When you’re short on cash and need money quickly, the choice often comes down to a payday loan or a personal loan. On the surface, both seem like easy solutions. But choosing the wrong one can lock you into high costs, rigid repayments, or unnecessary debt that lingers longer than expected.

The challenge is that most people focus on speed, not structure. This becomes riskier as digital lending grows. In fact, fintech lenders in India sanctioned over 10.9 crore personal loans in FY 2024–25, highlighting how easily credit is now accessible.

More access, however, does not guarantee better decisions.

Without understanding how these two options differ, it is easy to pick what feels convenient in the moment rather than what actually fits your financial situation. In this blog, we break down payday loans vs personal loans so you can choose with clarity, not urgency.

Key Takeaways

-

Payday loans are short-term, small-amount loans for urgent cash needs, repaid by your next paycheck.

-

Personal loans provide larger amounts with lower interest and structured monthly EMIs for planned expenses.

-

Payday loans are faster but more expensive; personal loans take longer to approve but cost less overall.

-

Misusing payday loans can trap you in high-cost debt; personal loans require a stable income but are safer long-term.

-

Digital apps like Pocketly offer quick, transparent, and manageable short-term borrowing for urgent expenses.

What Is a Payday Loan?

A payday loan is a short-term loan that helps you manage urgent expenses when you are running low on money before your next salary. It is commonly used by students and young professionals who need quick cash for immediate needs.

Instead of going through a long bank process, payday loans are designed to be fast and easy to access.

Key characteristics:

-

Short repayment period, usually within a few weeks or once you receive your next salary

-

Small loan amounts meant for urgent needs, not big expenses

-

Quick approval with basic details and minimal documents

-

Higher cost compared to regular loans due to convenience and speed

In simple terms, a payday loan is like borrowing a small amount now and returning it when your salary comes in.

It works best for situations like sudden medical bills, rent gaps, or urgent payments. However, since the repayment time is short and the cost is higher, it is important to borrow only what you can comfortably repay.

What Is a Personal Loan?

A personal loan is a type of loan where you borrow a fixed amount of money and repay it over time in small monthly payments, called EMIs. It is usually used for bigger expenses that cannot be managed with your regular monthly income.

Compared to payday loans, personal loans are more structured and spread out over a longer period, making them easier to repay in smaller chunks.

Key characteristics:

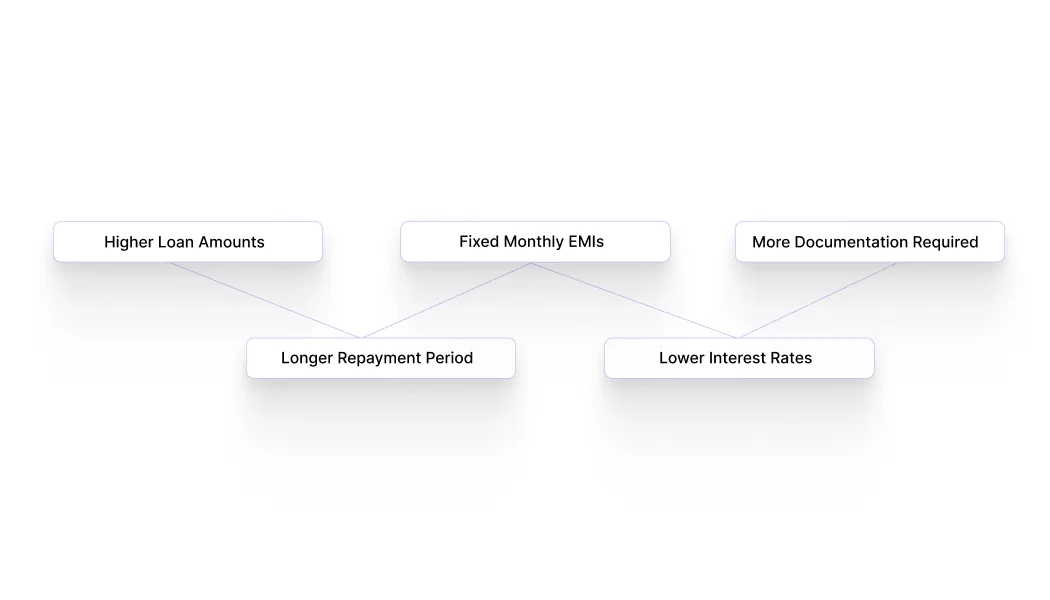

-

Higher loan amounts are suitable for larger expenses

-

Longer repayment period, usually a few months to a few years

-

Fixed monthly EMIs, so you know exactly how much to pay

-

Lower interest rates compared to payday loans

-

Requires more documents, such as income proof or bank statements

In simple terms, a personal loan is like borrowing a larger amount and paying it back slowly over time instead of all at once.

It works well for planned expenses like education, travel, medical treatments, or buying something important. However, since it is a longer commitment, you need a stable income and a clear repayment plan before applying.

Need quick cash for a short-term expense? “Applying for One Day Personal Loan in India” explains how you can get a personal loan in just one day. Learn the easy steps to apply safely and get funds fast.

Payday Loans vs Personal Loans: What’s the Real Difference?

Choosing between a payday loan and a personal loan becomes easier when you compare them side by side. The right option depends on how much money you need, how quickly you need it, and how you plan to repay it.

|

Factor |

Payday Loans |

Personal Loans |

|

Loan Amount |

Small amounts (₹1,000 to ₹25,000) |

Larger amounts (₹50,000 and above) |

|

Repayment Time |

Very short, usually within a few weeks |

Longer, from a few months to years |

|

Approval Speed |

Very fast, often within minutes or hours |

Slower, may take a few days |

|

Documents Required |

Minimal, basic KYC details |

More documents, like proof of income and bank statements |

|

Interest Cost |

Higher due to short-term and speed |

Lower compared to payday loans |

|

Best Use |

Urgent, short-term needs |

Planned, bigger expenses |

Also Read: Minimum Credit Score Required For Personal Loan

When Should You Choose a Payday Loan?

A payday loan makes sense only in specific situations where the need is urgent and short-term. It is not extra income but a temporary solution to handle immediate cash gaps.

You should consider a payday loan if:

-

You need money urgently and cannot wait for a few days

-

The amount required is small and clearly defined

-

You have a fixed income coming soon (salary, stipend, freelance payment)

-

The expense is unavoidable, like medical bills, rent, or essential payments

When it works well:

-

You already know how you will repay it

-

The repayment fits within your next income cycle

-

You are borrowing for a need, not a want

When to avoid it:

-

You are unsure about repayment

-

The expense is not urgent or essential

-

You are already managing other loans

A simple way to think about it: if the problem is short-term and your repayment is certain, a payday loan can help. If not, it can create more pressure instead of solving the issue.

When Is a Personal Loan a Better Option?

A personal loan is a better choice when your financial need is larger, and you need more time to repay it in smaller, manageable amounts.

Unlike payday loans, it is not meant for urgent, last-minute expenses but for planned or slightly bigger financial needs.

You should consider a personal loan if:

-

You need a larger amount of money

-

The expense is planned or semi-planned

-

You prefer paying in monthly instalments instead of one lump sum

-

You have a stable income to support regular EMIs

When it works well:

-

You want predictable monthly payments

-

The repayment can comfortably fit into your monthly budget

-

You are borrowing for important expenses like education, medical needs, or major purchases

When to avoid it:

-

You need money immediately

-

Your income is unstable or uncertain

-

You are not ready for a long-term financial commitment

A simple way to think about it: if your expense is bigger and you need time to repay it, a personal loan is the better fit.

Never miss a payment again. Access ₹1,000–₹25,000 instantly with Pocketly and keep your finances smooth. Apply in minutes and manage urgent expenses effortlessly.

6 Common Borrowing Risks and How to Stay Safe

Both payday loans and personal loans can solve short-term financial problems, but they also come with risks if you do not fully understand how they work. For beginners, the biggest mistake is focusing only on getting the money and not thinking about repayment.

Here are the key risks explained simply, along with how to manage them:

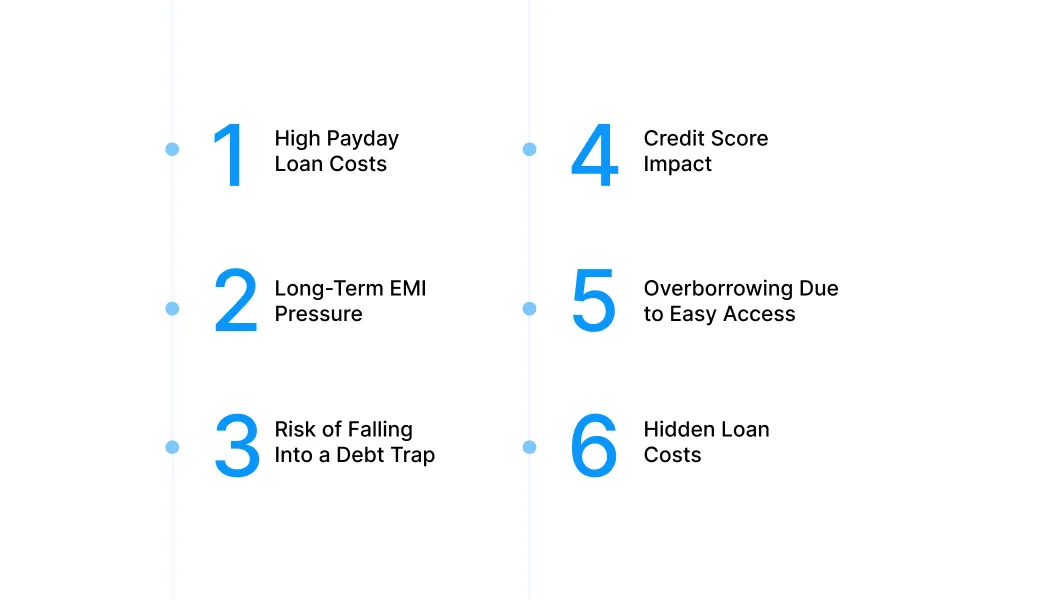

1. High Cost of Borrowing (Payday Loans)

Risk: Payday loans may look small, but they often come with higher interest rates. Because the repayment period is short, even a small delay can increase the total amount you owe. If you keep taking new payday loans, the cost adds up quickly.

Mitigation: Use payday loans only for urgent needs and repay them as soon as your income arrives. Treat them as a one-time solution, not a regular habit.

2. Long-Term Financial Pressure (Personal Loans)

Risk: Personal loans are easier to manage monthly, but they stay with you for a long time. A fixed EMI every month reduces your flexibility, especially if your expenses increase or your income changes.

Mitigation: Before taking a personal loan, check if you can comfortably afford the EMI even in a worst-case month. Do not stretch your budget just to get a higher loan amount.

3. Falling Into a Debt Trap

Risk: A common pattern is borrowing again to repay an existing loan. This creates a cycle where you are always paying off old debt instead of reducing it. Over time, this becomes stressful and difficult to manage.

Mitigation: Always have a clear repayment plan before taking a loan. If you cannot repay from your upcoming income, it is better to reconsider borrowing.

4. Impact on Your Credit Score

Risk: Your credit score reflects how responsibly you handle loans. Missing payments, delaying EMIs, or defaulting can lower your score, making it harder to get loans in the future or increasing your interest rates.

Mitigation: Pay all dues on time and keep track of your repayment schedule. Even one missed payment can have a lasting impact.

5. Overborrowing Because It Feels Easy

Risk: Digital loan apps have made borrowing quick and convenient. This can create a false sense of affordability, where you take loans for things you could have avoided or delayed.

Mitigation: Pause before borrowing and ask yourself if the expense is essential. If it is not urgent, it is better to wait and save.

6. Not Understanding the Total Cost

Risk: Many people only look at how much they are borrowing, not how much they will repay in total. Interest, processing fees, and penalties can increase the final amount significantly.

Mitigation: Always check the full repayment amount before accepting a loan. Make sure you are comfortable with the total cost, not just the monthly payment.

Need Quick Cash? Digital Payday Alternatives Like Pocketly

Life is unpredictable. Unexpected expenses like urgent medical bills, last-minute travel, or essential repairs can disrupt even the most carefully planned budget. When savings aren’t enough, a digital payday solution like Pocketly can help you bridge the gap safely and responsibly.

Here’s why Pocketly is a practical option for short-term borrowing:

-

Borrow only what you need: Loan amounts range from ₹1,000 to ₹25,000, so you avoid taking on unnecessary debt and keep repayments manageable.

-

No collateral or guarantor required: You don’t need to pledge assets or find a co-signer. The process is completely hassle-free.

-

Fast approval with minimal documentation: Quick KYC-based verification allows instant eligibility checks without lengthy paperwork or bank visits.

-

Instant bank transfer: Approved funds are credited directly to your account, giving you immediate access to cash when urgency strikes.

-

Flexible repayment terms: Choose a repayment schedule that aligns with your monthly budget, so EMIs don’t disrupt your financial plan.

-

Transparent pricing: Interest rates start at 2% per month, with processing fees between 1% and 8%, depending on your profile and loan amount—no hidden charges.

-

24/7 app access: Apply, track, and manage your loan anytime using the Pocketly mobile app, wherever you are.

For sudden expenses that can’t wait, Pocketly offers a short-term solution with loans from ₹1,000 to ₹25,000, instant approvals, minimal KYC, and transparent pricing—helping you bridge financial gaps without stress.

Download Pocketly on iOS or Android to handle urgent cash needs safely and stay on track with your budget and goals.

FAQs

1. What’s the key difference between payday loans and personal loans?

Payday loans are short-term, small-amount loans designed to be repaid by your next paycheck, usually at higher interest rates. Personal loans are longer-term, larger loans with structured EMIs, lower interest rates, and more adaptable repayment options.

2. Are payday loans safe to use in India?

Yes, but only when taken from regulated lenders or trustworthy fintech apps like Pocketly. Always review the interest rates, processing fees, and repayment terms to prevent falling into a debt trap.

3. Which type of loan costs less?

Personal loans generally have lower interest rates and fees compared to payday loans. Payday loans are high-cost because they are fast, unsecured, and short-term.

4. Can I get a personal loan without salary slips?

Some banks and fintech lenders accept alternative proof of income, like bank statements, freelance earnings, or business income. Eligibility varies by lender.

5. When should I avoid payday loans?

Avoid payday loans for long-term financial needs or large expenses. They are suitable only for urgent, short-term cash requirements that you can repay quickly.