The banking and finance industry is changing faster than most people realise. Digital banking, fintech platforms, AI-driven decisions, and real-time payments are not just improving convenience. They are reshaping how money is accessed, moved, and managed.

At the same time, the industry is becoming more stable. According to the Reserve Bank of India’s Trend and Progress of Banking 2024–25 report, the gross non-performing asset (GNPA) ratio dropped to around 2.1% in 2025, reflecting stronger balance sheets and improved financial health.

But here is the gap: while access has become faster and easier, understanding how the system actually works has not kept up.

Most users interact with apps, payments, and quick credit options without fully understanding what drives cost, risk, and decision-making behind the scenes.

This blog breaks down how the banking and finance industry is structured, the key trends shaping it in 2026, and what these changes actually mean when you use financial products in real life.

Key Takeaways

-

The banking and finance industry is becoming more digital and data-driven, with AI influencing lending, risk, and customer decisions.

-

Banks and fintech platforms are increasingly overlapping, reducing clear boundaries between traditional and digital financial services.

-

Real-time payments and embedded finance are changing how users interact with money, making transactions faster but decisions more frequent.

-

Access to credit and financial services is expanding, but evaluating cost and risk is becoming more important.

-

The biggest shift is not just faster access, but better control, where users can choose financial products that match their actual needs.

What Is the Banking and Finance Industry

The banking and finance industry is the system that manages money, credit, investments, and financial transactions across the economy.

At its core, it connects those who have money with those who need it.

For example, when you deposit money in a bank, it does not remain idle. Banks use those funds to provide loans to individuals and businesses, earning interest in the process. This cycle of deposits, lending, and repayments forms the foundation of the industry.

The industry includes multiple segments:

-

Banking services such as savings accounts, current accounts, and payments

-

Lending and credit including personal loans, home loans, and business financing

-

Investment services like mutual funds, stock markets, and wealth management

-

Insurance services for risk coverage

-

Fintech platforms that use technology to deliver faster and more accessible financial services

Together, these segments create a system that keeps money moving across individuals, businesses, and the broader economy.

Also Read: Interest Rates in India 2026: How They Affect Loans & Savings

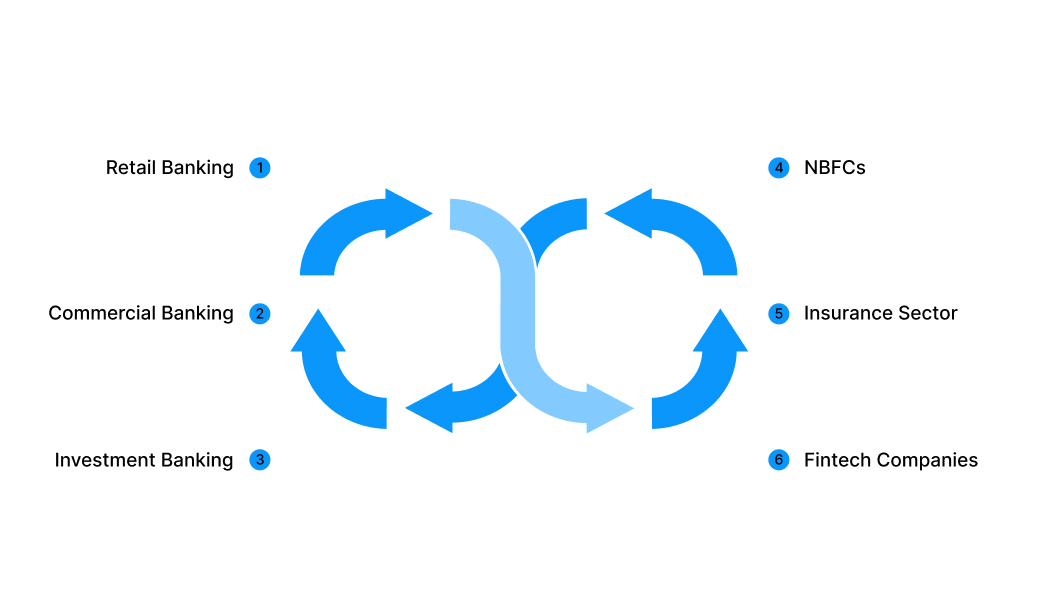

How the Banking and Finance Industry Is Structured Today

The banking and finance industry is not a single system. It is made up of different segments, each handling a specific role in how money is managed, moved, and allocated.

Understanding this structure makes it easier to see where different services fit and how they connect.

Retail Banking

This is the most visible part of the industry for everyday users.

-

Focuses on individuals and households

-

Offers savings accounts, personal loans, credit cards, and mortgages

Commercial Banking

Helps companies manage cash flow and fund operations.

-

Serves businesses and corporations

-

Provides business loans, working capital, and transaction services

Investment Banking

Works more with corporations and investors than individual customers.

-

Deals with capital markets and large financial transactions

-

Handles mergers, acquisitions, IPOs, and fundraising

Non-Banking Financial Companies (NBFCs)

Play a key role in expanding credit access, especially where traditional banks are slower.

-

Provide lending and financial services without being full-scale banks

-

Often focus on specific segments like personal loans, vehicle loans, or MSME financing

Insurance Sector

Helps individuals and businesses manage uncertainty.

-

Provides financial protection against risks

-

Includes life insurance, health insurance, and asset coverage

Fintech Companies

Driving innovation and changing how financial services are accessed.

-

Use technology to deliver financial services faster and more efficiently

-

Includes digital payments, lending platforms, investment apps, and neobanks

Each segment serves a different purpose, but together they form an interconnected system that supports everything from daily transactions to large-scale financial activity.

Also Read: AI in Investment Banking 2026: Boost Speed, Accuracy, and Profits

How Money Moves in the Banking and Finance Industry

At its core, the banking and finance industry works by moving money from where it is available to where it is needed. This flow may seem simple, but it involves multiple layers of lending, pricing, and risk management.

Here is how it typically works:

-

Deposits form the foundation: Individuals and businesses deposit money into banks through savings and current accounts. This creates a pool of funds.

-

Banks lend this money: The deposited funds are used to provide loans to borrowers, such as individuals, businesses, and institutions.

-

Interest drives the model: Banks pay a lower interest rate on deposits and charge a higher rate on loans. The difference between the two is a key source of revenue.

-

Risk is managed continuously: Not all borrowers repay on time, so banks assess creditworthiness, monitor loans, and maintain reserves to manage potential losses.

-

Transactions keep the system active: Payments, transfers, and digital transactions ensure continuous movement of money across the economy.

For example, when you deposit money in a savings account, a portion of it may be used to fund a loan for a business or another individual. The interest earned on that loan contributes to the system, while you receive a smaller return on your deposit.

This continuous movement of deposits, lending, and repayments is what keeps the financial system functioning.

Key Trends Reshaping the Banking and Finance Industry in 2026

The banking and finance industry is no longer evolving gradually. It is shifting in how services are delivered, how decisions are made, and how customers interact with financial systems. These changes are not isolated. They are connected and reshaping the entire ecosystem.

Here are the key trends defining the industry in 2026:

AI and Automation in Banking

Banks are moving beyond basic automation and using AI for decision-making across lending, fraud detection, and customer service. Credit assessments are becoming faster and more data-driven, reducing reliance on manual checks. At the same time, AI is helping banks personalize offerings based on user behavior.

Impact: Faster approvals, reduced operational costs, and more tailored financial products.

Digital and Mobile-First Banking

Banking has shifted from branch-based interactions to mobile-first experiences. Account opening, KYC, transactions, and service requests are now handled digitally. Physical presence is becoming less central to everyday banking.

Impact: Higher convenience for users and reduced infrastructure costs for banks.

Rise of Fintech and Embedded Finance

Fintech companies are not just competing with banks. They are integrating financial services into everyday platforms. Payments, credit, and insurance are now embedded within e-commerce, apps, and digital ecosystems.

Impact: Financial services are becoming more accessible, but competition is increasing for traditional banks.

Open Banking and API Integration

Open banking allows secure data sharing between financial institutions and third-party providers. This enables better product customization, aggregation of financial data, and smoother user experiences across platforms.

Impact: More control for users over their financial data and access to integrated financial solutions.

Real-Time Payments and UPI Growth

Payment systems are moving toward instant processing. In India, UPI has transformed how money is transferred, making transactions seamless across individuals and businesses.

Impact: Faster cash flow, increased transaction volume, and reduced reliance on traditional payment methods.

Cybersecurity and Data Protection

As digital adoption increases, so do risks related to data breaches and fraud. Financial institutions are investing heavily in security frameworks, encryption, and real-time monitoring systems.

Impact: Stronger focus on trust, compliance, and protection of user data.

Financial Inclusion Expansion

Technology is helping bring financial services to users who were previously underserved. Digital onboarding, simplified KYC, and mobile access are expanding the reach of banking and credit services.

Impact: Wider participation in the financial system and growth in new customer segments.

The industry is moving toward a model where technology, accessibility, and data-driven decisions define how financial services are created and delivered.

Also Read: AI in Banking That’s Actually Delivering Results in 2026

How These Trends Affect Users and Businesses

The shifts in the banking and finance industry are not just about technology. They are changing how financial decisions are made, how risk is assessed, and who gets access to money.

Here is how that shows up in real situations:

-

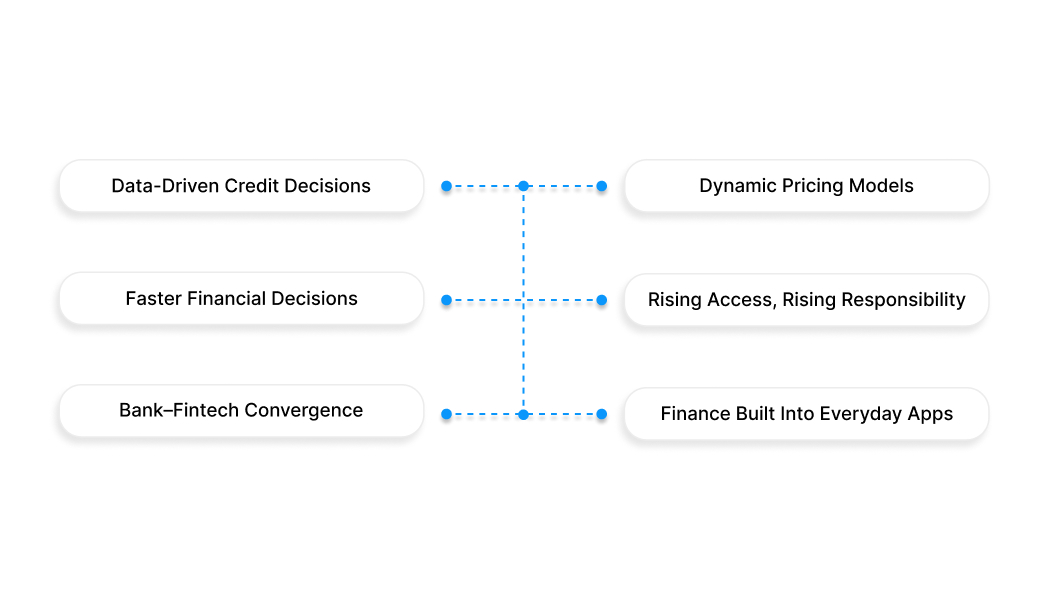

Credit decisions are becoming data-driven, not profile-driven: Earlier, access to credit depended heavily on formal income proof and credit history. Now, alternative data such as transaction behavior and spending patterns are influencing approvals. This is expanding access but also changing how risk is priced.

-

Speed is changing financial behavior: Instant payments and faster loan approvals are not just convenient. They are reducing the time people spend planning financial decisions, which can sometimes lead to quicker but less evaluated choices.

-

The gap between traditional banks and fintech is narrowing: Banks are adopting fintech-like experiences, while fintech platforms are taking on roles traditionally handled by banks. For users, this means fewer clear boundaries between where services come from.

-

Cost structures are becoming less visible but more dynamic: While interfaces are simpler, pricing is increasingly based on real-time risk assessment. This means two users may see different loan terms based on behavior, not just standard rates.

-

Financial access is increasing, but so is responsibility: More people can now access credit and financial tools, but this also requires a better understanding of cost, repayment, and long-term impact.

-

Financial services are becoming part of everyday platforms: Payments, credit, and insurance are now integrated into apps people already use. This reduces friction, but also makes financial decisions more frequent and less deliberate.

For example, a user may get instant credit while shopping online without actively seeking a loan. At the same time, a business may access working capital based on transaction data instead of traditional financial statements.

The industry is not just becoming faster. It is becoming more embedded, more data-driven, and less visible, which changes how financial decisions are made on a daily basis.

Key Challenges Shaping the Banking and Finance Industry Today

While the industry is evolving rapidly, these changes also introduce new pressures that are not always visible on the surface. Growth, technology, and competition are solving some problems, but creating others at the same time.

Here are the key challenges shaping the industry today:

-

Balancing innovation with regulation: Financial systems operate under strict regulatory frameworks. As new models like fintech, embedded finance, and digital lending grow, regulators are working to keep pace without slowing down innovation.

-

Legacy systems vs modern infrastructure: Many traditional banks still rely on older systems that are not built for real-time processing or seamless integrations. Upgrading these systems without disrupting operations remains a major challenge.

-

Rising cybersecurity risks: As more financial activity moves online, the risk of fraud, data breaches, and cyberattacks increases. Security is no longer just a technical issue but a core operational priority.

-

Changing customer expectations: Users now expect instant service, personalized offerings, and zero friction. Meeting these expectations consistently across systems and platforms is difficult.

-

Pressure on margins and pricing: Increased competition from fintech and digital platforms is forcing banks to rethink pricing models. Revenue from traditional interest-based models is under pressure.

-

Data management and privacy concerns: With more data being used for decision-making, ensuring accuracy, ethical use, and compliance with privacy regulations has become critical.

-

Access vs risk trade-off: Expanding credit access to more users increases financial inclusion, but it also raises the risk of defaults if not managed carefully.

For example, while digital lending has made credit more accessible, it has also introduced challenges in assessing risk accurately at scale. Similarly, while real-time payments improve convenience, they require stronger fraud detection systems.

The industry is not just managing growth. It is constantly balancing speed, access, risk, and control at the same time.

What the Future of Banking and Finance Looks Like

The direction of the banking and finance industry is not just about adding more technology. It is about changing how financial services are delivered, accessed, and experienced.

The next phase of growth is likely to be less visible but more integrated into everyday life.

Here is how the future is shaping up:

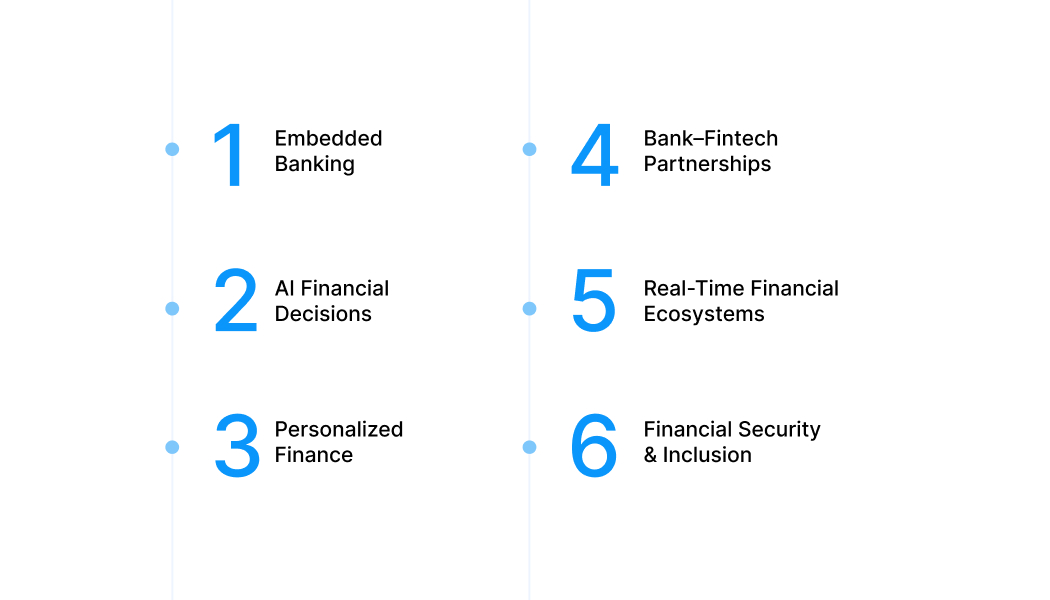

Banking becomes less visible, more embedded

Financial services will increasingly operate in the background. Payments, credit, and insurance will be built into platforms people already use.

Example: While booking a flight or ordering online, payment, insurance, and even credit options are offered within the same app without needing a separate banking step.

AI-driven financial decisions become standard

Credit approvals, fraud detection, and financial recommendations will rely more on real-time data and predictive models.

Example: Instead of applying for a loan, users may receive instant credit offers based on their transaction history and spending patterns.

Hyper-personalization of financial products

Users may see customized interest rates, limits, and repayment options based on their behavior rather than fixed offerings.

Example: Two users with similar incomes may receive different loan terms because their spending and repayment patterns differ.

Stronger collaboration between banks and fintech

Banks and fintech platforms are likely to work together more closely, combining infrastructure with user-focused experiences.

Example: A traditional bank may partner with a fintech app to offer digital onboarding and faster loan approvals.

Shift toward real-time financial ecosystems

Payments, settlements, and lending decisions will continue moving toward real-time systems.

Example: Instant transfers through systems like UPI allow money to move within seconds, improving both personal and business cash flow.

Greater focus on financial access with risk control

More people will gain access to financial services, supported by better risk assessment tools.

Example: Small businesses or first-time borrowers may get credit based on transaction data instead of traditional collateral requirements.

The future of the industry is not just digital. It is integrated into everyday platforms, driven by data, and increasingly tailored to individual behavior and needs.

How Lending Is Changing Across the Banking and Finance Industry

Lending is one of the clearest areas where the banking and finance industry is changing. Traditional loan models were built around longer tenures, fixed eligibility checks, and slower approval systems. That structure is shifting.

Here is what is changing across the industry:

-

Credit is becoming faster: Loan approvals that earlier took days are increasingly being processed in minutes or hours through digital systems and automated checks.

-

Eligibility is becoming more data-driven: Instead of depending only on formal income proofs and traditional credit history, lenders are also using transaction behavior, repayment patterns, and digital financial activity.

-

Borrowing is becoming more need-based: More users now prefer smaller, purpose-driven credit instead of large-ticket borrowing that creates long repayment commitments.

-

Digital channels are replacing branch-heavy processes: Application, verification, approval, and disbursal are increasingly happening online, which reduces turnaround time and operational friction.

-

Short-term credit is gaining relevance: Not every financial need requires a long-tenure loan. Smaller and shorter-duration credit products are becoming more common for immediate expenses and temporary cash gaps.

For example, someone dealing with a medical bill or a salary gap may not want a long-term personal loan. They are more likely to look for a smaller and faster borrowing option that matches the actual requirement.

Lending is becoming faster, more flexible, and more aligned with specific financial needs rather than one fixed borrowing model.

How Pocketly Fits into the Shift Toward Smaller and Faster Credit

As lending becomes more need-based, not every financial requirement calls for a large, long-term loan. Many situations involve smaller amounts and shorter timelines, where a long repayment cycle can increase the overall cost unnecessarily.

This is where Pocketly fits into the evolving lending landscape.

Pocketly is a digital lending platform working with RBI-registered NBFCs, designed for short-term borrowing needs where speed, flexibility, and clarity of cost matter.

Here is how it aligns with current lending trends:

-

Loan amounts from ₹1,000 to ₹25,000: This makes it relevant for smaller financial requirements such as urgent bills, temporary cash gaps, or short-term personal expenses.

-

Interest starting from 2% per month: The borrowing cost is structured for short-term use rather than long-term repayment cycles.

-

Processing fee from 1% to 8%: The applicable fee depends on the borrower profile and loan amount, which is why reviewing the total cost upfront is important.

-

No collateral required: The loan is unsecured, so users do not need to pledge assets or arrange guarantors.

-

Fully digital process: Application, digital KYC, approval, and disbursal happen online, which reduces the delay associated with traditional loan processes.

-

Shorter repayment orientation: The product is positioned around immediate and time-sensitive requirements, not long-term debt commitments.

If you are dealing with a temporary expense or a short-term cash gap, you can check your eligibility and get started by downloading the Pocketly app on Android or iOS.

FAQs

Q: What is the banking and finance industry?

The banking and finance industry includes institutions that manage money, credit, investments, and financial transactions. It connects individuals, businesses, and governments through services like banking, lending, and insurance.

Q: What are the latest trends in the banking and finance industry?

Key trends include AI-driven banking, digital and mobile-first services, fintech growth, and real-time payments. These changes are making financial services faster, more accessible, and more data-driven.

Q: How is fintech changing the banking industry?

Fintech is making financial services quicker and more flexible by using technology for payments, lending, and investments. It is also increasing competition for traditional banks.

Q: What is digital banking and why is it important?

Digital banking allows users to access financial services online without visiting branches. It improves convenience, reduces processing time, and supports real-time transactions.

Q: How can I choose the right borrowing option for short-term needs?

For short-term needs, it is better to choose smaller loan amounts with shorter repayment cycles to control interest cost. Platforms like Pocketly are designed for this kind of borrowing, where the loan stays aligned with the actual requirement.