Money moves faster today than most people can keep up with. Salaries arrive digitally, payments happen in seconds, and banking apps promise convenience at every tap. Yet, despite having more access to financial tools than ever before, many people still feel confused, anxious, or out of control when it comes to their money.

This gap shows up in everyday decisions. People overspend without realizing where their money goes, take loans without fully understanding interest or repayment terms, and trust banking products they don’t completely grasp. A single wrong decision can quietly turn into long-term debt, missed savings goals, or financial stress that lingers for years.

Financial literacy bridges this gap. It turns banking from a passive habit into an active skill. When you understand how banking systems, products, and digital tools actually work, you stop reacting to money and start directing it.

This blog explores how financial literacy and banking are deeply connected, why one cannot work effectively without the other, and how building the right knowledge can help you make smarter, calmer, and more confident financial decisions in everyday life.

TL;DR

- Financial literacy empowers individuals to understand money basics, saving, spending, borrowing, and investing, making everyday banking decisions smarter and safer.

- Banks play a central role in shaping financial behavior through products like savings accounts, loans, credit cards, and digital tools.

- Lack of financial knowledge often leads to poor banking choices, hidden fees, excessive debt, and vulnerability to fraud.

- Strong financial literacy helps people use banking services strategically, optimizing savings, managing credit responsibly, and planning long-term goals.

- As banking becomes increasingly digital, financial literacy is no longer optional; it’s essential for financial security and independence.

Understanding Financial Literacy

Financial literacy refers to the ability to understand and manage personal finances effectively. It includes knowledge of basic financial concepts and the confidence to apply them in real life.

Core Components of Financial Literacy

- Budgeting: Tracking income and expenses to avoid overspending

- Saving: Building emergency funds and short-term reserves

- Credit & Debt: Understanding loans, EMIs, interest rates, and credit cards

- Investing: Basics of returns, risk, and long-term wealth creation

A financially literate individual makes informed decisions instead of reacting impulsively to financial situations.

Why Banking Is Central to Financial Literacy?

Banking is not just a service layer; it is the execution layer of financial literacy. Every financial concept becomes real only when it is experienced through a bank product. From income flow to debt obligations, banks shape day-to-day money behavior and long-term financial outcomes.

- Banks act as the entry point to the formal financial system, converting income into traceable and manageable financial records

- Almost all personal financial decisions, including saving, borrowing, spending, and investing, are routed through banking channels

- Banking products translate abstract concepts such as interest, liquidity, and risk into tangible financial outcomes

- Repeated interaction with banks reinforces financial habits, both positive, like saving and planning, and negative, like over-borrowing and fee leakage

- Banking activity creates a financial history that influences future access to credit, interest rates, and financial opportunities

- The structure and design of banking products subtly guide user behavior, shaping how individuals prioritize spending, saving, and debt management

Without financial literacy, banking becomes reactive and confusing. With it, banking becomes intentional, informed, and strategic.

The Role of Banking in Financial Literacy

Banking plays a foundational role in building financial literacy because it is often the first formal interaction people have with money systems. From opening a savings account to taking a loan, banks influence how individuals understand, manage, and grow their finances.

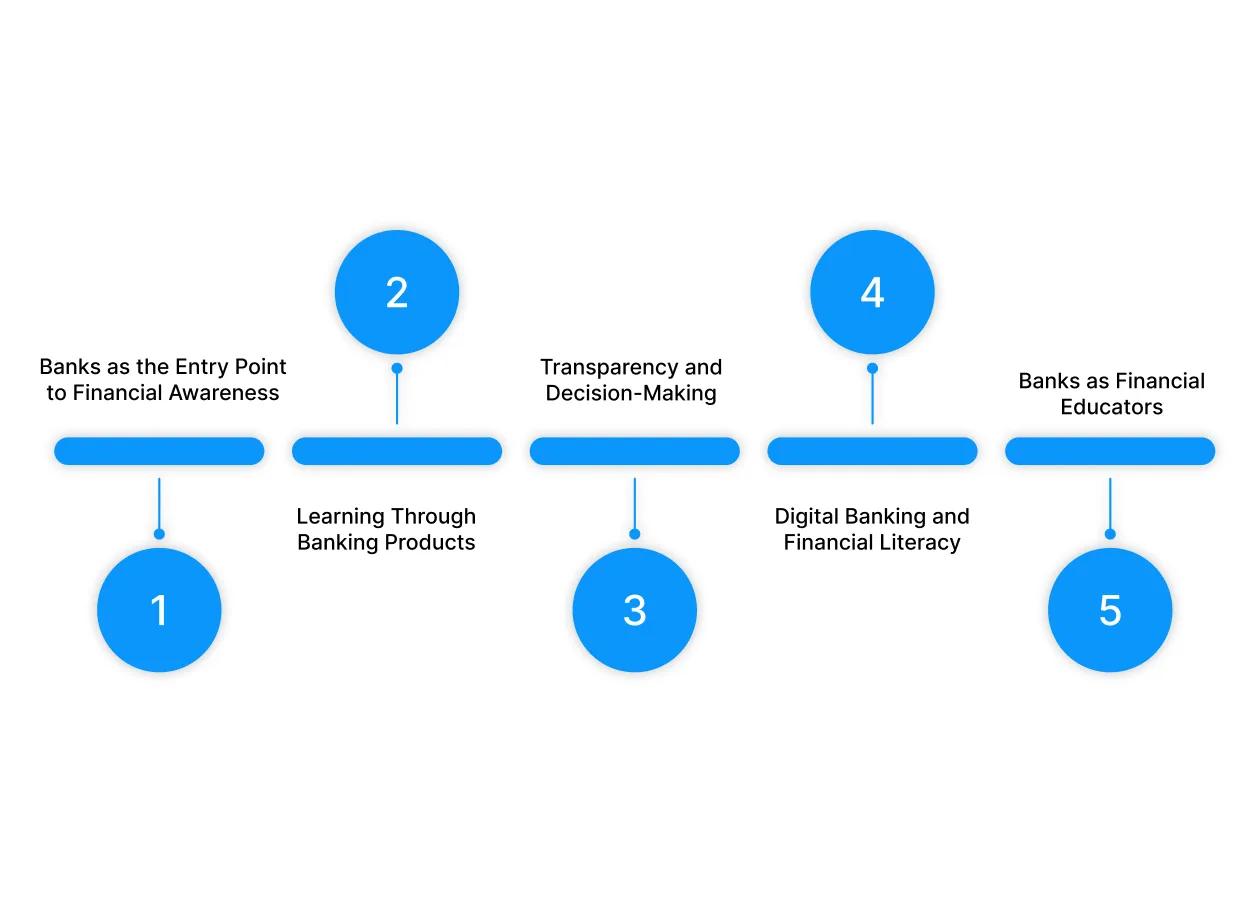

1. Banks as the Entry Point to Financial Awareness

1. Banks as the Entry Point to Financial Awareness

For many people, financial literacy begins with basic banking activities such as:

- Opening a bank account

- Depositing and withdrawing money

- Receiving salary credits or government benefits

These everyday actions introduce core concepts like account balances, interest, transaction records, and financial discipline, forming the groundwork for more advanced financial understanding.

2. Learning Through Banking Products

Banking products act as practical learning tools for financial concepts:

- Savings accounts teach the habit of saving and the concept of interest

- Fixed deposits explain compounding and long-term planning

- Loans and EMIs introduce credit management, interest rates, and repayment discipline

- Credit cards highlight responsible borrowing and the impact of late payments

By using these products, individuals learn financial principles not just theoretically, but through real-life experience.

3. Transparency and Decision-Making

Modern banking exposes users to detailed information such as:

- Fees and charges

- Interest rate structures

- Monthly statements and alerts

Understanding this information improves financial decision-making, helping customers compare products, avoid unnecessary costs, and recognize the importance of reading terms and conditions.

4. Digital Banking and Financial Literacy

Digital banking has significantly expanded access to financial knowledge:

- Mobile apps show real-time spending patterns

- Automated alerts promote better money management

- Expense categorization helps users understand where money goes

These tools make financial literacy more visual, immediate, and actionable, especially for younger and first-time banking users.

5. Banks as Financial Educators

Many banks now go beyond transactions by:

- Offering financial education content

- Providing in-app tips and calculators

- Conducting awareness programs and workshops

This positions banks not just as service providers, but as enablers of informed financial behavior.

Also Read: Simple Money Management Tips for Personal Finances

Key Banking Products Everyone Should Understand

A strong foundation in financial literacy and banking begins with understanding the essential banking products people use daily. Each product plays a specific role in managing money, building discipline, and supporting long-term financial goals.

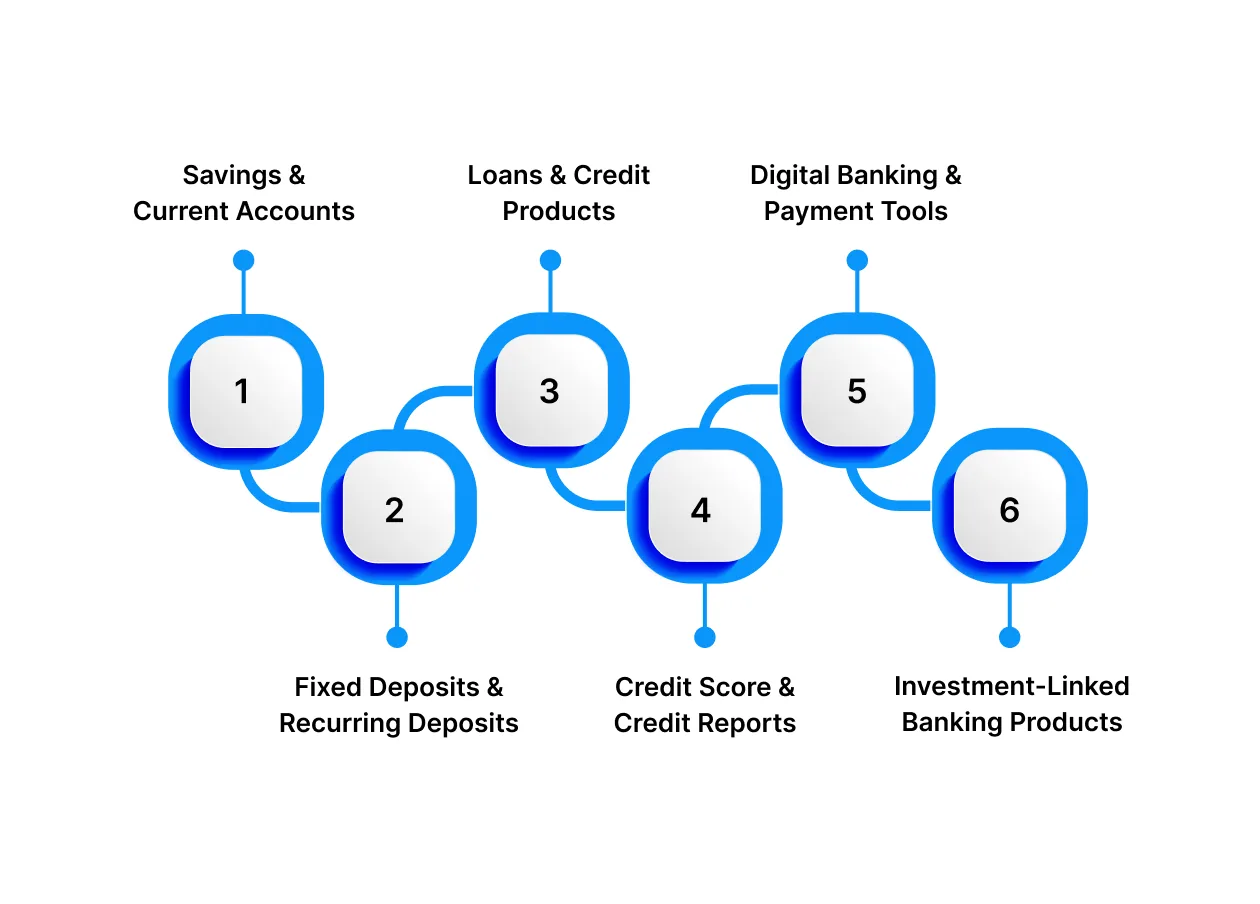

1. Savings and Current Accounts

1. Savings and Current Accounts

A savings account allows individuals to store money securely while earning interest. It supports regular deposits and withdrawals, making it suitable for everyday financial needs. Important aspects include interest rates, minimum balance requirements, transaction limits, and access to digital banking services.

A current account is mainly used by businesses and professionals who require frequent transactions. These accounts usually do not earn interest and come with higher minimum balance requirements and service charges.

Choosing the right type of account helps avoid unnecessary fees and ensures efficient money management.

2. Fixed Deposits and Recurring Deposits

Fixed deposits involve investing a lump sum for a predetermined period at a fixed interest rate. They are considered low-risk and provide predictable returns, though premature withdrawal may attract penalties.

Recurring deposits allow individuals to deposit a fixed amount every month for a specific duration. They are ideal for short-term goals and encourage consistent saving habits.

These products are useful for building financial discipline and maintaining stability in a broader financial plan.

3. Loans and Credit Products

Loans enable individuals to meet large financial needs such as education, housing, or emergencies. Common loan types include personal loans, home loans, and vehicle loans. Key factors to understand are interest rates, loan tenure, EMI structure, and prepayment conditions.

Credit cards provide short-term credit but carry high interest rates if balances are not paid in full. Responsible usage helps build a strong credit profile, while misuse can lead to long-term debt.

Understanding credit products prevents over-borrowing and financial stress.

4. Credit Score and Credit Reports

A credit score reflects an individual’s creditworthiness and is influenced by repayment history, credit utilization, and the length of credit history. Lenders use this score to assess loan eligibility, interest rates, and credit limits.

Maintaining a healthy credit score improves access to affordable financial products and enhances financial flexibility.

5. Digital Banking and Payment Tools

Digital banking includes mobile banking apps, internet banking, and instant payment systems such as UPI. These tools offer convenience, real-time transaction tracking, and reduced reliance on cash.

At the same time, users must be cautious about cybersecurity risks, including fraud and phishing attempts. Awareness of digital safety practices is essential.

6. Investment-Linked Banking Products

Many banks offer access to investment products such as mutual funds, systematic investment plans, and tax-saving instruments. While these products can help grow wealth, it is important to understand their risk, returns, and suitability.

Financial literacy enables individuals to differentiate between genuine financial advice and product-driven sales.

Financial Literacy Challenges in Banking

Despite widespread access to banking services, gaps in financial literacy expose individuals to several financial, operational, and digital risks. Below are the key risks and the corresponding mitigation logic that financial literacy enables.

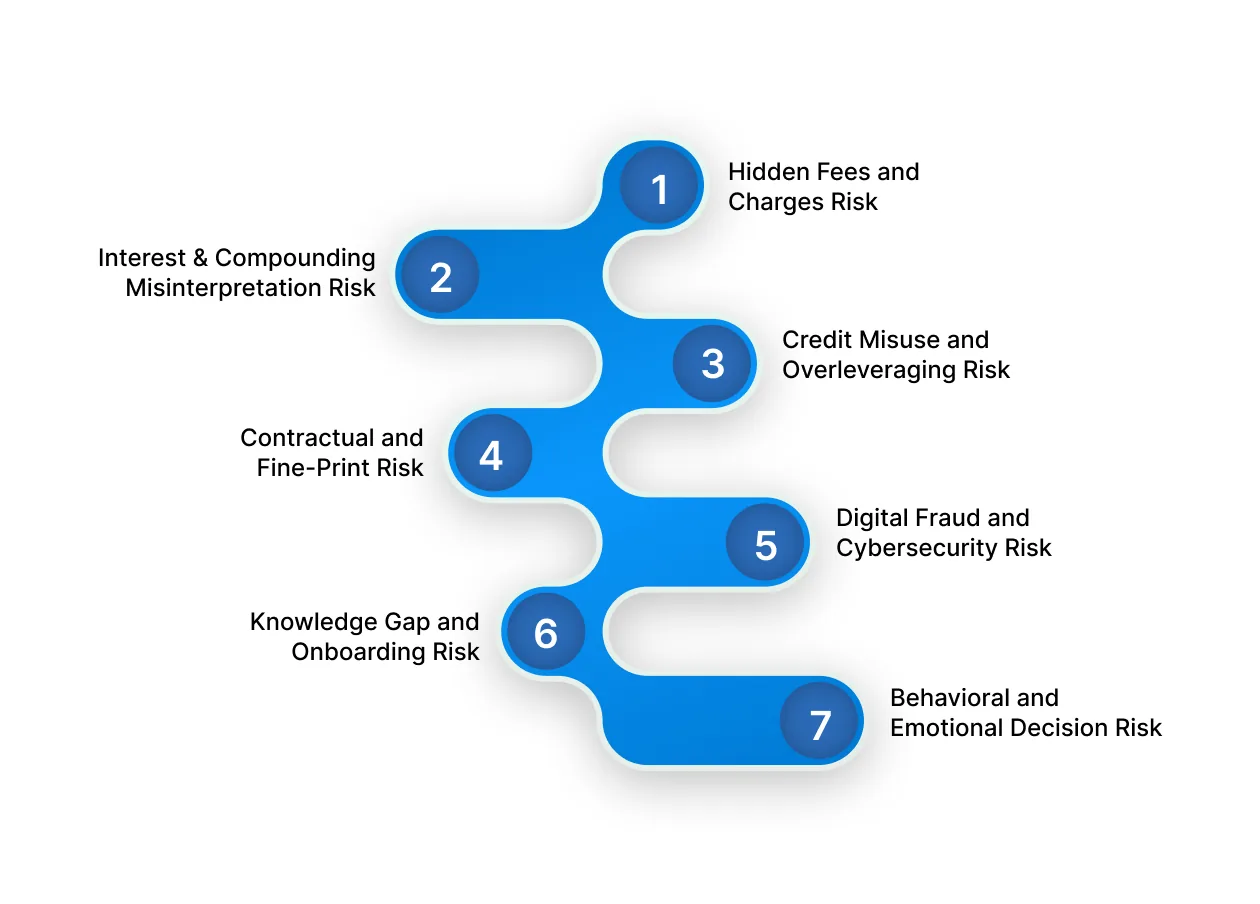

1. Hidden Fees and Charges Risk

1. Hidden Fees and Charges Risk

Risk: Unawareness of minimum balance penalties, ATM limits, card fees, and service charges leads to silent loss of money over time

Mitigation Logic: Financially literate users regularly review account statements, understand fee structures upfront, and choose accounts aligned with their usage patterns.

2. Interest and Compounding Misinterpretation Risk

Risk: Underestimating loan costs and overestimating short-term affordability due to poor understanding of interest rates and compounding.

Mitigation Logic: Understanding compounding enables accurate loan comparisons (APR, tenure impact) and better use of savings and fixed-income products.

3. Credit Misuse and Overleveraging Risk

Risk: Easy access to credit cards, personal loans, and BNPL services encourages overspending, high-interest debt, and credit score deterioration.

Mitigation Logic: Financial literacy promotes credit discipline through EMI planning, credit utilization limits, and prioritizing repayment over consumption.

4. Contractual and Fine-Print Risk

Risk: Mis-selling and unexpected liabilities due to misunderstanding banking terms such as floating rates, foreclosure penalties, and processing fees.

Mitigation Logic: Informed customers actively review terms, ask clarification questions, and compare products instead of relying solely on sales guidance.

5. Digital Fraud and Cybersecurity Risk

Risk: Exposure to phishing, OTP scams, fake banking apps, and social engineering attacks as digital banking adoption increases.

Mitigation Logic: Financial literacy now includes digital hygiene: verifying sources, avoiding unsolicited links, using strong authentication, and monitoring alerts.

6. Knowledge Gap and Onboarding Risk

Risk: First-time banking users make avoidable mistakes due to lack of early financial education and practical exposure.

Mitigation Logic: Structured self-learning through bank resources, trusted financial content, and gradual product adoption reduces costly trial-and-error.

7. Behavioral and Emotional Decision Risk

Risk: Impulsive financial decisions driven by FOMO, peer pressure, or short-term rewards override rational banking choices.

Mitigation Logic: Financial literacy introduces budgeting frameworks, goal-based planning, and delayed-decision strategies to counter emotional bias.

Also Read: Understanding Cash Flow: Definition, Types, and Analysis

How Pocketly Helps You Handle Unexpected Financial Needs

Even with careful planning and budgeting, unexpected expenses are sometimes unavoidable. Medical emergencies, sudden repairs, or last-minute payments can quickly strain your finances and create unnecessary stress. In such moments, having quick access to dependable financial support can make all the difference.

Pocketly is built to bridge that gap. As a digital lending platform, it offers quick and hassle-free access to short-term funds, without the paperwork or delays associated with traditional loans. Whether you’re a student, a working professional, or self-employed, Pocketly helps you manage urgent financial needs with ease.

Why Choose Pocketly?

- Instant, Small-Ticket Loans: Borrow amounts ranging from ₹1,000 to ₹25,000, perfect for covering unexpected expenses without overborrowing.

- Transparent and Affordable Pricing: Interest rates start at just 2% per month, with processing fees between 1% and 8%, so you always know what you’re paying.

- 100% Digital Experience: Complete your KYC online in minutes, no paperwork, no branch visits, and secure processing throughout.

- Flexible Repayment Options: Choose a repayment plan that suits your income and lifestyle, whether you prefer a one-time payment or easy instalments.

How to Apply for a Pocketly Loan

- Download the App: Available on both Google Play Store and Apple App Store.

- Complete Digital KYC: Enter your basic details and verify your identity quickly and securely.

- Choose Your Loan Amount: Select an amount up to ₹25,000 based on your immediate needs.

- Receive Funds Instantly: Once approved, the money is transferred directly to your bank account.

Conclusion

Building financial literacy in banking isn’t an overnight process, but its impact is undeniable. From understanding basic savings accounts to managing credit, loans, and digital payments, financial awareness empowers individuals to make smarter and more confident decisions. These everyday choices shape long-term financial stability and resilience.

With stronger financial literacy, people can use banking services more effectively, saving consistently, borrowing responsibly, and avoiding unnecessary fees or debt traps. It’s not just about accessing banking products; it’s about understanding how they work and using them to support real financial goals.

Looking to manage your finances with ease while embracing smarter solutions? Pocketly offers quick, secure, and transparent personal loans, designed to support you through short-term needs. Download the Pocketly app on iOS or Android and keep your financial momentum going with ease.