Most of us are acquainted with the idea of taking “loans” and what are the key factors that evolve around availing one. However, one key factor that can significantly influence your loan approval process is your CIBIL score.

This blog will guide you through the importance of the CIBIL score, what constitutes the best CIBIL score for loan approval, and steps you can take to improve your score before applying for a loan.

What is CIBIL Score and Why is it Important?

A CIBIL Score is a three-digit number that summarizes your credit history and punctuality in repaying debts. This score is assessed by the Credit Information Bureau (India) Limited (CIBIL), the oldest credit rating agency in India, operating under a license granted by the Reserve Bank of India (RBI).

CIBIL is the most popular among the four credit information companies licensed by the RBI, with the others being Experian, Equifax, and CRIF High Mark. As part of the TransUnion group, CIBIL maintains credit records on millions of individuals and businesses across India.

A CIBIL score ranges from 300 to 900. Typically, a score of 750 and above is considered excellent and significantly increases your chances of loan approval, as banks view you as a low-risk borrower. Conversely, if your score is below 550, you may face challenges, including higher interest rates or even outright rejection of your loan application.

People often ask as to whether CIBIL score is mandatory to avail a loan. The answer simply is: Yes!

A CIBIL score is essential when applying for a loan. It helps banks verify your creditworthiness and determines whether or not you are a legitimate borrower.

Now that we’ve looked at the significance of CIBIL score, let’s take a look at the various ranges of CIBIL Scores available.

CIBIL Score Range and Its Impact on Loan Approval

The CIBIL score range spans from 300 to 900. Here’s a breakdown of what these numbers typically signify and what impact it has on your loan amount and terms of lending:

| Si. No. | CIBIL Score Range | Description |

| 1. | 300-549 | A low score, indicating poor credit history. Loan approval is unlikely, and if granted, it will come with high-interest rates. Most traditional, well-established banks would hesitate before approving a personal loan with such a credit score. |

| 2. | 550-649 | A fair score that may still attract a comparatively high-interest rate and less favorable loan terms. |

| 3. | 650-749 | Having a score within this range signifies a good chance of your loan being approved, and could also lead to more relaxed terms as compared to those below the specified mark. |

| 4. | 750-900 | An excellent score, which gives you the best chance for approval with favorable interest rates and terms. Whilst most sources suggest that achieving a solid 900 score is close to not possible, with enough care and effort, one can reach the 850 mark, which would make you one of the most diligent persons in repaying your loans across India! |

We’ve discussed the basics of CIBIL score, but have you ever wondered how does CIBIL calculate your credit score?

How Does CIBIL Calculate Your Credit Score?

| Factor | Contribution to CIBIL Score | Description |

| Repayment History | 35% | Timely debt payments have the most significant impact on your score. Consistently paying on time boosts your score. |

| Credit Utilization Ratio | 30% | Measures how much of your available credit you’re using. Keeping utilization below 30% is ideal for maintaining a healthy credit score. |

| Length of Credit History | 15% | A longer history of responsible credit use positively impacts your score. The longer you've had credit accounts, the better it is for your score. |

| New Credit Inquiries | 10% | Frequent credit inquiries and opening new accounts can suggest higher credit risk, which may lower your score. |

| Credit Mix | 10% | A balanced mix of credit types (secured vs. unsecured, short-term vs. long-term) indicates a healthy credit profile and positively affects your score. |

Note: Keep in mind that while these percentages are commonly used in credit scoring models, the exact algorithm CIBIL uses may vary slightly, as the specific calculation details are proprietary. However, the general breakdown provided is a well-accepted approximation.

Importance of a Good CIBIL Score

Maintaining a good CIBIL score is essential for your overall financial health. A high score not only reflects your creditworthiness but also opens doors to a variety of financial opportunities. When reviewing your loan application, lenders heavily rely on your CIBIL score to assess your ability to manage and repay debt.

This evaluation includes examining your credit history, past repayment behavior, and overall credit balance to gauge the risk level of your profile.

Additionally, your CIBIL score influences the loan amount you qualify for and the interest rate you’ll be offered. A good CIBIL score doesn’t just enhance your chances of getting a loan approved; it also provides several other significant benefits:

Better Loan Approval Chances

A high CIBIL score significantly boosts your chances of getting your loan application approved. Lenders are more willing to offer credit to individuals with proven financial discipline.

Lower Interest Rates

Lenders often reward borrowers with high CIBIL scores by offering them lower interest rates. This can translate to significant savings over the life of your loan, reducing the overall cost of borrowing.

Longer Repayment Periods

With a good CIBIL score, you may also be eligible for longer repayment periods. This flexibility allows you to manage your finances better by spreading out your repayments over a more extended period.

Larger Loan Amounts

A higher CIBIL score can also qualify you for a larger loan amount. Lenders are more comfortable extending larger sums to borrowers who have demonstrated good credit behavior in the past.

Quicker Documentation and Approval Process

A high score simplifies the documentation and approval process. Lenders may require less verification and documentation, leading to quicker loan disbursement.

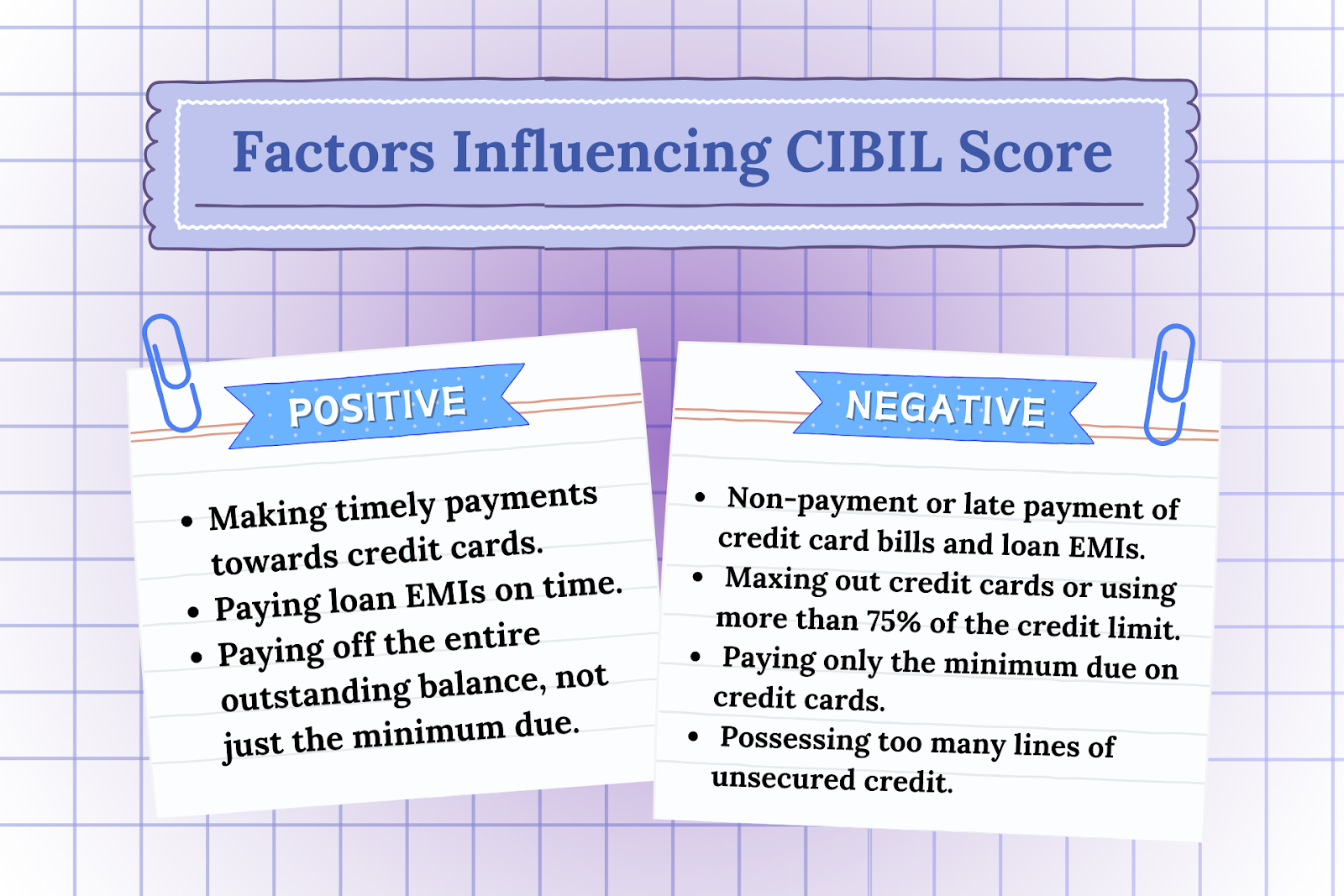

Factors Influencing CIBIL Score

Your CIBIL score is influenced by several factors, both positive and negative:

Positive Factors

- Making Timely Payments Towards Credit Cards: Consistently paying your credit card bills on time boosts your CIBIL score, reflecting your reliability as a borrower.

- Paying Loan EMIs on Time: Timely EMI payments on existing loans indicate good financial discipline, positively impacting your score.

- Paying Off the Entire Outstanding Balance, Not Just the Minimum Due: Clearing the entire outstanding balance on your credit card rather than just the minimum due shows lenders that you manage your debt responsibly.

Negative Factors

- Non-Payment or Late Payment of Credit Card Bills and Loan EMIs: Missing payments or making late payments significantly damages your CIBIL score, marking you as a high-risk borrower.

- Maxing Out Credit Cards or Using More Than 75% of the Credit Limit: High credit utilization indicates a higher dependency on borrowed funds, which can negatively impact your score.

- Paying Only the Minimum Due on Credit Cards: While paying the minimum due helps avoid penalties, it can lead to a high credit utilization rate, which can harm your CIBIL score over time.

- Possessing Too Many Lines of Unsecured Credit: Having multiple lines of unsecured credit, such as personal loans or credit cards, can lower your score, especially if you’re struggling to manage them.

What Happens if My CIBIL Score Isn't High Enough?

A low CIBIL score is often the result of outstanding debt. Lenders evaluate your creditworthiness by looking at your credit utilization ratio—this is the percentage of your available credit that you’re currently using.

If your credit utilization ratio is high, it indicates that you’re relying heavily on credit, which can negatively affect your score. This makes it more difficult to secure future loans, as lenders may view you as a higher-risk borrower.

While using credit is necessary to build your score, it's important to manage it wisely. Stay within your credit limits and ensure timely repayments to maintain a healthy score.

Excessive debt can lower your score and make future loan repayments more challenging, potentially leading to financial difficulties or even bankruptcy.

Now that we know the salient features of the CIBIL Score, let’s discuss the important steps pertaining to your loan application process.

Steps to Take Before Applying for a Loan

Before applying for a personal loan, it's crucial to take certain steps to ensure you're in the best possible position to get favorable terms. Here’s what you should do:

1. Check Your CIBIL Score Regularly

Maintaining a healthy credit score is essential. Regularly check your CIBIL score to stay informed about your credit health. By monitoring your score, you can address any issues or discrepancies before they affect your loan application.

2. Get Your Free CIBIL Report as Mandated by RBI

The Reserve Bank of India (RBI) mandates that you can access your CIBIL report for free once a year. This is an excellent opportunity to review your credit history and correct any errors that could impact your loan eligibility.

To get your free CIBIL report, visit the official CIBIL website or other credit bureaus’ websites. After providing the necessary credentials and completing the verification process, you’ll receive your detailed report.

3. Research and Compare Lenders for the Best Deals

Not all lenders offer the same loan terms. It’s essential to research and compare offers from different lenders to find the one that best suits your financial needs. Consider factors such as interest rates, loan tenure, processing fees, and other terms and conditions.

Also read: Getting a Personal Loan for Self Employed Without Income Proof or Salary Slip

4. Limit Loan Applications to Avoid Impact on Your CIBIL Score

Every time you apply for a loan, it triggers a hard inquiry on your credit report, which can temporarily lower your score. To minimize this impact, apply only to a few carefully selected lenders who offer the most favorable terms for your situation.

The next intuitive question which would follow here is: ‘How do I improve my CIBIL Score’? The answer to this important question lies below, so make sure that you go through it carefully if you feel that your CIBIL score isn’t satisfactory enough.

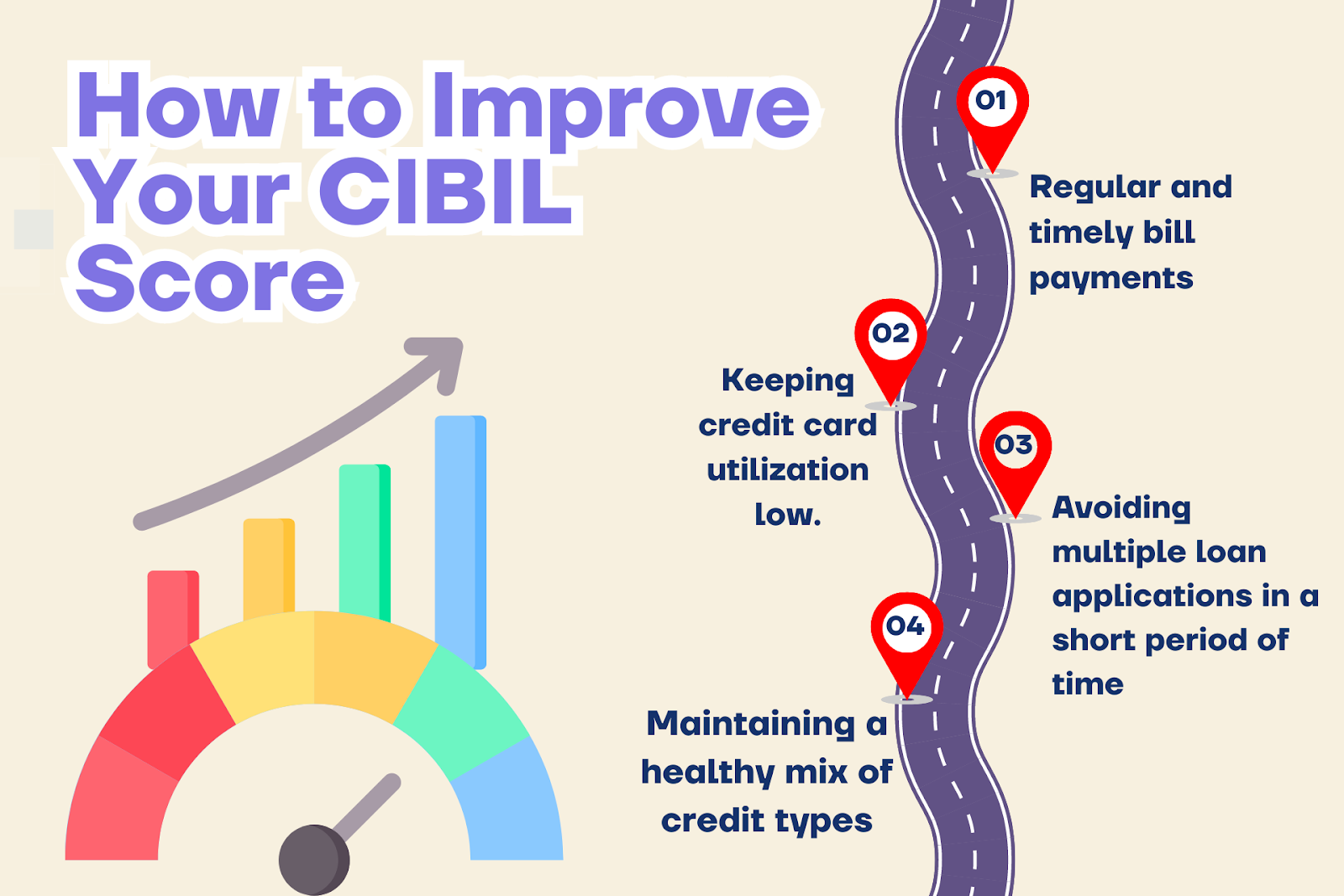

How to Improve Your CIBIL Score

Improving your CIBIL score is a gradual process that requires discipline and consistency. Here are some strategies to help boost your score:

Impact of Regular and Timely Bill Payments

One of the most effective ways to improve your CIBIL score is by making regular and timely payments on your credit cards and loans. Late payments can significantly impact your score, so it’s important to stay on top of your payment schedule. Consider setting up payment reminders or automating payments to ensure you never miss a due date.

Keeping Credit Card Utilization Low

Aim to keep your credit card utilization below 30% of your available credit limit. High credit utilization suggests over-reliance on credit, which can negatively affect your score. By maintaining a lower utilization rate, you demonstrate responsible credit management, which positively impacts your score.

Avoid Multiple Credit Applications in a Short Period

Applying for multiple loans or credit cards within a short time frame can lead to multiple hard inquiries on your credit report. This can signal financial distress to lenders and negatively impact your CIBIL score. To avoid this, space out your credit applications and only apply when necessary.

Maintaining a Healthy Mix of Credit Types

Having a balanced mix of secured (e.g., home loans) and unsecured credit (e.g., personal loans, credit cards) can improve your CIBIL score. Lenders favor borrowers who can responsibly manage different types of credit, as it indicates financial stability and maturity.

Error-Free Credit Report

Maintaining an error-free credit report is crucial to ensure your CIBIL score accurately reflects your creditworthiness. Here’s why it’s important and the steps you can take to rectify any errors before applying for a loan:

Importance of Checking for Errors in the Credit Report

Errors in your credit report can have a significant impact on your CIBIL score and, consequently, your ability to secure loans or credit. Common errors may include incorrect personal information, outdated account statuses, duplicated entries, or even fraudulent activities such as unauthorized loans or credit card accounts. These inaccuracies can unfairly lower your score, making you appear less creditworthy to lenders.

Regularly reviewing your credit report allows you to spot these errors early and take corrective action. An accurate report ensures that your CIBIL score truly reflects your financial behavior, increasing your chances of loan approval, securing favorable interest rates, and avoiding unnecessary complications during the loan application process.

Steps to Rectify Errors Before Applying for a Loan

If you find errors in your credit report, it’s essential to address them promptly. Here are the steps you should take to rectify any discrepancies:

- Review Your Credit Report Carefully: Obtain your free credit report from CIBIL or other credit bureaus at least once a year, as mandated by the RBI. Go through the report in detail to identify any inaccuracies or suspicious activities.

- Gather Supporting Documentation: If you find an error, collect all relevant documents that support your claim. This could include bank statements, loan agreements, or correspondence with lenders.

- Raise a Dispute with the Credit Bureau: Visit the official CIBIL website or the website of the relevant credit bureau and follow their process to raise a dispute. You will need to submit your supporting documents and provide a clear explanation of the error.

- Follow Up on Your Dispute: After filing the dispute, keep track of its status. The credit bureau typically has 30 days to investigate and resolve the issue. During this period, they may contact the lender involved to verify the information.

- Verify the Correction: Once the error is corrected, request an updated credit report to ensure that the correction has been accurately reflected in your credit history.

- Inform Your Lender: If you’re in the process of applying for a loan, inform your lender about the dispute and provide them with the corrected report once the issue is resolved. This will help ensure that your loan application is assessed based on accurate information.

By taking these steps, you can ensure that your credit report is accurate and error-free, giving you the best possible chance of securing a loan with favorable terms.

Can I Avail a Personal Loan with a Decent CIBIL Score through Pocketly?

Yes, you certainly can! Whilst not providing high loan amounts, Pocketly is certainly one of the online lending apps, which allows you to borrow small amounts of money in the form of personal loans.

Pocketly has been designed keeping in mind the common man of India. Not everyone could have a strong CIBIL Score, right? Especially if you’re a college student or a recent graduate or a young professional, you may not have a good score. You could also be the owner of a small business or even a self employed individual for that matter, Pocketly has got it covered for you!

You can avail your personal loan today, by just signing into our app. The two-step sign up process is so simple that it’s faster than cooking a packet of instant noodles!

Plus added to that is the fact that once you’ve gotten your loan sanctioned, your amount would reach your bank account directly within the matter of a few hours.

Unlike conventional banks, you don’t have to worry much about your CIBIL Score, but having a score close to 650 would make it easier for you to avail your instant loan right away. Doesn’t it seem more lenient than your regular bank loan, right?

What’s even more important is that Pocketly's flexible terms of repayment do not impact your CIBIL Score drastically as other loans might. So why don’t you try these amazing features today and apply now with Pocketly.

You can even download our app, available on both Google Play and the Apple App Store, and get started on your instant loan today!

Frequently Asked Questions

What is the Minimum CIBIL Score Required for Different Banks?

While the minimum CIBIL score required varies among banks, most lenders prefer a score of 750 and above for personal loan approval.

Can You Apply for Loans Without a CIBIL Score?

If you have no credit history and therefore no CIBIL score, some lenders may still offer loans based on your income, employment history, and other factors. However, the loan terms may not be as favorable.

Applying with a Low CIBIL Score?

If you have a low CIBIL score, you may still be able to secure a loan, but it will likely come with higher interest rates and stricter

What is a good CIBIL score for a loan?

A CIBIL score ranges between 300 and 900. You should ideally have a score that is closer to 900 as it helps you get better deals on loans and credit cards. Generally, a CIBIL score of 750 and above is considered as an ideal cibil/credit score by the majority of lenders.

Can I get a loan with a 700 CIBIL score?

Even with a score of 700, which is not very high, you can still apply for a personal loan. However, some lenders may charge you higher interest rates because your score is only moderate.

Is 680 a good CIBIL score?

A credit score of 680 is considered to be a fair one. Lenders consider individuals with this score as acceptable borrowers. Most lenders will be available and willing to lend. They offer various credit products for this score but not at the lowest interest rates.

How to get an 800 CIBIL score?

Paying all loan EMIs and credit card bills on time is the best way to achieve an 800 CIBIL score. To maintain a consistent repayment history, activate the e-mandate to clear your recurring payments before the due date automatically.

Is a 900 credit score possible?

While older models of credit scores used to go as high as 900, you can no longer achieve a 900 credit score. The highest score you can receive today is 850. Anything above 800 is considered an excellent credit score.

What is the Difference Between a Credit Score and a CIBIL Score?

- Credit Score: This is a general term that refers to a numerical representation of your creditworthiness. It typically ranges between 300 and 900 in India and is calculated based on factors like repayment history, credit utilization, credit history length, and types of credit used.

- CIBIL Score: This is a specific type of credit score provided by the Credit Information Bureau (India) Limited (CIBIL), which is one of the four major credit bureaus in India. CIBIL is the most widely known and used bureau in India, but it is not the only one. The term "CIBIL score" specifically refers to the score calculated by CIBIL based on your credit history as reported to them.