You need money urgently. The rent is due, a bill just hit your inbox, or an unexpected expense refuses to wait. In that moment, two options seem equally simple: fast cash or cash withdrawal. Both give you instant access to funds. Both look like quick fixes.

The real problem begins after the transaction. A credit card cash withdrawal can start charging high interest immediately. A fast cash loan may feel structured, but it comes with its own costs and repayment commitments. Without understanding the difference, you could end up paying far more than you expected.

The solution is not avoiding short-term funding altogether. It is knowing exactly how each option works before you choose. In this blog, we break down fast cash vs. cash withdrawal clearly so you can decide based on cost, speed, and long-term impact rather than urgency.

TL;DR

- Fast cash vs cash withdrawal: Fast cash is a short-term loan with interest and fixed repayment; cash withdrawal uses your own funds or credit card limit.

- Cost comparison: Debit withdrawals are usually free, fast cash has interest and fees, and credit card cash advances are the most expensive.

- Best use cases: Fast cash suits urgent expenses when funds are low; cash withdrawals work when you have an available balance or need instant cash.

- Risks: Fast cash can affect a credit score and cause debt cycles; credit card withdrawals accrue high interest immediately.

- Smart borrowing tips: Check total repayment, avoid loans for lifestyle spending, repay early, and keep an emergency fund for financial safety.

What Is Fast Cash?

Fast cash is a short-term loan that gives you quick access to borrowed money, usually through a digital lending app. It is designed to help you handle urgent financial needs without long approval timelines.

Fast cash typically includes:

- Small loan amounts for short-term needs

- Quick online application through a mobile app

- Minimal documentation with basic KYC verification

- Fixed repayment tenure

- Interest charges and processing fees

Unlike withdrawing your own savings, fast cash involves borrowing from a lender. This means you are required to repay the amount within a specified period, along with applicable charges.

For many young professionals in India, fast cash is used to cover temporary shortfalls such as medical expenses, rent gaps, travel emergencies, or unexpected bills.

Note: Fast cash can be helpful when used responsibly, but understanding the total repayment amount before borrowing is essential to avoid unnecessary financial pressure.

What Is a Cash Withdrawal?

A cash withdrawal is when you take money out of your bank account or credit card using an ATM or bank branch. The source of funds determines how it works and how much it costs.

Cash withdrawal typically includes:

- Withdrawing your own money using a debit card

- Taking a cash advance from your credit card

- ATM daily withdrawal limits

- Possible transaction fees after free limits are exceeded

- Immediate access to physical cash

If you withdraw using a debit card, you are accessing your own bank balance. There is usually no interest involved, though some banks may charge fees after a certain number of free ATM transactions.

If you withdraw using a credit card, it is treated as a cash advance. Interest starts accruing immediately, often at a higher rate than regular credit card purchases. Additional cash advance fees may also apply.

Note: Debit withdrawals are generally cost-effective if you have funds available, while credit card cash withdrawals can become expensive if not repaid quickly.

Fast Cash vs Cash Withdrawal: Key Differences at a Glance

At first glance, fast cash and cash withdrawal may seem similar because both give you immediate access to money. However, the source of funds, cost structure, repayment obligation, and impact on your credit profile are very different.

Understanding these differences helps you avoid unnecessary interest, hidden fees, and repayment stress. The comparison below breaks down the key factors side by side so you can quickly see which option suits your situation.

| Factor | Fast Cash | Debit Card Cash Withdrawal | Credit Card Cash Withdrawal |

| Source of Money | Borrowed from the lender | Your own bank balance | Borrowed from the credit limit |

| Interest Charges | Yes, as per the loan terms | No interest | High interest from day one |

| Processing Fees | May apply | Usually, none are within the free ATM limit | Cash advance fee applicable |

| Repayment Required | Yes, within fixed tenure | No repayment | Yes, plus interest |

| Approval Process | App-based approval required | Instant access | Instant access |

| Impact on Credit Score | Can affect the score if unpaid | No impact | May impact the utilisation ratio |

| Best Used When | No savings available, and structured repayment needed | You have sufficient balance | Last resort emergency with a quick repayment plan |

Also Read: Effective Debt Management Strategies and Tips

Risks You Should Consider Before Choosing

Both fast cash and cash withdrawals solve short-term liquidity problems. However, if used without planning, they can create longer-term financial pressure. Understanding the risks helps you make a decision based on control rather than urgency.

Both fast cash and cash withdrawals solve short-term liquidity problems. However, if used without planning, they can create longer-term financial pressure. Understanding the risks helps you make a decision based on control rather than urgency.

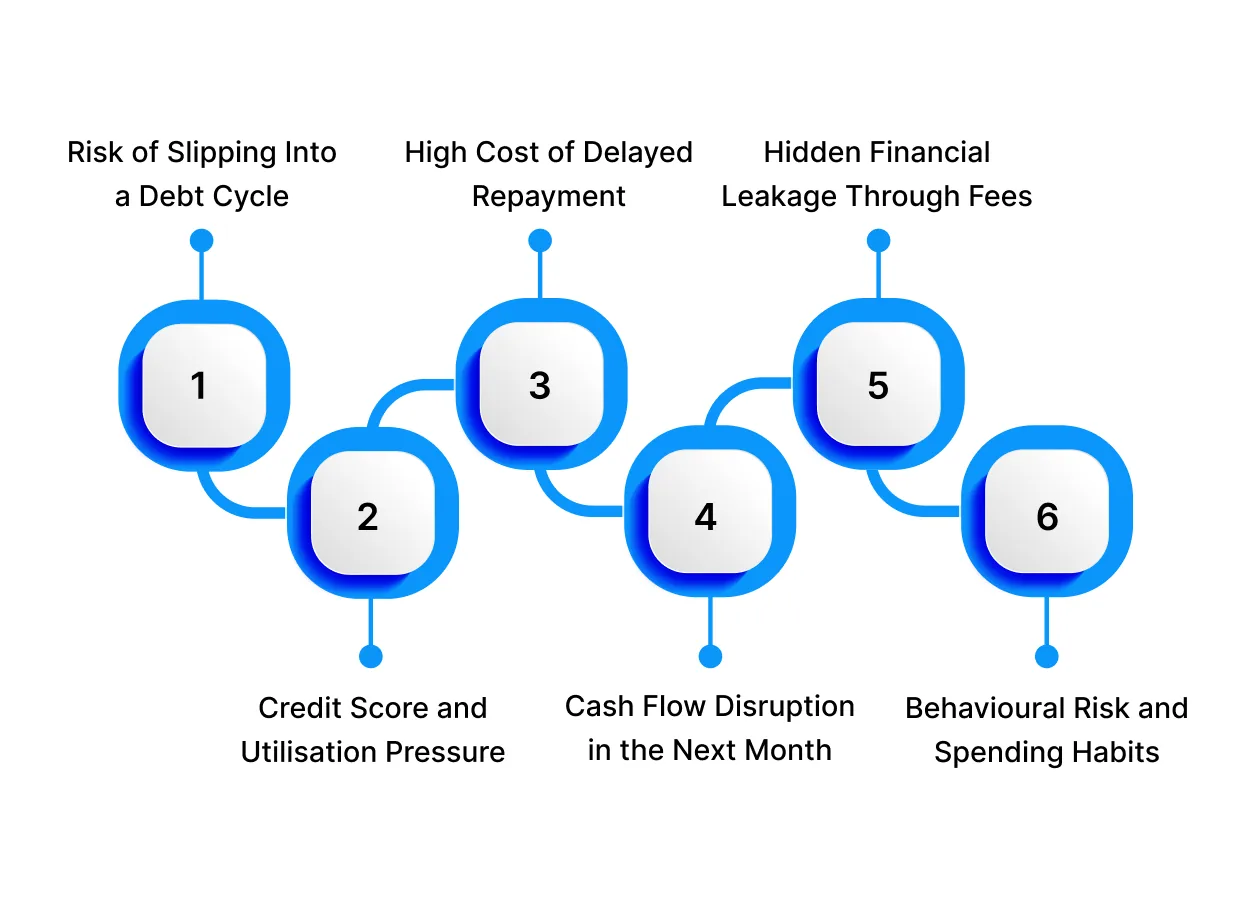

Risk of Slipping Into a Debt Cycle

Risk: When short-term borrowing becomes a recurring solution, it slowly turns into dependency. For example, using fast cash to repay a previous loan or taking a credit card cash advance to cover last month’s bill creates a rollover pattern. Over time, repayments stack up and reduce your future disposable income.

Mitigation: Borrow only when there is a defined, unavoidable need. Ensure the repayment comes from confirmed income, not from another borrowing source.

Credit Score and Utilisation Pressure

Risk: Many regulated lenders report fast cash loans to credit bureaus. Missing even one EMI can negatively impact your credit score. Similarly, withdrawing a large portion of your credit card limit increases your credit utilisation ratio, which can lower your score even if you repay later.

Mitigation: Keep credit utilisation below 30 to 40 per cent where possible. Set repayment reminders and avoid borrowing amounts that stretch your capacity.

High Cost of Delayed Repayment

Risk: Credit card cash withdrawals begin accruing interest immediately, often at rates significantly higher than standard purchase transactions. If you pay only the minimum due, interest compounds, and the repayment period extends. Fast cash loans may also include late payment penalties that increase the effective cost.

Mitigation: Always calculate the full repayment amount and timeline before proceeding. If possible, repay early to reduce total interest outflow.

Cash Flow Disruption in the Next Month

Risk: Short-term loans usually have tight repayment tenures. A large EMI in the following month can strain your regular budget, forcing you to cut essential expenses or borrow again.

Mitigation: Assess your next month’s fixed commitments, such as rent, EMIs, and bills, before borrowing. Ensure the repayment fits comfortably without affecting essentials.

Hidden Financial Leakage Through Fees

Risk: Processing charges, cash advance fees, ATM transaction limits, and late penalties can increase the effective cost beyond the advertised rate. These small charges may seem minor individually, but they add up quickly.

Mitigation: Review the complete cost breakdown, including interest, fees, and penalties. Focus on the total payable amount, not just the interest rate.

Behavioural Risk and Spending Habits

Risk: Easy access to digital loans and credit card advances can reduce the psychological barrier to borrowing. What starts as an emergency tool can gradually become a lifestyle funding mechanism, weakening long-term financial discipline.

Mitigation: Define clear personal rules. For example, only borrow for medical needs, rent gaps, or unavoidable emergencies. Avoid using borrowed money for discretionary spending.

When Should You Choose Fast Cash?

Fast cash is not meant for everyday spending. It works best as a short-term financial bridge when savings are unavailable, and the expense cannot be postponed. The key is to choose it strategically, not emotionally.

Choose fast cash if the following conditions apply:

- You do not have sufficient bank balance available: if your savings are exhausted or locked in investments, fast cash can provide immediate liquidity without breaking long-term financial plans.

- The expense is urgent and unavoidable: medical bills, essential repairs, or rent deadlines are situations where delaying payment could lead to more serious consequences.

- You want structured repayment clarity: Fast cash usually comes with a fixed tenure and predefined EMI or lump sum repayment schedule. This gives you a clear timeline instead of revolving interest uncertainty.

- You prefer transparent cost visibility: Digital lending platforms typically show the total repayment amount upfront, allowing you to assess affordability before confirming.

- You have a predictable income next month: Fast cash works best when you are confident that the upcoming income will comfortably cover the repayment without disrupting essentials.

In short, fast cash is most suitable when you need immediate funds, lack available savings, and can commit to disciplined repayment within a defined period.

When Should You Opt for a Cash Withdrawal

A cash withdrawal from your bank account or credit card is often the default choice, but it comes with its own considerations. Understanding when it makes sense can help avoid unnecessary fees and debt.

A cash withdrawal from your bank account or credit card is often the default choice, but it comes with its own considerations. Understanding when it makes sense can help avoid unnecessary fees and debt.

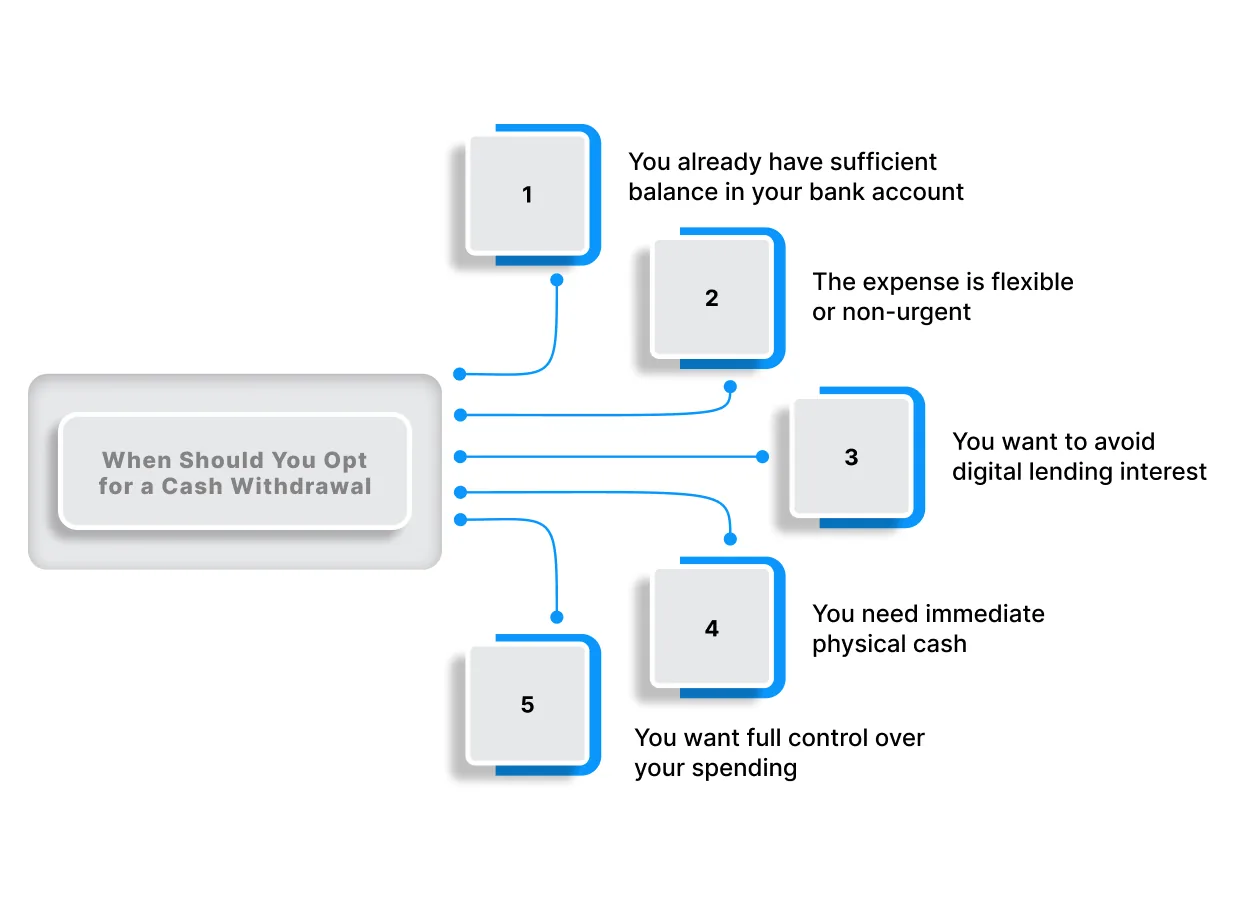

Opt for a cash withdrawal if the following apply:

- You already have sufficient balance in your bank account: With available funds, withdrawing cash avoids interest charges and extra fees, making it a cost-free solution.

- The expense is flexible or non-urgent: If the payment can wait until your next salary or income cycle, using your own money is safer than borrowing.

- You want to avoid digital lending interest: Withdrawing from your account or using your own credit card cash limit can be cheaper than fast cash options, which often carry higher rates.

- You need immediate physical cash: For in-person payments or situations where digital transfers are not accepted, withdrawals provide instant liquidity.

- You want full control over your spending: Using your own money encourages budgeting discipline and prevents over-reliance on short-term loans.

In essence, cash withdrawals are best when funds are available, fees are minimal, and the payment does not require urgent borrowing.

Also Read: Can Paying Bills Help Build a Credit Score?

Key Risks of Fast Cash Compared to Cash Withdrawals

While fast cash loans offer convenience, they also come with risks that can affect your financial health. Being aware of these risks helps you make informed decisions.

| Risk | Fast Cash | Cash Withdrawal |

| Interest & Fees | High interest rates and processing fees | Typically, none beyond bank charges |

| Repayment Timeline | Short, often within weeks | Flexible, depends on account balance |

| Debt Cycle | High risk if used frequently | Low risk if within own funds |

| Credit Score Impact | Late or missed payments can hurt your credit | No impact |

| Consumer Protection | Limited transparency and dispute resolution | Regulated, full protection |

Smart Borrowing Tips to Avoid Financial Stress

Borrowing can be a lifesaver for short-term cash needs, but it can also create stress if not managed carefully. By following these practical tips, you can use loans responsibly while keeping your finances healthy:

1. Calculate the Total Repayment Amount

Before borrowing, know exactly how much you’ll owe in total, including interest, processing fees, and any other charges. This prevents surprises and helps you budget effectively.

For example: Borrowing ₹10,000 at 2% monthly interest for three months means a total repayment of ₹10,600. Knowing this upfront helps you plan your monthly cash flow so repayments don’t derail other expenses.

2. Avoid Borrowing for Lifestyle Spending

Loans should address urgent needs, not discretionary spending. Using borrowed money for shopping, vacations, or entertainment increases financial risk and adds stress.

For example, If you need ₹5,000 for a weekend getaway, it’s better to save over a month instead of taking a short-term loan that adds interest costs.

3. Repay Early When Possible

Paying off your loan sooner reduces interest payments and frees up cash for other priorities. Early repayment also boosts your creditworthiness, making future borrowing easier.

For example: Paying off a ₹15,000 loan two weeks early could save ₹200–₹300 in interest, which could be redirected to your savings or emergency fund.

4. Maintain an Emergency Fund

Having a small cash buffer reduces reliance on loans for unexpected expenses, giving you peace of mind and financial stability.

For example, Saving ₹5,000 for sudden medical or travel expenses can prevent taking a high-interest loan when emergencies arise.

5. Compare Multiple Borrowing Options

Not all loans are created equal. Short-term personal loans, payday loans, or app-based instant credit can vary widely in interest rates, fees, and repayment flexibility. Always compare options to find the most cost-effective and convenient solution.

For example, Pocketly offers loans from ₹1,000 to ₹25,000 with transparent pricing and flexible repayment terms, whereas some traditional lenders may require collateral or charge higher interest for similar amounts. Comparing options helps you borrow smarter and avoid unnecessary costs.

Need Quick Funds? Pocketly Makes Fast Cash Easy and Safe

Life is unpredictable, and sometimes you need cash quickly, whether it’s for an urgent bill, medical expense, or unexpected travel. Pocketly offers a fast, structured way to access funds without the risks of high-interest credit card advances.

Here’s why Pocketly is the smarter choice for fast cash:

- Borrow exactly what you need: ₹1,000 to ₹25,000, so you avoid unnecessary debt.

- No collateral or guarantor required: hassle-free access even if you don’t have assets.

- Fast approval: simple KYC verification and instant decision-making.

- Instant fund transfer: money reaches your bank account immediately after approval.

- Transparent pricing: interest from 2%/month with processing fees between 1%–8%, no hidden charges.

- Flexible repayment: pick a plan that fits your budget, keeping EMIs manageable.

With Pocketly, you get quick, safe, and predictable access to funds, unlike risky credit card cash advances that can spiral into high costs.

Conclusion

Choosing between fast cash and a regular cash withdrawal comes down to cost, convenience, and urgency. While debit card withdrawals are free and ideal for everyday access, credit card cash advances are costly and should only be used in emergencies.

Fast cash solutions like Pocketly provide a transparent, quick, and structured way to manage short-term financial needs without hidden surprises. They bridge gaps responsibly, letting you cover urgent expenses while keeping your long-term budget intact.

The key is to use each option wisely: withdraw cash for routine needs, and rely on fast cash only for emergencies. By understanding the costs and benefits of both, you can make smarter decisions, reduce financial stress, and stay in control of your money.

Download the Pocketly app today on [Android] or [iOS] to access fast, reliable support whenever you need it.

FAQs

1. What is the difference between fast cash and a cash withdrawal?

Fast cash is a short-term loan from a lender, often approved instantly via apps, while a cash withdrawal is taking out your own money from a bank account or using a credit card’s cash advance feature. Fast cash usually involves interest, whereas debit withdrawals don’t.

2. Is fast cash more expensive than a cash withdrawal?

It depends. Debit withdrawals are free since you’re using your own money. Fast cash may charge interest and processing fees, but credit card cash advances typically have higher interest and fees, making them the costliest option.

3. Can fast cash affect my credit score?

Yes. If you fail to repay fast cash on time, it can impact your credit score. Regular debit card withdrawals do not affect your score, while credit card cash advances may impact your credit utilisation.

4. When should I opt for fast cash instead of a cash withdrawal?

Fast cash is best for urgent situations when your bank balance is low, you need structured repayment, or you want quick access to funds without collateral. It’s a safer alternative to high-interest cash advances on credit cards.

5. Are there limits on fast cash loans?

Yes. Most fast cash services provide small loan amounts, usually ranging from ₹1,000 to ₹25,000, making them suitable for short-term emergencies rather than large expenses.

6. Can I withdraw cash from my credit card?

Yes, through a cash advance. However, it comes with high interest, processing fees, and interest starts accruing immediately, so it’s only recommended for emergencies.