A yearly bonus, freelance payment, or unexpected cash inflow can make early loan closure feel tempting. India’s digital personal loan market crossed ₹1.39 lakh crore in FY25–26, showing how many borrowers now rely on short-term credit for urgent expenses.

Many borrowers start wondering whether paying off a personal loan early could reduce interest costs and monthly repayment pressure. But closing a loan before the tenure ends is not always straightforward. Some lenders apply foreclosure charges, lock-in periods, or additional conditions before approving early closure. Missing important steps can also create issues with your loan records or credit history later.

Understanding how to close a personal loan early helps you avoid unnecessary costs and complete the process correctly. This guide explains the steps, charges, documents, and common mistakes borrowers in India should know before foreclosing a personal loan.

Key Takeaways

-

Closing a personal loan early can help reduce future interest costs and lower monthly EMI pressure.

-

Foreclosure charges, GST, lock-in periods, and lender-specific rules can affect the total closure cost.

-

The foreclosure process usually includes checking the loan agreement, requesting a foreclosure statement, making a payment, and collecting the NOC.

-

Borrowers should verify that the loan status is updated as “closed” in their credit report after repayment.

-

Pocketly supports short-term borrowing needs with digital personal loans ranging from ₹1,000 to ₹25,000 for eligible borrowers.

What Does Closing a Personal Loan Early Mean?

Closing a personal loan early means repaying the remaining loan amount before the original tenure ends. Lenders usually call this loan foreclosure or pre-closure. Instead of continuing monthly EMIs for the full tenure, the borrower clears the outstanding balance in one payment.

Many salaried professionals choose early closure after receiving a bonus, incentive payout, or additional income. Some borrowers also prefer foreclosure to reduce long-term interest costs and free up monthly cash flow.

However, foreclosure is different from regular loan closure. In a regular closure, the loan ends after all scheduled EMIs are paid during the agreed tenure. In foreclosure, the borrower requests to close the loan before the final EMI date.

Some lenders may apply foreclosure charges, minimum repayment conditions, or lock-in periods before allowing early closure. Checking these terms before making payment helps avoid unexpected costs later.

When Does Closing a Personal Loan Early Make Sense?

A long repayment tenure can increase your total interest payout, especially when monthly EMIs continue alongside rent, bills, or other financial commitments. Many borrowers start feeling this pressure after taking multiple short-term loans or handling sudden expenses.

Continuing the loan for the full tenure may reduce monthly flexibility and increase the overall borrowing cost. In some cases, borrowers end up paying significantly more interest than expected because the outstanding balance remains active for longer.

Closing the loan early can make sense if you have extra funds available and the interest savings are higher than the foreclosure charges. Before making a decision, check:

-

Remaining loan balance

-

Foreclosure or pre-closure charges

-

Lock-in period conditions

-

Total interest saved after closure

For example, a salaried employee receiving an annual bonus may use part of that amount to clear the remaining loan balance early. If the remaining interest cost is higher than the foreclosure fee, early closure could help reduce the total repayment burden.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

How to Close a Personal Loan Early in India

Closing a personal loan early involves more than simply paying the remaining balance. Most lenders follow a formal foreclosure process, and missing a step can create problems later with pending dues, loan records, or credit report updates.

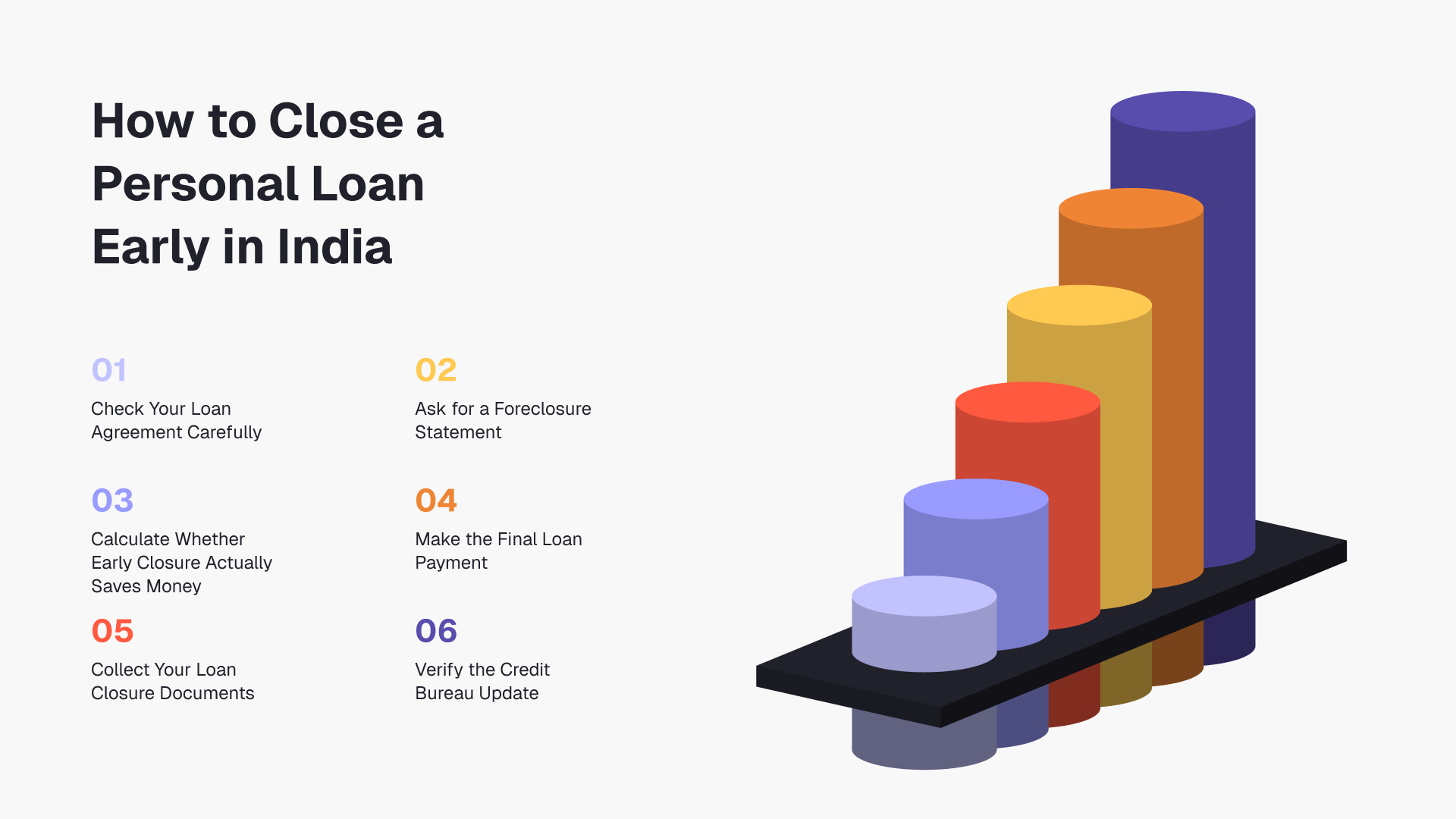

1. Check Your Loan Agreement Carefully

Start by reviewing the original loan agreement before making any payment decision. Many borrowers skip this step and later discover additional foreclosure costs or repayment restrictions.

Check for:

-

Lock-in period conditions

-

Foreclosure or pre-closure charges

-

Minimum EMI repayment requirements

-

Part-payment restrictions

-

Notice period requirements

Some lenders do not allow early closure during the first few months of the loan tenure. Others may charge a percentage of the outstanding balance as a foreclosure fee. Understanding these conditions first helps you avoid unexpected costs.

2. Ask for a Foreclosure Statement

Contact your lender and request a foreclosure or pre-closure statement. This document gives the exact amount required to close the loan completely.

The statement usually includes:

-

Remaining principal amount

-

Pending interest amount

-

Foreclosure charges

-

GST on applicable fees

-

Total final settlement amount

-

Validity period of the statement

Always check the validity date carefully. If the payment is delayed beyond that period, the lender may generate a revised amount with additional interest charges.

3. Calculate Whether Early Closure Actually Saves Money

Many borrowers assume foreclosure automatically reduces costs. However, this may not always happen if the lender applies high foreclosure charges.

Before making payment, compare:

-

Total remaining interest payable

-

Foreclosure fee

-

Any additional taxes or charges

-

Impact on your monthly cash flow

For example, a salaried employee receiving an annual bonus may decide to close the remaining loan balance early. If the interest savings are higher than the foreclosure charges, early closure could reduce the overall repayment burden.

4. Make the Final Loan Payment

After confirming the final payable amount, complete the payment using the lender’s approved method. Depending on the lender, this may include:

-

Net banking

-

UPI transfer

-

Mobile banking app

-

Debit card payment

-

Branch payment

Keep copies of:

-

Payment receipts

-

Transaction IDs

-

Bank confirmation messages

-

Final settlement acknowledgement

These records can help if disputes arise later regarding pending dues or incorrect closure status.

5. Collect Your Loan Closure Documents

Many borrowers make the payment but forget to collect official closure documents. This can create issues later during credit verification or future loan applications.

After repayment, ask the lender for:

-

No Objection Certificate (NOC)

-

Loan closure letter

-

Final account statement

-

Payment acknowledgement receipt

Check that your name, loan account number, and closure date are correct on all documents before storing them safely.

6. Verify the Credit Bureau Update

Lenders usually report loan closure details to credit bureaus after settlement. This process may take a few weeks.

Check your credit report later to confirm the loan status shows:

-

“Closed”

-

“Paid”

-

“Settled” should NOT appear unless applicable

An incorrect update can affect future loan approvals or credit score assessments. If the loan still appears active after a reasonable period, contact the lender and raise a correction request immediately.

Read More: How to Achieve a Perfect 900 CIBIL Score?

What Charges Apply When You Close a Loan Early?

Closing a personal loan early can reduce future interest costs, but lenders may still apply certain charges before approving foreclosure. These costs vary across lenders and loan agreements, so checking the terms carefully before making payment is important.

Foreclosure or Pre-Closure Charges

Many lenders charge a foreclosure fee when borrowers close the loan before the agreed tenure ends. This fee is usually calculated as a percentage of the outstanding loan amount.

The exact charge depends on:

-

Loan type

-

Remaining tenure

-

Repayment history

-

Lender policy

Some lenders may also allow foreclosure only after a minimum number of EMIs are paid.

GST on Applicable Fees

GST is usually charged on foreclosure fees and other service-related charges. Borrowers sometimes calculate only the foreclosure amount and overlook the additional tax component.

Before making payment, ask the lender for:

-

Base foreclosure charge

-

Applicable GST amount

-

Total final settlement value

This helps avoid payment shortfalls during closure.

Lock-In Period Conditions

Certain lenders apply a lock-in period during which early loan closure is not allowed. This period often ranges across the initial months of the loan tenure.

If a borrower requests foreclosure during the lock-in period:

-

The request may be rejected

-

Additional charges may apply

-

Minimum EMI conditions may still remain active

Checking the lock-in clause early helps avoid unnecessary repayment planning issues.

Lender-Specific Foreclosure Rules

Every lender follows different foreclosure policies. Some may allow:

-

Online foreclosure requests

-

Partial prepayments before full closure

-

Zero foreclosure charges after a specific tenure

Others may require branch visits, written requests, or additional verification before processing closure.

Before proceeding, always confirm:

-

Total payable amount

-

Closure eligibility

-

Processing timeline

-

Required documents

-

Payment method accepted by the lender

If the charges appear too high, compare the total savings before deciding whether early closure makes financial sense.

Also Read: Personal Loan vs Cash Advance Cost Comparison: What You’ll Actually Pay

Which Documents Are Required for Personal Loan Closure?

Keeping the correct documents ready can help avoid delays during the foreclosure process. Some lenders may request additional verification before approving early loan closure, especially for online applications or digital loans.

Here are the common documents borrowers usually need during personal loan closure:

-

Loan account number or loan agreement copy

-

Registered mobile number linked to the loan account

-

PAN card or another valid identity proof

-

Bank account details used for EMI payments

-

Latest loan statement or repayment schedule

-

Foreclosure statement provided by the lender

-

Final payment transaction receipt

-

Written foreclosure request form, if required by the lender

After the payment is completed, borrowers should also collect these important closure documents from the lender:

-

No Objection Certificate (NOC)

-

Loan closure certificate

-

Final account statement showing zero outstanding balance

-

Payment acknowledgement receipt

Before leaving the branch or closing the request online, verify that:

-

Your name is correct

-

Loan account details match

-

The closure date is accurate

-

The outstanding balance shows zero

Keeping both digital and physical copies of these documents can help during future credit checks, disputes, or loan applications.

Also Read: Personal Loan Prepayment Charges Guide: Save or Lose Money?

How Early Closure Can Affect Your Credit Score

Closing a personal loan early can affect your credit score in different ways depending on your repayment history, overall credit profile, and how the lender reports the closure. The impact is usually not immediate or identical for every borrower.

One positive effect of early closure is a lower debt obligation. Paying off an active loan reduces your outstanding liability and may improve your credit profile over time. Consistent repayment before foreclosure also shows responsible credit behaviour.

Early closure can also improve your debt-to-income ratio, which lenders often review during future loan applications. Borrowers managing multiple EMIs may benefit from reduced repayment pressure after closure.

However, temporary score fluctuations are also possible in some cases. Closing a loan account early may slightly reduce the length or mix of active credit accounts in your profile. This impact is usually minor, but it can appear temporarily in certain credit reports.

The larger risk comes from incorrect reporting. If the lender updates the account as “settled” instead of “closed,” it may negatively affect future loan approvals. A settled status usually indicates the borrower paid less than the agreed amount.

After foreclosure, always check your credit report to confirm:

-

Loan status shows “closed”

-

Outstanding balance is zero

-

EMI dues are cleared

-

No delayed payment remarks appear

If the report contains errors, raise a correction request with the lender immediately.

Also Read: Payday Loans vs Personal Loans in India: Borrow Smartly in 2026

Mistakes to Avoid Before Foreclosing a Loan

Closing a personal loan early can reduce future interest costs, but rushing the process without proper checks may create new financial problems later. Many borrowers focus only on clearing the loan quickly and overlook important details during foreclosure.

Using Emergency Savings for Loan Closure

Some borrowers use their entire emergency fund to close a loan early. While this may reduce EMI pressure, it can create financial stress later if unexpected expenses arise.

Before using savings for foreclosure, check whether you still have enough funds available for:

-

Medical emergencies

-

Rent or utility payments

-

Insurance premiums

-

Temporary income gaps

Maintaining some financial cushion is important even after the loan closes.

Ignoring Foreclosure Penalties and Charges

Many borrowers calculate only the remaining principal amount and ignore additional foreclosure costs. This can reduce the actual savings from early closure.

Always check:

-

Foreclosure fee

-

GST on charges

-

Pending interest amount

-

Lock-in conditions

-

Other lender-specific fees

Comparing the total savings against these charges helps you make a better repayment decision.

Forgetting to Collect the NOC

Paying the final amount alone does not complete the closure process. Some borrowers forget to collect the No Objection Certificate (NOC) after repayment.

Without proper closure documents, future issues may arise during:

-

Credit verification

-

Loan applications

-

Dispute resolution

-

Balance confirmation checks

Always collect:

-

NOC

-

Loan closure letter

-

Final account statement

-

Payment acknowledgement

Store both physical and digital copies safely.

Not Checking the Loan Closure Status

Some lenders take time to update closure details with credit bureaus. Borrowers who do not verify the update may later discover the loan still appears active in their credit report.

After foreclosure, check your credit report to confirm:

-

Loan status shows “closed”

-

Outstanding balance is zero

-

No overdue amount appears

-

“Settled” status is not incorrectly marked

If any mismatch appears, contact the lender immediately and request a correction.

A Structured Way to Manage Short-Term Borrowing Needs with Pocketly

Closing a personal loan early can reduce future EMI pressure, but it may also temporarily affect your monthly cash flow if most savings go toward foreclosure. Many borrowers later face smaller urgent expenses such as rent gaps, utility bills, medical costs, or travel payments before the next salary cycle arrives.

This is where structured short-term borrowing can help. Instead of relying on informal borrowing or high-value long-term credit, smaller loan amounts with transparent repayment terms may help manage temporary financial gaps more comfortably.

Pocketly is a digital lending platform working with RBI-registered NBFCs. It is designed for young Indians looking for short-term personal loans between ₹1,000 and ₹25,000 for urgent expenses and temporary cash shortages.

Here’s how Pocketly supports short-term borrowing in a more structured way:

-

Borrow based on your requirement: Loan amounts range from ₹1,000 to ₹25,000, depending on profile and eligibility.

-

No collateral needed: Borrowers can apply without pledging assets or arranging a guarantor.

-

Quick digital process: The application and verification process is completed digitally through KYC verification.

-

Direct bank transfer: Approved funds are transferred directly to the borrower’s bank account.

-

Flexible repayment structure: Repayment options are designed around short-term borrowing requirements.

-

Transparent pricing structure: Interest rates start from 2% per month, with processing fees ranging between 1% and 8%.

-

Fully digital access: Borrowers can manage the process online without extensive paperwork.

How to Apply

-

Download the Pocketly app or visit the website.

-

Complete the digital KYC process.

-

Select the required loan amount.

-

Review the loan details shown upfront.

-

Receive approval and disbursal for eligible applications.

What to Check Before Taking Any Short-Term Loan

Before applying for any short-term loan, review:

-

Total repayment amount

-

Interest and processing charges

-

Repayment timeline

-

Monthly affordability

-

Actual borrowing requirement

Borrowing only what fits your repayment capacity can help reduce financial pressure later.

If you need a small amount for an urgent expense, you can check your eligibility on Pocketly in a few minutes. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

Frequently Asked Questions (FAQs)

1. Can I close my personal loan within 6 months?

Some lenders allow personal loan foreclosure within six months, while others apply a lock-in period before early closure is permitted. The conditions depend on the lender’s policy and loan agreement terms. Before making a payment, check whether any foreclosure charges or minimum EMI requirements apply.

2. What is the difference between prepayment and foreclosure?

Prepayment means paying a portion of the outstanding loan amount while continuing the remaining EMIs. Foreclosure means repaying the entire outstanding balance and closing the loan account before the tenure ends.

3. Does early closure improve your credit score?

Early loan closure may help reduce overall debt obligations and improve repayment behaviour over time. However, the impact varies across borrowers and credit profiles. After foreclosure, borrowers should check their credit report to confirm the loan status appears as “closed” instead of “settled.”

4. Are foreclosure charges mandatory for personal loans?

Not always. Some lenders apply foreclosure or pre-closure charges, while others may waive them after a certain repayment period. The charges usually depend on lender policy, remaining tenure, and loan type. GST may also apply on certain foreclosure fees.

5. What happens if I do not collect the NOC after loan closure?

Failing to collect the No Objection Certificate (NOC) can create problems during future loan applications or credit verification checks. The NOC acts as proof that the loan has been fully repaid and no dues remain pending with the lender.

6. Can I close a personal loan online?

Some lenders allow borrowers to complete the foreclosure process online through mobile apps, internet banking, or customer portals. Others may require branch visits or written closure requests before processing the final settlement. Always confirm the lender’s process before initiating payment.