Debt usually feels like a financial red flag. The instinct is simple: avoid it at all costs. But here’s the catch: not all debt is destructive. When misunderstood, it can either limit your growth or quietly drain your future income.

Many young earners in India struggle with this dilemma. Should you take an education loan? Is a business loan smart? Is every EMI a burden? Without clarity, people either reject opportunities that could multiply their income or take on loans that trap them in repayment cycles.

The real issue isn’t debt itself. It’s the type of debt and the intention behind it.

Used strategically, the right kind of borrowing can help you build assets, increase earning potential, and accelerate financial progress. In this blog, we’ll break down what good debt actually means, how it differs from harmful borrowing, and how to use debt as a tool, not a trap, in 2026.

TL;DR

- Not all debt is harmful. Good debt builds income, assets, or long-term financial stability, while bad debt funds short-term consumption.

- The difference lies in purpose and return. If borrowing increases earning potential or net worth beyond its cost, it can be strategic.

- Education loans, home loans, business capital, and skill development funding are common examples of debt that can create financial upside.

- Debt turns risky when it strains cash flow, exceeds repayment capacity, or depends on uncertain future income.

- Smart borrowing requires evaluating total cost, ROI potential, EMI affordability, and worst-case scenarios before committing.

What Is Good Debt?

Good debt is borrowing that helps you build long-term value. Instead of draining your finances, it supports income growth, asset creation, or financial stability.

The difference lies in purpose and outcome.

If a loan helps you acquire something that appreciates in value or increases your earning capacity, it can be considered good debt. The focus is not just on borrowing, but on return on investment.

For example, taking a loan to buy a car for luxury use may add a liability. But taking a loan for a professional course that increases your salary can create future financial upside.

Good debt typically has the following characteristics:

- It funds assets or skills that generate returns

- It has manageable interest rates

- It fits within your repayment capacity

- It aligns with long-term financial goals

Understanding this distinction is essential before evaluating different types of good debt.

What Is Bad Debt?

Bad debt is borrowing that creates financial strain instead of long-term value. Rather than helping you grow income or build assets, it usually supports short-term consumption with no meaningful return.

The key difference lies in impact.

If a loan is used for something that quickly loses value or offers no financial return, it is generally considered bad debt. Over time, interest payments increase the total cost, making the expense heavier than it initially appeared.

For example, using credit to fund frequent shopping, vacations, or high-end gadgets may provide temporary satisfaction, but these purchases do not contribute to long-term financial growth.

Bad debt typically has the following characteristics:

- It funds lifestyle spending or depreciating assets

- It carries high interest rates

- It does not generate income or long-term returns

- It stretches your repayment capacity

- It delays savings and wealth building

Recognising bad debt early helps you avoid financial pressure and focus on borrowing that actually supports your long-term goals.

Good Debt vs Bad Debt: Key Differences

Understanding the difference between good debt and bad debt is essential for making smarter financial decisions. Not all borrowing is harmful; some forms of debt can actually help you grow wealth or improve your financial stability.

Here’s how you differentiate it:

| Factor | Good Debt | Bad Debt |

| Purpose of borrowing | Used to acquire assets or opportunities that can grow in value or increase income | Used for consumption, lifestyle spending, or impulse purchases |

| Impact on net worth | Can increase net worth over time by building assets or earning potential | Reduces net worth due to depreciation and high interest costs |

| Interest rates | Usually lower, especially for secured loans like home or education loans | Often higher, such as credit card debt or unsecured consumer loans |

| Return on investment potential | Has the potential to generate returns that exceed borrowing costs | Does not generate financial returns and adds repayment burden |

| Long-term financial effect | Can support wealth creation and financial stability when managed well | Can create financial stress and limit future borrowing capacity |

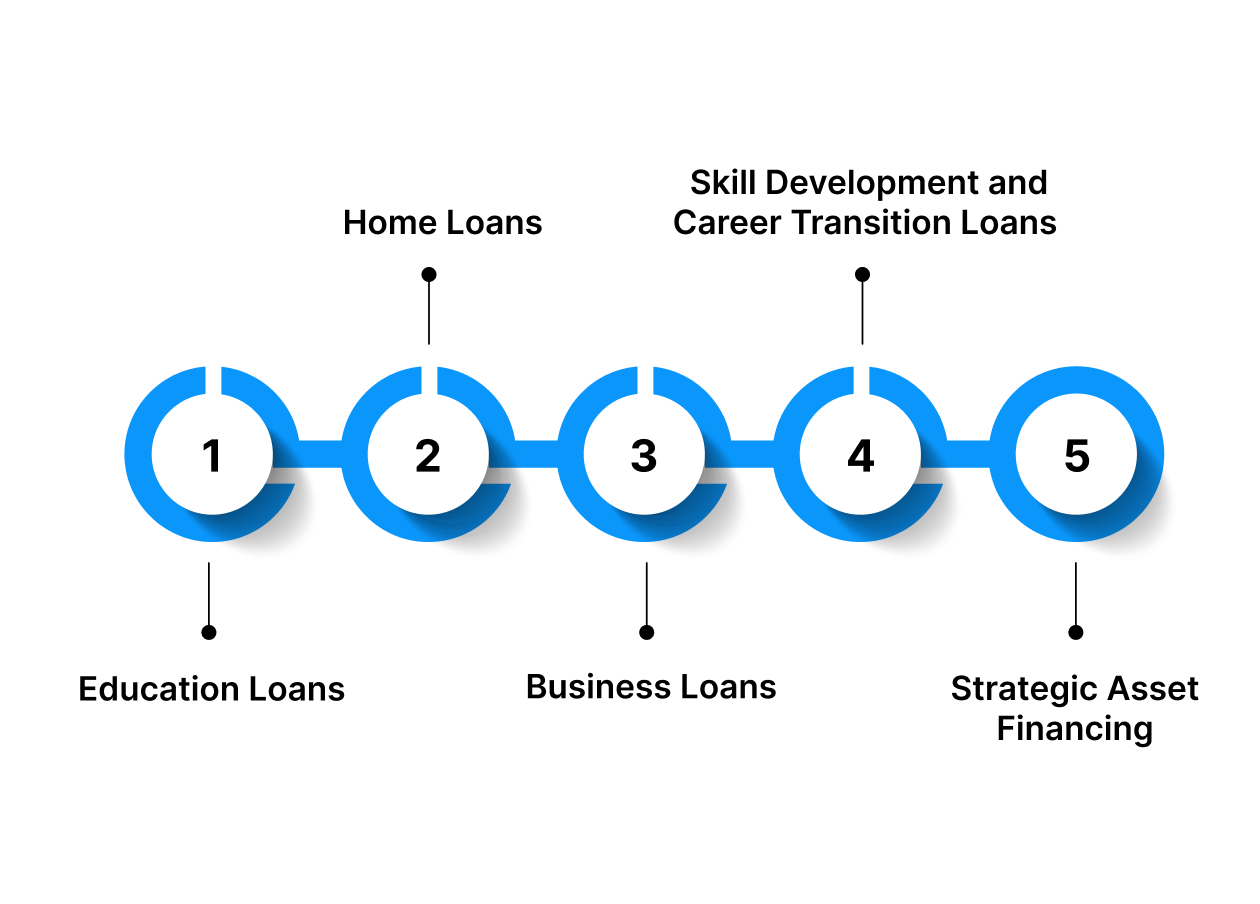

Types of Good Debt and How They Create Financial Value

Good debt is not defined by the loan itself, but by what it enables. The same financial product can either strengthen or weaken your finances depending on how it is used. Below are the most common categories of good debt and the logic behind why they work.

Good debt is not defined by the loan itself, but by what it enables. The same financial product can either strengthen or weaken your finances depending on how it is used. Below are the most common categories of good debt and the logic behind why they work.

1. Education Loans

An education loan finances degrees, certifications, or skill development programs that improve employability and income potential. When structured properly, this type of borrowing is an investment in future cash flow rather than present consumption. Education increases earning capacity. If a course increases your annual income significantly over time, the return compounds far beyond the interest paid.

Financial Impact

- Higher salary

- Faster career progression

- Better job security

- Long-term income growth

Example: A marketing professional earning ₹4 lakh per year takes a ₹3 lakh loan for a data analytics certification. Within a year of completion, she transitions into a higher-paying role, earning ₹8 lakh annually. The income increase offsets the loan cost within a short period and continues to generate higher returns for years.

2. Home Loans

A home loan allows you to acquire property, which can appreciate over time while simultaneously building equity.

Unlike rent, which provides no ownership, home loan EMIs gradually convert into asset ownership. Property can appreciate in value, hedge against inflation, and offer tax advantages. Over time, equity builds as the principal reduces.

Financial Impact

- Asset appreciation potential

- Equity accumulation

- Stability and inflation protection

- Tax benefits under applicable laws

Example: An individual purchases a ₹50 lakh apartment with a home loan. Over ten years, the property value grows to ₹75 lakh while a significant portion of the principal is repaid. Instead of spending on rent with no ownership, they now hold an appreciating asset.

3. Business Loans

Business loans provide capital for expansion, operations, equipment, marketing, or working capital. When the borrowed funds generate returns greater than the cost of borrowing, the loan fuels growth rather than risk. Utilisation accelerates scale. Instead of waiting years to accumulate capital, businesses can grow faster and capture opportunities early.

Financial Impact

- Increased revenue capacity

- Market expansion

- Improved operational efficiency

- Higher profit margins

Example: A small bakery takes a ₹5 lakh business loan to purchase additional ovens and hire staff. Production capacity doubles, monthly revenue increases by ₹1.5 lakh, and profits comfortably cover loan repayments while expanding the business footprint.

4. Skill Development and Career Transition Loans

Short-term professional certifications or technical skill programs can significantly shift earning potential. In evolving industries, continuous skill upgrades often determine salary growth. Targeted upskilling can increase income within months, not years.

Financial Impact

- Higher negotiation power

- Access to better roles

- Greater employability

- Reduced career stagnation risk

Example: An IT support executive earning ₹3.5 lakh annually takes a short-term loan for a cloud computing certification. After completion, he secures a role in cloud infrastructure with a ₹7 lakh package, doubling his income within a year.

5. Strategic Asset Financing

Borrowing to acquire income-generating assets can be productive when those assets directly increase earning capacity. The asset generates recurring income that offsets repayment costs.

Financial Impact

- Increased productivity

- Higher income streams

- Business scalability

- Long-term asset ownership

Example: A freelance videographer takes a ₹2 lakh equipment loan to upgrade to professional-grade cameras. With higher quality output, she attracts premium clients and increases project rates, recovering the loan cost within a year.

How to Identify Good Debt Before You Borrow

Good debt is not defined by the type of loan. It is defined by the outcome it creates. A home loan can be good debt or bad debt, depending on affordability. An education loan can create wealth or become a burden depending on career outcomes.

Before borrowing, evaluate the debt using a structured financial filter instead of emotion or urgency.

1. Does It Create Economic Value or Just Emotional Satisfaction

The first filter is value creation.

Good debt should improve your net worth, income potential, or long-term financial position. If it only delivers temporary satisfaction without improving your financial standing, it is not strategic debt.

There are three measurable ways debt can create value

- Income expansion

- Asset appreciation

- Cost efficiency

If none of these applies, the loan is consumption-driven.

Example: Taking a ₹4 lakh loan to pursue a specialised certification that increases your annual salary from ₹6 lakh to ₹9 lakh creates direct income acceleration. The loan has a clear return path.

Taking a ₹4 lakh loan for a luxury destination wedding, while emotionally meaningful, does not generate economic return. It increases liability without strengthening future income or assets.

Value-based borrowing builds leverage. Emotion-based borrowing builds pressure.

2. Is the Expected Return Higher Than the True Cost of Borrowing

Most borrowers make one critical mistake. They compare only the interest rate with a vague idea of “future benefit.”

That is incomplete.

To determine whether debt is good, you must calculate the real cost of capital and compare it against a realistic, measurable return, not an optimistic assumption.

Interest rate alone does not define cost. The true cost includes

- Interest

- Processing fees

- Documentation charges

- Insurance premiums, if bundled

- Opportunity cost of locked income

To qualify as good debt, the financial return must exceed the total borrowing cost.

This concept is called positive financial spread. If returns exceed borrowing cost, you gain flexibility. If borrowing costs exceed returns, you lose wealth over time.

Example: If a small business takes a loan at an effective annual cost of 16 per cent and uses it to expand inventory that increases profit margins by 32 per cent annually, the debt is productive.

However, if projected returns are uncertain or fluctuate below 16 per cent, the business carries risk without guaranteed upside.

Debt should create financial multiplication, not financial compression.

3. Does It Strengthen or Strain Your Cash Flow

Cash flow stability is often more important than asset growth. An asset may appreciate over time, but if EMI payments reduce your monthly flexibility and increase stress, the debt may not be suitable for your current financial stage.

Evaluate

- Your debt-to-income ratio

- Income stability

- Existing fixed obligations

- Emergency savings coverage

Example: A salaried professional earning ₹90,000 per month with stable employment and six months of savings can responsibly manage a calculated home loan EMI of ₹25,000.

A freelancer with fluctuating income between ₹50,000 and ₹1,00,000 per month may struggle with the same EMI because variability increases risk exposure.

Good debt improves your future without destabilising your present.

4. Does It Accelerate Long-Term Financial Goals

Debt should compress time. That is its real strategic function. When used correctly, debt allows you to achieve in five years what may otherwise take fifteen. But if it does not meaningfully accelerate your financial growth, it is not a tool; it is simply an obligation.

To evaluate this, ask three deeper questions:

- Does this loan create a compounding advantage?

- Does it improve my earning curve?

- Does it increase my net worth over time?

Compounding advantage means the benefit of the loan continues to multiply even after the loan is repaid.

Example: Borrowing to invest in skill development that increases earning potential aligns with long-term wealth growth.

Borrowing for high-end gadgets or lifestyle upgrades while neglecting emergency savings contradicts financial stability goals.

Good debt moves you closer to your financial vision. Bad debt pulls you sideways.

5. Can It Survive a Risk Scenario

Every loan introduces structural risk. The real question is not whether you can repay under ideal conditions. The question is whether you can repay under imperfect conditions. A strong financial structure has shock absorption capacity.

Ask yourself these questions:

- What happens if income drops by 20 to 30 per cent?

- What if business revenue slows for three months?

- Can you still service EMIs comfortably?

If repayment becomes impossible under mild disruption, the debt carries structural risk.

Example: If your EMI remains manageable even at 70 per cent of your current income, the debt has resilience.

If one unexpected expense forces you to borrow again to repay existing EMIs, the structure is fragile.

Resilient debt structures are strategic. Fragile ones compound risk.

6. Is There a Clear Exit or Repayment Strategy

Borrowing without a repayment roadmap turns debt into a gamble. A strong repayment strategy answers four things clearly:

- What is the exact tenure

- What is the total interest outflow

- Can I prepay without heavy penalties

- What is my fallback plan if income slows

Most people only calculate EMI affordability. That is an incomplete analysis. You must calculate the total cost of capital over the full tenure and understand how interest compounds.

For example: A ₹5 lakh loan at 15 per cent interest over five years may seem manageable at a ₹12,000 EMI. But over time, you could end up paying more than ₹2 lakh in interest.

Now compare that to prepaying aggressively in three years. The interest outflow reduces significantly. That difference is real money retained.

Flexibility is equally important. Loans that allow part prepayment without penalty give you control. Rigid structures trap you in long commitments even when your income increases. Strategic borrowing requires clarity on both entry and exit.

Also Read: Should You Save for an Emergency Fund or Pay Off Debt?

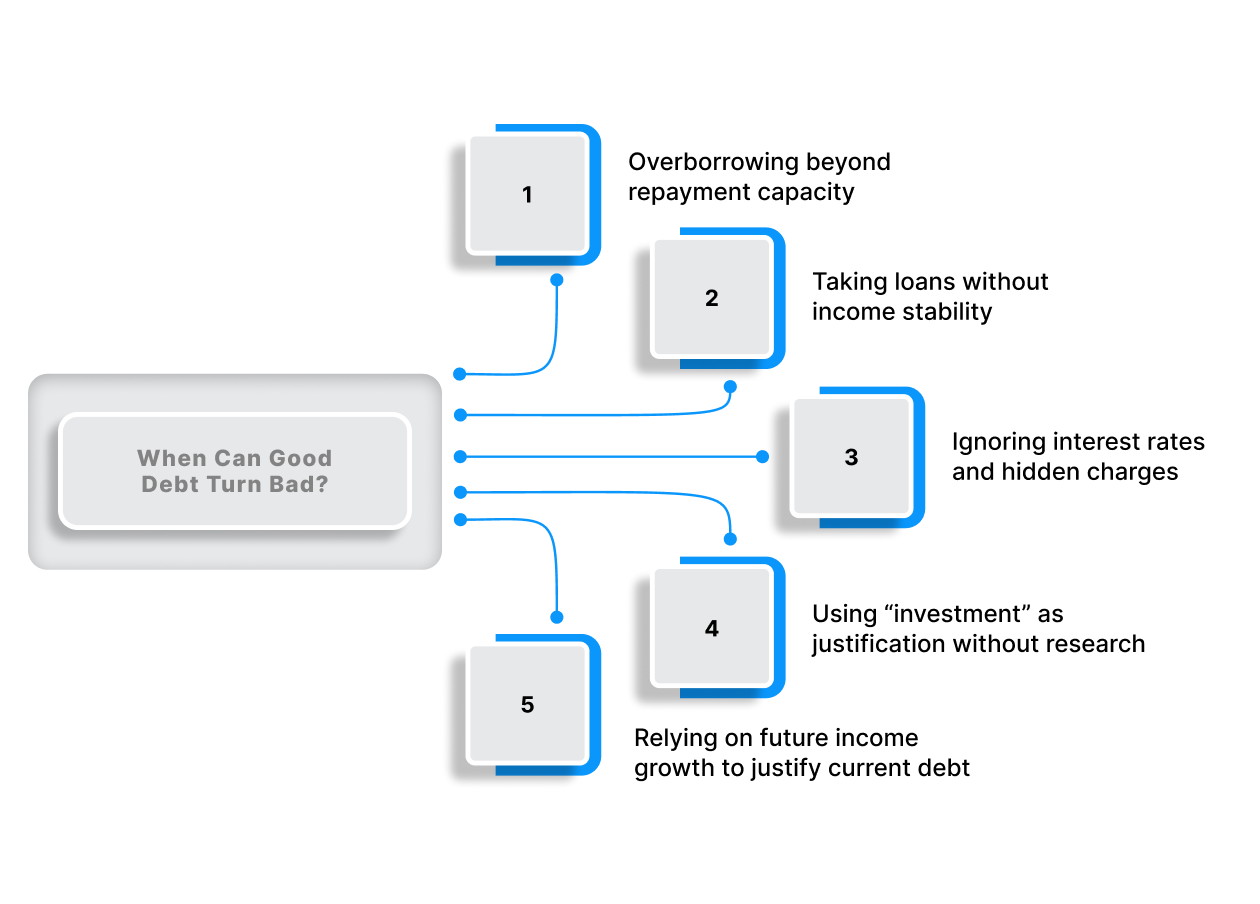

When Can Good Debt Turn Bad?

Good debt turns bad when risk factors outweigh your repayment strength. Below are the key risks and the logic to mitigate them before they damage your finances.

Good debt turns bad when risk factors outweigh your repayment strength. Below are the key risks and the logic to mitigate them before they damage your finances.

1. Overborrowing beyond repayment capacity

Risk: Taking a loan that stretches your EMI beyond a comfortable percentage of your monthly income can strain cash flow, reduce savings, and increase stress. Even productive loans can become burdensome if they dominate your budget.

Mitigation: Keep total EMIs within a safe threshold of your net income. Maintain an emergency fund that can cover at least 3 to 6 months of repayments.

2. Taking loans without income stability

Risk: Borrowing without a predictable income source increases the chance of missed payments. Irregular cash flow can quickly convert manageable debt into default risk.

Mitigation: Secure stable income or reliable revenue streams before committing to repayment obligations. If income is variable, plan conservatively and assume lower earnings in projections.

3. Ignoring interest rates and hidden charges

Risk: Focusing only on EMI size while ignoring the total cost of borrowing can inflate your repayment burden. High interest rates, processing fees, or penalties increase long-term liability.

Mitigation: Always calculate the total repayment amount, annual percentage rate, and additional fees before signing. Compare multiple lenders to ensure transparent pricing.

4. Using “investment” as justification without research

Risk: Labelling a loan as an “investment” does not guarantee returns. If the expected income boost or asset appreciation does not materialise, repayment pressure remains.

Mitigation: Conduct realistic research, evaluate worst-case scenarios, and assess return timelines before borrowing for growth opportunities.

5. Relying on future income growth to justify current debt

Risk: Borrowing based on expected promotions, business expansion, or market growth can be risky if those projections are delayed or fail to happen. This creates repayment pressure without the anticipated income boost.

Mitigation: Base borrowing decisions on current, verified income rather than optimistic projections. Treat future growth as a bonus, not a repayment strategy.

Also Read: Can Paying Bills Help Build a Credit Score?

Smart Borrowing Framework for Young Professionals in India

For young professionals in India, borrowing should support growth, not create pressure. Use this practical framework to evaluate debt decisions before committing.

1. Keep Your EMI Within a Safe Limit

Your total EMIs should ideally stay within 30 to 40 per cent of your monthly take-home income. This ensures that loan repayments do not interfere with essential expenses, savings, or lifestyle flexibility. A balanced EMI ratio protects you from financial stress and reduces the risk of missing payments during unexpected situations.

For example, if your monthly income is ₹40,000, your total EMIs should not exceed ₹12,000–₹16,000. This leaves enough room for rent, groceries, savings, and personal spending without stretching your finances too thin.

2. Build an Emergency Fund Before Taking Large Loans

Before committing to a significant loan, create an emergency fund that covers at least three to six months of essential expenses. This financial cushion ensures that temporary income disruptions do not immediately turn into repayment pressure.

For instance, if your monthly essential expenses are ₹25,000, aim to build a reserve of ₹75,000–₹1.5 lakh. This buffer allows you to continue servicing your loan even if you switch jobs or face a short-term setback.

3. Compare Lenders Beyond Just Interest Rates

Interest rate is important, but it is not the only factor that determines loan affordability. Processing fees, foreclosure charges, late payment penalties, and hidden terms can significantly increase the total cost of borrowing. Comparing lenders thoroughly helps you choose a transparent and cost-effective option.

For example, one lender may offer a slightly lower interest rate but charge a high processing fee, while another may have a marginally higher rate with zero foreclosure charges. Evaluating the total cost gives you a clearer picture.

4. Borrow With a Clear Financial Purpose

Loans should support long-term growth, not temporary lifestyle upgrades. Borrowing for education, skill development, or asset creation typically strengthens your financial future. On the other hand, taking loans for social pressure or lifestyle comparison can create unnecessary financial strain.

For example, financing a professional certification that increases your earning potential is strategic borrowing. Taking a personal loan for an expensive vacation because peers are travelling may not deliver long-term value.

5. Understand the Total Repayment Obligation

Always calculate how much you will repay over the entire tenure, not just the monthly EMI. Understanding the total repayment amount helps you evaluate whether the loan is worth the cost and prevents unpleasant surprises later.

For instance, a ₹2 lakh loan at a certain interest rate over three years may result in a total repayment of ₹2.6 lakh or more. Knowing this upfront allows you to make a more informed decision.

Smart borrowing is not about avoiding debt entirely. It is about using it strategically, responsibly, and with full clarity.

Short-Term Cash Gap? Keep It Controlled with Pocketly

Even with careful planning, some expenses refuse to wait. A sudden medical bill, urgent travel, or an unexpected repair can stretch your monthly budget beyond its limit. In such moments, the goal is not just access to money, but access to money in a way that stays manageable. Pocketly is designed to help you handle short-term gaps without creating long-term financial strain.

Here’s how it supports smarter borrowing:

- Borrow within limits: Loan amounts range from ₹1,000 to ₹25,000, allowing you to take only what your situation requires. Smaller, need-based borrowing reduces repayment pressure and helps you stay disciplined.

- No collateral complications: You don’t need to pledge assets or arrange a guarantor. The process is fully unsecured, which makes it accessible for students and young professionals building their financial base.

- Fast, app-based approval: A streamlined KYC process enables quicker eligibility checks. There’s no branch visit, no lengthy documentation, and no waiting in queues.

- Direct transfer to your account: Once approved, funds are credited straight to your bank account, making it practical for urgent, time-sensitive needs.

- Repayment that fits your salary cycle: Flexible tenure options help you align EMIs with your income flow, so repayments don’t disrupt essentials like rent, groceries, or savings.

- Transparent cost structure: Interest starts from 2 per cent per month, and processing fees typically fall between 1 per cent and 2 per cent, depending on your profile and loan size. The structure is clearly outlined before you commit.

- Complete control from your phone: The Pocketly app lets you apply, track due dates, and manage repayments anytime, giving you visibility and convenience throughout the loan cycle.

Used responsibly, Pocketly works best as a temporary financial bridge, not a habit. It can help you solve urgent cash needs while keeping your broader budgeting and financial goals steady.

FAQs

1. What is good debt in simple terms?

Good debt is borrowing that helps improve your financial position over time. It is usually taken for education, buying a home, or starting a business, where the long-term benefits outweigh the cost of interest.

2. Is a home loan considered good debt?

A home loan is often considered good debt because it helps you build an asset that may appreciate in value. However, it is only good debt if the EMI is affordable and does not strain your finances.

3. Can personal loans ever be good debt?

Yes, personal loans can be good debt if used for productive purposes such as consolidating high-interest debt, funding skill development, or managing essential expenses. They become bad debt when used for unnecessary lifestyle spending.

4. How do I know if I am taking too much debt?

If your total EMIs exceed a comfortable percentage of your monthly income, or if you struggle to cover basic expenses after repayments, you may be overleveraged. A good rule is to keep total EMIs within a manageable portion of your income.

5. Is credit card debt always bad debt?

Credit card debt is generally considered bad debt when balances are carried forward at high interest rates. However, if the full amount is paid on time every month, it can be a useful financial tool rather than harmful debt.