You apply for a loan expecting quick approval, but the status stays stuck at “under verification.” This stage often creates confusion, especially when there is no clear update from the bank. What most borrowers miss is that approval depends heavily on verification, not just the application.

In India, access to formal financial services is expanding fast, with the Reserve Bank of India reporting a Financial Inclusion Index score of 67 in 2025, showing deeper usage of banking and credit systems across the country.

As more people enter the formal credit system, banks are tightening verification checks to confirm identity, income, and repayment ability before disbursing any loan. Understanding this process helps avoid delays and reduces the chances of rejection.

At a Glance

- Loan approval depends on verification, not just application submission. Most delays happen after you apply, during document and identity checks.

- KYC accuracy directly impacts processing speed. Even small mismatches in name, address, or DOB can pause verification.

- Credit behaviour matters more than just your score. Lenders assess repayment patterns, active debt, and financial discipline.

- Income consistency is verified, not just declared. Banks cross-check documents and bank statements to confirm repayment capacity.

- Faster approval comes from cleaner applications, not faster banks. Complete documents, consistent details, and digital KYC can reduce delays significantly.

What Is the Bank Loan Verification Process

The bank loan verification process is the stage between the loan application and final approval. During this stage, the lender checks whether the borrower’s details are genuine and whether the application can move forward for approval.

It is a mandatory part of lending, not an extra step. Even if the application is submitted correctly, the loan is not disbursed until verification is completed.

In simple terms, this process helps the lender confirm two things:

- The applicant’s details are valid

- The loan request fits the applicant’s profile

If something does not match, the bank may pause the application, ask for clarification, or take longer to process it.

For example, many applicants think a submitted form means the loan is almost approved. In reality, the verification stage is where the lender decides whether the application is ready for approval at all.

Also Read: Instant Approval Loans vs Traditional Bank Loans: 2026 Comparison

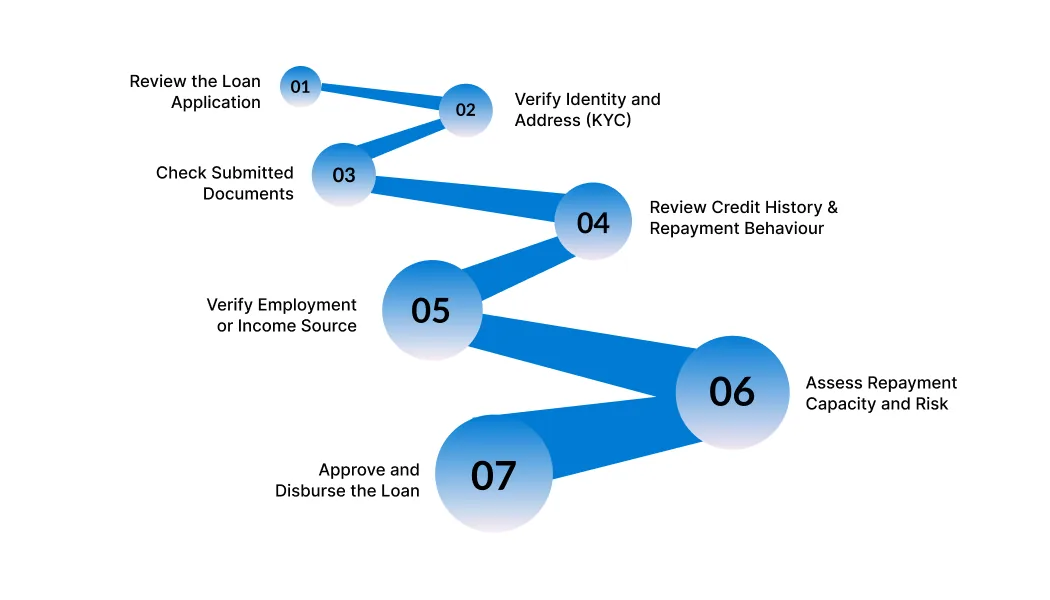

Step-by-Step Bank Loan Verification Process in India

After submitting a loan application, the bank reviews the applicant’s details for accuracy, completeness, and financial reliability. This process goes beyond document collection, including verifying identity records, income proof, repayment history, and assessing the borrower’s ability to repay the requested loan.

Even if the application appears complete, mismatched KYC details, poor credit behaviour, or inconsistent income can delay approval. While most banks follow a similar verification process, the speed can vary depending on the lender, loan type, and whether the process is digital or branch-based.

Step 1: Reviewing the loan application

The first check begins with the information entered in the application form. The bank reviews personal details such as name, date of birth, mobile number, PAN, address, employment type, monthly income, and the amount requested. At this stage, the lender is checking whether the application is complete and whether the details appear logically consistent.

Step 2: Verifying identity and address through KYC

The next stage is KYC verification. This is where the bank confirms that the applicant is a real person with valid identity and address records. Documents such as Aadhaar, PAN, passport, voter ID, or other officially valid documents may be used, depending on the lender and loan type.

Step 3: Checking submitted documents for accuracy

After KYC, the bank reviews the financial and supporting documents submitted with the application. For salaried applicants, this usually includes salary slips, bank statements, and employment proof. For self-employed applicants, it may include bank records, business proof, income documents, or GST-related records, depending on what the lender asks for.

Step 4: Reviewing credit history and repayment behaviour

Banks usually check the applicant’s credit report through a recognised credit bureau. This helps them understand whether previous loans or credit card bills were paid on time, how much debt is already active, and whether there have been defaults, settlements, or overdue accounts.

Step 5: Verifying employment or source of income

The lender may also verify whether the applicant’s current job or income source is stable. For salaried borrowers, this can involve checking company details, employment status, or salary flow. For self-employed individuals or small business owners, the bank may review business continuity and income regularity.

Step 6: Assessing overall repayment capacity and risk

Once identity, documents, and credit behaviour have been checked, the bank assesses the applicant’s broader financial position. This includes existing EMIs, monthly obligations, credit utilisation, and the relationship between income and debt. The purpose is to decide whether the requested loan amount is manageable.

Step 7: Final approval and disbursal

If all checks are cleared, the bank moves the loan to final approval and then to disbursal. At this point, the borrower may receive a sanction letter or final terms, including the approved amount, interest, repayment schedule, and any applicable charges. Only after these checks are completed does the money get transferred.

For applicants, this is why the verification stage matters so much. A loan is not delayed only because the bank is slow. In many cases, the delay comes from document mismatch, incomplete details, or risk checks that require more review.

Also Read: E‑Verification Meaning: Understanding Its Role in Digital Tax Filing

Documents Required for Bank Loan Verification

Even when the application looks complete, most delays happen at the document stage. Banks rely heavily on documents to confirm identity, income, and financial behaviour. If any document is missing, outdated, or inconsistent with the application, the verification process slows down immediately.

The exact requirement can vary slightly across lenders, but the core set of documents remains largely the same.

Identity proof

Banks need to confirm who the applicant is before moving ahead with any financial approval. This is usually done through officially valid documents such as an Aadhaar card, a PAN card, a passport, or a voter ID.

The details on these documents must match the information entered in the application. Even small differences in name spelling or date of birth can trigger re-verification requests.

Address proof

In addition to identity, lenders verify where the applicant currently resides. Address proof can include Aadhaar, utility bills, rental agreements, or bank statements showing the current address.

If the address submitted does not match recent records, the bank may ask for updated proof. This step becomes important for communication, verification calls, and in some cases, physical checks.

Income proof

Income verification plays a key role in deciding whether the loan can be repaid comfortably.

For salaried individuals, banks typically ask for:

- Recent salary slips

- Bank statements showing salary credits

- Employment details

For self-employed applicants, documents may include:

- Bank statements

- Business proof or registration

- Income records based on the nature of work

The lender compares these documents with the declared income in the application. Any mismatch can lead to further checks or delays.

Bank statements

Bank statements are used to understand spending patterns, existing obligations, and the consistency of income. Lenders usually review the last few months to see how money flows in and out of the account.

Irregular deposits, frequent low balances, or heavy existing EMIs can affect how the application is assessed.

Additional supporting documents

Depending on the loan type and applicant profile, banks may ask for extra documents. These can include employment proof, offer letters, business invoices, or tax-related records.

Not every application requires all documents, but being prepared with accurate and recent records helps avoid back-and-forth during verification.

Types of Loan Verification Methods Used by Banks

The way verification is carried out has changed significantly over time. While traditional methods involved branch visits and physical checks, many lenders now use digital verification to speed up the process.

Physical verification

In some cases, banks still conduct physical verification. This can involve a representative visiting the applicant’s address or workplace to confirm details. It is more common in higher-value loans or when additional validation is required.

This method takes more time but adds another layer of confirmation for the lender.

OTP-based eKYC

eKYC allows identity verification using Aadhaar-linked mobile numbers. The applicant enters an OTP to confirm their identity digitally. This method is faster and reduces the need for physical document submission.

However, it depends on the accuracy of Aadhaar-linked details.

Video KYC

Video KYC has become more common in recent years. The applicant completes a live video interaction where identity documents are shown and verified in real time.

This method helps lenders confirm both identity and presence without requiring a branch visit. It is widely used in digital lending journeys.

CKYC database verification

Some lenders also check records through the Central KYC (CKYC) database. If an applicant has already completed KYC with another financial institution, the same record can be accessed and reused.

This reduces duplication and speeds up the process, provided the records are up to date.

Common Reasons Loan Verification Gets Delayed or Rejected

A loan application does not usually get delayed without reason. Most issues arise from gaps in information, inconsistencies, or risk-related concerns that appear during verification.

- Mismatch in KYC details: If the name, address, or date of birth does not match across documents, the bank may pause the process until corrected documents are submitted.

- Incomplete or outdated documents: Submitting partial documents or older records can lead to repeated requests from the lender. Each round of correction adds to the overall processing time.

- Low or unstable credit history: A weak repayment track record, frequent defaults, or high outstanding debt can affect the lender’s confidence. Even if other documents are correct, this factor can influence the final decision.

- Irregular income patterns: If income appears inconsistent or difficult to verify, the bank may take longer to assess repayment capacity. This is common in cases where income sources are not clearly documented.

- High existing financial obligations: If a large portion of income is already committed to other EMIs or expenses, the lender may reduce the approved amount or decline the application altogether.

If delays are becoming a pattern and the requirement is small and urgent, waiting through long verification cycles may not always be practical.

If the loan amount is small and the need is immediate, a digital app like Pocketly may be worth considering for faster access to funds. Get started now!

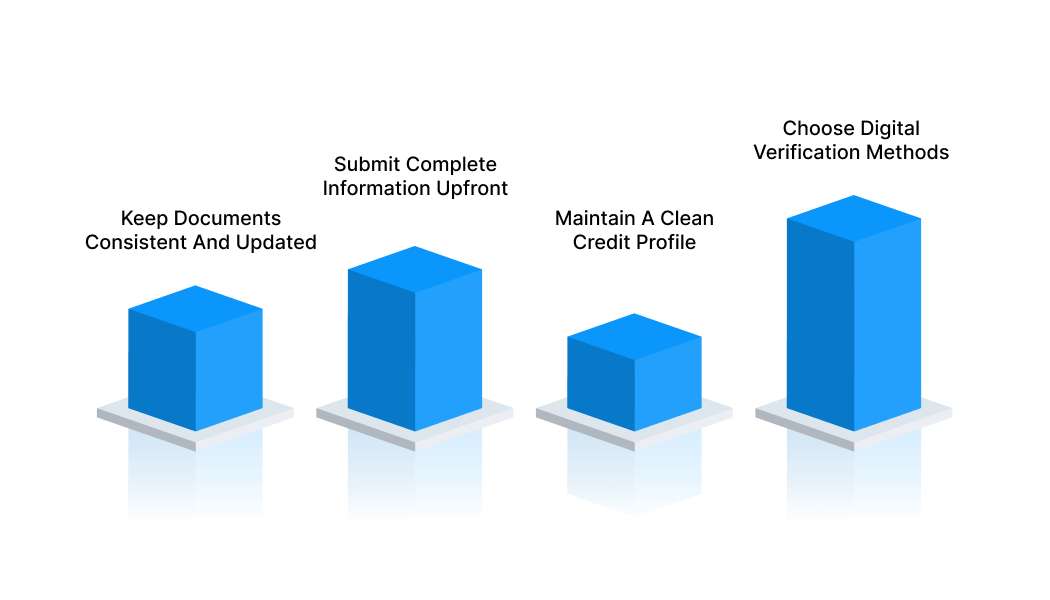

How to Speed Up Your Bank Loan Verification Process

Verification delays are often not because the bank is slow, but because something in the application requires clarification. Small errors or missing details can add days to the process, especially when multiple checks are involved.

A few practical steps can reduce this waiting time significantly.

Keep all documents consistent and updated

Before applying, check that your name, date of birth, and address match across all documents. If your PAN, Aadhaar, and bank account show different details, the lender will ask for corrections.

Using recent documents also helps. Outdated address proof or old bank statements can lead to re-submission requests.

Submit complete information in one go

Applications that require multiple follow-ups usually take longer to process. Providing all required documents upfront reduces back-and-forth communication.

It also signals that the application is ready for review, which can move it forward faster in the queue.

Maintain a clean credit profile

While this is not something that can be fixed instantly, a stable credit history helps the verification process move smoothly. Regular repayments and controlled credit usage reduce the need for additional checks.

Even if the credit score is not perfect, avoiding recent defaults or overdue payments makes a difference.

Choose digital verification where possible

Digital methods like eKYC or video KYC are generally faster than physical verification. They reduce dependency on manual checks and allow lenders to verify details in real time.

This is especially useful for smaller loan amounts where speed matters more than extensive documentation.

For smaller urgent expenses, apps like Pocketly can be a practical option when you want a simpler process and quicker access to money. Apply now!

How Pocketly Simplifies Loan Verification for Small Amounts

For smaller, short-term financial needs, lengthy verification processes can feel disproportionate to the amount required. This is where digital lending platforms are designed differently.

Pocketly focuses on quick verification for small-ticket loans, typically between ₹1,000 and ₹25,000. The process is structured to reduce delays while still following required verification checks.

Instead of multiple layers of manual validation, the platform uses a streamlined digital flow.

- Loan range: ₹1,000 to ₹25,000

- Interest rates starting from around 2% per month

- Processing fee between 1% and 8%

- No collateral required

How the process works

- Visit the platform or download the app

- Complete a quick digital KYC

- Select the required loan amount

- Receive approval and disbursal based on eligibility

Pocketly operates as a digital lending platform working with RBI-registered NBFC partners. The availability of higher amounts depends on the applicant’s profile, and some users may see lower limits based on eligibility.

If you need a small amount for an urgent expense, download Pocketly on iOS or Android in a few minutes.

FAQs

Q: How long does the bank loan verification process take in India?

The timeline can vary based on the lender and document accuracy. In many cases, it takes a few days, but delays can happen when documents need correction or extra checks are required.

Q: Can a loan be approved before verification is completed?

No, approval depends on successful verification. The lender does not disburse funds until the required checks are completed.

Q: Do all banks follow the same verification process?

The core process is usually similar, but the speed and method can differ. Some lenders rely more on digital verification, while others may take a more manual route.

Q: Does loan verification include checking my bank account activity?

Yes, lenders may review bank statements to understand income flow, spending patterns, and existing financial commitments before making a decision.

Q: Can I get a small urgent loan with a simpler verification process?

For smaller short-term amounts, some digital lending platforms offer a quicker process than traditional bank routes. Pocketly, for example, lets eligible users complete digital KYC and check available loan options for short-term cash needs.

Q: What happens if my loan verification fails?

If the verification does not meet the lender’s requirements, the application may be rejected or placed on hold until the issue is resolved.