Securing a loan as a freelancer in India can be challenging. While freelancers often have steady income, the lack of salary slips and formal employment records can make lenders hesitant.

This issue becomes more significant as India’s gig economy grows. According to NITI Aayog and government data, India’s gig workforce is expected to reach 1 crore workers by 2024–25, with projections of 2.35 crore by 2029–30.

The problem isn't always income, but how it's assessed. Freelancers deal with irregular payment cycles, multiple income streams, and inconsistent monthly earnings—factors traditional loan systems don't easily accommodate, leading to delays or rejections.

However, credit access is improving. Today, digital lenders are increasingly evaluating freelancers based on bank transactions, income consistency, and repayment history, rather than just salary slips.

In this blog, we’ll explore how freelancers can secure loans in India, the best platforms to consider, what lenders look for, and tips to improve your chances of approval.

At a Glance

- Freelancers can get loans in India even without salary slips, but approval depends more on how income is documented and assessed.

- Lenders usually evaluate bank transactions, income consistency, credit score, and existing repayment obligations instead of fixed employment proof.

- The strongest loan applications come from freelancers who show stable cash flow, organised records, and responsible repayment behaviour over time.

- Loan amount, approval chances, and interest rate are shaped by financial reliability, not just total earnings or the number of clients you work with.

- Before taking a loan, freelancers should assess repayment timing carefully, since irregular client payments can create pressure even when overall income is healthy.

Why Getting a Loan for Freelancers Is More Difficult Than for Salaried Users

Freelancers often face more friction during loan applications, not because they earn less, but because their income structure does not fit traditional lending models.

Lenders are designed to evaluate predictable income. Salaried users typically provide fixed monthly payslips, employer details, and stable income records, which makes risk assessment straightforward. Freelancers, on the other hand, present a different financial pattern.

Here are the key reasons why getting a loan is more difficult for freelancers:

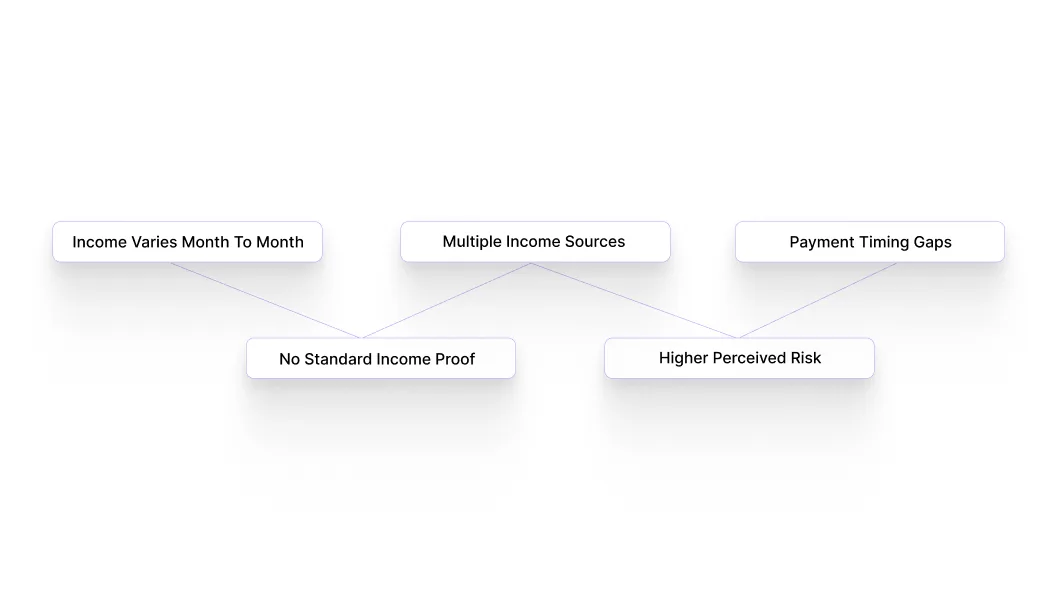

- Income is not fixed month-to-month: Even if the total annual income is strong, variations in monthly inflow can make it harder for lenders to assess repayment capacity.

- No standardised income proof: Freelancers do not have salary slips or employer-backed documents, which are commonly used in traditional loan evaluation.

- Multiple income sources create complexity: Payments may come from different clients, platforms, or projects, making income tracking less structured.

- Higher perceived risk from the lender’s perspective: Without consistent documentation, lenders may classify freelance income as less predictable compared to salaried income.

- Gaps between payments: Delays in client payments or irregular billing cycles can affect cash flow timing, even if overall earnings are stable.

For example, a freelancer may earn more than a salaried employee over a few months, but if the income comes in uneven intervals, it may still raise concerns during loan evaluation.

The challenge is not earning capacity, but how freelance income is structured and evaluated by lenders.

Also Read: Manage Your Finances With The Top 10 Budgeting Tips for Freelancers

How Lenders Evaluate Freelancers for Loan Approval (Beyond Salary Slips)

Since freelancers do not have traditional income proof, lenders rely on alternative ways to assess their financial stability and repayment capacity. The evaluation focuses more on patterns and consistency rather than on a fixed monthly income.

Here is what lenders typically look at:

- Bank transaction patterns: Regular inflow of payments, even from different sources, helps demonstrate active earnings and financial movement.

- Consistency of income over time: Lenders check whether income is recurring across months rather than one-time high payments.

- Average monthly balance and cash flow behaviour: Maintaining a stable balance and avoiding frequent overdrafts or low-balance situations improves credibility.

- Credit score and repayment history: A CIBIL score of 650 or above increases approval chances, as it reflects responsible borrowing behaviour in the past.

- Existing financial obligations: Ongoing EMIs or liabilities are considered to evaluate how much additional repayment you can handle.

- Type of work and earning stability: Freelancers with ongoing contracts, repeat clients, or steady project flow are viewed more favourably.

For example, a freelancer with steady monthly inflows through bank transactions and a good credit history is more likely to be approved than someone with irregular deposits and no repayment track record.

Lenders evaluate freelancers based on income patterns and financial behaviour, not just fixed salary proof.

Best Loan Apps and Platforms for Freelancers in India (Features, Pros, Cons)

Freelancers often need loan options that work with irregular income, faster approvals, and minimal documentation. The right platform is not just about availability, but how well it adapts to flexible income patterns and short-term needs.

Here are some of the most suitable loan apps and platforms for freelancers in India:

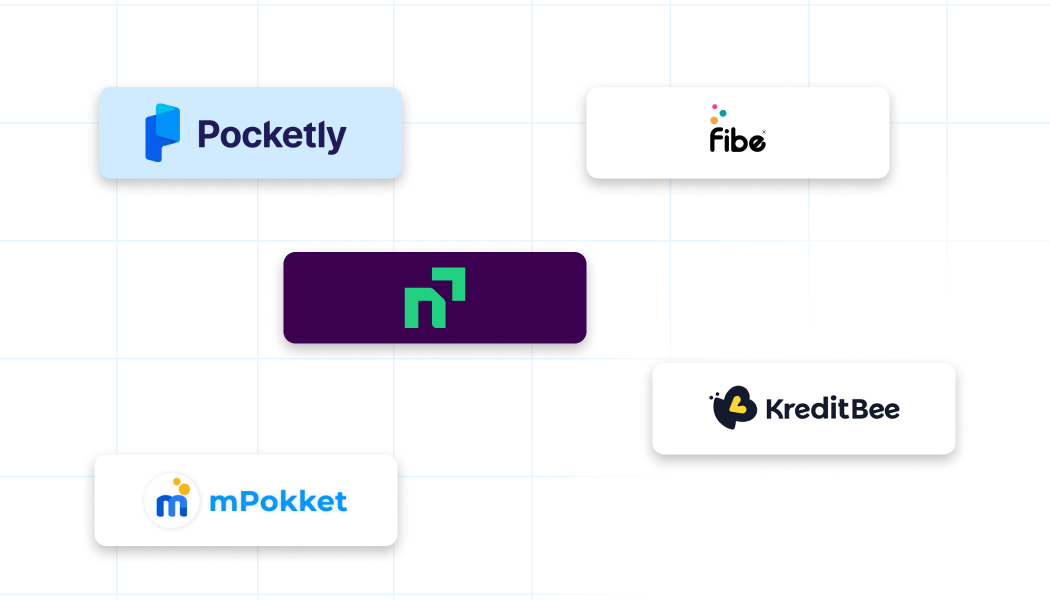

1. Pocketly

Pocketly is a great choice for freelancers in need of quick, short-term financial support. It is designed to address cash flow issues, like payment delays or timing gaps between projects. With its flexible and easy-to-use platform, Pocketly helps you access funds without the typical paperwork or lengthy approval processes.

Key Features:

- Loan Amounts: Borrow between ₹1,000 and ₹25,000, making it ideal for small, urgent financial needs. This range is suitable for freelancers who may need to cover everyday expenses or handle short-term lulls in income.

- Interest Rates: The interest starts from around 2% per month, which makes it a cost-effective solution for short-term borrowing. With low rates, freelancers don’t need to worry about steep financial burdens.

- Processing Fee: The processing fee ranges from 1% to 8%, based on your individual profile, ensuring that the costs remain flexible and tailored to your needs.

- Fully Digital Application: From application to approval, everything is done online. This quick, paperless process allows freelancers to apply anytime and anywhere without needing to visit a physical branch.

- No Collateral: Pocketly does not require any collateral, which is a big advantage for freelancers who may not own property or assets to pledge.

Pros:

- Quick Access to Funds: Since Pocketly operates with a fully digital process, freelancers can expect quick approvals and fast access to funds, often within hours. This is ideal when you need funds immediately to keep your work running smoothly.

- Flexible Loan Amounts for Freelancers: The loan amount range is perfect for freelancers who typically face cash flow gaps due to irregular payments. Whether it's covering business expenses or handling personal costs, Pocketly offers an accessible solution.

- Simple Process: The platform’s clear, easy-to-understand application makes the process smooth and stress-free. No long forms or excessive documentation, just a few details, and you're good to go.

- No Collateral Required: Since freelancers often don't have property to pledge, Pocketly's lack of collateral requirement makes it accessible to a wider group of borrowers who may not have assets to offer.

- Transparency: The platform is clear about its terms, so freelancers can avoid hidden fees or surprises, ensuring peace of mind during the borrowing process.

Cons:

- Limited Loan Amounts: The available loan amounts, ranging from ₹1,000 to ₹25,000, may not meet the needs of freelancers who require more substantial financial help for large projects or investments.

- Not Suitable for Long-Term Loans: Pocketly is focused on short-term borrowing, so it may not be the right fit for those needing loans for long-term financial planning or investments.

2. KreditBee

KreditBee offers personal loans with flexible options, making it suitable for freelancers who have moderate and consistent income patterns.

Key Features

- Loan amounts up to ₹2,00,000

- Flexible repayment tenure

- Digital application process

Pros

- Higher loan limits

- Widely accessible

Cons

- Approval depends on income consistency

- Higher cost for shorter tenures

3. Navi

Navi provides fully digital personal loans with competitive rates for users who meet credit and income criteria.

Key Features

- Quick approval process

- Competitive interest rates

- Flexible tenure

Pros

- Smooth user experience

- Lower rates for strong profiles

Cons

- Approval depends heavily on credit score

- Less flexible for highly irregular income

4. Fibe (EarlySalary)

Fibe offers instant loans with flexible repayment options and is commonly used by freelancers with a relatively stable inflow.

Key Features

- Instant approval

- Digital onboarding

- Flexible repayment

Pros

- Fast disbursal

- Suitable for short-term needs

Cons

- Cost may vary significantly

- Requires basic income stability

5. CASHe / mPokket

These platforms cater to younger users and freelancers looking for smaller loans with simplified processes.

Key Features

- Small-ticket loans

- Minimal documentation

- Quick approval

Pros

- Easy access for first-time borrowers

- Fast process

Cons

- Higher effective cost

- Limited loan amounts

If your income is irregular but your need is small and immediate, options like Pocketly can help bridge short-term gaps without complex approval requirements.

The best loan platform for freelancers is the one that aligns with how your income flows, not just how much you earn.

What Documents Freelancers Need to Apply for a Loan in India

Freelancers are not evaluated using salary slips, so the documentation required is focused on proving identity, financial activity, and income consistency through alternative records.

Here are the key documents typically required:

- KYC documents (PAN and Aadhaar): These are mandatory for identity verification and basic eligibility checks.

- Bank statements (last 3 to 6 months): This is the most important document for freelancers, as lenders use it to assess income inflow, frequency of payments, and financial behaviour.

- Income proof alternatives: Instead of salary slips, freelancers may provide invoices, client contracts, or payment receipts to support income claims.

- GST returns (if applicable): Freelancers registered under GST may use returns as additional proof of business activity and earnings.

- Basic profile details: Information about your work type, industry, and client base may also be required during the application.

For example, a freelancer with consistent bank inflows and clear transaction records is more likely to get approved than someone with irregular or unclear financial activity, even if total income is similar.

Freelancers are evaluated through financial activity and transaction history, not traditional salary documents.

What Impacts Loan Approval, Loan Amount, and Interest Rate for Freelancers

Once your documents are submitted, lenders move to a deeper evaluation stage where they decide whether to approve your loan, how much to offer, and at what cost. This decision is based on a combination of risk and repayment capacity.

Here are the key factors that influence this:

- Credit score and repayment track record: A CIBIL score of 650 or above generally improves approval chances and helps secure better interest rates.

- Stability of cash flow, not just total income: Lenders assess whether your income pattern supports regular repayment, even if the amounts vary month to month.

- Existing liabilities and financial commitments: Active EMIs or debts reduce the amount you may qualify for, as they impact your repayment capacity.

- Loan amount requested relative to income pattern: Requesting a realistic amount based on your inflow improves approval chances and reduces perceived risk.

- Type of lender and risk model used: Some digital lenders may offer more flexible terms for freelancers, while traditional lenders may apply stricter criteria.

In terms of cost, loan interest rates in India typically range between 10% to 24% annually, depending on your credit profile and lender policies.

Approval, loan amount, and interest rate are driven by how stable and reliable your financial profile appears, not just how much you earn.

Also Read: Instant Personal Loan Application for Self-Employed Individuals

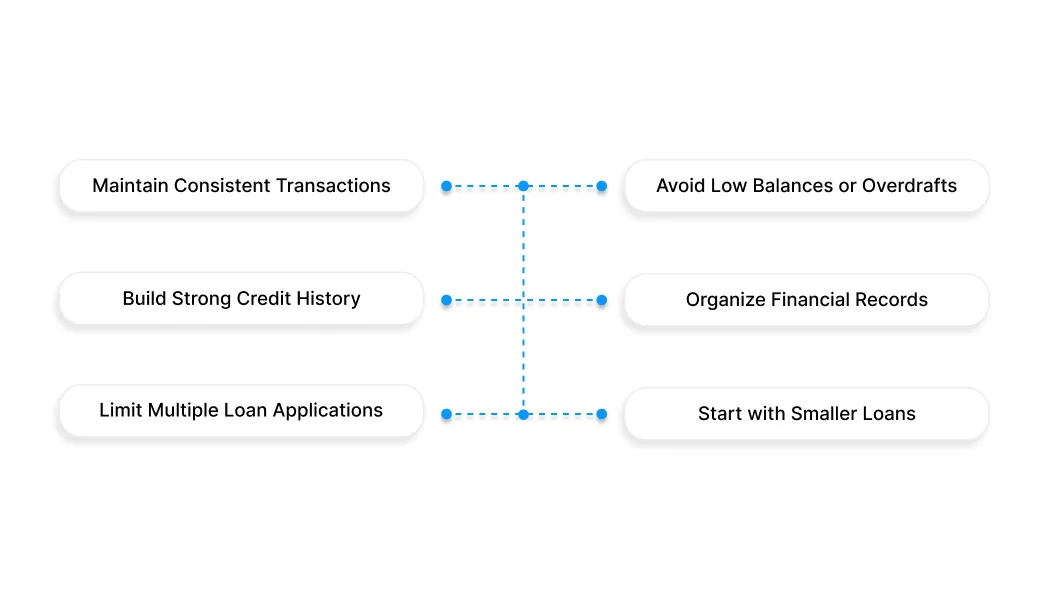

How Freelancers Can Improve Loan Approval Chances (Practical Steps)

Improving loan approval as a freelancer is not about changing your income type, but about making your financial profile easier for lenders to assess and trust.

Here are practical steps that can help:

- Maintain a consistent transaction pattern: Try to receive payments in a structured way through your primary bank account instead of multiple scattered accounts.

- Avoid frequent low-balance or overdraft situations: Keeping a stable account balance signals better financial discipline to lenders.

- Build and maintain a strong credit history: Timely repayment of any existing loans or credit cards helps improve your credit score over time.

- Keep financial records organised: Having clear invoices, payment records, and client details makes it easier to support your income during evaluation.

- Limit multiple loan applications at the same time: Applying across several platforms simultaneously can negatively impact your credit profile and reduce approval chances.

- Start with smaller loan amounts if needed: Building a repayment track record with smaller loans can improve eligibility for larger amounts later.

For example, a freelancer who maintains consistent bank inflows and avoids irregular financial behaviour is more likely to be approved than someone with the same income but less structured records.

If your income is irregular but your need is small and immediate, options like Pocketly can help bridge short-term gaps without complex approval requirements. Apply now!

Risks Freelancers Should Know Before Taking a Loan

Taking a loan as a freelancer requires careful consideration, especially because income patterns are not always predictable. Understanding the risks helps you avoid situations where repayment becomes difficult.

Here are the key risks to be aware of:

- Mismatch between repayment schedule and income timing: Fixed EMI dates may not always align with when you receive payments, which can create pressure during repayment.

- Higher cost for short-term or flexible loans: Some loans designed for quick access may have higher effective costs compared to traditional loans.

- Overestimating future income: Relying on expected client payments that may be delayed can lead to repayment challenges.

- Stacking multiple small loans: Taking multiple short-term loans at the same time can increase the overall repayment burden without clear visibility.

- Limited flexibility in repayment terms: Some lenders may not offer flexibility once the loan is approved, which can be difficult for fluctuating income situations.

For example, taking a loan based on an expected payment that gets delayed can lead to stress, penalties, or the need for additional borrowing.

The main risk is not borrowing itself, but misalignment between your repayment commitments and actual cash flow timing.

How Pocketly Helps Freelancers Manage Irregular Cash Flow

Freelancers often deal with gaps between completed work and received payments. These gaps are not about lack of income, but about timing, which can affect day-to-day expenses or urgent payments.

Pocketly is designed to address this exact situation by focusing on small, short-term borrowing needs rather than large, long-term commitments.

Here is how it fits into a freelancer’s workflow:

- Bridges payment timing gaps: When client payments are delayed or staggered, a small loan can help maintain continuity without disrupting ongoing work or commitments.

- Keeps borrowing aligned with actual need: Loan amounts from ₹1,000 to ₹25,000 make it suitable for temporary shortfalls instead of long-term financial obligations.

- Supports quick access without complex processes: A fully digital flow allows freelancers to apply and get access without lengthy documentation or approvals.

- Cost structure suited for short-term use: Interest starts from around 2% per month, with processing fees between 1% and 8%, depending on the borrower profile and loan amount.

- No collateral requirement: The loan is unsecured, making it accessible without tying up assets.

For example, if a freelancer is waiting for a payment from a client but needs to cover an immediate expense, a small, short-term loan can help manage the gap without affecting ongoing financial commitments.

If you need quick access to a small loan between payments, you can download Pocketly on iOS or Android and check your eligibility to get started.

FAQs

Q: Can freelancers get a loan without a salary slip in India?

Yes, freelancers can get a loan without a salary slip through digital lenders. These platforms evaluate bank statements, income patterns, and credit history instead of fixed employment proof.

Q: What is the best loan for freelancers with irregular income?

The best loan for freelancers depends on the need, but short-term digital loans are often more suitable for irregular income. They offer faster approval and flexibility compared to traditional personal loans.

Q: How do lenders verify freelancer income for loan approval?

Lenders verify freelancer income using bank statements, transaction consistency, and past repayment behaviour. Some also consider invoices or client payments as supporting proof.

Q: What is the minimum CIBIL score required for freelancers to get a loan?

Most lenders prefer a CIBIL score of 650 or above for better approval chances. However, some digital platforms may still offer loans based on alternative credit assessment methods.

Q: What documents are required for a loan for freelancers in India?

Freelancers typically need PAN, Aadhaar, and bank statements for the last 3 to 6 months. Additional documents like invoices or GST returns may be required depending on the lender.

Q: Are there instant loan apps for freelancers in India?

Yes, several digital lending apps offer instant loans for freelancers with minimal documentation. These apps focus on quick approval and shorter loan cycles.

Q: How can freelancers improve their chances of getting a loan approved?

Freelancers can improve approval chances by maintaining consistent bank inflow, avoiding missed payments, and keeping a good credit score. Clear financial records also help lenders assess eligibility more easily.

Q: Can freelancers get small loans for short-term needs?

Yes, freelancers can access small-ticket loans designed for short-term needs. Platforms like Pocketly offer loans that help manage temporary cash flow gaps between client payments.