You start the month feeling sorted. Your allowance is credited, maybe a bit of part-time income too, and everything seems manageable. Then suddenly it is the 20th, and your account balance is almost zero. You are wondering where the money went and whether you should ask for more or survive on the bare minimum.

This happens to most students, not because they are irresponsible, but because there is no clear spending plan. Small daily expenses, food orders, travel, outings, and surprise college costs quietly drain your balance. The stress builds up every month.

The fix is simpler than you think. In this blog, we will break down how to create a practical student monthly budget, share a realistic spending structure, and show you how to manage your money confidently without sacrificing your college life.

What Is a Student Monthly Budget?

A student's monthly budget is a simple financial plan that helps them manage their income and expenses over a month. It tells you how much you can spend, how much you should save, and where your money needs to go.

For most students, income comes from allowances, scholarships, stipends, or part-time jobs. Since this amount is usually fixed and limited, planning becomes essential. Without a budget, small daily expenses like food delivery, cab rides, and online subscriptions can quickly drain your balance.

A proper student monthly budget divides money into categories such as accommodation, food, transport, academic costs, and personal spending. When you allocate money in advance, you reduce financial stress and avoid running out of funds before the month's end.

In short, it is not about restriction. It is about control and clarity.

Why Every Student Needs a Monthly Budget?

Managing money as a student is different from earning a full salary. Your income is usually fixed and limited, but your expenses can change every week. Without a clear budget, it becomes easy to overspend early and struggle later.

Managing money as a student is different from earning a full salary. Your income is usually fixed and limited, but your expenses can change every week. Without a clear budget, it becomes easy to overspend early and struggle later.

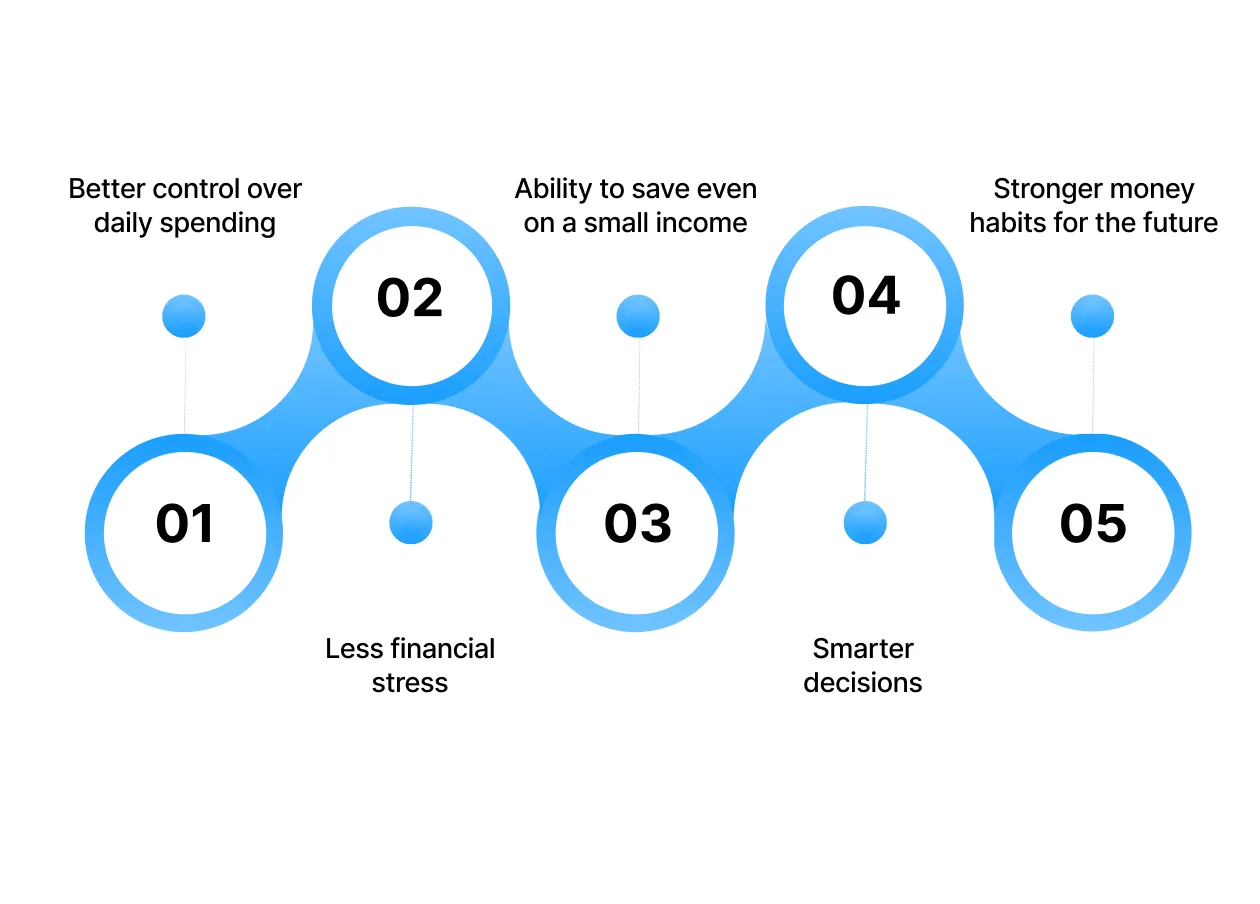

Here is why creating a student's monthly budget is important:

- Better control over daily spending: When you know how much you can spend on food, outings, and shopping, you avoid random impulse purchases that drain your balance.

- Less financial stress: A clear budget reduces the anxiety of checking your account balance every few days or worrying about running out of money before the month end.

- Ability to save even on a small income: Even setting aside a small amount each month builds discipline and creates a safety cushion for emergencies.

- Smarter decisions: Budgeting helps you separate needs from wants, so you can prioritise essentials without feeling restricted.

- Stronger money habits for the future: Learning to manage money in college prepares you for handling salary, rent, EMIs, and larger responsibilities later in life.

How Much Does a Student Spend in a Month?

A student’s monthly expenses depend on the city, living situation, and lifestyle. Someone staying in a hostel in a Tier 2 city will likely spend less than a student renting a PG in Mumbai or Bengaluru. Still, most student budgets follow a similar structure.

Here are the common spending categories:

| Expense Type | Category | Typical Monthly Cost (INR) |

| Fixed | Rent / Hostel / PG | ₹5,000 – ₹20,000 |

| Fixed | Utilities (Electricity, Internet, Phone) | ₹1,000 – ₹5,000 |

| Variable | Food & Groceries | ₹3,000 – ₹8,000 |

| Variable | Transportation | ₹500 – ₹2,500 |

| Variable | Study Materials & Books | ₹500 – ₹3,000 |

| Variable | Personal & Miscellaneous | ₹1,000 – ₹5,000 |

| Estimated Total Monthly Budget | ₹11,000 – ₹43,000 |

Also Read: Understanding Differences between Form 16, Form 16A and Form 16B

How to Create a Student Monthly Budget That Actually Works

Creating a student's monthly budget is not about restricting every expense. It is about knowing where your money goes and making intentional decisions. Here is a simple step-by-step approach you can follow.

1. Calculate Your Total Monthly Income

A budget built on unclear income will fail quickly. Start by identifying all consistent and predictable money you receive each month. This includes allowance from parents, part-time job earnings, internships, stipends, scholarships, or recurring freelance work. Avoid counting one-time gifts or irregular income unless you are certain it will continue.

The key is to work with your minimum guaranteed amount, not your best-case scenario. Suppose your part-time income fluctuates between ₹3,000 and ₹6,000, budget using ₹3,000. This prevents overspending during slower months.

For instance, if you receive ₹8,000 as allowance and reliably earn ₹4,000 from tutoring, your practical monthly income is ₹12,000. This becomes the foundation of every spending decision you make.

2. Prioritise Fixed Expenses First

Fixed expenses are commitments you cannot delay without consequences. Rent, hostel fees, mess charges, WiFi, electricity, subscriptions, and mobile bills should be allocated immediately after your income is credited.

Many students overspend early in the month on food delivery, outings, or shopping and then struggle to cover essentials. Allocating fixed costs first removes this risk entirely.

For example, if your rent is ₹6,000, utilities are ₹1,000, and your phone bill is ₹500, ₹7,500 is already committed. Once this is set aside, you know exactly how much remains for variable spending. This clarity reduces anxiety and prevents last-minute borrowing.

3. Estimate Variable Expenses Realistically

Variable expenses are where most budgeting mistakes happen. Food delivery, transport, coffee runs, subscriptions, online shopping, and weekend outings can quietly exceed your expectations.

Instead of guessing, review your last two to three months of UPI or bank transactions. Categorise them. You may discover patterns like frequent small payments that add up significantly.

For example, daily ₹150 food deliveries can easily cross ₹4,000 a month. Similarly, frequent cab rides instead of public transport may double your transport budget. When you see actual numbers, it becomes easier to adjust consciously rather than react emotionally at the end of the month.

Realistic budgeting is not about cutting everything. It is about aligning your spending with your priorities.

4. Set a Small but Non-Negotiable Savings Target

Even as a student, building a financial cushion is crucial. Unexpected expenses like medical needs, exam fees, travel, or device repairs can disrupt your entire month.

Start small but stay consistent. Saving 5 to 10 per cent of your income is a practical starting point. Treat this amount as compulsory, just like rent.

For example, saving ₹1,000 from a ₹12,000 monthly income may not feel significant immediately. However, in six months, you build ₹6,000. In a year, ₹12,000. That buffer reduces dependence on friends or short-term borrowing during emergencies.

Consistency matters more than size.

5. Track and Adjust Weekly

A budget is not something you create once and forget. It needs regular monitoring. Weekly reviews help you identify overspending early and course correct before the situation becomes stressful.

Set aside 10 minutes every Sunday to review your expenses. Compare what you planned versus what you actually spent. If you exceeded your food budget in week one, reduce discretionary spending in week two.

For instance, if 70 per cent of your eating out budget is gone halfway through the month, you can switch to home-cooked meals for the remaining weeks. Small adjustments prevent financial panic at the end of the month.

6. Separate Needs From Wants Clearly

One of the biggest budgeting mistakes students make is treating every expense as essential. Rent, groceries, transport, and academic materials are needs. Frequent food delivery, impulse shopping, and subscription upgrades are wants.

The problem is not spending on wants. The problem is not recognising them as optional.

For example, buying course books is necessary. Ordering late-night snacks three times a week is optional. When you consciously label expenses, it becomes easier to cut back temporarily if money feels tight.

This clarity helps you protect essentials while keeping lifestyle spending under control.

7. Create a Small Emergency Buffer Category

Even with savings, it helps to set aside a small monthly buffer specifically for unpredictable costs. College life is full of surprises, such as last-minute events, extra academic fees, travel plans, or minor medical expenses.

Instead of disrupting your entire budget, create a “miscellaneous” category with a fixed limit.

For instance, allocating ₹500 to ₹1,000 for unexpected expenses ensures that small surprises do not force you to dip into savings or borrow money. If unused, you can roll it into savings at the end of the month.

This makes your budget more resilient and realistic.

8. Use a Simple Tracking System You Will Actually Stick To

A complicated spreadsheet is useless if you stop updating it after two weeks. Choose a system that matches your habits.

Some students prefer a budgeting app, while others use a basic notes app or even a physical notebook.

The goal is consistency, not perfection.

For example, simply noting daily expenses in your phone every night builds awareness. Over time, you naturally start questioning unnecessary purchases before making them.

Budgeting works best when tracking feels effortless, not overwhelming.

Also Read: Understanding TAN and Its Application

Common Student Budgeting Mistakes to Avoid

Even with the best intentions, many students struggle to stick to their monthly budget. The issue is rarely a lack of income. It is usually avoidable mistakes that quietly derail the plan.

Even with the best intentions, many students struggle to stick to their monthly budget. The issue is rarely a lack of income. It is usually avoidable mistakes that quietly derail the plan.

1. Underestimating Small Daily Expenses

Risk: Small, frequent purchases like coffee, snacks, auto rides, or food delivery may feel insignificant individually, but together they can create a major gap between your planned and actual spending.

Mitigation: Track every expense, even the ₹50 and ₹100 ones. Review weekly totals to identify patterns. Setting a fixed cap for discretionary daily spending helps prevent these micro expenses from spiralling.

2. Ignoring Irregular or Seasonal Costs

Risk: Expenses such as exam fees, college trips, festival travel, annual subscriptions, or medical costs can disrupt your budget if they are not planned in advance.

Mitigation: Break large, occasional expenses into smaller monthly allocations. If you expect a ₹6,000 annual cost, set aside ₹500 per month so it does not feel overwhelming later.

3. Budgeting Based on Expected Income

Risk: Planning your expenses around income that is not guaranteed, such as freelance gigs or fluctuating part-time shifts, can lead to shortfalls during slower months.

Mitigation: Build your budget using your minimum assured income. Treat additional earnings as surplus and allocate them to savings rather than essentials.

4. Not Reviewing the Budget Regularly

Risk: Spending habits change over time. Without regular reviews, small deviations can turn into large financial gaps by the end of the month.

Mitigation: Schedule a weekly check-in to compare planned versus actual expenses. Early adjustments are easier than last-minute corrections.

5. Emotional or Impulse Spending

Risk: Stress, peer pressure, social media influence, and limited-time offers can lead to purchases that were never part of your plan.

Mitigation: Use a simple pause rule. Wait 24 hours before making non-essential purchases. This reduces emotional decisions and improves financial discipline.

Tools and Apps to Manage Your Student's Monthly Budget

The right tools can turn budgeting from a stressful task into a simple monthly habit. Whether you need tracking support, better visibility, or a financial backup option, here are practical tools that can help students manage their money more effectively.

1. Pocketly

Pocketly is built specifically for students and young professionals who may not have access to traditional credit options. It acts as a short-term financial bridge when your monthly budget falls short due to emergencies, urgent bills, or timing gaps between income and expenses.

USP: Quick access to small ticket loans without collateral and with transparent pricing

Best for: Students facing temporary cash shortfalls or unexpected expenses

Key Features:

- Loan amounts range from ₹1,000 to ₹25,000, so you borrow only what is required

- No collateral or guarantor is needed, making it accessible for students

- Fast approval through quick digital KYC verification

- Direct bank transfer after approval, often within minutes

- Flexible repayment tenures aligned with your budget cycle

- Interest starting from 2 percent per month, and processing fees typically between 1 percent and 8 per cent

- Fully digital mobile app access, available 24/7

Pocketly works best as a responsible backup option. Instead of disrupting your long-term financial plan, it helps you manage short-term liquidity gaps in a structured way.

2. Budgeting and Expense Tracking Apps

Budgeting apps categorise your expenses automatically and provide a clear visual breakdown of where your money goes each month. This reduces manual effort and increases awareness.

USP: Real-time visibility into spending patterns

Best for: Students who want automated tracking and spending insights

Key Features:

- Automatic expense categorisation

- Monthly and weekly spending summaries

- Budget limit alerts and notifications

- Visual graphs to track category-wise spending

- Goal-based savings tracking

These apps are ideal if you struggle to manually track expenses or want data-driven insights to improve spending habits.

3. Spreadsheets

Using Excel or Google Sheets gives you complete control over how your budget is structured. You can customise categories, track monthly variations, and analyse trends over time.

USP: High flexibility and long-term tracking capability

Best for: Students who prefer structured and detailed financial planning

Key Features:

- Planned versus actual expense comparison

- Monthly savings rate calculation

- Custom budget categories

- Multi-month tracking for pattern analysis

- Scenario planning for income changes

Spreadsheets are powerful for students who want deeper financial discipline and enjoy structured analysis.

4. Notes App or Manual Daily Log

Writing down daily expenses in your phone’s notes app or a notebook increases spending awareness without complexity. The simplicity improves consistency.

USP: Low effort and easy to sustain

Best for: Beginners who want a simple habit-building approach

Key Features:

- Quick daily expense logging

- No setup or technical knowledge required

- Encourages mindful spending

- Helps identify impulse purchases

This method works well if you are just starting to manage your student's monthly budget.

5. Bank and UPI Transaction History

Your banking or UPI apps already contain detailed transaction histories. Reviewing two to three months of data gives you a realistic understanding of your spending patterns.

USP: Uses actual spending data instead of estimates

Best for: Students who want accurate budgeting based on real data

Key Features:

- Access to detailed transaction records

- Easy identification of high spending categories

- Historical comparison across months

- Helps create realistic budget benchmarks

This approach ensures your budget is based on facts, not assumptions.

Smart Saving Tips for Students on a Tight Budget

Saving money as a student may feel unrealistic, especially when income is limited. However, small, consistent actions can create meaningful financial stability over time. The goal is not drastic restriction but smarter spending decisions.

1. Pay Yourself First

The most effective way to save as a student is to remove the decision from your hands. Instead of saving whatever is left at the end of the month, set aside a fixed amount the moment you receive money.

When savings happen first, spending naturally adjusts to what remains.

For example, if you receive ₹12,000 monthly and immediately move ₹1,000 into a separate account, you train yourself to live on ₹11,000. Over a year, that becomes ₹12,000 saved without feeling like a sacrifice. This simple shift builds financial discipline faster than trying to save sporadically.

2. Optimise the Timing of Your Purchases

Strategic timing can stretch your budget significantly without changing your lifestyle. Many students overspend simply because they buy at the wrong time.

For instance, purchasing electronics during festive sales, buying winter clothing at the end of season clearance, or renewing subscriptions during discount offers can reduce costs by 20 to 50 per cent. Similarly, stocking up on non-perishable groceries during bulk discounts prevents higher last-minute spending.

Over an academic year, better timing alone can save several thousand rupees without restricting your needs.

3. Control High-Frequency Expenses

It is rarely one large purchase that breaks a student’s budget. It is repeated small spending. Daily food delivery, frequent cab rides, snacks between classes, and impulse online orders slowly drain cash flow.

Instead of eliminating these entirely, reduce frequency. Cooking at home four extra times a week or switching to public transport twice a week can lower your monthly expenses substantially.

For example, cutting ₹150 daily discretionary spending can free up ₹4,000 to ₹4,500 per month. Small daily discipline creates a large monthly impact.

4. Use Cost Sharing Strategically

Student life offers built-in opportunities to reduce expenses through sharing. Rent, groceries, OTT subscriptions, transport, and even study materials can be shared responsibly.

For example, splitting WiFi and electricity with roommates reduces fixed costs. Buying groceries together lowers per-unit costs. Sharing textbooks instead of buying new copies for each semester prevents duplicate spending.

Cost sharing does not reduce quality of life. It simply reduces individual burden.

5. Plan and Pre-Fund Bigger Expenses

Unexpected spending feels stressful. Planned spending feels controlled. If you know you will need money for travel, a college event, a certification course, or a gadget upgrade, start setting aside small amounts in advance.

For example, if you plan to spend ₹8,000 in four months, saving ₹2,000 per month spreads the load evenly. This prevents sudden budget shocks and keeps your monthly financial structure stable.

Planning ahead protects your student's monthly budget from disruption and reduces the need for emergency borrowing.

Conclusion

Building and maintaining a student's monthly budget is one of the smartest financial habits you can develop early in life. By understanding your income, planning your expenses, and reviewing your spending regularly, you move from reacting to money problems to managing them with confidence.

Budgeting is not about cutting out everything you enjoy. It is about making intentional choices, prioritising essentials, and creating space for both savings and flexibility. When you plan ahead and adjust consistently, financial stress reduces significantly.

And when unexpected expenses arise despite careful planning, having access to responsible options like Pocketly ensures that short-term cash gaps do not disrupt your academic or personal goals.

Ready to take control of your student finances? Download the Pocketly app today on [Android] or [iOS] and experience smarter, stress-free spending management.

FAQs

1. How much should a student's monthly budget be in India?

Most students spend between ₹11,000 and ₹30,000 per month, depending on their city, accommodation, and lifestyle. Metro cities typically cost more due to higher rent and food prices. The right budget is based on your actual expenses, not just averages.

2. How can I manage a budget with irregular income?

Use your minimum guaranteed monthly income as the base for planning. Treat any extra earnings as surplus and allocate them toward savings or upcoming expenses to avoid shortfalls during low-income months.

3. How much should a student ideally save each month?

Saving 5 to 10 per cent of your income is a practical starting point. Even setting aside ₹500 to ₹1,000 consistently can build a helpful emergency cushion over time. The focus should be on regular saving habits rather than large amounts.

4. What are common budgeting mistakes students make?

Students often underestimate small daily expenses, forget irregular costs like exam fees or travel, overspend early in the month, and fail to review their budget regularly. Weekly tracking can help prevent most of these issues.

5. What should I do if my monthly budget falls short?

First, calculate the exact shortfall, then reduce non-essential spending immediately. If needed, use your emergency savings. For urgent gaps, responsible short-term financial solutions like Pocketly can help bridge the difference without disrupting your long-term financial stability.

6. Is taking a short-term loan safe for students?

Short-term loans can be safe if used responsibly. Borrow only what you need, understand the interest and fees clearly, and plan repayment within your next budget cycle. The objective should be to manage a temporary gap, not create ongoing dependency.