Interest rates are never static, especially in India’s evolving credit market. One change in the repo rate can quietly increase your EMI, affecting everything from your monthly cash flow to your long-term savings. When choosing a loan, the decision between a fixed or floating interest rate may seem technical, but it directly shapes how much you repay over the years.

The real challenge is uncertainty. A floating rate may look cheaper today, but can rise without warning. A fixed rate offers predictability, yet it may start higher and limit flexibility. Many borrowers decide based on short-term comfort instead of long-term financial impact, and that mistake can be costly.

Understanding how each option behaves across different rate cycles is essential. In this blog, you will learn the difference between fixed and floating interest rates, the risks involved, and how to choose the option that aligns with your income stability and financial goals in 2026.

TL;DR

- Fixed rates offer stability: Your EMI remains constant, helping with predictable budgeting and planning, especially during rising interest cycles.

- Floating rates can save money: Start lower and may reduce if market rates fall, but EMIs can increase unexpectedly, impacting cash flow.

- Choose based on your profile: Consider income stability, loan tenure, risk tolerance, and the current interest rate trend before deciding.

- Conversions are possible: Many banks allow switching between fixed and floating, but check fees and total savings before opting.

- Cover urgent gaps smartly: Short-term loans from platforms like Pocketly help manage unexpected expenses without derailing your repayment plan.

What Is a Fixed Interest Rate?

A fixed interest rate means your loan interest remains constant for a specified period, regardless of changes in market conditions or RBI policy rates. Whether interest rates rise or fall, your agreed rate stays the same during the fixed tenure.

In practical terms, this means your EMI does not change because of external rate fluctuations. The predictability makes financial planning easier, especially for long-term loans like home loans.

Key Characteristics

- The interest rate remains constant for the chosen fixed period

- EMIs stay stable and predictable

- Limited or no immediate impact from repo rate changes

- Often slightly higher than floating rates at the start

Advantages

Stable EMIs help you plan monthly expenses confidently without worrying about sudden increases. This makes fixed rates appealing during periods when interest rates are expected to rise.

Limitations

Fixed rates may start higher than floating rates. If market rates fall significantly, you may not benefit unless your loan allows conversion, which could involve additional charges.

Fixed interest rates are typically preferred by borrowers who value stability over potential savings from market fluctuations.

What Is a Floating Interest Rate?

A floating interest rate changes over time based on market conditions. In India, most floating loans are linked to external benchmarks such as the RBI repo rate. When the benchmark moves up or down, your loan interest rate adjusts accordingly.

This means your EMI or loan tenure can increase or decrease depending on interest rate cycles. During falling rate periods, borrowers may benefit from lower EMIs or faster loan repayment. However, when rates rise, repayments can become more expensive.

Key Characteristics

- Linked to benchmark rates such as the RBI repo rate

- The interest rate fluctuates during the loan tenure

- EMI or tenure may change periodically

- Usually starts lower than fixed rates

Advantages

Floating rates often begin at a lower interest rate compared to fixed loans. In a declining interest rate environment, borrowers can benefit from reduced EMIs or shorter loan tenure without renegotiating the loan.

Limitations

The biggest risk is unpredictability. If interest rates rise, your EMI may increase, or your loan tenure may extend, affecting your monthly cash flow and long-term repayment plan.

Fixed vs Floating Interest Rate: Detailed Comparison

At first glance, the difference between a fixed and floating interest rate may appear minimal. However, the real impact becomes visible over time, especially in long-term loans where even small rate changes can significantly alter your total repayment.

Instead of focusing only on the starting interest rate, it is important to compare stability, risk exposure, and how each option performs in different rate cycles. The table below breaks down these critical differences in a clear and practical way.

| Criteria | Fixed Interest Rate | Floating Interest Rate |

| EMI Predictability | EMI remains the same during the fixed tenure, making monthly planning easier | EMI or loan tenure changes when benchmark rates move |

| Exposure to Rate Changes | Protected from short-term market fluctuations | Directly linked to external benchmarks such as the repo rate |

| Initial Interest Rate | Typically slightly higher at the start | Generally lower at the beginning |

| Behaviour in Rising Rate Cycle | EMI remains stable even if market rates increase | EMI may increase, or tenure may extend |

| Behaviour in Falling Rate Cycle | Does not automatically benefit from rate cuts | EMI may be reduced, or the loan may close faster |

| Risk Profile | Lower risk, more predictable | Higher risk due to uncertainty |

| Long-Term Cost Visibility | Easier to estimate total repayment in advance | Total repayment depends on future rate movements |

| Flexibility | May involve charges to switch to floating | Easier to benefit from falling rates without conversion |

Also Read: Can Paying Bills Help Build a Credit Score?

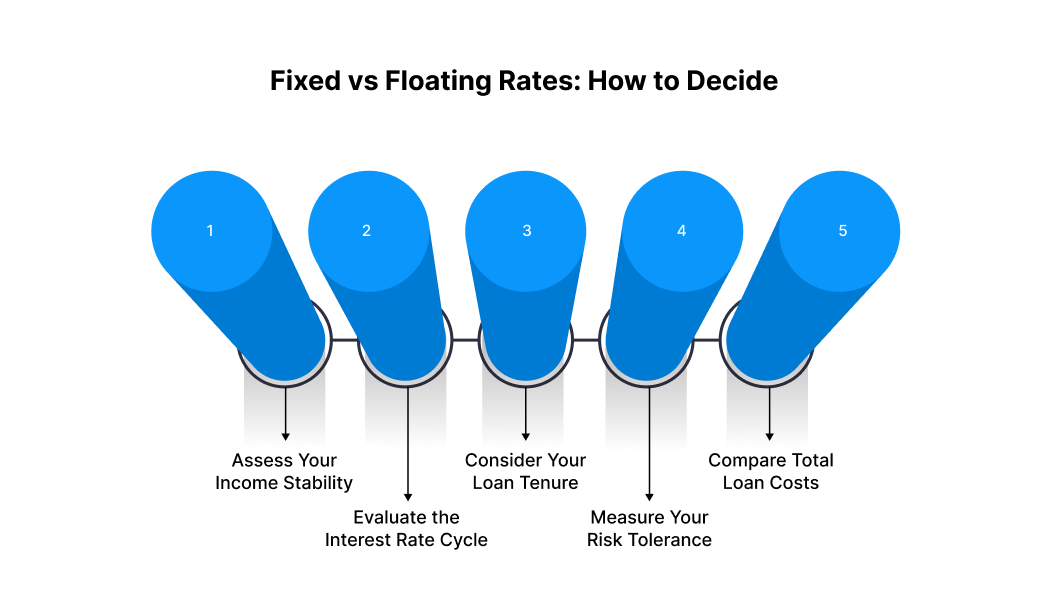

How to Choose Between Fixed and Floating Interest Rates

Choosing the right option depends on your financial profile, loan tenure, and risk appetite. Instead of guessing, use this structured decision checklist.

Choosing the right option depends on your financial profile, loan tenure, and risk appetite. Instead of guessing, use this structured decision checklist.

1. Assess Your Income Stability

Your income pattern should guide your decision. If your salary is fixed and your monthly commitments are already high, predictable EMIs can make financial planning smoother. A fixed interest rate reduces the risk of sudden increases that may strain your cash flow.

On the other hand, if you earn through commissions, business income, or variable freelance payments, you may have the flexibility to absorb EMI fluctuations when rates change.

For example, a salaried employee with tight monthly expenses may prefer fixed rates for stability, while a business owner with seasonal income might manage floating rate variations more comfortably.

2. Evaluate the Current Interest Rate Cycle

Interest rates move in cycles. When rates are relatively low and expected to rise, locking in a fixed rate can protect you from future EMI increases. When rates are high but projected to decline, a floating rate may help you benefit from reductions over time.

Understanding the broader rate environment helps you avoid choosing based solely on the lowest visible rate today.

For instance, if the repo rate has been increasing steadily, a floating loan could become more expensive quickly, whereas fixing your rate early may shield you from that upward trend.

3. Consider Your Loan Tenure

The longer your loan tenure, the greater the impact of rate fluctuations. Even a small percentage increase on a 20-year home loan can significantly raise your total repayment amount. For shorter-term loans, the overall effect of changing rates may be limited.

For example, a five-year personal loan may not experience dramatic cost changes from minor rate adjustments, but a long-term home loan can see a noticeable difference in total interest paid.

4. Measure Your Risk Tolerance

Some borrowers prefer certainty, even if it means paying slightly more at the start. Others are comfortable taking calculated risks to save money. Your comfort with financial uncertainty matters just as much as the numbers.

For example, if rising EMIs would cause stress or disrupt your monthly planning, fixed rates may offer peace of mind. If you are financially prepared for possible fluctuations, floating rates may align better with your goals.

5. Compare the Total Cost, Not Just the Starting Rate

Many borrowers focus only on the initial interest rate, but the real impact lies in the total repayment over the full loan tenure. Fixed rates may appear slightly higher at the beginning, while floating rates may start lower but increase over time. The difference becomes clearer when you calculate the overall interest payable.

Look beyond the headline rate and examine reset clauses, spread margins, and possible conversion charges. A small difference in percentage can translate into a significant amount over long tenures.

For example, on a 20-year home loan, even a 0.5% rate difference can change your total repayment by lakhs. Comparing long-term cost projections helps you make a financially sound decision instead of choosing based on short-term appeal.

Also Read: Short Term vs Long Term Loans: Key Differences

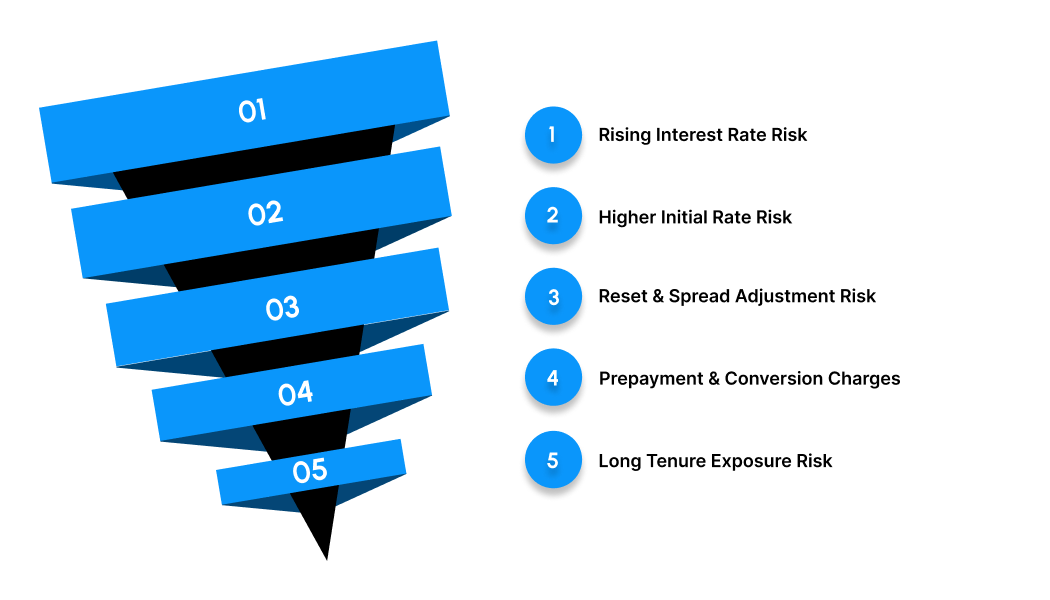

Risks You Should Consider Before Choosing

Selecting between a fixed or floating interest rate is a long-term financial decision, not just a comparison of today’s EMI. Both options carry risks that can impact your repayment burden, cash flow stability, and overall loan cost. Evaluating these risks carefully helps you avoid surprises later in the loan tenure.

Selecting between a fixed or floating interest rate is a long-term financial decision, not just a comparison of today’s EMI. Both options carry risks that can impact your repayment burden, cash flow stability, and overall loan cost. Evaluating these risks carefully helps you avoid surprises later in the loan tenure.

1. Rising Interest Rate Risk

Risk: Floating interest rates are directly linked to benchmark rates. If interest rates increase during your loan tenure, your EMI may rise or your repayment period may extend, increasing the total interest paid over time.

Mitigation: Build a financial cushion that can absorb possible EMI hikes. Avoid stretching your budget to the maximum eligible loan amount. Choosing a manageable EMI from the start reduces stress during rate increases.

2. Paying a Higher Initial Rate Risk

Risk: Fixed interest rates typically start slightly higher than floating rates. If market rates remain stable or decline, you may end up paying more compared to borrowers on floating plans.

Mitigation: Review current interest rate trends before locking into a fixed rate. If you expect rates to soften in the coming years, evaluate whether a shorter fixed period or a floating option may be more cost-effective.

3. Reset and Spread Adjustment Risk

Risk: Floating loans include reset periods and a lender-defined spread over the benchmark rate. Even if benchmark rates fall, changes in the spread or delayed resets may reduce the benefit passed on to you.

Mitigation: Read the loan agreement carefully. Understand how frequently the interest rate resets and whether the lender can modify the spread. Clarity on these clauses prevents repayment surprises.

4. Prepayment and Conversion Charge Risk

Risk: Switching between fixed and floating rates or repaying your loan early may involve processing fees, conversion charges, or penalties. These additional costs can reduce the financial advantage of changing rate types.

Mitigation: Before choosing a loan, review prepayment terms and conversion fees. Factor these costs into your long-term comparison so your decision reflects the true total cost, not just the headline interest rate.

5. Long Tenure Exposure Risk

Risk: The longer your loan tenure, the greater the impact of interest rate movements. Small percentage changes may seem minor initially, but over 15 to 25 years, they can significantly increase the overall repayment amount.

Mitigation: If financially feasible, opt for a shorter tenure or make periodic prepayments to reduce principal faster. Lower outstanding principal reduces the long-term effect of future rate fluctuations.

Understanding these risks ensures that your choice between fixed and floating interest rates is based on long-term financial impact rather than short-term convenience.

Can You Switch From Fixed to Floating (or Vice Versa)?

Interest rates and financial goals change over time. You may begin your home loan with a fixed rate for stability and later prefer the flexibility of a floating rate, or vice versa. Most banks in India allow you to switch between the two, but it usually involves certain conditions and charges.

Let’s break it down clearly.

How Loan Conversion Works?

When you switch from fixed to floating or from floating to fixed, you are not taking a new loan. Instead, your existing lender restructures the interest rate type under a formal request.

Here’s how it typically works:

1. Submit a written request to your bank or NBFC.

2. The lender evaluates:

- Current outstanding principal

- Remaining tenure

- Applicable interest rate benchmarks (like RBI repo-linked rates)

3. You sign a conversion agreement or addendum.

4. The bank applies the revised rate structure from the next EMI cycle.

In India, most floating-rate home loans are linked to the Repo Linked Lending Rate (RLLR) introduced by the Reserve Bank of India, which means rates move with RBI policy changes.

When Switching Makes Sense?

Switching depends on interest rate trends and your personal comfort with risk.

1. Switch From Fixed to Floating When:

- Market interest rates are expected to fall

- RBI policy signals a softer rate cycle

- You want to benefit from repo rate cuts

If rates decline, your EMI or tenure may reduce under a floating structure.

2. Switch From Floating to Fixed When:

- Interest rates are rising sharply

- You prefer EMI stability

- You want predictable long-term budgeting

However, remember that “fixed” loans in India are often fixed only for 2–5 years and may reset later.

A Practical Rule of Thumb

- If you are early in your loan tenure and rates are clearly falling → floating may help you save more.

- If you are risk-averse and prefer certainty (especially during economic uncertainty) → fixed may give peace of mind.

Before switching, always calculate:

- Remaining tenure

- Interest rate difference

- Total savings vs conversion cost

If the savings over time are significantly higher than the fee, the switch may be worth it.

Fixed or Floating for Different Loan Types

Choosing between a fixed or floating interest rate often depends on the type of loan you’re taking, your risk appetite, and how long you plan to repay. Here’s a breakdown of common loan types in India:

| Loan Type | Recommended Rate Type | Short Logic |

| Home Loan | Floating | Long tenure; benefits if rates fall; can switch to fixed later. |

| Personal Loan | Fixed | Short-term, unsecured; predictable repayments avoid surprises. |

| Business Loan | Depends | Floating if cash flows vary; fixed if revenue is stable. |

| Education Loan | Floating | Long-term, floating allows a benefit if rates drop before repayment. |

| Auto Loan | Fixed | Short to medium tenure; fixed ensures EMI stability and easier planning. |

| Loan Against Property (LAP) | Floating | Typically, long tenure and floating can save interest if the property yields cash flows. |

| Gold Loan | Fixed | Short-term, small amounts; fixed keeps interest predictable. |

| Agricultural Loan | Floating | Flexible repayment tied to seasonal income; floating adapts to rate cuts. |

Pocketly: Quick, Transparent Loans Without the Rate Confusion

When unexpected expenses hit, there’s no time to stress over fixed vs floating interest rates. Pocketly gives you fast, short-term loans with clear terms, so you can get the funds you need, no guesswork required.

Why Pocketly is ideal for urgent borrowing:

- Borrow exactly what you need: ₹1,000–₹25,000, keeping repayments manageable.

- No collateral or guarantor: Simple approval, even if you don’t have assets.

- Fast KYC and approval: Get a decision in minutes, not days.

- Instant bank transfer: Funds reach your account immediately after approval.

- Flexible repayment options: Choose a plan that fits your budget.

- Transparent pricing: Interest from 2% per month, processing fees of 1–8%, and no hidden charges.

- 24/7 mobile access: Apply, track, and manage your loan anytime via the app.

With Pocketly, short-term borrowing is straightforward and stress-free. You don’t need to worry about rate types; just focus on covering your urgent expenses quickly and responsibly.

Conclusion

Deciding between a fixed or floating interest rate isn’t just about numbers; it’s about control. Fixed rates give you stability and predictable EMIs, while floating rates can save money if market rates drop. Knowing the difference helps you pick the option that aligns with your budget, goals, and risk tolerance.

Financial surprises happen, from urgent bills to unexpected expenses. With tools like Pocketly, you can access quick, responsible support to manage short-term gaps without disrupting your long-term plans.

Make informed choices, stay in control of your repayments, and protect your financial peace. Download the Pocketly app today on [Android] or [iOS] to handle loans and unexpected expenses with confidence, anytime, anywhere.

FAQs

1. What is the difference between a fixed and a floating interest rate?

A fixed interest rate stays constant for the entire loan tenure, keeping your EMIs stable. A floating interest rate changes based on the RBI’s repo rate or market conditions, which can make your EMIs fluctuate over time.

2. Which is better: a fixed or floating interest rate?

It depends on your risk tolerance and financial goals. Fixed rates suit those who prefer predictable EMIs and stability. Floating rates can be cheaper if market rates fall, but carry the risk of higher EMIs if rates rise.

3. Can I switch from a fixed to a floating interest rate, or vice versa?

Yes, many banks allow conversions between fixed and floating rates. However, it may involve conversion fees or processing charges, so check with your lender before deciding.

4. Are floating interest rates always cheaper than fixed rates?

Not necessarily. Floating rates often start lower than fixed rates but can rise over time with RBI rate hikes. Over the long term, fixed rates may be more cost-effective in a rising rate environment.

5. Should first-time homebuyers choose fixed or floating rates?

If you prefer EMI predictability and a structured budget, fixed rates are safer. If you can handle some EMI fluctuation and want to benefit from potential rate drops, floating rates may save money in the long run.