Getting access to money when you need it should not feel like a battle. Yet for many borrowers in India, choosing between instant approval loans and traditional bank loans can be confusing. One promises speed and minimal paperwork. The other offers stability and potentially lower interest rates. The real challenge is knowing which one actually fits your situation.

When an emergency expense hits or a major financial goal comes up, delays can cost more than just time. Waiting days or weeks for approval can add stress, while rushing into the wrong loan can increase your overall repayment burden.

Understanding the difference between instant approval loans and traditional bank loans helps you make a decision based on urgency, cost, and long-term impact. This blog will break down how both options work so you can choose confidently instead of reacting under pressure.

TL;DR

- Instant approval loans provide fast disbursal, minimal documentation, and smaller loan amounts, making them suitable for urgent, short-term cash needs.

- Traditional bank loans offer lower interest rates, higher loan limits, and longer repayment tenures, ideal for planned or large expenses.

- The right option depends on urgency, total borrowing cost, eligibility criteria, and repayment capacity.

- Choosing based only on speed or interest rate can lead to higher long-term financial strain.

- Comparing approval time, flexibility, penalties, and total repayment amount helps borrowers make a financially sound decision.

What Are Instant Approval Loans?

Instant approval loans are short-term, unsecured loans designed to provide quick access to funds through a fully digital process. Unlike traditional borrowing, there is no need to visit a branch, submit physical paperwork, or wait several days for manual verification. The application, KYC, approval, and disbursement are typically completed online.

The core purpose is speed. These loans are built for situations where waiting is not an option.

Common characteristics of instant approval loans include:

- Unsecured borrowing: No collateral or guarantor is required.

- Minimal documentation: Basic KYC, identity proof, and income details are usually sufficient.

- Fast decision-making: Approval decisions are often provided within minutes or a few hours.

- Short repayment tenure: Loan durations are generally brief, ranging from a few weeks to a few months.

- Moderate loan amounts: Best suited for small- to mid-sized financial needs rather than large, long-term commitments.

Example: If your salary is delayed and you need funds for rent or an urgent repair, an instant approval loan can bridge the gap quickly without a lengthy approval cycle.

What Are Traditional Bank Loans?

Traditional bank loans are structured credit products offered by banks through a more detailed underwriting process. Unlike instant approval loans, these loans typically involve in-depth eligibility checks, income verification, credit score evaluation, and physical or digital documentation review before approval.

The primary focus is stability and structured repayment over a longer tenure.

Common characteristics of traditional bank loans include:

- Detailed eligibility assessment: Banks evaluate income stability, employment history, credit score, and existing liabilities before approving the loan.

- Extensive documentation: Salary slips, income tax returns, bank statements, identity proof, and address verification are usually required.

- Longer repayment tenure: Loan terms can range from one year to several years, depending on the loan type.

- Higher borrowing limits: Suitable for larger financial needs such as home renovation, education, or business expansion.

- Lower interest rates: compared to short-term digital loans, especially for borrowers with strong credit profiles.

Example: If you are planning a major expense like funding higher education or consolidating multiple debts, a traditional bank loan may offer a larger amount and longer repayment period at a more competitive interest rate.

Instant Approval Loans vs Traditional Bank Loans: Detailed Comparison

The choice between instant approval loans and traditional bank loans should be based on context, not convenience alone. Speed, borrowing costs, eligibility requirements, and repayment structure all impact your long-term financial stability.

Before selecting either option, it is important to compare how they differ in approval timelines, loan size, interest burden, and flexibility. The table below outlines the key distinctions to help you make a practical and informed decision.

| Criteria | Instant Approval Loans | Traditional Bank Loans |

| Processing Speed | Approval is often within minutes or hours | Approval may take several days or weeks |

| Application Mode | Fully digital through apps or websites | Branch-based or detailed online process |

| Documentation Level | Basic KYC and limited income proof | Salary slips, ITR, bank statements, and credit checks |

| Loan Size | Usually small to mid-sized amounts | Suitable for large borrowing needs |

| Interest Cost | Typically higher due to the short-term nature | Generally lower for strong credit profiles |

| Repayment Period | Short tenure, often a few months | Longer tenure can extend to several years |

| Eligibility Strictness | Relatively flexible criteria | Strict eligibility and credit evaluation |

| Disbursement Time | Often, the same day after approval | Disbursed after full verification cycle |

| Financial Commitment | Designed for temporary cash gaps | Structured for long-term financial planning |

| Risk of Overborrowing | Lower ticket size but frequent borrowing risk | Larger commitment but predictable EMI structure |

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

When Should You Choose an Instant Approval Loan?

An instant approval loan makes sense when speed matters more than long-term cost. It is not designed for major financial commitments, but for temporary, urgent gaps where waiting could create additional stress.

Choose an instant approval loan if:

Choose an instant approval loan if:

1. During Time-Sensitive Emergencies

Instant approval loans are most appropriate when urgency outweighs cost considerations. In emergencies, the priority is immediate access to funds rather than optimising interest rates. Delays in such situations can lead to penalties, service disruption, or added stress.

For example, an unexpected medical bill, urgent travel requirement, or critical appliance repair may need same-day payment. Waiting a week for bank approval could worsen the situation financially or personally.

2. When You Need a Small, Clearly Defined Amount

These loans are structured for limited borrowing needs, not large financial commitments. If you know the exact amount required and plan to repay it quickly, a short-term digital loan can be efficient.

For instance, borrowing ₹7,000 to manage a temporary shortfall is more practical through a fast approval channel than initiating a lengthy bank loan process meant for larger sums.

The key is discipline. Borrow only what is necessary and align repayment with your next income cycle.

3. If Convenience and Speed Matter More Than Cost

For many working professionals, time is a constraint. Gathering documents, visiting branches, and waiting for approval may not be feasible during busy schedules. A fully digital loan process simplifies the experience.

For example, completing KYC verification through an app and receiving funds within hours can reduce both logistical effort and stress.

However, this convenience typically comes at a higher interest cost, so the trade-off should be intentional.

4. To Bridge a Predictable Salary Gap

Short-term loans can act as temporary cash flow stabilisers when income and expenses are misaligned. This is common when large payments such as rent, school fees, or EMIs fall just before salary credit.

For instance, if fixed expenses are due three to five days before payday, a small loan can prevent late fees while maintaining your payment record.

This approach works best when repayment is planned and does not extend beyond one salary cycle.

5. When Your Credit Profile Limits Traditional Options

If your credit history is limited or your score does not meet strict bank criteria, instant approval lenders may offer slightly more flexible evaluation models. While approval is not guaranteed, digital platforms may consider income consistency and transaction patterns alongside credit scores.

For example, a young professional with a short credit history but steady monthly income may find it easier to qualify for a smaller digital loan than a large bank facility.

In such cases, responsible borrowing and timely repayment can also help strengthen your credit profile over time.

When Should You Choose a Traditional Bank Loan?

Traditional bank loans are better suited for structured, long-term financial commitments where cost, stability, and repayment planning matter more than speed. They involve more paperwork and waiting time, but they often reward borrowers with lower interest rates and better repayment terms.

Choose a traditional bank loan if:

1. For Large Financial Commitments

Traditional bank loans are better suited for significant expenses that require substantial funding. These may include higher education, home renovation, medical procedures, or business investment.

For example, if you need ₹5–10 lakh for a major planned expense, a bank loan offers higher borrowing limits and structured repayment over several years, which keeps monthly EMIs manageable.

2. When You Want Lower Overall Interest Cost

If time is not a constraint and you qualify under bank eligibility norms, traditional loans generally offer lower interest rates compared to short-term digital loans. Over a longer tenure, this can result in meaningful savings.

For instance, choosing a lower-interest loan for a two-year repayment plan can reduce the total cost significantly compared to repeated short-term borrowing.

3. If You Have a Strong Credit Profile

Borrowers with stable income, good credit scores, and low existing liabilities are more likely to secure favourable terms from banks. This includes better interest rates, higher loan amounts, and longer tenures.

For example, a salaried professional with a strong repayment history may negotiate better loan conditions that reduce financial pressure over time.

4. When You Prefer Structured, Predictable Repayment

Traditional loans come with fixed EMIs and clearly defined repayment schedules. This structure supports long-term financial planning and reduces uncertainty.

For instance, if you are planning around multiple financial responsibilities such as rent, investments, and insurance, a fixed EMI structure makes cash flow forecasting easier.

5. When the Expense Is Planned, Not Urgent

Bank loans are ideal when you can afford the approval timeline. If the expense is planned weeks or months in advance, you can complete documentation comfortably and secure more cost-effective financing.

For example, funding a professional certification or planned home improvement project allows enough time to go through proper underwriting without pressure.

Read More: How to Achieve a Perfect 900 CIBIL Score?

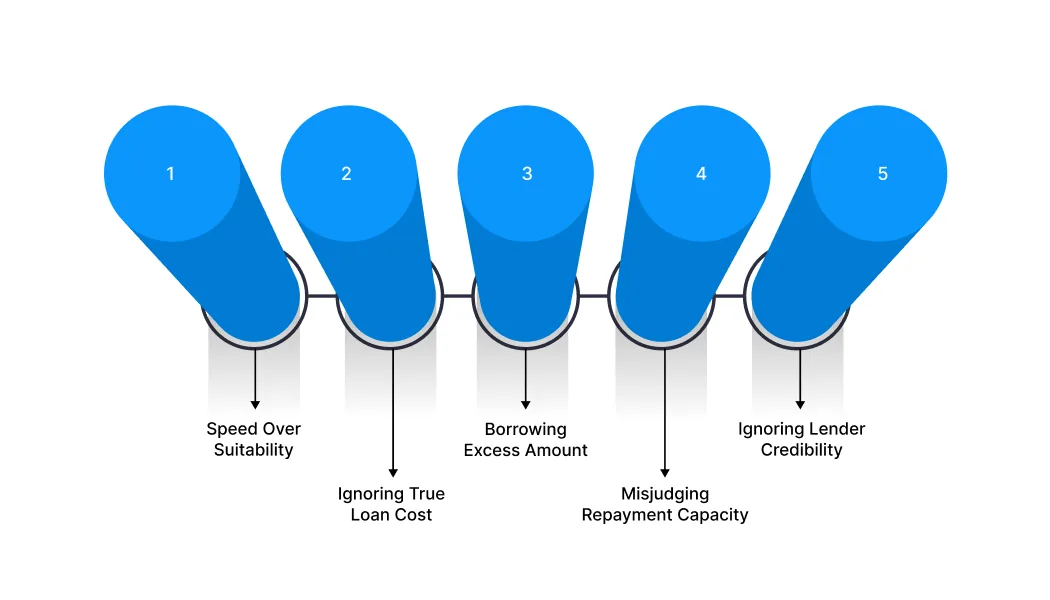

Common Mistakes Borrowers Make While Taking Loans

Even after understanding the differences between instant approval loans and traditional bank loans, borrowers often make avoidable errors during the final decision stage. These mistakes usually happen due to urgency, lack of clarity, or incomplete cost evaluation. Recognising them early can protect your credit profile and long-term financial stability.

Here are the most common borrowing mistakes and how to avoid them:

Here are the most common borrowing mistakes and how to avoid them:

1. Prioritising Speed Over Suitability

Risk: Choosing a loan simply because it offers instant approval can result in higher interest rates, shorter repayment windows, and avoidable financial strain. Convenience without evaluation often leads to expensive borrowing decisions.

Mitigation: Assess whether the loan matches your actual need. Compare tenure, EMI, total repayment amount, and flexibility before confirming. Speed should support your decision, not drive it.

2. Overlooking the True Cost of the Loan

Risk: Many borrowers focus only on the monthly EMI or advertised interest rate, ignoring processing fees, platform charges, penalties, and GST. This creates a gap between expected and actual repayment.

Mitigation: Review the complete cost structure, including all charges and the final repayment amount. Make decisions based on total cost, not just the rate displayed upfront.

3. Borrowing Beyond Immediate Requirements

Risk: Taking a larger loan than necessary increases both repayment pressure and total interest paid. It may also lead to poor financial discipline or dependency on rolling credit.

Mitigation: Clearly define the purpose of the loan and calculate the minimum amount required. Smaller, well-planned borrowing is easier to manage and repay responsibly.

4. Misjudging Repayment Capacity

Risk: Assuming future income growth or ignoring existing financial commitments can lead to missed EMIs. Even short delays can impact your credit profile and increase penalties.

Mitigation: Evaluate your monthly cash flow realistically. Ensure the EMI fits within your surplus income after accounting for essentials and ongoing obligations.

5. Ignoring Lender Credibility

Risk: Borrowing from unverified digital platforms increases the risk of hidden charges, unclear terms, and aggressive recovery practices. This can create both financial and emotional stress.

Mitigation: Verify that the lender operates under proper regulatory oversight. Read loan terms carefully, check customer feedback, and confirm transparency before proceeding.

Instant Approval Loans for Emergencies: How Pocketly Fits In

Unexpected expenses can disrupt even a well-planned budget. Whether it is a medical bill, urgent travel, or a temporary cash shortfall, waiting days for a traditional bank loan may not be practical. Pocketly is designed for such moments, offering small, short-term loans with a fast and fully digital process.

- Loan amounts from ₹1,000 to ₹25,000: You borrow only what is required, which helps keep repayments manageable and avoids unnecessary debt.

- Collateral-free access: No need for assets or a guarantor, making it accessible to students and young professionals.

- Quick digital verification: A streamlined KYC-based process enables fast eligibility checks without physical paperwork.

- Fast disbursal: Once approved, funds are transferred directly to your bank account, helping you address urgent needs without delay.

- Flexible repayment options: You can choose a tenure that aligns with your monthly cash flow and budgeting capacity.

- Transparent pricing: Interest rates start from 2% per month, with processing fees typically ranging between 1% and 8%, depending on your profile and loan amount.

- 24/7 mobile access: Applications, tracking, and repayments are managed entirely through the Pocketly app.

When used thoughtfully, Pocketly can provide timely support without derailing your broader financial goals.

Conclusion

Instant approval loans and traditional bank loans are designed for different financial situations. The right choice depends on how urgently you need funds, how much you plan to borrow, and how comfortably you can repay it.

Traditional bank loans work well for larger, planned expenses where lower interest rates and longer tenures matter. Instant approval loans are better suited for short-term, urgent needs where speed and minimal documentation are priorities.

The smart approach is simple: evaluate the total cost, borrow only what is necessary, and ensure repayments fit within your monthly budget. Credit should act as support, not create additional financial pressure.

If you are facing a temporary cash shortfall and need quick access to funds, Pocketly offers a fast and transparent solution with flexible repayment options.

Download the Pocketly app today on [Android] or [iOS] to manage urgent expenses confidently while staying aligned with your financial goals.

FAQs

1. What is the difference between instant approval loans and traditional bank loans?

Instant approval loans are processed digitally with minimal paperwork and fast disbursal. Traditional bank loans involve stricter eligibility checks, detailed documentation, and longer approval timelines.

2. Are instant approval loans more expensive?

They often come with higher interest rates due to the speed and convenience offered. Bank loans generally have lower interest rates but stricter approval criteria.

3. Which loan is better for emergencies?

Instant approval loans are more suitable for urgent, short-term needs because funds are disbursed quickly. Bank loans are better for planned, larger financial requirements.

4. Do I need a high credit score for instant approval loans?

Not necessarily. Eligibility is often more flexible than traditional banks, but your credit profile can still influence approval and loan terms.

5. Can I borrow large amounts through instant approval loans?

These loans are usually designed for smaller amounts. For higher loan requirements, traditional banks are typically the better option.

6. Is the documentation process different?

Instant approval loans require basic KYC and limited documentation. Bank loans typically require proof of income, bank statements, and additional verification.