Why do so many Indians learn to earn, but never learn to manage money? Most of us finish school knowing calculus and chemical equations, but not how credit cards charge interest, how taxes work, or how to build savings. There’s no structured money education at home or in classrooms. So young adults enter real life without the financial playbook they actually need.

That gap shows up fast. Salaries vanish before the month ends. Credit is used without understanding interest. Investments are skipped out of fear or poor advice. Insurance is bought without knowing what it covers. Small mistakes stack up into stress, debt, and missed opportunities.

The encouraging part is that financial literacy isn’t complicated. Once you grasp basic money concepts, earning, spending, saving, borrowing, and investing,g things shift quickly. This blog breaks down the state of financial literacy in India, why the gap exists, and what practical steps can help young Indians build financial confidence that lasts.

TL;DR

- Financial literacy in India is still low, especially among students, women, and rural households, despite the rapid rise of UPI, digital loans, and investing apps.

- Financial literacy means knowing how to budget, save, borrow, invest, insure, and use digital finance safely.

- Low literacy leads to poor credit decisions, debt traps, low savings, and higher exposure to scams and mis-selling.

- Small habits like tracking expenses, comparing financial products, learning interest rates, and planning goals help young Indians build confidence and long-term financial health.

What Is Financial Literacy?

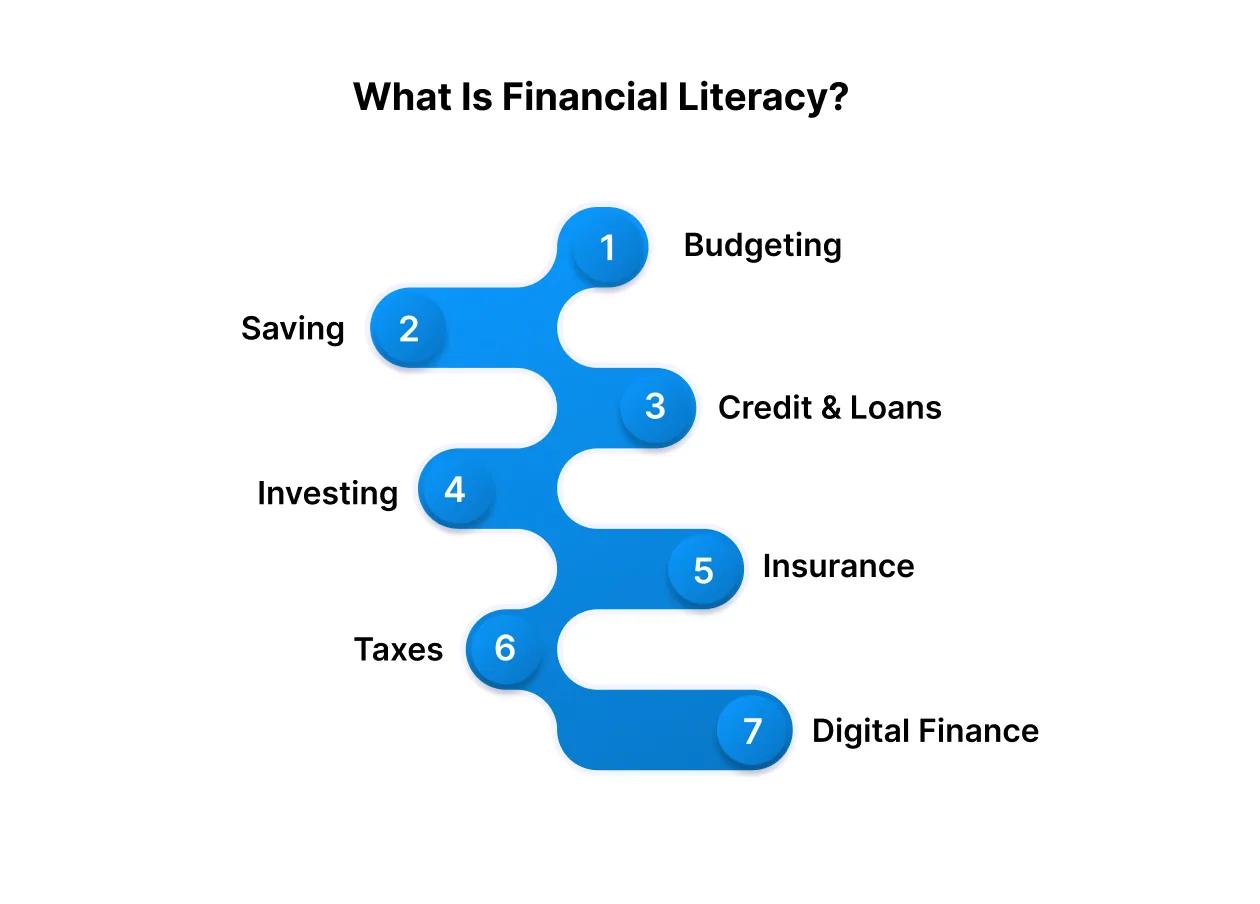

Financial literacy is the ability to understand and manage personal money decisions. It covers how you earn, spend, save, borrow, insure, and invest.

Financial literacy is the ability to understand and manage personal money decisions. It covers how you earn, spend, save, borrow, insure, and invest.

At its core, financial literacy helps you answer questions like:

- How much do I spend every month?

- How do I save for emergencies?

- Should I use credit for this purchase?

- Where should my money grow?

- What risks do I need to protect against?

Key parts of financial literacy include:

- Budgeting: Tracking income and expenses so money doesn’t disappear without reason.

- Saving: Building buffers for emergencies and future needs.

- Credit & Loans: Knowing interest, fees, repayment timelines, and limits.

- Investing: Putting money into assets that can grow over time.

- Insurance: Protecting against health, life, and property risks.

- Taxes: Knowing what you owe and why.

- Digital Finance: Using UPI, net banking, wallets, and financial apps safely.

Once these basics click, handling money becomes less about guesswork and more about informed choices.

The State of Financial Literacy in India Today

India has made progress in digital payments and banking access, but financial literacy hasn’t kept pace. Most people use money every day without understanding how financial systems work.

Surveys over the last few years show a consistent pattern: a large share of Indians lack basic knowledge of budgeting, saving, credit, insurance, or investing. Many open bank accounts but don’t actively use them. People invest based on word-of-mouth, not research. Credit cards are used without knowing how interest accumulates. Insurance policies are purchased for tax benefits rather than protection.

There are clear gaps across demographic groups:

- Urban vs Rural: Urban users adopt digital finance faster, but awareness of products is still limited.

- Men vs Women: Women face lower exposure to financial decisions at home, reducing confidence.

- Youth vs Older Adults: Young people transact digitally but lack planning and investment habits.

The mismatch is striking: India is becoming more digital, yet most users are financially under-informed. This creates room for missteps, mis-selling, and avoidable financial stress.

Why Financial Literacy Matters in India?

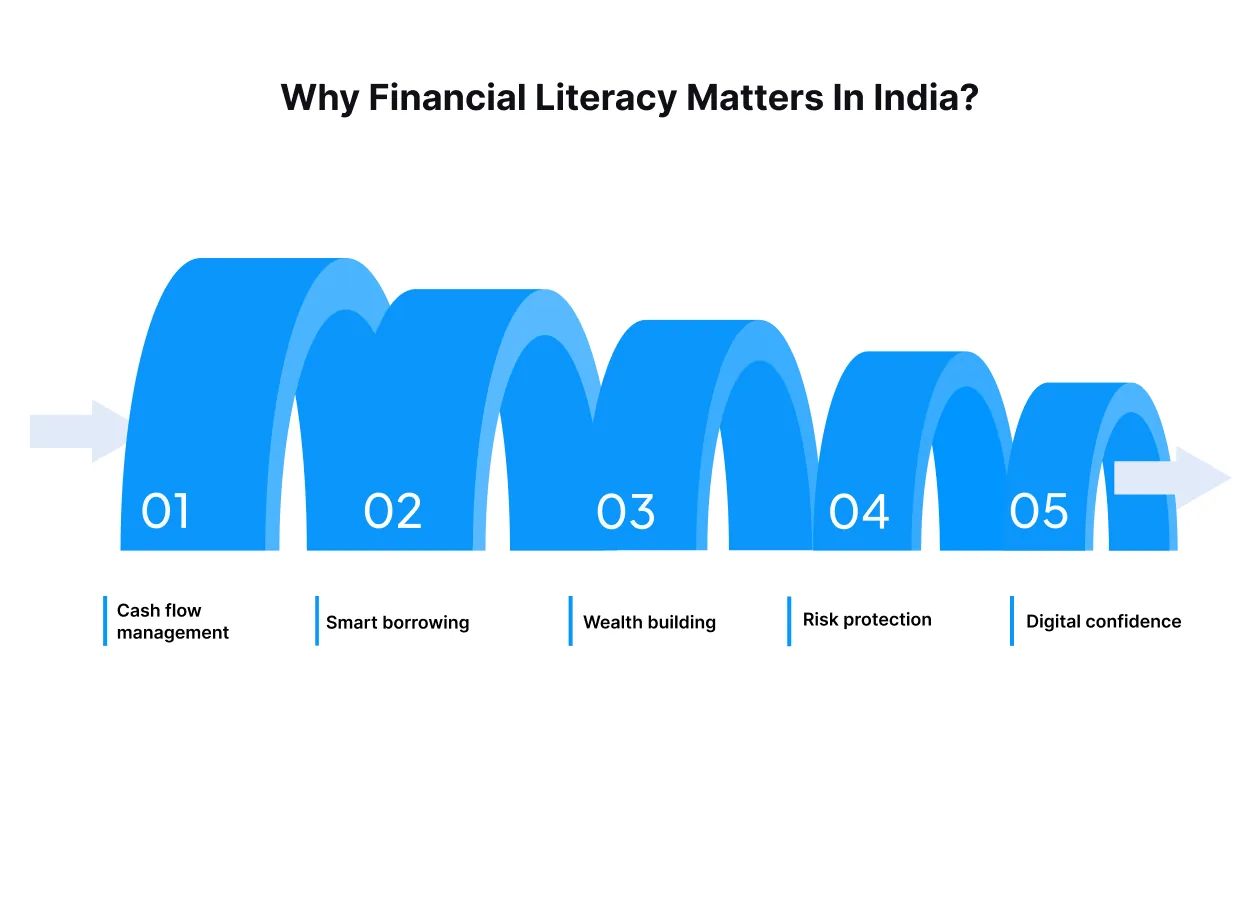

Money decisions shape daily life, yet without basic financial skills, those decisions become guesses. In India, this gap shows up quickly in how people borrow, spend, save, and invest.

Money decisions shape daily life, yet without basic financial skills, those decisions become guesses. In India, this gap shows up quickly in how people borrow, spend, save, and invest.

When financial literacy is low:

- Salaries get consumed by routine expenses with little left at the end of the month.

- Credit cards and BNPL offers turn into unplanned debt.

- Insurance is avoided or misunderstood.

- Investments are delayed until “later”.

- Digital payments increase, but fraud awareness doesn’t.

- Taxes feel intimidating, so compliance suffers.

Financial literacy solves these problems by building practical money skills around:

- Cash flow management: Knowing where money goes and how to control it.

- Smart borrowing: Understanding interest, tenure, and repayment impact.

- Wealth building: Using systematic saving and investing instead of hoarding cash.

- Risk protection: Using insurance to absorb unpredictable shocks.

- Digital confidence: Using UPI, wallets, and accounts safely without falling for scams.

For a fast-growing country with rising digital payments, first-time investors, expanding credit access, and a young workforce, financial literacy isn’t just helpful; it’s a foundational life skill.

Barriers to Financial Literacy in India

Financial literacy doesn’t lag because people don’t care about money; it lags because the environment makes it hard to learn. Several structural and behavioural barriers get in the way:

1. No Early Exposure

Most Indians leave school knowing algebra but not how debt works, how to pay taxes, or how to open an investment account. Money management simply isn’t part of the curriculum, so young adults enter the workforce without basic financial judgment.

Take a first-time credit card user. Without knowing how interest compounds, it’s easy to treat it like “extra money” and end up paying more than expected. Not because they’re careless, but because no one taught them how the system works.

The outcome is predictable: people learn about money through costly mistakes instead of structured learning. What should be taught early ends up being learned late.

2. Cultural Silence Around Money

Money is a sensitive topic in many Indian households. Parents make financial decisions quietly, children aren’t involved, and debt or investment choices are rarely discussed openly. The intention is protective, but the side effect is isolation from practical money lessons.

For example, someone may start earning a salary without knowing how to create a basic budget or why insurance matters. They’ve seen money move in the family, but never learned how it was planned.

When financial decision-making stays behind closed doors, the next generation starts their financial journey without a map.

3. Informal Advice Over Informed Decisions

When financial knowledge is limited, people turn to the sources they trust most: friends, relatives, or agents. The problem is that informal advice often lacks context or accuracy. Some suggest buying insurance only for tax savings, while others promote investments purely on “tips.”

Picture someone investing in a random stock because a colleague did, or buying a complex insurance policy without reading the fine print. It feels convenient in the moment, but the risk is high when decisions aren’t grounded in facts.

Without credible inputs, financial planning becomes guesswork instead of strategy.

4. Product Complexity

Mutual funds, credit cards, and insurance policies are designed with layers of terms, conditions, and jargon. For someone new to finance, words like “ULIP”, “expense ratio”, or “credit utilisation” can feel like a foreign language.

Imagine trying to pick a health insurance plan and ending up overwhelmed by network hospitals, room rent caps, or co-pay clauses. The result? People either avoid products entirely or choose based on whatever sounds simplest, not what actually suits them.

Complexity doesn’t stop people from needing financial tools; it just stops them from using them correctly.

5. Language & Accessibility Gaps

Even as digital finance grows, most high-quality financial content is still produced in English. For a country where regional languages dominate everyday life, that’s a huge barrier.

Think about someone in a Tier-2 city trying to understand SIPs or credit scores. If the best explanations are in English, their access to financial clarity instantly shrinks. They end up depending on second-hand interpretations, which aren’t always accurate.

Language shouldn’t decide who gets to make informed money decisions, but in India, it still does.

6. Digital Adoption Without Education

India adopted UPI, BNPL, and digital banking at an incredible pace. The problem is that financial awareness hasn’t grown at the same speed. People know how to make payments, but not how to avoid fraud. They know how to swipe credit, but not how billing cycles or interest rates work.

Take BNPL apps, users love the convenience, but many don’trealisee that late payments affect their credit score. Small delays can snowball into future borrowing issues, all because the terms weren’t understood upfront.

Digital tools make transactions easier, but without education, they make mistakes faster, too.

If you're a student looking to start earning online but unsure where to begin, check out our comprehensive guide How to Make Money Online as a Student Without Investment.

Who Is Most Affected by Low Financial Literacy in India?

Low financial literacy doesn’t impact everyone equally. Certain groups feel the gap more because of lower exposure, limited guidance, or reduced access to reliable information.

| Group | What Makes Them Vulnerable |

| Students & Young Adults | Learn to earn before learning to budget, save, or handle credit. |

| Women | Handle expenses but are often excluded from loans, insurance, and investing decisions. |

| Low-Income Households | Prefer informal borrowing due to convenience and familiarity, leading to high-cost choices. |

| Rural Populations | Access to banking has improved, but usage knowledge remains limited. |

| First-Time Digital Users | Use UPI and credit products without clarity on charges, credit scores, or fraud risks. |

These groups don’t lack intelligence; they lack access, exposure, and financial guidance. And that gap shapes how confidently they can participate in India’s growing financial ecosystem.

How Digital Finance Is Changing the Literacy Conversation

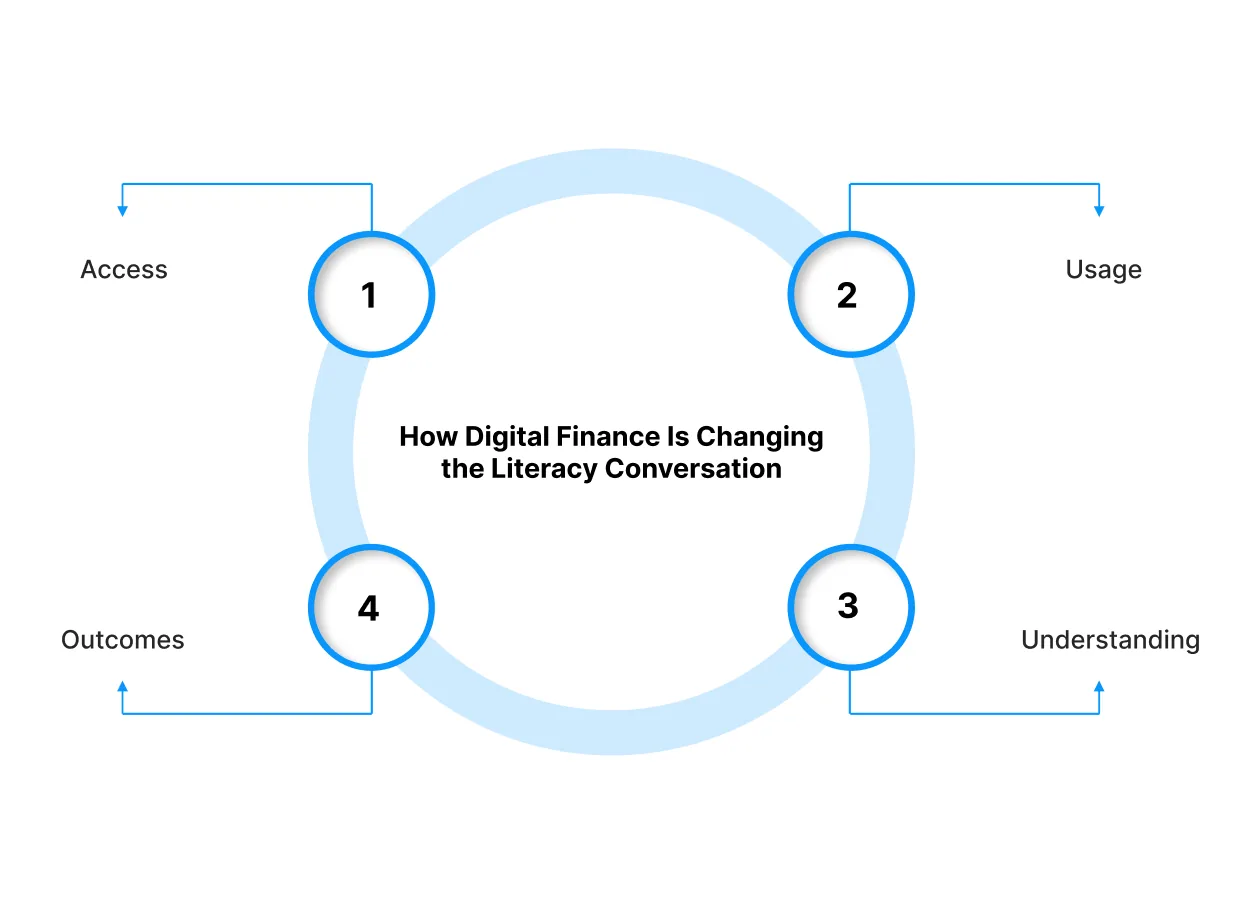

Digital finance in India isn’t just about new apps; it has rewritten how people interact with money. The shift can be understood through a simple four-stage model:

Digital finance in India isn’t just about new apps; it has rewritten how people interact with money. The shift can be understood through a simple four-stage model:

1. Access

Digital systems lowered entry barriers that once required paperwork or physical branches.

Examples: UPI onboarding with mobile numbers, instant KYC on investing apps, Aadhaar-linked bank accounts.

2. Usage

Once access was unlocked, product adoption surged. People began using tools without first learning the mechanics.

Behaviours observed:

- UPI for daily transactions

- Wallets for micro-payments

- BNPL for small credit needs

- App-based SIPs for investing

3. Understanding

Usage triggered new literacy needs that didn’t exist earlier. People started encountering concepts like:

- Credit score (how borrowing affects reputation)

- Interest & billing cycles (especially for BNPL and credit cards)

- Risk & diversification (for mutual funds or equities)

- Data safety (UPI fraud, phishing, unauthorised access)

4. Outcomes

Digital finance has produced mixed but notable outcomes:

Positive:

- Wider banking participation

- Early entry into investing

- More exposure to formal credit

- Faster payments and lower friction

Negative:

- Higher fraud exposure

- Misuse of credit due to a weak understanding

- Savings replaced by convenience spending

- Overconfident investing without risk awareness

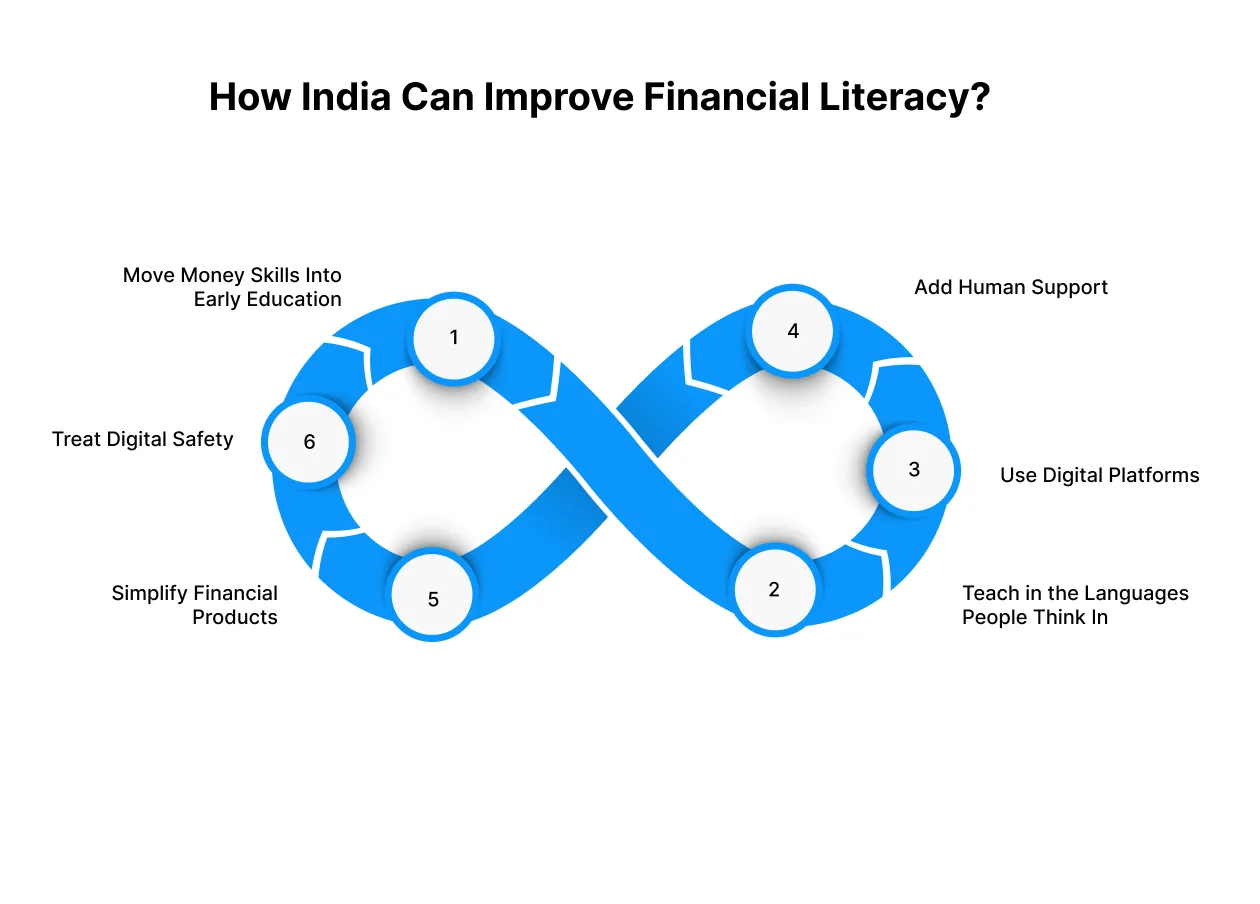

How India Can Improve Financial Literacy?

Improving financial literacy is not just about awareness campaigns. It is about changing how people learn about money and how they behave when making financial decisions. A workable approach looks like this:

Improving financial literacy is not just about awareness campaigns. It is about changing how people learn about money and how they behave when making financial decisions. A workable approach looks like this:

Step 1: Move Money Skills Into Early Education

If compound interest and credit scores were taught in Class 8, students would understand how borrowing and saving actually work before they start earning.

For example, a student who learns how credit utilisation affects credit score will handle a first credit card very differently from someone who learns through penalties.

Why it matters: Early exposure builds familiarity, and familiarity reduces fear-driven avoidance later in life.

Step 2: Teach in the Languages People Think In

People often think and plan in their regional language even if they transact in English digitally. When concepts like SIP or insurance coverage are explained in Tamil or Marathi, they stop feeling abstract.

For instance, a farmer in Maharashtra understanding crop insurance through a Marathi WhatsApp explainer will make better risk decisions than through an English brochure.

Why it matters: Language changes comprehension speed. Better comprehension leads to healthier financial decisions.

Step 3: Use Digital Platforms That Already Have Attention

Mass behaviour change works when learning happens where attention already exists. Short modules inside UPI apps or personal finance videos on YouTube reach more people than traditional workshops.

For example, a thirty-second animation explaining billing cycles on a credit card inside a BNPL app will prevent more late fees than a PDF buried on a website.

Why it matters: Education becomes ambient rather than scheduled, and ambient learning scales effortlessly.

Step 4: Add Human Support Where Digital Alone Cannot Convert

Many first-time users trust humans more than interfaces. Community workshops run by banks, post offices, SHGs or local NGOs help people ask basic questions without feeling judged.

Imagine a pensioner in Bihar learning how to use net banking through a local banker instead of a chatbot. That one interaction unlocks long-term confidence.

Why it matters: Trust accelerates adoption. Humans provide trust in a way screens cannot.

Step 5: Simplify Financial Products Instead of Complicating Them

Financial products often fail not because they are bad, but because they are confusing. Insurance brochures with room rent limits and co-pay terms overwhelm users. Meanwhile, a simple term plan with clear benefits gets adopted faster.

Consider the mutual fund industry shifting from jargon-heavy brochures to simple SIP calculators. Adoption increased because the decision became intuitive.

Why it matters: When comprehension improves, mis-buying and regret buying go down dramatically.

Step 6: Treat Digital Safety as a Core Financial Skill

UPI, BNPL, credit apps and trading platforms have fused finance with technology. Users need to know how to recognise phishing attempts, why auto-debits must be checked, and how late BNPL payments impact credit score.

For example, someone who understands how CIBIL scoring works will think twice before defaulting on a 900 rupee BNPL payment.

Why it matters: Digital participation without digital literacy creates vulnerability. The goal is not just access, but safe access.

To learn more about the basics of financial planning, read our guide on Understanding the Basics of Financial Planning and Its Importance.

Building Money Skills Takes Time, Pocketly Helps With Short Gaps

Financial literacy helps you plan, save, and make better decisions. But even when you’re learning good habits, real life still brings timing issues. A delayed stipend, a sudden repair, or a medical bill can disrupt your budget and push you to borrow from friends or use expensive credit.

Pocketly helps young Indians handle these timing gaps with quick, small loans you can control.

Why people choose Pocketly:

- Borrow only what you need (₹1,000 to ₹25,000)

- No collateral or guarantors

- Fast digital KYC and quick approval

- Instant transfer to your bank account after approval

- Repayment options that follow your cash flow

- Transparent pricing: interest from 2% per month, processing fee 1% to 8%

- 24/7 access through the app

Pocketly partners with regulated NBFCs, offering secure, clear terms without hidden charges. When unexpected costs show up, Pocketly helps you handle them calmly and get back to your routine.

Conclusion

Financial literacy grows with practice. Small steps like learning to budget, comparing financial products, or understanding interest rates can improve how you handle money over time. The aim isn’t to know everything at once but to build steady habits that support your financial goals.

Track your expenses, stay curious, and adjust when needed. When month-end shortages or unexpected expenses arise, address them early so they don’t disrupt your plans. With basic financial awareness, you stay in control even during stressful situations.

If a temporary cash gap shows up, short-term support can help you stay on track. Pocketly offers quick, small-ticket loans for students and young professionals facing short-term cash crunches, giving you some breathing room without derailing your progress. Download the Pocketly app on iOS or Android to get support when you need it.

FAQs

1. What does financial literacy mean?

Financial literacy means understanding how to manage money, covering budgeting, saving, investing, borrowing, credit, and basic financial planning.

2. Why is financial literacy important in India?

It helps people make smarter financial decisions, avoid debt traps, use digital finance safely, and build long-term financial stability.

3. What areas does financial literacy cover?

It includes budgeting, saving, investments, insurance, credit and loans, taxes, and digital financial tools like UPI or net banking.

4. Is financial literacy low in India?

Yes. Surveys from RBI and NCFE show that financial literacy levels in India are still low, especially among women, students, and rural households.

5. How can students improve their financial literacy?

Students can start by learning to budget, tracking expenses, understanding interest rates, exploring basic investment options, and avoiding impulsive borrowing.

6. Does financial literacy help with borrowing?

Yes. It helps people understand interest rates, repayment schedules, and total borrowing costs, which leads to better credit decisions and fewer financial mistakes.