Feeling like you’re constantly tracking EMIs, credit cards, and due dates, yet something still slips through? You’re not alone. In India, borrowing has become a normal part of managing everyday expenses. According to RBI data, retail loan growth stood at 16.6% year-on-year in June 2024, highlighting how more individuals are actively relying on multiple credit sources.

The real problem is not taking loans, but managing them without a clear system. Different interest rates, due dates, and repayment amounts can quickly become overwhelming. Even a single missed payment can lead to penalties, higher interest costs, and a drop in your credit score. Over time, this creates unnecessary stress and financial pressure.

In this blog, we will explore simple and practical ways to manage multiple loans, stay consistent with repayments, reduce financial stress, and take better control of your money step by step.

Key Takeaways

- Even a single missed EMI can turn into penalties, higher interest, and a dip in your credit score. Tracking due dates is non-negotiable.

- Write down every loan’s EMI, interest, due date, and balance. Seeing everything in one place lets you prioritise high-cost loans and avoid last-minute stress.

- Tackle high-interest loans first or small loans first, and schedule EMIs right after your salary to stay ahead.

- Say no to extra debt unless essential, and keep a small emergency fund to handle surprises without disrupting repayments.

- Use apps like Money View, Walnut, Jupiter, or UPI payment histories for reminders and tracking. Staying consistent protects your credit and keeps your finances stress-free.

How Multiple Loans Quietly Turn Into a Financial Burden

Managing multiple loans becomes difficult when different repayments start overlapping and competing for your income. What looks manageable on paper often turns into a situation where one small miss can trigger bigger financial consequences.

Here’s where most people struggle:

- Tracking Multiple Due Dates: Each loan comes with its own repayment schedule. When due dates are spread across the month, it increases the chances of missing a payment, which can lead to penalties and a drop in your credit score.

- Handling Different Interest Rates: Not all loans cost the same. Credit cards and short-term loans often carry higher interest rates, and if they are not prioritised, they can significantly increase your total repayment over time.

- Managing Monthly Cash Flow: Multiple EMIs reduce the amount of money available for daily expenses, savings, and emergencies. This can create financial pressure and make it harder to stay consistent with repayments.

- Staying Organised Financially: Keeping track of several loans at once can become overwhelming. Missing details or delaying decisions often leads to poor financial planning and reactive choices.

- Protecting Your Credit Score: Your repayment behaviour directly impacts your credit profile. Missed payments, high utilisation, or frequent borrowing can make lenders view you as a higher-risk borrower.

Example: If you are managing a personal loan, two credit cards, and a short-term loan at the same time, each with different due dates and interest rates, even one missed payment or delay can increase your total cost and affect your credit score.

Know Your Debt First: List Every Loan Clearly

If you’re handling multiple loans, the first step is very simple: know exactly what you owe. Most people don’t struggle because they can’t pay; they struggle because they don’t have a clear picture of their loans. Things feel confusing when details are scattered across different apps, messages, or emails.

Start by writing down basic details of each loan:

- Total amount left to pay

- Monthly EMI

- Interest rate (how much extra you’re paying)

- Due date (when payment is required)

- Remaining months to finish the loan

You don’t need anything fancy. A notes app, an Excel sheet, or even a notebook works perfectly.

When everything is in one place, you can finally see the following:

- How much money goes into EMIs every month

- Which loan is the most expensive

- When your payments are due

This makes it easier to plan instead of feeling lost or stressed.

What this helps you do:

- Avoid missing payments

- Focus on loans that cost more

- Manage your money better every month

Example: Let’s say you have a credit card bill, a small personal loan, and a short-term loan. When you list all three together, you can quickly see which one has the highest interest and which one is due first, so you can plan your payments smartly.

Also Learn: Understanding the Ideal CIBIL Score Range for Personal Loan Applications

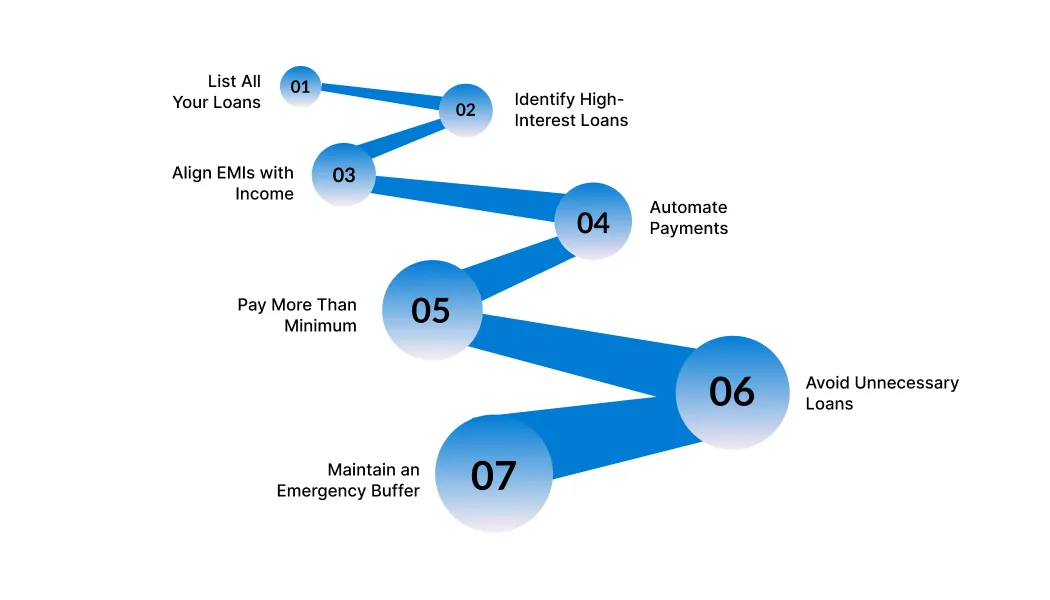

7 Steps to Manage Multiple Loans Without Missing EMIs or Risking Your Credit

Things start to feel overwhelming when you’re just reacting to due dates instead of planning ahead. Once your loans are organised, payments are tracked, and a fixed routine is in place, staying on top of everything becomes far more manageable.

Here’s a step-by-step approach you can follow:

Step 1: List All Your Loans in One Place

Start by writing down every loan you currently have, along with key details like EMI, due date, interest rate, and remaining balance.

This step gives you complete clarity. Instead of guessing or relying on memory, you can clearly see how much you owe and when payments are due.

For example, if you have a credit card bill, a personal loan, and a short-term loan, listing them together helps you understand your total monthly outflow and avoid surprises.

Step 2: Identify Which Loans Are Costing You More

Not all loans are equal. Some loans, especially credit cards or instant loans, come with higher interest rates and increase your total repayment faster.

By identifying these loans early, you can prioritise them and reduce the overall interest you pay over time.

For example, paying off a loan with 24% interest faster will save you much more money compared to a loan with 12% interest.

Step 3: Align Your EMI Dates with Your Income

Your repayment schedule should work with your cash flow, not against it. If your EMIs are due before you receive your salary, it increases the risk of missed or delayed payments.

If possible, request lenders to adjust your due dates closer to your income date so you always have funds available.

For example, if your salary comes on the 5th, keeping EMIs between the 6th–10th makes repayment smoother and stress-free.

Step 4: Automate Payments or Set Reminders

Consistency is key when managing loans. Missing even one EMI can lead to late fees and affect your credit score.

Setting up auto-debit or simple reminders ensures you never forget a payment, even during busy or stressful periods.

For example, you can enable auto-pay through your bank or set phone reminders 2–3 days before the due date.

Step 5: Pay More Than the Minimum Whenever Possible

Paying only the minimum amount keeps your loan active but increases the total interest you pay. Even small extra payments can make a big difference over time.

This helps you reduce your loan faster and saves money in the long run.

For example, paying an extra ₹500–₹1,000 towards a high-interest loan every month can shorten your repayment period and lower your overall cost.

Step 6: Avoid Taking New Loans Without a Clear Need

When you already have multiple loans, taking on new debt can increase pressure on your income and make management difficult.

Before applying, always ask yourself if the expense is necessary and if you can comfortably handle another EMI.

For example, taking a loan for non-essential purchases can increase your financial burden without adding real value.

Step 7: Keep a Small Emergency Buffer

Unexpected expenses like medical needs or urgent travel can disrupt your repayment plan. Having a small backup fund helps you stay consistent even during such situations.

This reduces your dependence on new loans and keeps your credit profile stable.

For example, setting aside even ₹2,000–₹5,000 can help you manage EMIs during a tight month without stress.

Juggle multiple loans with ease. Pocketly offers ₹1,000–₹25,000 instantly to cover EMIs or urgent bills. Apply in minutes and keep your finances stress-free. Apply now!

What Impacts Your Credit Score Most When You Have Multiple Loan

Most people think having multiple loans is the problem. It’s not. What actually matters is how your behaviour looks to lenders when all your loans are viewed together.

Lenders don’t see your loans one by one. They see a combined pattern of your borrowing, spending, and repayment habits. This means even if each loan looks manageable individually, the overall picture can still appear risky.

Here’s what actually impacts your credit score when you have multiple loans:

1. Payment History (Your Repayment Behaviour)

This is the most important factor in your credit score. It shows whether you pay your EMIs on time or delay them.

Example: If you have three loans and miss one EMI, your score can drop even if the other payments were on time.

When it works: Paying every EMI on time builds a strong repayment record and increases your chances of getting loans easily in the future.

Caution: Even one missed or late payment can stay on your credit report for a long time and affect your credibility with lenders.

2. Credit Utilisation (How Much Credit You’re Using)

This mainly applies to credit cards and shows how much of your available limit you are using. High usage can make it look like you depend too much on credit.

Example: If your credit limit is ₹40,000 and you consistently use ₹35,000, it reflects high utilisation.

When it works: Keeping your usage below 30 to 40% shows that you are using credit wisely and not over-relying on it.

Caution: Using most of your limit regularly can lower your score, even if you pay your bill on time every month.

3. Number of Active Loans (How Much You’re Handling at Once)

This refers to how many loans or credit accounts you have at the same time. Managing too many can increase your financial responsibility.

Example: Handling a personal loan, two credit cards, and a short-term loan together can make your profile look heavy.

When it works: A limited number of loans, managed properly, shows that you can handle credit in a balanced way.

Caution: Too many active loans can make lenders feel you may struggle with repayments, which can reduce approval chances.

4. Frequent Loan Applications (How Often You Apply for Credit)

Every time you apply for a loan or credit card, lenders check your credit report. This is called a hard enquiry and can slightly reduce your score.

Example: Applying for multiple loans within a short time can signal that you urgently need money.

When it works: Applying only when necessary helps maintain a stable credit profile and avoids unnecessary score drops.

Caution: Too many applications in a short period can lower your score and make lenders hesitant to approve your request.

5. Consistency Over Time (Your Long-Term Habits)

Your credit score improves slowly based on your behaviour over time. It reflects how consistently you manage your loans month after month.

Example: Paying all your EMIs on time for 6 to 12 months can gradually improve your score, even if it was low earlier.

When it works: Consistent repayments, low credit usage, and fewer applications help build a strong and reliable credit profile.

Caution: Missing payments or taking unnecessary loans can quickly undo your progress and bring your score down again.

Handle Unexpected Payments Smoothly with Pocketly

Sudden bills, EMIs, or gaps between salary payments can disrupt your financial plans and hurt your credit. Pocketly steps in as a fast, flexible financial buffer, helping you pay on time, avoid penalties, and keep your money management stress-free.

Here’s how it helps:

- Never miss a payment: Cover bills or EMIs on time and avoid late fees, penalties, or CIBIL score hits, even if your salary is delayed.

- Borrow only what you need: Get instant access to ₹1,000–₹25,000 to handle urgent expenses, without piling on unnecessary debt.

- Fast and fully digital: Apply in minutes and receive money directly in your bank account, no long forms or paperwork.

- No strict credit requirements: No perfect credit history, collateral, or guarantor needed, designed for real-world emergencies.

- Flexible repayments: Pick a schedule that matches your income cycle, making repayments easy and stress-free.

- Transparent costs upfront: Interest starts at 2% / month, and processing fees range from 1%–8%, with zero hidden charges.

- All-in-one convenience: Track, manage, and repay directly from the app, keeping your finances organised and under control.

With Pocketly, you get a reliable partner to pay urgent bills on time, protect your credit health, and stay in control of your finances, without disrupting your savings or monthly budget.

Download Pocketly on iOS or Android and never let sudden cash needs derail your financial plan.

FAQs

1. How do I manage multiple EMIs efficiently?

List all your loans with EMIs, interest rates, and due dates. Highlight high-interest or urgent payments first, set calendar alerts or auto-debit, and track weekly. This way, nothing slips through the cracks, and stress stays low.

2. Should I pay off one loan first or split payments across all?

Use the snowball method to clear small loans first for quick wins, or the avalanche method to tackle high-interest loans and save money. Pick the approach that keeps you consistent without stretching your budget.

3. Can I consolidate multiple loans into one in India?

Yes, loan consolidation combines several EMIs into a single payment, often at a lower interest rate. Before opting, check processing fees, prepayment penalties, and whether the total interest actually drops.

4. What happens if I miss an EMI?

Missing even one EMI can trigger late fees, higher interest, and a hit to your credit score. In India, it may also affect future loan approvals. Using reminders, apps, or auto-debit helps prevent these costly mistakes.

5. How many loans are too many?

There’s no magic number, but aim to keep total EMIs under 30–40% of your monthly income. More than that can strain your budget and increase stress, making it harder to manage unexpected expenses.

6. Does having multiple loans reduce my credit score?

Not automatically. Timely payments and responsible management can boost your credit score, while missed EMIs, delays, or defaults will lower it. A clean track record is more important than the number of loans.

7. Can I prepay loans to reduce interest?

Yes. Prepaying high-interest loans first can cut both interest and tenure. Just check for prepayment penalties, which some Indian banks may charge. Partial prepayments also work if a full payoff isn’t possible.

8. What tools can help me track multiple loans?

Google Sheets or Excel work well for manual tracking. Apps like Money View, Walnut, Jupiter, and even UPI payment history (Google Pay, PhonePe, Paytm) can automate tracking and send reminders for EMIs.