Paying off a personal loan early sounds like a smart financial move. You reduce interest, close the loan faster, and free up your monthly cash flow. But the decision is not always as straightforward as it seems.

Many borrowers assume that prepayment automatically saves money. What they often overlook are prepayment charges. These fees can reduce or even cancel out the expected savings, depending on when and how you repay the loan.

This is where confusion begins.

Without understanding how personal loan prepayment charges work, it becomes difficult to judge whether closing your loan early is actually beneficial. In this blog, we break down what prepayment charges are, how they are calculated, what RBI rules say, and when prepaying makes financial sense.

Key Takeaways

-

Prepaying a loan only works when the total cost goes down, not just because you close it early.

-

Prepayment charges directly reduce your savings, especially if done early in the loan cycle.

-

Outstanding amount and timing decide your actual cost, not just the interest rate.

-

Comparing interest saved vs charges paid is critical, otherwise prepayment can backfire.

-

The goal is to reduce total repayment, not just finish the loan faster.

What Are Personal Loan Prepayment Charges and Why Banks Apply Them

Personal loan prepayment charges are fees applied when you repay your loan before the agreed tenure ends.

At first, this may seem counterintuitive. You are paying early, so why should there be a cost?

The answer lies in how loans are structured.

When a bank gives you a loan, it expects to earn interest over the full tenure. This expected interest is built into the loan’s pricing and repayment schedule. When you close the loan early, that expected income reduces.

Prepayment charges are applied to balance this loss.

Here is how to think about it:

-

Loans are priced for full tenure: Interest is calculated assuming you will repay over the entire duration

-

Early closure reduces expected earnings: When you prepay, the bank earns less interest than planned

-

Charges help recover part of that loss: The fee compensates for the reduced interest income

This is why prepayment is not always a clear win.

Even if you are closing the loan early, the cost of doing so needs to be evaluated. The real benefit depends on whether the interest saved is higher than the charges applied.

Also Read: How to Manage Monthly Expenses Smartly in 2025

Partial Prepayment vs Full Foreclosure: What Changes in Cost and Flexibility

Not all early repayments are treated the same. The impact on cost depends on whether you make a partial prepayment or close the loan completely through foreclosure.

Understanding this difference helps you choose the option that actually reduces your total cost.

Partial Prepayment

Partial prepayment means paying a portion of the outstanding loan before the scheduled tenure ends, while the rest of the loan continues.

Key things to know:

-

Reduces the principal balance: A lower principal can reduce future interest outflow and may also shorten the tenure.

-

May have lender-specific limits: Some lenders allow partial prepayment only after a certain number of EMIs or only up to a specific percentage of the outstanding balance.

-

Charges may still apply: Even though the loan stays active, the lender may charge a fee on the amount being prepaid.

Full Foreclosure

Full prepayment, also called foreclosure, means closing the entire loan before the original end date.

Key things to know:

-

Ends the loan completely: Once the outstanding principal and applicable charges are paid, the loan account is closed.

-

Usually has stricter conditions: Some lenders apply a lock-in period before full closure is allowed.

-

May involve a higher charge than partial repayment: In some cases, foreclosure charges are applied to the full outstanding balance.

What This Means for You

-

Partial prepayment helps reduce interest gradually with a lower cost impact

-

Foreclosure gives a clean exit but may involve charges that reduce savings

The better option depends on one thing: Which approach lowers your total repayment after accounting for charges?

Also Read: Minimum Credit Score Required For Personal Loan

How Prepayment Charges Are Calculated on a Personal Loan

Personal loan prepayment charges are usually calculated as a percentage of the outstanding principal at the time of repayment. The exact percentage depends on the lender, the loan agreement, and how early you choose to prepay.

This is why two borrowers with the same original loan amount may pay very different charges.

Here is how the calculation typically works:

-

Outstanding principal is the base: The lender usually applies the charge to the unpaid principal balance, not the original loan amount.

-

The charge is a percentage: Many lenders define prepayment charges as a fixed percentage of the amount being prepaid or the total outstanding balance.

-

Timing can affect the cost: Some lenders allow prepayment only after a lock-in period. Others may charge differently depending on how far along you are in the loan tenure.

-

Partial and full prepayment may be treated differently: A partial payment may attract charges only on the prepaid amount, while full foreclosure may apply to the entire outstanding principal.

A simple way to understand the formula is:

Prepayment charge = Outstanding loan amount × Applicable prepayment percentage

For example, if you still owe a certain principal amount and the lender applies a prepayment fee on that balance, the charge is calculated on the unpaid portion, not on what you have already repaid.

This is why it is important to check three things before prepaying:

-

the outstanding principal

-

the applicable prepayment percentage

-

whether any lock-in or minimum EMI condition applies

Once these are clear, you can compare the charge against the interest you would save and decide whether prepayment actually makes financial sense.

Does Prepaying a Personal Loan Actually Save Money

Understanding the calculation is one part. The real decision depends on whether prepaying your loan actually reduces your total cost after accounting for charges.

Let’s break this down with a simple scenario.

Example

-

Outstanding loan amount: ₹1,00,000

-

Prepayment charge: 3%

-

Remaining interest if you continue the loan: ₹20,000

Step 1: Calculate prepayment charge

Prepayment charge = 3% of ₹1,00,000 = ₹3,000

Step 2: Compare cost vs savings

-

Interest saved by prepaying early = ₹20,000

-

Prepayment charge = ₹3,000

Net benefit = ₹17,000 saved

In this case, prepaying makes financial sense because the interest saved is significantly higher than the prepayment charge.

When It May Not Be Worth It

-

If you are in the later stage of the loan, most of the interest is already paid, so savings are limited.

-

If the prepayment charge is high, it can reduce or cancel out the benefit.

-

If the remaining interest is low, the cost advantage of prepayment becomes minimal.

Prepayment is not automatically beneficial. The decision depends on one simple comparison:

Interest you save vs charges you pay

If the savings are higher, prepayment works in your favor. If not, continuing the loan may be the better option.

This is why running a quick cost comparison before making a decision is essential.

Worried about being stuck in a long loan you will want to exit early? Pocketly is built differently. Borrow ₹1,000 to ₹25,000 with short repayment cycles, transparent fees shown upfront, and approval in under 7 minutes, so you always know your total cost before you commit. No surprises at foreclosure. [Check Your Eligibility on Pocketly]

Also Read: Understanding the Process And Meaning of Credit Control

RBI Rules on Personal Loan Prepayment Charges

Prepayment charges are not just decided by lenders. They are also influenced by regulatory guidelines, especially those issued by the Reserve Bank of India (RBI).

Understanding these rules is important because, in some cases, you may not have to pay any prepayment charges at all.

Here are the key points:

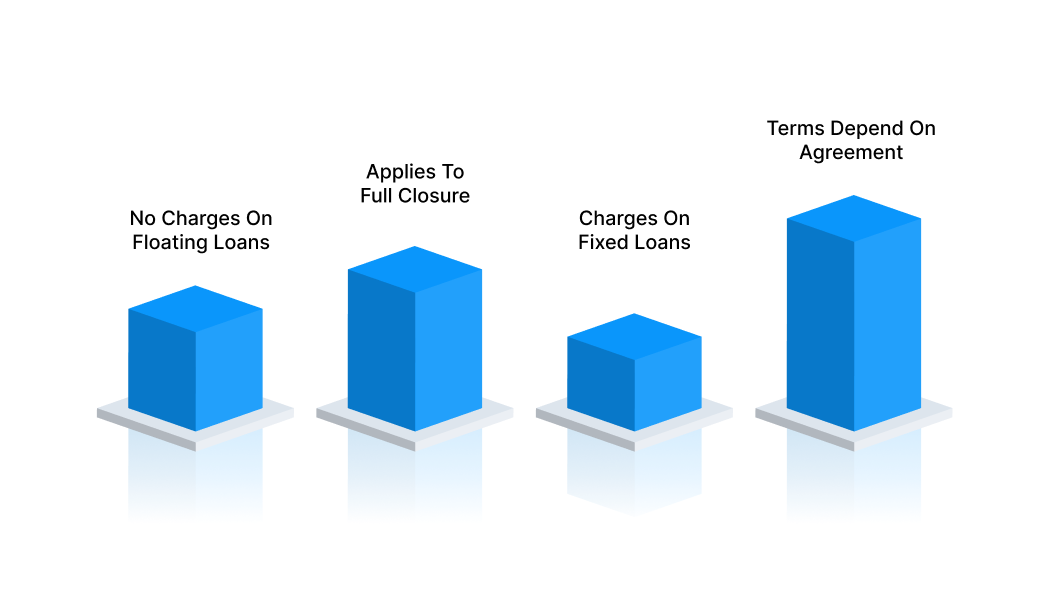

-

No prepayment charges on floating-rate loans (for individuals): As per RBI guidelines, banks and NBFCs are not allowed to charge foreclosure or prepayment fees on floating-rate personal loans taken by individual borrowers.

-

Applies to full prepayment or foreclosure: If your loan falls under this category, you can close it early without paying additional charges.

-

Fixed-rate loans may still have charges: If your personal loan has a fixed interest rate, the lender may apply prepayment or foreclosure charges based on their policy.

-

Terms depend on your loan agreement: The exact conditions, including lock-in periods and eligibility for prepayment, are defined in your loan terms.

For example, if you have a floating-rate personal loan as an individual borrower, you may be able to repay the loan early without any extra fee. However, if your loan is fixed-rate, charges may still apply.

Before deciding to prepay, always check whether your loan is fixed or floating rate. This alone can determine whether you pay a charge or avoid it completely.

When Does Prepayment Make Financial Sense

Prepaying a personal loan can reduce your total interest cost, but only in certain situations. The benefit depends on timing, interest structure, and the remaining loan balance.

Here are the situations where prepayment usually makes sense:

-

Early in the loan tenure: In the initial months, a larger portion of your EMI goes toward interest. Prepaying at this stage can significantly reduce the total interest you pay over time.

-

High-interest-rate loans: If your loan carries a higher interest rate, the potential savings from prepayment are greater compared to lower-rate loans.

-

Large outstanding principal: When a substantial amount of principal is still unpaid, reducing it early can lower future interest outflow.

-

No or low prepayment charges: If your loan has minimal or no charges, especially in the case of floating-rate loans, prepayment becomes more beneficial.

-

Stable cash flow or surplus funds: If you have extra funds that are not required for essential expenses or emergency savings, using them to reduce debt can improve your financial position.

For example, if you are in the first half of your loan tenure and have surplus funds, prepaying can meaningfully reduce your total repayment. On the other hand, doing the same near the end of the tenure may not offer much benefit.

Prepayment works best when it reduces a meaningful portion of future interest without adding significant charges or affecting your financial stability.

When You Should Avoid Personal Loan Prepayment

Prepayment is not always the smarter financial move. In some cases, it can reduce your liquidity without creating meaningful savings.

Here are situations where prepayment may not be worth it:

-

You are near the end of the loan tenure: At this stage, much of the interest has already been paid. Prepaying now may not reduce your total cost by much.

-

Prepayment charges are too high: If the fee takes away most of the interest savings, the financial benefit becomes limited.

-

Your loan carries a low interest rate: If the cost of the loan is already moderate, prepaying may not offer a strong return on your extra funds.

-

You do not have enough emergency savings: Using all available cash to close a loan can leave you financially exposed if an urgent expense comes up later.

-

The money can be used more effectively elsewhere: If the funds are needed for essential expenses, high-cost debt, or stronger financial priorities, prepaying this loan may not be the best use of cash.

For example, if you are in the final stage of repayment and the remaining interest is small, paying a prepayment charge may not create real savings. In that case, continuing the EMI may be more practical.

Do not look at prepayment as a default good decision. It only makes sense when the savings are meaningful and your overall financial position stays strong.

The real fix is not planning a better exit. It is not needing one in the first place. Pocketly's short-term loans are open to salaried individuals, self-employed professionals, and non-salaried borrowers. The loan amounts are structured to match what you actually need, so you repay on schedule without running into foreclosure charges. [Download the Pocketly App and Apply in Minutes]

Also Read: 10 Essential Financial Habits For Success

Hidden Factors Most Borrowers Miss Before Prepaying a Loan

Prepayment decisions are often based on interest savings alone. But there are other factors that can impact the actual benefit.

Here are the key ones most borrowers overlook:

-

Interest is front-loaded in early EMIs: In the initial phase of a loan, a larger portion of your EMI goes toward interest. This means prepaying early can have a higher impact compared to later stages

-

Charges may be reduced after a certain period: Some lenders lower or remove prepayment fees after a specific number of EMIs. Timing your prepayment can change the cost significantly

-

Cash flow impact matters: Using a large lump sum to close a loan may affect your liquidity, even if it reduces total interest

-

Alternative use of funds: The same money could be used elsewhere, such as investments or emergencies, which may offer better flexibility

-

Loan tenure left changes the outcome: If only a few EMIs remain, the interest left may be too low to justify prepayment charges.

These factors show that prepayment is not just a calculation problem. It is also a timing and cash-flow decision.

Also Read: 10 Smart Spending Tips For Financial Wellness

Avoid Prepayment Charges with Pocketly for Short-Term Needs

Prepayment charges usually become a concern when the original loan does not match the actual need. A longer tenure is chosen for flexibility, but later you try to close it early to reduce interest. That is when additional costs come into play.

In many cases, this is not a repayment problem. It is a structuring problem.

Instead of taking a long-term loan and planning to prepay, it can be more efficient to choose a borrowing option that already aligns with a shorter repayment cycle.

Pocketly is built around this idea. It focuses on short-term borrowing where the tenure and loan size are designed to match immediate needs, reducing the need for early closure.

Here is how it fits better in this context:

-

Short tenure reduces the need for prepayment: With repayment cycles typically ranging from around 60 to 180 days, the loan is structured to be completed within a shorter period rather than extended over years.

-

Smaller loan sizes avoid long-term commitment: Borrowing within a limited range helps ensure that the loan is aligned with the actual requirement instead of creating excess debt that needs to be prepaid later.

-

Cost is visible before you proceed: Interest and processing fees are defined upfront, allowing you to evaluate the total cost instead of dealing with unexpected charges during repayment.

-

No need to plan an exit strategy: Since the borrowing is short-term by design, you are not forced to think about foreclosure or prepayment charges midway.

-

Faster access for time-sensitive needs: A fully digital process with quick verification helps you address urgent expenses without entering a long approval cycle.

Download the Pocketly app on Android or iOS to check your eligibility and access funds when you need them.

FAQs

Q: What are personal loan prepayment charges?

Personal loan prepayment charges are fees applied when you repay your loan before the agreed tenure. They are usually calculated as a percentage of the outstanding principal.

Q: How are prepayment charges calculated on a personal loan?

They are typically calculated as a fixed percentage of the remaining loan amount at the time of prepayment. The exact rate depends on the lender and your loan terms.

Q: Is it always beneficial to prepay a personal loan early?

Not always, because prepayment charges can reduce the savings from lower interest. It makes sense only when the interest saved is higher than the fee paid.

Q: What is the difference between partial prepayment and foreclosure?

Partial prepayment means paying a portion of the loan early while continuing EMIs. Foreclosure means closing the entire loan before the end of the tenure.

Q: When should I avoid prepaying my personal loan?

You should avoid it if you are near the end of the tenure or if charges are too high. In such cases, the savings may not justify the cost.

Q: Does prepaying a personal loan affect my credit score?

Yes, it can have a positive impact if the loan is closed responsibly. However, the effect depends on your overall credit profile and repayment history.