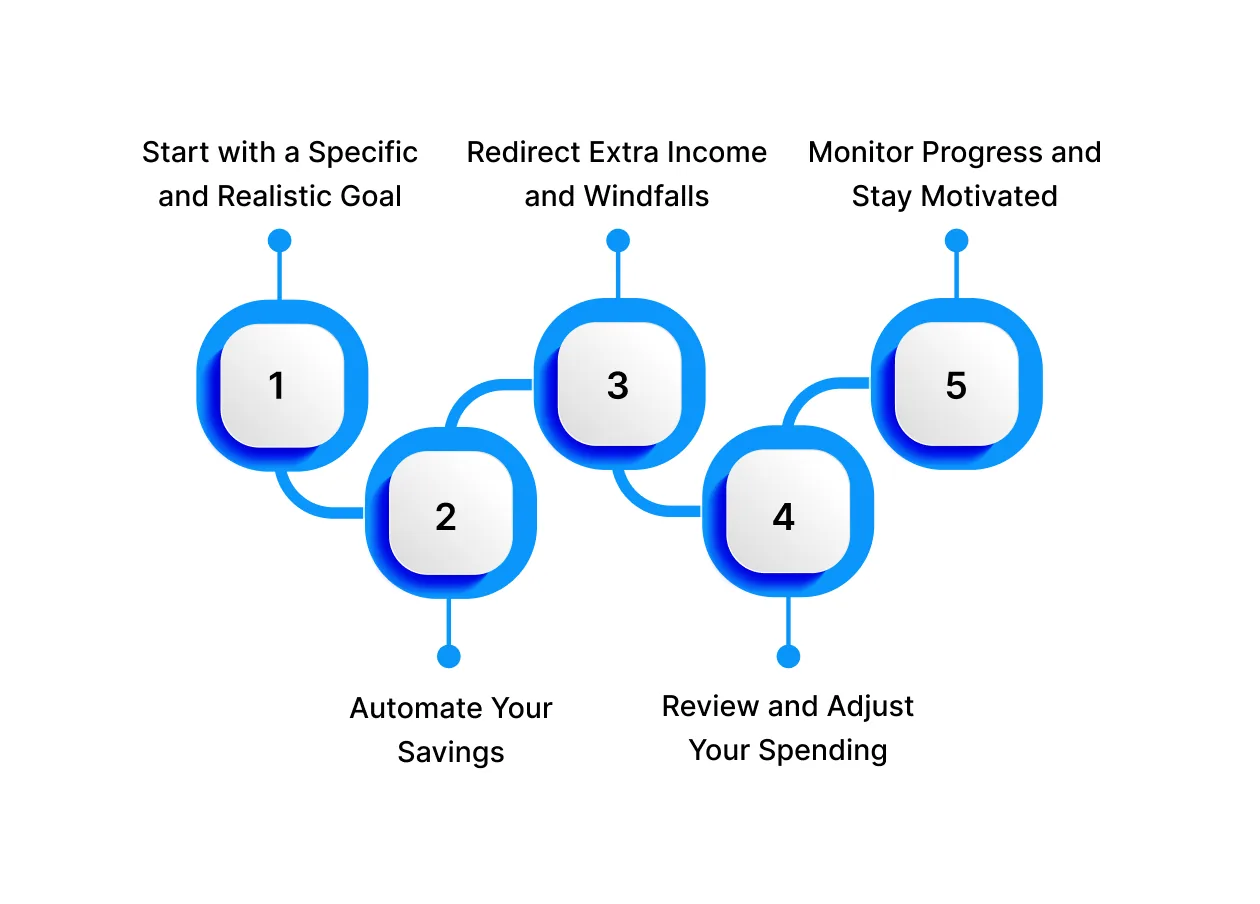

Step 1: Start with a Specific and Realistic Goal

The first step is to determine how much your emergency fund should cover. Financial experts usually suggest saving three to six months’ worth of essential expenses. Calculate your monthly costs, including rent, utilities, groceries, transportation, EMIs, and other non-negotiable payments.

For example, if your monthly essentials add up to ₹30,000, your target emergency fund should range between ₹90,000 and ₹1,80,000. Defining a clear goal helps you stay focused and gives you a tangible target to work toward.

Step 2: Automate Your Savings

Consistency is key when building an emergency fund. Set up automatic monthly transfers to a separate bank account or digital wallet dedicated exclusively to your emergency savings. Treat it like a recurring bill that must be paid, rather than money you can spend freely.

For instance, setting aside ₹5,000 every month will help you accumulate ₹1,00,000 in just 20 months without having to consciously remember to save. Automation eliminates procrastination and ensures your fund grows steadily over time.

Step 3: Redirect Extra Income and Windfalls

Income beyond your regular salary, such as bonuses, freelance earnings, tax refunds, or monetary gifts, can be directed straight into your emergency fund. Using unexpected money in this way accelerates your progress without impacting your monthly budget.

For example, a ₹25,000 bonus could cover almost a month of essential expenses, bringing you closer to your goal in a single transaction. Treating windfalls as savings rather than spending opportunities builds a habit of prioritising financial security.

Step 4: Review and Adjust Your Spending

Carefully examine your current spending habits and identify areas where temporary adjustments can free up money for your emergency fund. This could include reducing dining out, postponing luxury purchases, or limiting non-essential subscriptions.

Even small savings, such as ₹2,000–₹3,000 a month, can significantly shorten the time needed to reach your target. The focus is not on depriving yourself but on reallocating funds to strengthen your financial safety net.

Step 5: Monitor Progress and Stay Motivated

Tracking your fund’s growth is essential for staying committed. Monitor contributions monthly and celebrate milestones to maintain motivation. Recognising progress, even in smaller increments, reinforces the habit of saving.

For example, marking milestones at ₹50,000, ₹1,00,000, or each subsequent addition provides a sense of accomplishment and keeps you involved with your financial goals.

Also Read: Should You Save for an Emergency Fund or Pay Off Debt?

Common Mistakes While Building an Emergency Fund

Even when you’re motivated to save, certain habits or misconceptions can slow your progress or reduce the effectiveness of your emergency fund. Being aware of these mistakes can help you stay on track and build a truly reliable financial safety net.

Treating Your Emergency Fund Like a Regular Savings Account

Risk: Keeping your emergency fund in the same account used for daily spending makes it easy to dip into for non-emergencies, leaving you unprepared for real financial shocks.

Mitigation: Open a dedicated account for your emergency fund, ideally one that earns interest. This separation ensures the money is available only for real emergencies such as healthcare bills, urgent repairs, or temporary loss of income.

Not Setting a Clear Savings Goal

Risk: Saving without a defined target can result in underfunding. You may feel that any amount is enough, which can leave you vulnerable during significant financial setbacks.

Mitigation: Calculate your monthly essential expenses and aim to save at least three to six months’ worth. A clear target gives you direction, tracks progress, and motivates consistent contributions.

Ignoring Small, Consistent Contributions

Risk: Waiting for bonuses or extra income to save slows progress and can delay the completion of your emergency fund.

Mitigation: Make small, regular contributions, even ₹1,000–₹5,000 per month. Consistency is more effective than occasional large deposits and builds a reliable savings habit.

Using the Fund for Non-Emergencies

Risk: Treating your emergency fund like a flexible stash for lifestyle upgrades or impulse purchases reduces its availability when a real crisis occurs.

Mitigation: Clearly define what qualifies as an emergency, an urgent medical bill, essential repairs, or temporary income loss and strictly use the fund for those situations.

Failing to Reassess Your Fund Over Time

Risk: Life changes such as marriage, children, relocation, or lifestyle upgrades can increase monthly expenses, making your fund insufficient.

Mitigation: Review your emergency fund regularly to ensure it still covers three to six months of living costs, adjusting contributions if necessary.

Overlooking Inflation and Interest

Risk: Keeping your fund in a low-interest account while ignoring inflation reduces its real value, meaning it may not fully cover future expenses.

Mitigation: Use a high-yield savings account or liquid instruments that offer better returns while remaining easily accessible. This preserves and grows your fund over time.

Tips to Grow Your Emergency Fund Faster

Building a robust emergency fund requires strategy, discipline, and smart money management. Here’s how you can accelerate your savings:

Building a robust emergency fund requires strategy, discipline, and smart money management. Here’s how you can accelerate your savings:

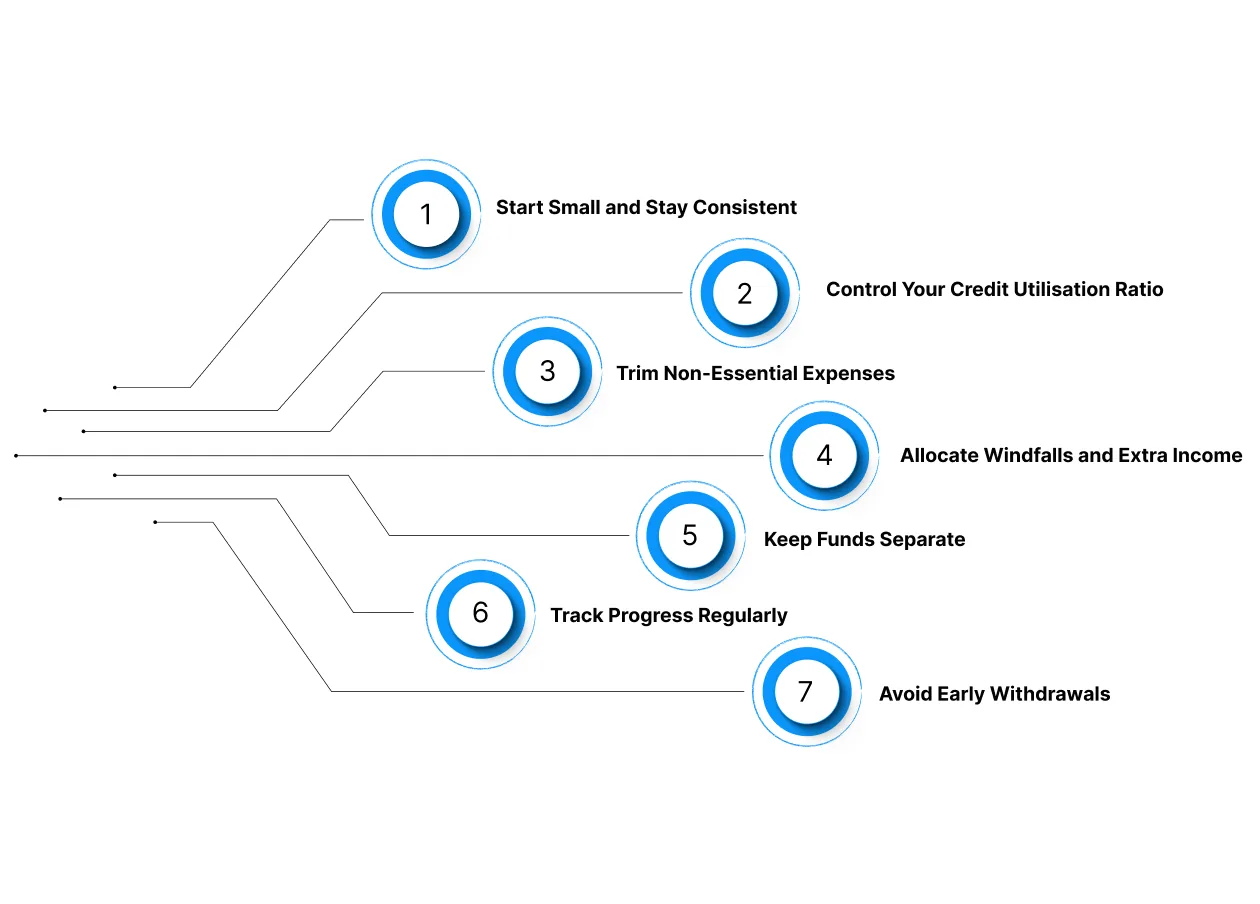

- Start Small and Stay Consistent: Even small contributions add up over time. Consistency builds the habit of saving, making it easier to increase contributions as your income grows or expenses decrease.

- Automate Your Savings: Automating transfers to a dedicated emergency fund reduces the temptation to spend the money elsewhere. It also ensures your fund grows steadily without requiring active effort every month.

- Trim Non-Essential Expenses: Review your monthly spending to identify discretionary costs that can be reduced, such as subscriptions, dining out, or entertainment. Redirecting even small amounts can significantly boost your emergency fund over time.

- Allocate Windfalls and Extra Income: Unexpected earnings like bonuses, tax refunds, or freelance payments can accelerate your fund growth. Treat these as priority contributions rather than discretionary spending.

- Keep Funds Separate: Maintaining your emergency fund in a separate account safeguards it from everyday spending and provides a clear picture of your financial safety net.

- Track Progress Regularly: Monitoring your emergency fund helps you stay accountable and motivated. Tracking also allows you to adjust monthly contributions as your financial situation changes.

- Avoid Early Withdrawals: The effectiveness of an emergency fund depends on discipline. Only use it for genuine emergencies, medical costs, urgent repairs, or sudden income gaps to maintain its purpose and long-term stability.

Pocketly: Handle Short-Term Gaps Without Dipping Into Your Emergency Fund

Life is unpredictable. Even with an emergency fund, sudden expenses like medical bills, urgent travel, or home repairs can strain your finances. Using your savings for every unexpected cost slows your fund’s growth and reduces security when real emergencies arise.

Pocketly offers a smart alternative to quick, short-term loans that cover temporary shortfalls while keeping your emergency fund intact.

Why Pocketly makes sense:

- Borrow only what you need: ₹1,000 to ₹25,000.

- No collateral or guarantor required.

- Fast KYC-based approval for instant access to funds.

- Direct transfer to your bank account immediately after approval.

- Flexible repayment plans that fit your budget.

- Transparent pricing: interest from 2% per month and 1–8% processing fees.

- 24/7 app access to apply, track, and manage loans.

With Pocketly, you can manage urgent expenses confidently, protect your savings, and keep your emergency fund growing for when it really counts.

Conclusion

Having an emergency fund is one of the smartest steps you can take for financial security in 2026. By saving consistently, setting clear targets, and keeping funds accessible, you create a safety net that protects you from unexpected expenses and financial stress.

An emergency fund isn’t about restriction; it’s about preparedness, peace of mind, and giving yourself the freedom to handle life’s surprises without panic.

When urgent costs exceed your fund, tools like Pocketly can provide quick, responsible support so short-term gaps don’t derail your long-term financial plan.

Take control of your financial future today. Download the Pocketly app today on [Android] or [iOS] to access fast, transparent support whenever you need it.

FAQs

1. What is an emergency fund?

An emergency fund is a separate pool of money set aside to cover unexpected expenses such as medical emergencies, urgent repairs, or sudden job loss. It acts as a financial security net and helps you avoid relying on debt during unforeseen situations.

2. How much should I save in an emergency fund?

A general rule is to save three to six months’ worth of essential monthly expenses. The exact amount relies on factors like income stability, number of dependents, lifestyle, and financial obligations.

3. Where should I safeguard my emergency fund?

It’s best to keep your emergency fund in a liquid and safe account, such as a high-yield savings account or a liquid mutual fund. Avoid volatile investments like stocks or long-term fixed deposits.

4. Can I spend my emergency fund for non-emergencies?

No. Using it for discretionary spending defeats its purpose. The fund should be used only for genuine emergencies, such as medical bills, urgent travel, or sudden job loss.

5. How do I start building an emergency fund with a limited budget?

Start small and contribute consistently. Even saving a small amount each month adds up over time. Automate your savings and gradually increase contributions as your income grows.