Many young Indians today use UPI, digital wallets, and short-term credit regularly, but understanding concepts such as EMIs, interest charges, and repayment planning still remains a challenge. India’s rapid growth in digital borrowing and retail finance participation has increased the need for better financial awareness among young borrowers.

Without proper financial literacy, borrowers may misunderstand loan terms, ignore repayment obligations, or rely on informal financial advice. This can lead to unnecessary debt pressure, missed EMIs, and poor financial decisions over time.

As digital finance becomes more accessible across India, financial awareness is becoming equally important for students, salaried professionals, and self-employed individuals. This guide explores the major challenges of financial literacy in India, how they affect borrowing behaviour, and practical ways to make more informed financial decisions.

Key Takeaways

-

Financial literacy helps individuals understand budgeting, EMIs, loan repayments, savings, and borrowing decisions more responsibly.

-

Many young Indians still face challenges such as limited financial education, poor loan awareness, and dependence on unverified financial advice.

-

Weak financial literacy can lead to missed EMIs, unnecessary borrowing, repayment pressure, and misunderstanding of total loan costs.

-

Practical habits such as tracking expenses, reviewing loan terms, and understanding repayment affordability can improve financial decision-making over time.

-

Structured borrowing and better repayment awareness can help students, salaried professionals, and self-employed individuals manage short-term financial needs more responsibly.

What Is Financial Literacy and Why Does It Matter?

Financial literacy refers to the ability to understand and manage money-related decisions responsibly. This includes understanding:

-

Budgeting and monthly expenses

-

Savings and emergency planning

-

Loan repayments and EMIs

-

Interest rates and borrowing costs

-

Digital payment and credit systems

In simple terms, financial literacy helps people make informed decisions about spending, saving, borrowing, and managing debt.

Financial literacy has become increasingly important as more young Indians enter formal financial systems through digital banking, UPI payments, EMI-based purchases, and short-term borrowing products.

Without proper financial awareness, borrowers may struggle to understand repayment obligations, interest charges, or the long-term impact of borrowing decisions.

Good financial literacy can help individuals:

-

Plan monthly budgets more effectively

-

Compare loan options carefully

-

Avoid unnecessary debt pressure

-

Manage EMIs responsibly

-

Identify unsafe financial practices or scams

For example, a student taking a first personal loan or purchasing a smartphone through EMI may need to understand repayment timelines, processing charges, and monthly affordability before borrowing. Without this awareness, even small repayment obligations may become difficult to manage later.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

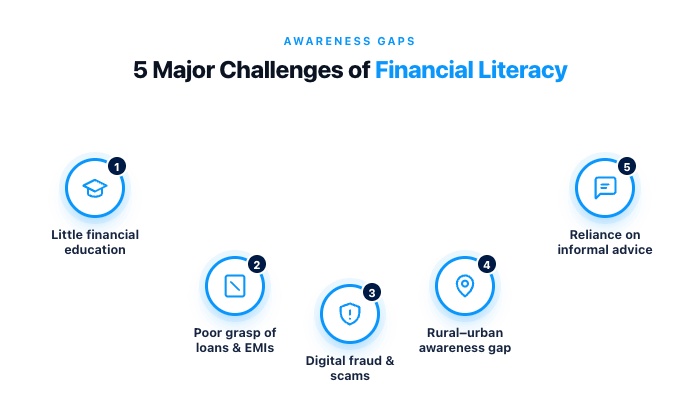

Major Challenges of Financial Literacy in India in 2026

Financial awareness in India has improved with the growth of digital banking, UPI payments, online investing, and easier access to short-term credit. However, access to financial products has grown much faster than financial understanding.

Many individuals now use digital financial services regularly without fully understanding repayment obligations, interest costs, budgeting, or long-term borrowing impact.

This gap often affects financial decisions across students, salaried professionals, self-employed individuals, and first-time borrowers who are entering formal credit systems for the first time.

Challenge 1: Lack of Financial Education

One of the biggest challenges is the absence of practical financial education in schools and colleges. While students may learn academic subjects in detail, many receive little exposure to real-world financial concepts such as:

-

Budgeting monthly expenses

-

Understanding interest rates

-

Managing savings

-

Calculating EMIs

-

Using credit responsibly

-

Reading loan terms and repayment schedules

As a result, many young adults begin managing salaries, bank accounts, or loans without understanding how borrowing decisions may affect their future finances.

Financial learning often happens only after facing repayment stress or making avoidable financial mistakes.

Challenge 2: Poor Understanding of Loans and EMIs

Many borrowers focus mainly on whether the monthly EMI appears affordable without evaluating the full repayment structure. This creates confusion around:

-

Total repayment amount

-

Processing charges

-

Late-payment penalties

-

Interest accumulation

-

Loan tenure impact

For example, a borrower may choose a longer repayment tenure to reduce monthly EMI pressure without realising that the overall repayment cost may become significantly higher over time.

Similarly, some first-time borrowers may not understand how missed EMIs can affect credit history and future borrowing eligibility.

Limited understanding of borrowing terms can lead to:

-

Overborrowing

-

Multiple active loans

-

Repayment delays

-

Debt pressure during income gaps

Challenge 3: Digital Finance and Fraud Risks

India’s rapid digital finance growth has also increased exposure to financial fraud and unsafe borrowing practices. Many first-time borrowers struggle to identify genuine lending platforms, secure digital practices, or suspicious financial behaviour online.

Common risks include:

-

Fake loan apps requesting upfront payments

-

Phishing links targeting banking credentials

-

Fraudulent customer-support calls

-

Unverified financial advice on social media

-

Unsafe sharing of Aadhaar, PAN, or OTP information

Borrowers with limited digital financial awareness may become more vulnerable to high-pressure borrowing decisions or fraudulent financial schemes.

This challenge has become more significant as instant digital borrowing becomes increasingly accessible through mobile platforms.

Challenge 4: Rural-Urban Awareness Gap

Financial literacy awareness remains uneven across different regions and income groups in India. Urban populations often have greater access to:

-

Financial education content

-

Digital banking services

-

Formal credit systems

-

Investment and budgeting tools

In many rural or underserved areas, access to verified financial guidance may still remain limited. This gap can affect how individuals understand:

-

Loan agreements

-

Repayment obligations

-

Banking procedures

-

Digital payment systems

-

Credit-related risks

As financial services become increasingly digital, unequal financial awareness may also widen the gap between access to credit and the ability to manage it responsibly.

Challenge 5: Dependence on Informal Advice and Online Misinformation

Many individuals still rely heavily on informal financial advice from friends, relatives, or social media content creators instead of verified financial sources. While some information may be helpful, unverified financial guidance can create unrealistic expectations around:

-

Easy borrowing

-

Credit usage

-

Loan repayment

-

Instant approvals

-

Investment returns

Social media trends and short-form financial content sometimes simplify complex financial concepts without explaining repayment risks or long-term financial consequences properly. This may encourage borrowers to make impulsive financial decisions without evaluating affordability or repayment capacity carefully.

Financial awareness gaps affect borrowing, savings, budgeting, and repayment behaviour across different income groups in India.

As digital financial access continues to grow, improving practical financial literacy may become increasingly important for making safer and more informed money decisions.

Read More: How to Achieve a Perfect 900 CIBIL Score?

How Poor Financial Literacy Affects Borrowers

Many borrowers enter loan agreements without fully understanding repayment terms, interest structures, or long-term borrowing obligations.

While digital borrowing has made access to credit faster and more convenient, limited financial awareness can make repayment management significantly more difficult later.

1. Borrowing Without Understanding Repayment Terms: One of the most common problems is accepting a loan based only on quick approval or low monthly EMI amounts without reviewing the complete repayment structure. Many borrowers may overlook:

-

Total repayment amount

-

Interest charges over time

-

Processing fees

-

Late-payment penalties

-

Loan tenure impact

Without understanding these details, borrowers may underestimate the actual financial commitment involved.

2. Missed EMIs and Repayment Pressure: Poor financial planning often leads to repayment difficulties during salary delays, income gaps, or unexpected expenses. Borrowers who do not budget properly for EMIs may struggle to manage multiple financial obligations together.

This can result in:

-

Missed EMI payments

-

Additional penalty charges

-

Increased debt pressure

-

Difficulty managing monthly expenses

Over time, repeated repayment issues may create long-term financial stress.

3. Negative Impact on Credit Score: Many first-time borrowers are unaware that delayed or missed repayments can affect their credit history. A poor credit score may reduce future access to:

-

Personal loans

-

Credit cards

-

Home loans

-

Better borrowing terms

For borrowers planning future financial goals, repayment discipline becomes extremely important.

4. Unnecessary or Excessive Borrowing: Limited financial literacy may also encourage borrowers to take multiple short-term loans without evaluating repayment affordability properly. Some borrowers rely on new credit to manage older repayment obligations, which can gradually increase financial pressure.

For example, a young salaried employee managing rent, bills, and existing EMIs may take additional short-term loans during temporary cash shortages without calculating future repayment obligations carefully. Once multiple repayment cycles overlap, managing monthly finances may become difficult.

5. Misunderstanding Total Borrowing Cost: Many borrowers focus only on the immediate availability of funds and ignore the total cost of borrowing. This includes:

-

Interest charges

-

Processing fees

-

Penalties for delayed payments

-

Extended repayment costs

Even smaller loans can become financially stressful when repayment planning is ignored.

Before taking any loan, borrowers should review repayment terms, total costs, and monthly affordability carefully.

Also Read: Personal Loan vs Cash Advance Cost Comparison: What You’ll Actually Pay

Common Financial Mistakes Young Indians Make

Financial mistakes are not always caused by low income. In many cases, they happen because borrowers make quick financial decisions without understanding repayment impact, long-term affordability, or borrowing costs properly.

As digital finance becomes more accessible, these mistakes are becoming increasingly common among young Indians.

|

Financial Mistake |

How It Affects Borrowers |

|

Borrowing without budgeting |

Monthly EMIs become difficult to manage alongside rent, bills, and daily expenses |

|

Ignoring hidden loan charges |

Processing fees, penalties, and interest increase the total repayment cost |

|

Missing EMI deadlines |

Delayed payments may lead to penalties and affect credit history |

|

Using multiple credit sources together |

Managing several repayment cycles can increase financial pressure |

|

Relying on unverified financial advice online |

Borrowers may make unrealistic or risky financial decisions |

How These Mistakes Affect Real Borrowers

A student purchasing gadgets through EMIs may underestimate monthly repayment commitments while managing education expenses. A salaried professional facing temporary cash shortages may rely on multiple short-term loans without reviewing future repayment obligations carefully.

Similarly, a self-employed borrower with irregular monthly income may delay repayments while continuing to depend on additional credit for operational expenses.

In many situations, the financial pressure builds gradually rather than immediately. Small repayment mistakes, when repeated over time, can affect budgeting, savings, and long-term financial stability.

Also Read: Personal Loan Prepayment Charges Guide: Save or Lose Money?

Practical Ways to Improve Financial Literacy in 2026

Improving financial literacy does not always require advanced financial knowledge. In many cases, small everyday financial habits can help individuals make better borrowing, budgeting, and repayment decisions over time.

Financial Habits That Can Help:

1. Track Monthly Expenses Regularly: Understanding where money is spent each month can help individuals manage expenses more effectively. Tracking spending patterns also makes it easier to identify unnecessary expenses and improve budgeting habits.

2. Understand Loan Terms Before Borrowing: Before accepting any loan, borrowers should carefully review:

-

Interest rates

-

Processing fees

-

Repayment tenure

-

EMI obligations

-

Penalty charges

This can help avoid confusion and unexpected repayment pressure later.

3. Learn Basic EMI and Interest Calculations: Understanding how EMIs and interest charges work can improve borrowing decisions significantly. Even basic awareness of repayment calculations may help borrowers compare loan options more realistically.

4. Build Emergency Savings Gradually: Unexpected expenses such as medical emergencies, travel costs, or temporary income gaps can affect monthly budgets quickly. Building emergency savings gradually may reduce dependence on urgent borrowing during financial stress.

5. Use Trusted Financial Sources for Guidance: Financial advice from verified banking, regulatory, or financial education sources is generally more reliable than unverified social media content or informal recommendations. Borrowers should avoid making financial decisions based only on viral online advice.

6. Review Repayment Affordability Before Applying for Credit: Borrowers should evaluate whether future EMIs fit comfortably within their monthly income and existing obligations. Borrowing only what matches repayment capacity can reduce long-term financial pressure.

Small financial habits can improve long-term borrowing and repayment decisions over time.

Also Read: Payday Loans vs Personal Loans in India: Borrow Smartly in 2026

Why Financial Awareness Matters Before Borrowing

Many borrowing mistakes happen before the loan is even approved. Borrowers often focus on how quickly funds are available without evaluating whether the repayment structure is actually manageable in the long run.

Financial awareness helps individuals make borrowing decisions based on affordability rather than urgency alone.

A financially aware borrower is more likely to:

-

Compare total repayment costs instead of checking only EMI amounts

-

Borrow only what is actually required

-

Understand interest and processing charges clearly

-

Plan repayments around monthly income and existing expenses

-

Avoid unnecessary debt pressure later

A Simple Borrowing Checklist

Before applying for any loan, borrowers should ask themselves:

-

Can the monthly EMI fit comfortably within current income?

-

Have all interest and processing charges been reviewed?

-

What will the total repayment amount become over time?

-

Is the loan amount actually necessary?

-

Will future expenses affect repayment ability later?

For example, a salaried borrower facing a temporary expense may avoid unnecessary financial stress by selecting a smaller loan amount that matches repayment affordability instead of borrowing the maximum amount available.

For short-term financial needs, borrowers should review repayment terms carefully before choosing any credit option.

A Structured Way to Manage Short-Term Borrowing with Pocketly

Temporary financial gaps can affect anyone, including students managing education expenses, salaried professionals handling month-end shortages, or self-employed individuals facing irregular cash flow. In such situations, structured short-term borrowing may help manage urgent expenses more responsibly instead of relying on unplanned credit decisions.

Pocketly is a digital lending platform and not an NBFC. It works with RBI-registered NBFC partners to provide short-term borrowing options for eligible borrowers in India.

Pocketly supports borrowers looking for:

-

Short-term credit for temporary expenses

-

Emergency liquidity during cash shortages

-

Structured repayment-based borrowing

-

A fully digital borrowing process

Key Features of Pocketly

|

Feature |

Details |

|

Loan amount range |

₹1,000–₹25,000 |

|

Interest rate |

Starting from 2% per month |

|

Processing fee |

Between 1% and 8% |

|

KYC process |

Fully digital |

|

Collateral requirement |

No collateral required |

|

Disbursal |

Direct bank transfer for eligible borrowers |

|

Application process |

Completely digital |

Borrowers may use short-term credit for situations such as:

-

Utility bill payments

-

Emergency travel expenses

-

Temporary rent gaps

-

Medical costs

-

Short-term cash shortages

How the Application Process Works

-

Download the app or visit the website.

-

Complete the digital KYC process.

-

Select the required loan amount.

-

Review repayment terms carefully.

-

Receive approval and disbursal for eligible applications.

If you need a small amount for an urgent expense, you can check your eligibility on Pocketly in a few minutes.

Before taking any short-term loan, borrowers should borrow only what they actually need, review repayment affordability carefully, and understand the total repayment cost before making a borrowing decision.

If you need a small amount for an urgent expense during a temporary cash flow gap, you can check your eligibility on Pocketly in a few minutes. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

Frequently Asked Questions (FAQs)

1. Why is financial literacy important in India?

Financial literacy helps individuals understand how to manage money responsibly, including budgeting, savings, borrowing, and repayment planning. As digital finance and short-term credit become more accessible in India, financial awareness also helps borrowers avoid repayment mistakes and make informed financial decisions.

2. What are the biggest financial literacy challenges in India?

Some major challenges include limited financial education in schools and colleges, poor understanding of loans and EMIs, digital fraud risks, dependence on informal financial advice, and unequal access to financial awareness across different regions and income groups.

3. How does poor financial literacy affect borrowers?

Limited financial awareness may lead borrowers to misunderstand repayment terms, ignore loan charges, miss EMIs, or borrow beyond their repayment capacity. Over time, this can increase financial stress and affect overall money management.

4. Why should borrowers understand loan terms before applying?

Reviewing loan terms carefully helps borrowers understand interest charges, processing fees, repayment timelines, and the total borrowing cost before accepting credit. This can reduce confusion and help avoid unexpected repayment pressure later.

5. How can young Indians improve financial literacy?

Young Indians can improve financial literacy by tracking monthly expenses, learning basic EMI and interest calculations, following trusted financial sources, and reviewing repayment affordability before borrowing. Small financial habits can improve long-term money management decisions over time.