You swipe your credit card for a new phone, laptop, or appliance, thinking you will manage the payment later. When the statement arrives, the full amount feels heavier than expected. Paying it all at once can strain your monthly budget, but ignoring it is not an option either.

This is where credit card EMI steps in. It promises smaller, manageable monthly payments instead of one large bill. Sounds simple. But many people do not fully understand how EMI actually works, how interest is calculated, or how it affects their credit limit and overall repayment amount.

Without clarity, what feels convenient today can quietly become expensive tomorrow.

In this blog, you will learn exactly how EMI works on a credit card, what charges are involved, and when choosing EMI makes financial sense, so you can make smarter borrowing decisions.

TL;DR

- Credit card EMI helps you split big purchases into fixed monthly payments instead of paying the full amount upfront.

- The real cost depends on interest rate, tenure, processing fees, and how “no cost EMI” is structured.

- The total purchase amount reduces your available credit limit until the EMI is fully repaid.

- Late or missed EMIs can increase your repayment burden and damage your credit score.

- EMI works best for essential, high-value purchases when it improves cash flow without creating long-term debt pressure

What Is Credit Card EMI?

Credit card EMI is a facility that allows you to convert a large credit card purchase into smaller, fixed monthly instalments instead of paying the full amount in one go.

When you normally swipe your card, the entire amount appears in your next billing statement. If you cannot pay it fully, interest starts accumulating on the outstanding balance. EMI gives you a structured alternative.

Here’s how it differs from regular credit card billing:

- The total purchase amount is divided into fixed monthly payments

- You choose a repayment tenure, usually 3, 6, 9, 12 months or more

- Interest may be charged depending on the offer

- Some transactions qualify for no-cost EMI

- A processing fee may apply in certain cases

Instead of revolving high-interest debt month after month, EMI creates a predictable repayment schedule. However, understanding the total repayment amount is crucial before opting for it.

How Does EMI Work on a Credit Card?

Credit card EMI is not just about splitting a bill into smaller parts. It is essentially a short-term loan attached to your credit card. Understanding the mechanics helps you decide whether it is a convenient or costly comfort.

Here is what actually happens behind the scenes.

Here is what actually happens behind the scenes.

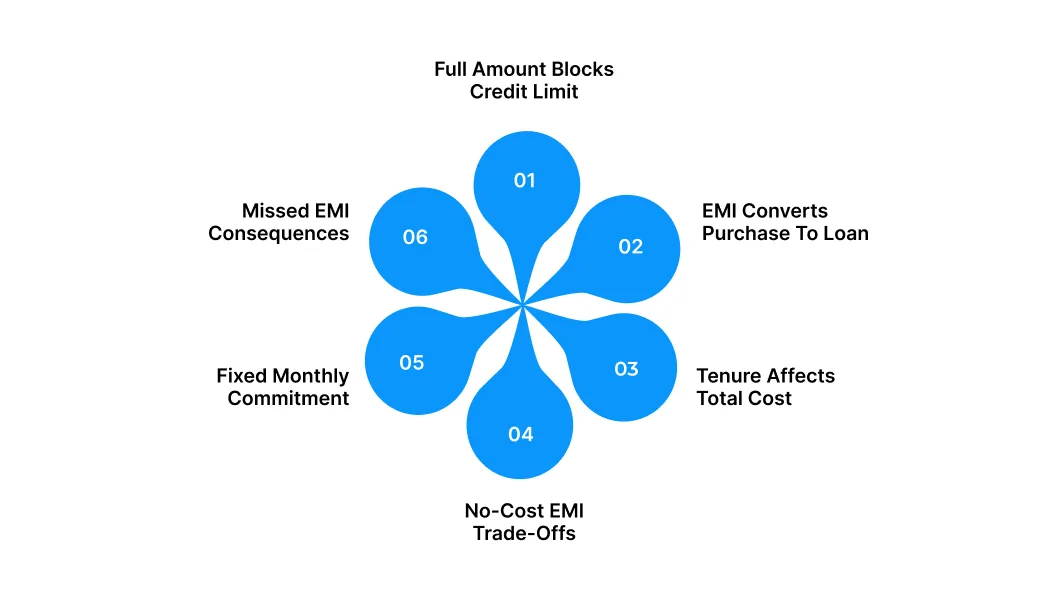

1. The Full Purchase Amount Is Blocked From Your Credit Limit

When you convert a transaction into EMI, the bank immediately blocks the entire purchase amount from your available credit limit. Even though you will repay in instalments, the bank treats it as fully utilised credit until you gradually repay the principal.

This means your spending power reduces instantly. As you pay each EMI, only the principal portion restores your limit, not the interest.

For example, if your credit limit is ₹80,000 and you convert a ₹30,000 purchase into EMI, your available limit drops to ₹50,000. If your first EMI includes ₹2,500 principal and ₹600 interest, only ₹2,500 gets restored to your limit.

2. EMI Converts Your Purchase Into a Fixed Loan

Unlike regular credit card billing, where you can avoid interest by paying the full amount before the due date, EMI creates a structured repayment schedule with fixed monthly instalments.

Each EMI includes two components:

- Principal repayment

- Interest charged by the bank

The interest is usually quoted monthly, but the real cost becomes clearer when annualised.

For example, a 1.5% monthly interest rate may look small, but over a year it becomes 18% plus GST on interest. On a ₹40,000 purchase over 12 months, this can add several thousand rupees to your total repayment.

3. Tenure Directly Impacts the Total Amount You Repay

The longer the tenure, the smaller your monthly EMI, but the higher the total interest paid. Shorter tenures increase monthly payments but reduce overall borrowing cost.

Choosing tenure should depend on affordability, not just convenience.

For example, a ₹25,000 purchase over 3 months may cost you significantly less in interest compared to spreading it over 12 months. While the longer option feels lighter each month, you end up paying more in total.

4. No-Cost EMI May Still Have Trade-Off

No-cost EMI usually means the interest is absorbed through a discount funded by the merchant. While you may not see a separate interest charge, you might lose other benefits like upfront cashback or additional discounts.

It is important to compare the final payable amount in both scenarios.

For example, if a product costs ₹20,000 with a ₹2,000 instant discount for full payment but only a ₹500 discount under no-cost EMI, you are indirectly paying more by choosing EMI.

5. EMI Becomes a Fixed Monthly Commitment

Every EMI adds to your list of fixed monthly expenses. Multiple EMIs can reduce flexibility in your budget and increase financial pressure if income fluctuates.

Banks also report EMI payments to credit bureaus, so timely repayment is essential to protect your credit score.

For example, if you already have two EMIs running and add a third for a new gadget, your monthly commitments may increase beyond what feels comfortable, leaving little room for emergencies.

6. Missing an EMI Has Financial Consequences

If you miss an EMI, the bank may charge late payment fees and additional interest and report the delay to credit bureaus. In some cases, the EMI facility may be cancelled, and the remaining amount could become immediately payable.

For example, delaying one EMI by even a few days can attract penalty charges and reflect negatively on your credit history, making future borrowing more expensive.

Also Read: 10 Essential Financial Habits For Success

Types of Credit Card EMI in India

Not all EMIs work the same way. The structure, cost, and flexibility can vary depending on the bank, merchant partnership, and offer type. Understanding the differences helps you choose the right option for your situation.

1. No Cost EMI

No-cost EMI is marketed as an option where you pay no additional interest on your purchase. In most cases, the interest component is adjusted through a discount provided by the merchant, so the total payable amount appears similar to the product’s original price.

However, there are often trade-offs. You may lose upfront discounts, cashback offers, or reward points. Processing fees and GST may still apply.

For example, if a phone costs ₹30,000 and you choose no-cost EMI for 6 months, the total repayment may remain ₹30,000. But if paying upfront would have given you ₹2,000 cashback, you are indirectly paying more by choosing EMI.

2. Standard EMI With Interest

In a standard EMI, the bank charges interest on the converted amount. The rate is usually quoted monthly, and the total interest depends on the tenure you select.

This option provides flexibility but increases the total repayment amount. Some banks also charge a processing fee at the time of conversion.

For example, if you convert ₹40,000 into a 12-month EMI at 1.5% per month, your total repayment could exceed ₹44,000 once interest and GST are included.

3. Post-Purchase EMI Conversion

Many banks allow you to convert a transaction into EMI after it appears in your statement. This is useful if you initially planned to pay in full but later decide to spread the cost.

The bank may offer pre-approved EMI conversion for eligible transactions through its app or SMS notification. Interest rates and tenure options are usually similar to standard EMI.

For example, if you purchase a laptop and later realise the bill is straining your monthly budget, you can convert that specific transaction into EMI instead of revolving the full outstanding amount at a much higher credit card interest rate.

When Should You Choose EMI on a Credit Card?

Credit card EMI is not inherently good or bad. Its value depends on why you are using it and whether it aligns with your financial situation. The key is to distinguish between planned borrowing and convenience-driven spending.

1. When the Purchase Is Necessary, Not Impulsive

EMI makes more sense for essential or high-value purchases that serve a long-term purpose. Spreading the cost of something important can protect your monthly cash flow without disrupting other priorities.

For example, converting a ₹35,000 laptop needed for work into a 6-month EMI may be reasonable if it supports your income. Converting a last-minute luxury purchase simply because EMI feels affordable is a different situation.

2. When You Can Comfortably Manage the Monthly EMI

Before choosing EMI, check whether the instalment fits within your budget without reducing savings or essentials. EMI should not push you into financial stress.

A practical rule is to ensure your total EMIs do not exceed a manageable portion of your monthly income. If adding one more EMI makes your budget tight, reconsider the tenure or delay the purchase.

For example, if your monthly income is ₹50,000 and fixed commitments already consume ₹30,000, adding multiple EMIs can reduce your flexibility significantly.

3. When the Interest Cost Is Lower Than Alternatives

Credit card revolving interest rates are often extremely high. If you cannot pay the full outstanding amount, converting to EMI can be cheaper than paying only the minimum due and carrying forward the balance.

For example, if your credit card charges over 30% annually on unpaid balances, converting a ₹20,000 purchase into a structured EMI at a lower rate can reduce total interest.

4. When You Understand the Total Repayment Amount

Always calculate the final payable amount before confirming EMI. Convenience should not replace clarity.

Check:

- Total interest payable

- Processing fees

- GST on charges

- Foreclosure terms

For example, if a 9-month EMI increases your total repayment by ₹3,500, ask whether the flexibility justifies the additional cost.

5. When It Protects Your Emergency Savings

If paying upfront would wipe out your emergency fund, EMI may help preserve liquidity. Keeping cash available for unexpected situations can sometimes be more valuable than avoiding small interest costs.

For instance, using EMI for a medical expense instead of draining your entire savings may give you better financial stability in the short term.

Also Read: 10 Smart Spending Tips For Financial Wellness

Smart Tips to Use Credit Card EMI Responsibly

Using EMI on your credit card can be convenient, but without discipline, it can quietly increase your financial burden. Follow these practical guidelines to ensure EMIs support your budget instead of straining it.

Using EMI on your credit card can be convenient, but without discipline, it can quietly increase your financial burden. Follow these practical guidelines to ensure EMIs support your budget instead of straining it.

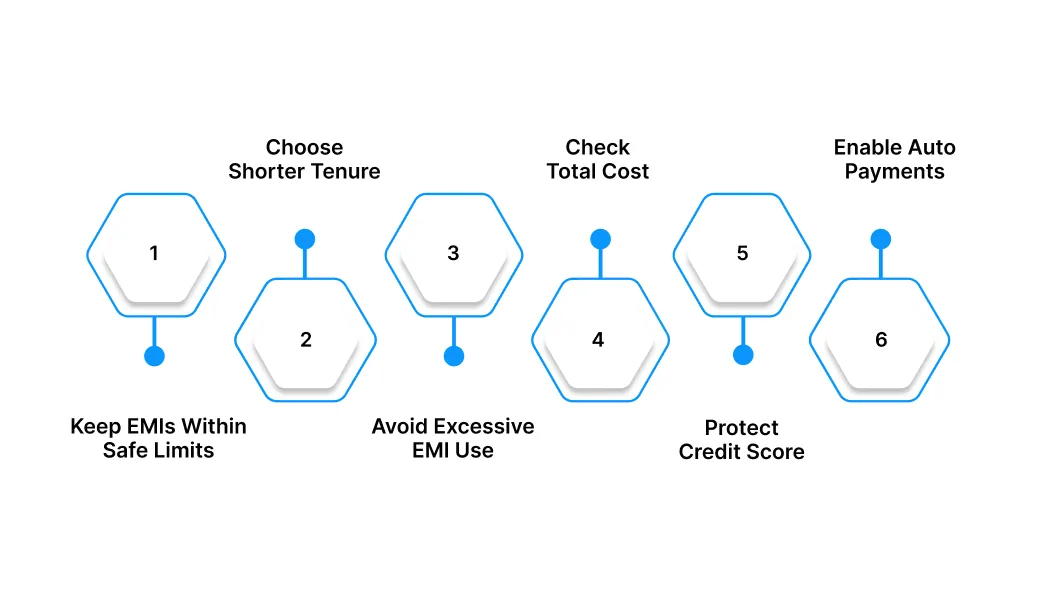

1. Keep Your Total EMIs Within a Safe Limit

EMIs should support your budget, not dominate it. As a general rule, your total monthly EMIs across all loans and credit cards should not exceed 30 to 40% of your income. When fixed commitments rise too high, even a small emergency can create financial pressure.

Before converting a purchase into EMI, calculate your existing obligations and see how the new instalment fits into your monthly cash flow. If it makes your finances feel tight on paper, it will likely feel tighter in real life.

For example, if your monthly income is ₹50,000 and you already pay ₹12,000 in EMIs, adding another ₹8,000 instalment pushes you close to the risk zone. A smaller purchase or shorter tenure may be a safer choice.

2. Choose the Shortest Tenure You Can Comfortably Afford

Longer tenures reduce your monthly EMI but increase the total interest paid over time. While a smaller EMI may feel easier, the overall cost of the purchase becomes significantly higher.

If your budget allows, choose the shortest tenure that keeps your monthly finances stable. This helps you clear the debt faster and reduces the psychological burden of long-running instalments.

For instance, selecting a 6-month tenure instead of 12 months may increase your EMI slightly, but it can save you a noticeable amount in total interest and free up your credit limit sooner.

3. Avoid Converting Every Purchase Into EMI

Turning every large transaction into EMI can create a false sense of affordability. Individually, each instalment may look manageable, but collectively, they can strain your monthly income.

Use EMI selectively for essential or high-value purchases rather than lifestyle upgrades that can wait. Discipline in choosing what qualifies for EMI keeps your financial commitments controlled.

For example, converting a necessary laptop purchase into EMI may be reasonable, but splitting fashion or dining expenses into instalments can quickly add unnecessary long-term liabilities.

4. Focus on Total Cost, Not Just the EMI Amount

A low EMI can be misleading. Always check the total repayment amount, including interest and processing fees. Comparing the final amount payable with the original purchase price gives you a clearer picture of the real cost.

If the difference is too high, consider paying upfront or exploring alternative options.

For instance, a ₹40,000 purchase may look easy at ₹3,800 per month, but if the total repayment reaches ₹45,000 after interest and fees, you are effectively paying ₹5,000 extra for convenience.

5. Protect Your Credit Score

Credit card EMIs reduce your available credit limit and increase your credit utilisation ratio. High utilisation can negatively impact your credit score, especially if you are already using a large portion of your limit.

Maintain a healthy buffer by keeping overall usage below 30% of your credit limit whenever possible. Timely EMI payments are equally important to avoid penalties and negative reporting.

For example, if your total credit limit is ₹1,00,000 and an EMI blocks ₹60,000 of it, your available limit drops sharply, which may affect both your spending flexibility and your credit profile.

6. Set Auto Payments to Avoid Missed EMIs

Missing even one EMI can lead to late payment charges, higher interest, and a dip in your credit score. Setting up auto debit or reminders ensures that instalments are paid on time without manual effort.

Consistency is key. A clean repayment history strengthens your creditworthiness and keeps borrowing costs lower in the future.

For instance, a single missed EMI can trigger penalty fees and additional interest that make the purchase more expensive than initially planned.

Using credit card EMI responsibly is about awareness, planning, and self-control. When used thoughtfully, it can improve cash flow. When used casually, it can quietly weaken your financial stability.

How Pocketly Complements Credit Card EMI Usage

Credit card EMIs are one way to manage large purchases, but they are not always the most flexible option. They reduce your available credit limit, follow fixed billing cycles, and may carry higher effective costs depending on tenure and fees.

Pocketly operates in the short-term digital credit space, helping users manage temporary liquidity gaps without overextending their credit cards.

As a regulated digital lending platform, Pocketly supports users by:

- Offering small ticket loans from ₹1,000 to ₹25,000, ideal for covering short-term cash gaps instead of converting large purchases into long EMIs.

- Providing fast, fully digital access with quick KYC verification and minimal paperwork compared to traditional bank processes.

- Maintaining transparent pricing, with interest starting at 2% per month and clearly defined processing fees between 1% and 8%, depending on profile and loan amount.

- Avoiding credit limit blockage, allowing your credit card to remain available for other planned or emergency expenses.

- Helping users manage urgent payments such as bills, medical costs, travel needs, or temporary shortfalls without restructuring their entire monthly budget.

By focusing on speed, clarity, and responsible borrowing, Pocketly complements traditional credit card EMIs. It works best as a short-term financial bridge rather than a long-term debt commitment, giving users flexibility without permanently stretching their credit profile.

Conclusion

Credit card EMI lets you convert large purchases into fixed monthly payments instead of paying the full amount up front. It can improve short-term cash flow, but it also comes with interest, fees, and an impact on your credit limit.

Before choosing EMI, check the interest rate, processing charges, tenure, and total repayment amount. Ensure the EMI fits within your monthly budget and avoid stacking multiple instalments.

If an unexpected expense disrupts your budget, short-term options like Pocketly can provide quick support without long-term complications.

Download the Pocketly app today on [Android] or [iOS] to access funds when you need them and stay financially prepared.

FAQs

1. Does credit card EMI affect my credit score?

Yes. While converting a purchase into EMI does not reduce your score by itself, missing or delaying payments can negatively impact it. Consistent, on-time payments can help build a stronger credit history.

2. Is no-cost EMI really free?

Not completely. The interest is often adjusted as a merchant discount, but you may still pay processing fees or lose other offers. Always check the total repayment amount before choosing it.

3. Is interest charged monthly or annually?

Banks usually display an annual interest rate, but EMI is calculated monthly. Reviewing the annual percentage rate helps you understand the true borrowing cost.

4. Can I convert any transaction into EMI?

No. Banks set minimum transaction limits, and eligibility depends on the card, merchant, and your credit profile. You can check available options through your bank’s app or net banking.

5. What happens if I miss an EMI?

You may be charged a late fee and additional interest, and your credit score can be affected. Delays can also increase your overall repayment amount.