An urgent expense can show up at the worst moment, especially when your bank balance refuses to cooperate. In that moment, people start searching for financial institutions that allow quick cash access through credit cards. The goal is simple: find immediate money without dealing with lengthy loan approvals or complicated paperwork.

Many credit cards quietly include an option that allows cardholders to withdraw cash instead of making purchases. It sounds straightforward, especially when a sudden repair, medical bill, or travel expense demands attention immediately. Yet most borrowers only discover the real costs after the withdrawal appears on their statement.

Understanding how this feature works before using it can save unnecessary fees and prevent unpleasant surprises later. A closer look at how these withdrawals function helps you decide whether it is truly the right move.

Key Takeaways

-

Cash advances let you withdraw cash directly from your credit card, typically limited to 20–40% of your total credit limit, through ATMs, bank tellers, convenience cheques, or online transfers.

-

The cost structure includes multiple charges, such as a 2.5–3% cash advance fee, higher interest rates of around 2.5–3.5% per month, and possible ATM network withdrawal fees.

-

Interest begins accumulating immediately without a grace period, meaning even a $1,000 withdrawal could start at about $1,053–$1,055 before interest continues adding up.

-

Carefully reviewing limits, fees, and repayment rules helps avoid expensive borrowing, especially when cash advances are used for urgent short-term expenses.

What Is a Cash Advance?

A cash advance is a way to withdraw cash using your credit card instead of using it for purchases. Unlike regular transactions, this feature lets you access part of your credit limit as physical cash through an ATM or a bank teller. Many people turn to this option when they need money immediately and start looking for banks that allow credit card cash advances without lengthy loan approvals.

To understand this option better, it helps to look at the key characteristics that define how a credit card cash advance works.

-

It allows you to withdraw cash against your available credit limit rather than making a purchase.

-

Interest usually starts accumulating immediately, unlike regular credit card purchases that often include a grace period.

-

Cash advances typically come with a separate cash advance limit, which is lower than your total credit card limit.

-

Banks may charge a cash advance fee, often calculated as a small percentage of the withdrawn amount.

How Does a Cash Advance Work?

Accessing cash from a credit card follows a specific process, and understanding it beforehand prevents expensive surprises later.

To see how banks actually release this money, here are the most common ways people access a credit card cash advance.

1. ATM Cash Withdrawal

Using an ATM remains the quickest method when someone needs physical cash without waiting for bank assistance.

-

Insert your credit card into the ATM and enter the PIN linked to your card account.

-

Choose the withdrawal option and enter an amount within your cash advance limit.

-

The ATM dispenses the cash immediately while the transaction appears on your card balance.

-

This withdrawal is recorded separately from purchases because banks classify it as a cash advance transaction.

2. Bank Teller Withdrawal

Some borrowers prefer requesting the withdrawal directly at a bank counter, especially when ATM withdrawal limits become restrictive.

-

Visit a bank branch supporting your card network and present identification with the credit card.

-

Ask the teller to process a credit card cash advance withdrawal for the required amount.

-

The teller verifies the card and releases the funds once the transaction receives approval.

-

The amount is added to the card balance and may include a cash advance processing fee.

3. Convenience Checks Issued by Credit Card Providers

Certain card issuers send convenience cheques that allow cardholders to convert part of their credit line into cash.

-

Write the cheque to yourself or another recipient and deposit it like a normal bank cheque.

-

Once processed, the amount is deducted from your available cash advance credit limit.

-

Banks treat the transaction as a credit card cash advance, meaning fees and interest rules apply.

-

Interest normally begins accruing immediately after the cheque clears through the banking system.

4. Online Transfer to a Bank Account

Some banks allow cardholders to move funds directly from their credit card into a bank account through digital banking.

-

Log in to the bank’s mobile application or online banking portal connected to your credit card.

-

Select the option that allows transferring money from your cash advance balance to a bank account.

-

Enter the transfer amount within the permitted advance limit and confirm the transaction securely.

-

The funds are transferred to the chosen account while the amount appears as a cash advance transaction.

Also read: How to Manage Budget vs Expenses

The process becomes clearer once you know how withdrawals happen, but the next question many people ask is where this facility is actually available.

Where to Get a Cash Advance in 2026: Banks and Options

Cash advances are typically offered through credit cards issued by banks, but access points can vary depending on the provider and card network.

To understand where you can actually access this facility in India, here are the most common institutions and channels that allow a credit card cash advance.

Banks That Allow Cash Advances

-

HDFC Bank: Most HDFC credit cards allow cash withdrawals through ATMs within a predefined cash advance limit, usually a percentage of the card’s credit limit.

-

ICICI Bank: ICICI credit cards support ATM withdrawals as cash advances, though the bank applies a cash advance fee and immediate interest charges.

-

SBI Card: SBI credit cards allow cardholders to withdraw cash from ATMs across India under their approved credit card cash advance limit.

-

Axis Bank: Axis credit card users can withdraw cash from ATMs worldwide, provided the card has an active PIN and an available advance limit.

-

Kotak Mahindra Bank: Kotak credit cards also permit ATM cash withdrawals against available credit, though banks generally advise using this option cautiously due to higher costs.

-

American Express India: Certain American Express cards allow cash advances through designated ATMs, although access may depend on card eligibility and activation.

Availability is only part of the story, because banks also set clear boundaries on how much money can be withdrawn through this feature.

Cash Advance Limits: How Much Can You Withdraw?

The amount you can withdraw through a cash advance is restricted by a separate limit set by the card issuer.

To understand how much cash you can realistically access from a credit card, here are the key factors banks use to determine the cash advance limit.

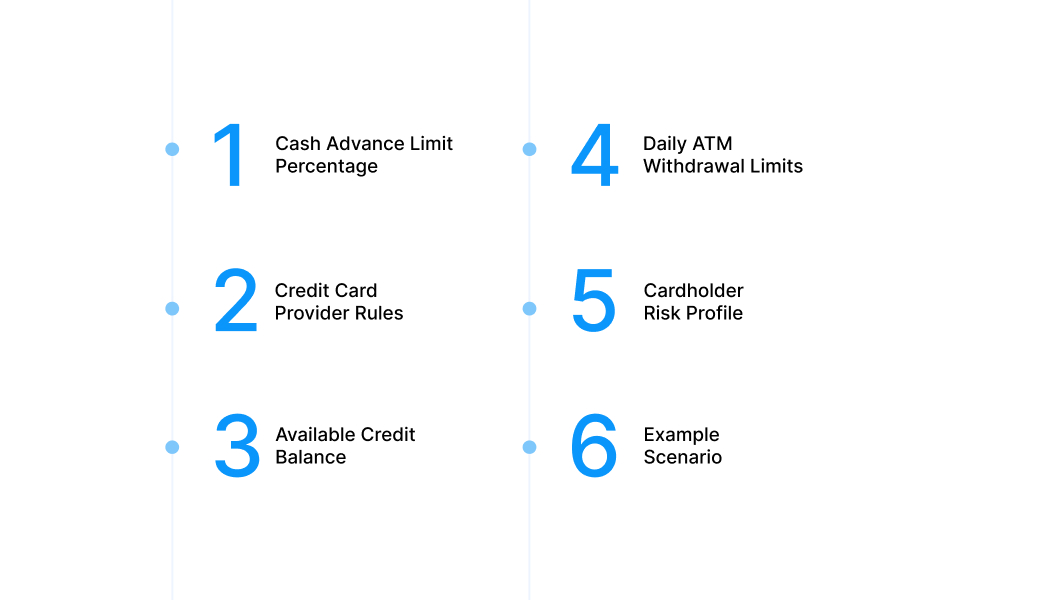

-

Cash Advance Limit Percentage: Most Indian credit card issuers allow withdrawals between 20% and 40% of the total credit limit, depending on the card profile.

-

Credit Card Provider Rules: Banks such as HDFC Bank, ICICI Bank, Axis Bank, and SBI Card assign a specific advance limit visible in the card statement or mobile banking application.

-

Available Credit Balance: Even if the approved advance limit is higher, the actual withdrawal cannot exceed the remaining available credit on the card.

-

Daily ATM Withdrawal Limits: Some banks impose daily ATM withdrawal caps, which may restrict how much can be withdrawn in a single day.

-

Cardholder Risk Profile: Banks may adjust the cash advance limit based on repayment history, credit score, and card usage behaviour.

-

Example Scenario: If a credit card has a ₹1,00,000 limit and the bank sets a 30% advance cap, the maximum withdrawable cash would be ₹30,000.

Also read: Get Debt Consolidation Loan Online: How It Works

Understanding withdrawal limits is useful, yet the real impact appears when the associated charges start adding up.

Fees and Costs of Cash Advances in 2026

Cash advances often appear convenient at first, but the real cost becomes clear once the associated fees and interest begin accumulating.

To understand why this borrowing option can quickly become expensive, here are the major cost components attached to a credit card cash advance.

1. Cash Advance Fee

Banks charge a cash advance fee every time cash is withdrawn using a credit card through an ATM or bank teller. In India, this fee generally ranges between 2.5% and 3% of the withdrawn amount, often with a minimum charge between ₹250 and ₹500, depending on the bank. The fee is added instantly to the cardholder’s balance, meaning the borrower starts repaying a higher amount from the first billing cycle.

2. Higher APR

Cash advances usually attract a higher interest rate compared with regular credit card purchases. Interest typically begins accruing from the date of the withdrawal itself, because cash advances normally do not include an interest-free grace period. Many Indian banks charge monthly finance rates of around 2.5% to 3.5%, which can significantly increase the repayment amount if the balance remains unpaid.

3. ATM Withdrawal Fees

ATM operators may apply an additional withdrawal charge when a cash advance is taken from an ATM, especially if it belongs to another bank network. These fees can range around ₹20–₹25 per transaction at other-bank ATMs, and international withdrawals may also include foreign currency conversion charges. When combined with the advance fee and interest charges, the total cost of accessing cash through a credit card can increase considerably.

Regulatory note: In India, the Reserve Bank of India (RBI) requires banks and card issuers to clearly disclose interest rates and all charges related to credit card transactions, including cash advance fees and finance charges.

Numbers often explain things better than theory, so a quick example helps show how these charges combine in a real situation.

Example: How Much a Cash Advance Can Actually Cost

Seeing a simple scenario helps explain how quickly the cost of a credit card cash advance can build.

To make the impact clearer, consider how the charges accumulate in a typical withdrawal situation.

-

Cash Withdrawn: $1,000 taken as a credit card cash advance from an ATM during an urgent expense.

-

Cash Advance Fee: The bank applies a 5% advance fee, adding $50 immediately to the card balance.

-

ATM Withdrawal Fee: The ATM operator may charge an additional $3–$5 usage fee, depending on the network.

-

Interest Starts Immediately: Interest begins accruing from the withdrawal date because cash advances normally do not include a grace period.

-

Total Initial Balance: Before interest grows further, the cardholder already owes about $1,053–$1,055 on a $1,000 withdrawal.

-

Real Cost Over Time: If repayment takes several weeks, the combined effect of interest and fees increases the final repayment amount further.

Also Read: What is Debt Trap and How to Avoid It?

Seeing the numbers makes the costs clearer, but it also helps to weigh the practical benefits and drawbacks before deciding to use one.

Pros and Cons of Credit Card Cash Advances You Should Know

A credit card cash advance can provide quick access to funds, but the convenience often comes with notable trade-offs.

To evaluate whether this option fits your situation, here are the key advantages and drawbacks borrowers should understand.

1. Advantages of Credit Card Cash Advances

-

Immediate Access to Cash: Cardholders can withdraw money instantly from ATMs or bank branches without waiting for loan approvals.

-

No Separate Loan Application: The facility is already linked to the credit card, so no additional documentation or verification is required.

-

Useful for Short-Term Emergencies: Cash advances can help manage urgent expenses such as medical bills, repairs, or unexpected travel costs.

-

Wide ATM Availability: Most credit card networks allow withdrawals from ATMs across India and internationally.

2. Drawbacks of Credit Card Cash Advances

-

High Interest Rates: Cash advances typically attract higher interest rates compared with regular credit card purchases.

-

No Interest-Free Grace Period: Interest generally starts accruing from the transaction date rather than the billing cycle.

-

Additional Transaction Fees: Banks charge a cash advance fee, and ATM operators may apply additional withdrawal charges.

-

Lower Cash Advance Limits: The amount available for withdrawal is usually only a portion of the total credit card limit.

Also Read: Features and Types of Long-Term Personal Loans

Once the advantages and downsides are clear, the next piece of the puzzle is understanding how repayment actually works.

How Repayment Works After a Cash Advance?

Repayment begins the moment the transaction posts to your credit card account, unlike regular purchases that often include a billing grace period.

To understand how repayment actually affects your outstanding balance, here are the key details borrowers should know.

-

The withdrawn amount appears separately on your statement as a cash advance balance, not as a normal purchase entry.

-

Most banks apply a cash advance fee immediately, typically calculated as a small percentage of the withdrawn amount.

-

Interest usually starts accruing from the transaction date, since credit card cash advances rarely include a grace period.

-

Any payment made towards the card balance first covers fees and interest before reducing the cash advance principal amount.

-

Clearing the advance early can significantly reduce the interest charges that accumulate on the outstanding balance.

Repayment rules explain the financial side, but it is also worth comparing this option with other ways of borrowing money.

Cash Advance vs Other Borrowing Options

Different borrowing options offer varying levels of speed, cost, and flexibility, making it important to understand how they compare.

To see how a credit card cash advance stacks up against other ways of borrowing money, here is a clear comparison.

|

Borrowing Option |

Approval Speed |

Typical Cost |

Loan Amount |

Repayment Flexibility |

Best Used For |

|

Credit Card Cash Advance |

Instant |

High interest + advance fee |

Limited to an advance limit |

Short repayment window |

Urgent short-term cash |

|

Personal Loan |

Moderate approval time |

Lower than credit card interest |

Higher loan amounts |

Planned larger expenses |

|

|

Payday Loan |

Very fast approval |

Extremely high charges |

Small amounts |

Very short tenure |

Emergency borrowing |

|

Salary Advance Apps |

Quick approval |

Moderate service fee |

Small amounts |

Next salary cycle |

Temporary cash gaps |

|

Instant Loan Apps |

Fast digital approval |

Medium to high interest |

Small to medium |

Flexible tenure options |

Short-term financial needs |

Looking at these alternatives often raises a simple question about whether there is a more straightforward way to handle short-term cash needs.

Need Quick Cash Without the Credit Card Headache? Meet Pocketly

Sometimes the problem is not access to credit, but finding a simpler option that avoids high cash advance fees and interest charges.

If a cash advance feels expensive or complicated, here is why many borrowers prefer trying Pocketly instead.

-

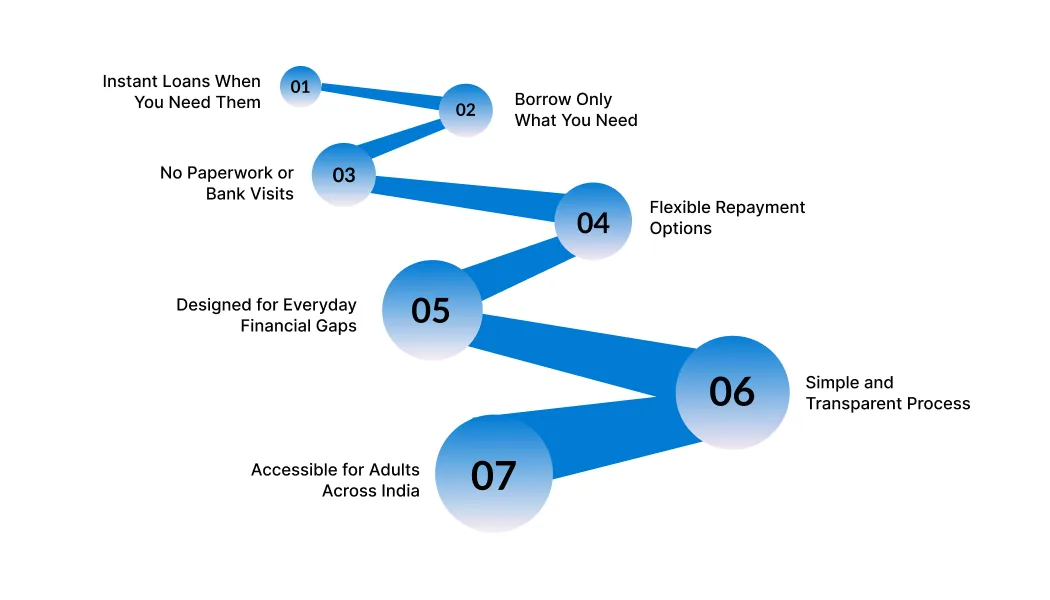

Instant Loans When You Actually Need Them: Apply directly through the Pocketly mobile app and receive funds in minutes once your KYC is approved.

-

Borrow Only What You Need: Pocketly offers small personal loans ranging roughly from ₹1,000 to ₹25,000, which helps cover urgent expenses without taking a large loan.

-

No Paperwork or Bank Visits: The entire process happens online, including identity verification and application submission.

-

Flexible Repayment Options: Borrowers can repay within 60 to 180 days, making it easier to manage short-term financial gaps.

-

Designed for Everyday Financial Gaps: Pocketly is built to help people handle small but urgent needs such as bills, travel expenses, or unexpected costs.

-

Simple and Transparent Process: The platform focuses on fast approvals, minimal documentation, and clear loan terms.

-

Accessible for Adults Across India: Any Indian resident aged 18 or above with a bank account can apply through the app.

When cash is urgently needed, the smartest move is choosing a solution that feels simple, transparent, and quick to access. Pocketly keeps things straightforward so you can focus less on paperwork and more on solving the financial situation in front of you.

Download the Pocketly app on Android or iOS today and get quick access to funds whenever life throws an unexpected expense your way.

FAQs

1. Is taking a cash advance bad for your credit score?

A cash advance itself does not directly damage your credit score, but it increases your credit utilisation ratio. Higher utilisation can affect your score if the balance remains unpaid for a long time.

2. Can you take a cash advance without a PIN?

Most ATM cash advances require a credit card PIN. Without a PIN, the withdrawal usually has to be completed through a bank teller or authorised branch.

3. How long does a cash advance take to appear on a credit card statement?

A cash advance typically appears on the credit card account almost immediately after the withdrawal. The transaction is then reflected in the next billing statement along with the associated charges.

4. Can you pay off a cash advance immediately?

Yes, you can repay a cash advance as soon as the transaction posts to your credit card account. Early repayment helps reduce the interest that begins accruing from the withdrawal date.

5. Do all credit cards allow cash advances?

Not every credit card automatically enables this feature. Banks may restrict cash advances depending on the card type, user eligibility, or risk assessment.

6. Is there a daily limit on cash advance withdrawals?

Yes, many banks impose daily ATM withdrawal limits for credit card cash advances. This limit works alongside the overall cash advance limit assigned to the card.