Artificial Intelligence (AI) is no longer a futuristic idea. It is actively reshaping how financial services operate, particularly in lending. Globally, AI is transforming how lenders assess risk, approve loans, and prevent fraud. In India, the surge in fintech adoption has revolutionised access to credit, with digital lending platforms and alternative credit models rapidly growing.

According to industry estimates, FinTech non‑bank lenders in India sanctioned a record 10.9 crore personal loans in FY 2024-25, showing a significant increase in digital credit adoption. By improving risk assessment, broadening data sources, and speeding up approvals, AI is transforming how credit reaches individuals and small businesses.

By tapping into more data sources, AI makes it easier for traditionally underserved individuals and small businesses to access credit. For young borrowers, gig economy workers, and first-time users, AI opens the door to financial opportunities where traditional lending models fail.

This guide will explore how AI enhances access to credit, improves efficiency for lenders, and what it means for borrowers.

Key Takeaways

- AI in Lending Revolutionises Credit Access: AI is transforming the lending process by making credit decisions faster, fairer, and more inclusive, especially for underserved individuals and small businesses in India.

- AI Improves Risk Assessment and Credit Scoring: Through machine learning, predictive analytics, and natural language processing, AI can assess creditworthiness using alternative data, allowing individuals with limited credit history to access loans.

- Enhanced Customer Onboarding and Fraud Detection: AI streamlines customer onboarding with automated KYC processes and helps detect fraud in real time, protecting both borrowers and lenders.

- AI Benefits Borrowers: Borrowers benefit from faster loan approvals, personalised loan offers, greater credit inclusion, and improved transparency in decision-making.

- Risks and Ethical Considerations: While AI offers numerous benefits, it also raises concerns around data privacy, algorithmic bias, and regulatory compliance, making responsible AI deployment crucial.

- Future of AI in Lending: The future of AI in lending includes more transparent AI models, integration with digital identity and open banking, and broader use across financial products like savings, insurance, and investment services.

What Is AI in Lending and Why It Matters

Artificial Intelligence (AI) refers to systems that learn patterns, make predictions, and automate decisions based on data. AI’s primary strength lies in its ability to process and analyse vast amounts of data, far beyond human capacity.

Artificial Intelligence (AI) refers to systems that learn patterns, make predictions, and automate decisions based on data. AI’s primary strength lies in its ability to process and analyse vast amounts of data, far beyond human capacity.

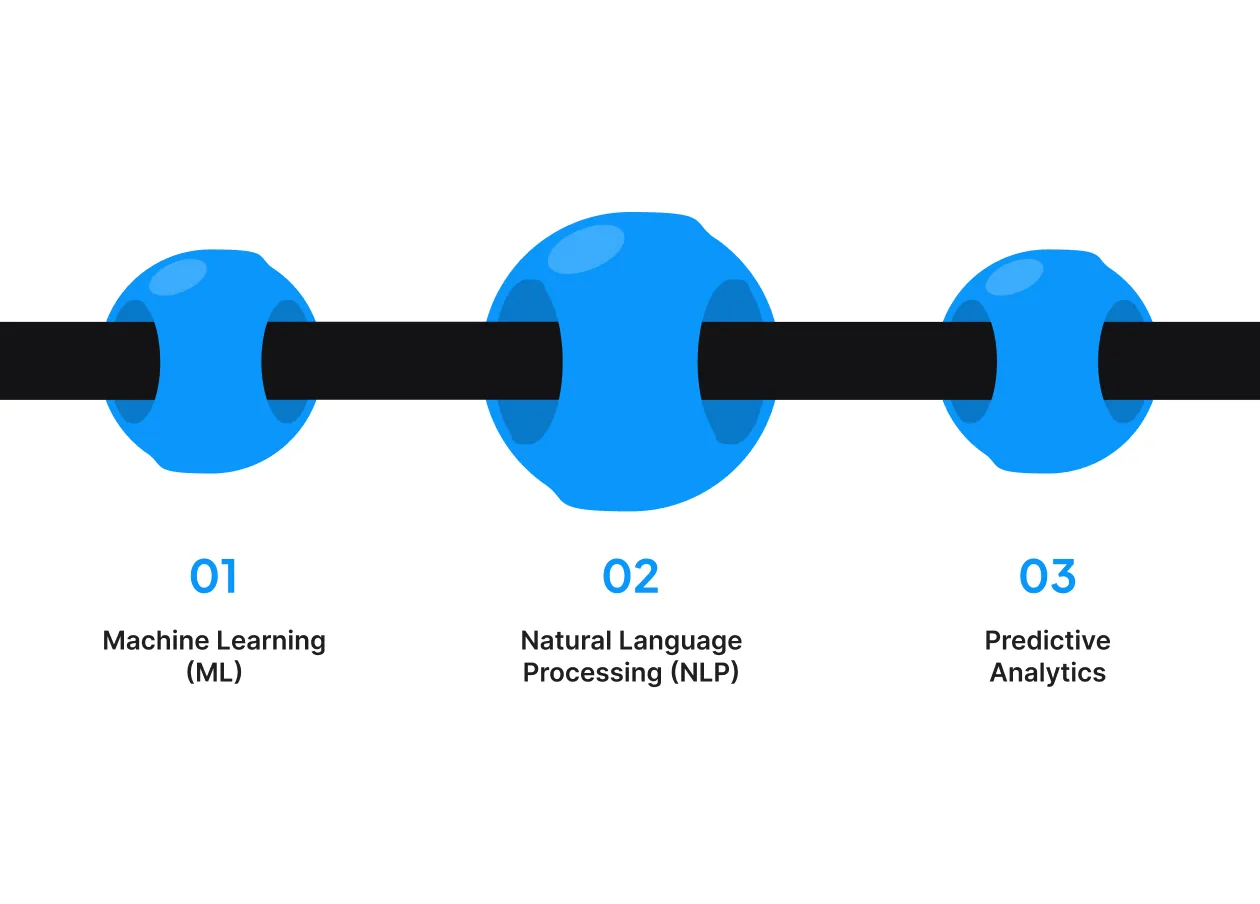

In the context of lending, AI applies techniques such as machine learning (ML), natural language processing (NLP), and predictive analytics to assess credit risk, underwrite loans, and detect fraud. Here’s a breakdown of how these techniques are used:

- Machine Learning (ML): This enables systems to analyse historical data to predict future creditworthiness based on variables like payment history, income patterns, spending habits, and even social media activity.

- Natural Language Processing (NLP): NLP helps AI read and understand unstructured data (such as loan applications and documents) by converting text into valuable insights that can influence lending decisions.

- Predictive Analytics: AI uses predictive models to estimate the likelihood of a borrower repaying their loan based on their financial history, demographic information, and even alternative data like utility payments and rent history.

By implementing these AI technologies, lenders are not only making faster decisions but are also improving the accuracy of those decisions, which in turn increases fairness in lending.

Why AI Matters for Credit Access

For decades, credit decisions were primarily based on a limited set of data, such as credit scores, income, and existing debts. These traditional models often left out individuals who don’t have a long credit history or a bank account, particularly young borrowers, gig workers, or those with non-traditional income streams.

AI changes the game by expanding the data horizon. Instead of relying solely on credit scores, AI can evaluate alternative data sources to gain a better understanding of a borrower’s ability to repay a loan. These alternative data sources might include:

- Transaction history from digital wallets or mobile payments

- Utility bills and rent payments

- Social media behaviour and other digital footprints

For example, gig workers or students who have irregular income streams and may not have a formal credit score are often excluded from traditional credit channels. AI models, however, can look at non-traditional data, such as regular income from freelance work or digital payments, and give them access to credit where traditional systems fail.

With the basics clear, let’s explore the key ways AI is actively changing the lending process and how it benefits both lenders and borrowers.

Also Read: AI in Finance: How It Is Changing Your Money?

How AI Is Transforming the Lending Lifecycle

AI isn’t limited to one part of lending. It enhances every stage of the credit process.

1. Intelligent Customer Onboarding

The first step in any lending process is customer onboarding, where AI is making significant strides. Traditionally, verifying a borrower’s identity and reviewing documents required substantial manual input, which was time-consuming and prone to errors. Now, AI is making the process more efficient and user-friendly by automating key aspects.

- Automated KYC (Know Your Customer): Using OCR (Optical Character Recognition) and image recognition, AI can verify identity documents quickly and accurately, reducing human intervention and accelerating approvals.

- Faster Approvals: This automated system eliminates the need for manual review, cutting down approval times from days to minutes, benefiting both lenders and customers.

AI-powered onboarding makes it easier and faster for young borrowers or those with limited formal financial history to access lending platforms without the typical paperwork delays.

2. Advanced Credit Scoring

Traditional credit scoring models rely heavily on a person’s credit history, which can leave individuals with limited credit records excluded from loan opportunities. AI addresses this by incorporating alternative data into the credit evaluation process.

- Using Alternative Data: AI models can analyse a wider range of factors like digital footprints, payment patterns, and utility history (e.g., electricity and mobile bills) to assess creditworthiness. These alternative data sources allow AI to assess risk for individuals with no formal credit history.

- More Inclusive Credit Decisions: This model benefits students, gig economy workers, and others who may lack traditional credit scores but still show financial responsibility through alternative data sources.

AI in credit scoring offers more inclusive and accurate credit evaluations, opening doors for young borrowers and those without long credit histories.

3. Automated Underwriting and Decisioning

Once the initial credit evaluation is done, underwriting and decisioning play a crucial role in determining whether a loan gets approved. AI’s influence extends to these stages as well, bringing efficiency and consistency to the process.

- Instant Risk Evaluation: AI models can instantly evaluate a borrower’s risk using historical data and predictive algorithms. This reduces manual intervention and allows for faster decision-making.

- Reduction in Human Bias: One of the most significant advantages of AI in underwriting is its ability to reduce human biases. Traditional underwriting could sometimes be influenced by subjective factors, but AI evaluates purely on data-driven patterns, ensuring a more consistent and fair process.

AI also reduces manual errors, which means that loan decisions are more accurate and reliable, further benefiting first-time borrowers and those who previously faced bias in credit assessments.

4. Real-Time Fraud Detection

Fraud detection is another area where AI has a game-changing impact. Traditional fraud detection relied heavily on static rules, but AI has taken it to the next level by detecting complex fraud patterns in real-time.

- Pattern Recognition: AI can scan massive datasets, identify unusual patterns, and alert lenders to potential fraud within seconds.

- Better Protection: By continuously learning from new data, AI is capable of improving its fraud detection capabilities, helping to protect both borrowers and lenders from fraud, and ensuring the lending environment remains secure.

This protection fosters trust in the lending process, offering peace of mind to users, especially those who are new to credit.

AI in lending is revolutionising access to credit, but managing unexpected financial gaps still requires practical, responsible solutions. Pocketly helps you handle those short-term gaps efficiently, ensuring your financial planning stays intact.

Download Pocketly and get the financial support you need with fast approvals and clear terms.

Also Read: Digital Lending In India: Future Trends And Insights

Benefits of AI in Lending for Borrowers

For borrowers, AI’s impact goes beyond speed. It affects fairness, access, and convenience.

1. Faster Loan Approvals

One of the most noticeable benefits of AI in lending is the speed at which loans are processed. Traditional lending decisions could take days or even weeks, but AI-driven platforms streamline the process.

- Real-Time Assessments: AI evaluates creditworthiness almost instantly by scanning a variety of data points. This makes it possible for borrowers to receive loan decisions in minutes, improving overall user satisfaction.

- Improved User Experience: Faster decisions reduce waiting times and improve the overall experience for young borrowers who need quick access to funds.

2. Greater Credit Inclusion

AI is also a significant factor in increasing credit inclusion, especially for those who have been excluded from traditional banking systems due to a lack of formal credit history.

- Alternative Data: By considering factors beyond credit scores, AI enables lenders to evaluate students, gig workers, and self-employed individuals more accurately. This opens up access to credit for young Indians who may have previously struggled to get loans through traditional channels.

- Broader Eligibility: AI-driven platforms expand the pool of eligible borrowers by making the credit decision process more inclusive.

Also Read: What Is Credit Underwriting In Digital Lending?

3. Personalised Loan Offers

AI’s ability to assess individual risk profiles allows it to tailor loan offers to suit specific borrowers.

- Customised Loan Terms: AI can provide loan terms that are better suited to the borrower’s financial situation, such as loan amounts, interest rates, and repayment schedules.

- Fairer Pricing: By personalising loan offers based on real-time data, AI ensures that borrowers are matched with products that fit their financial needs, rather than relying on a generic approach.

4. Enhanced Transparency and Decision Explanation

One of the criticisms of traditional lending systems is the lack of transparency. Borrowers often don’t understand why they were declined or why certain terms were offered.

- Explainable AI: Modern AI models are increasingly designed to explain their decisions in ways that borrowers can understand. Instead of opaque decisions, AI-driven platforms now offer clear explanations for loan decisions.

However, AI’s rise also brings challenges and responsibilities that lenders must address.

Risks and Ethical Considerations with AI in Lending

With great power comes great responsibility and AI in lending is no exception.

With great power comes great responsibility and AI in lending is no exception.

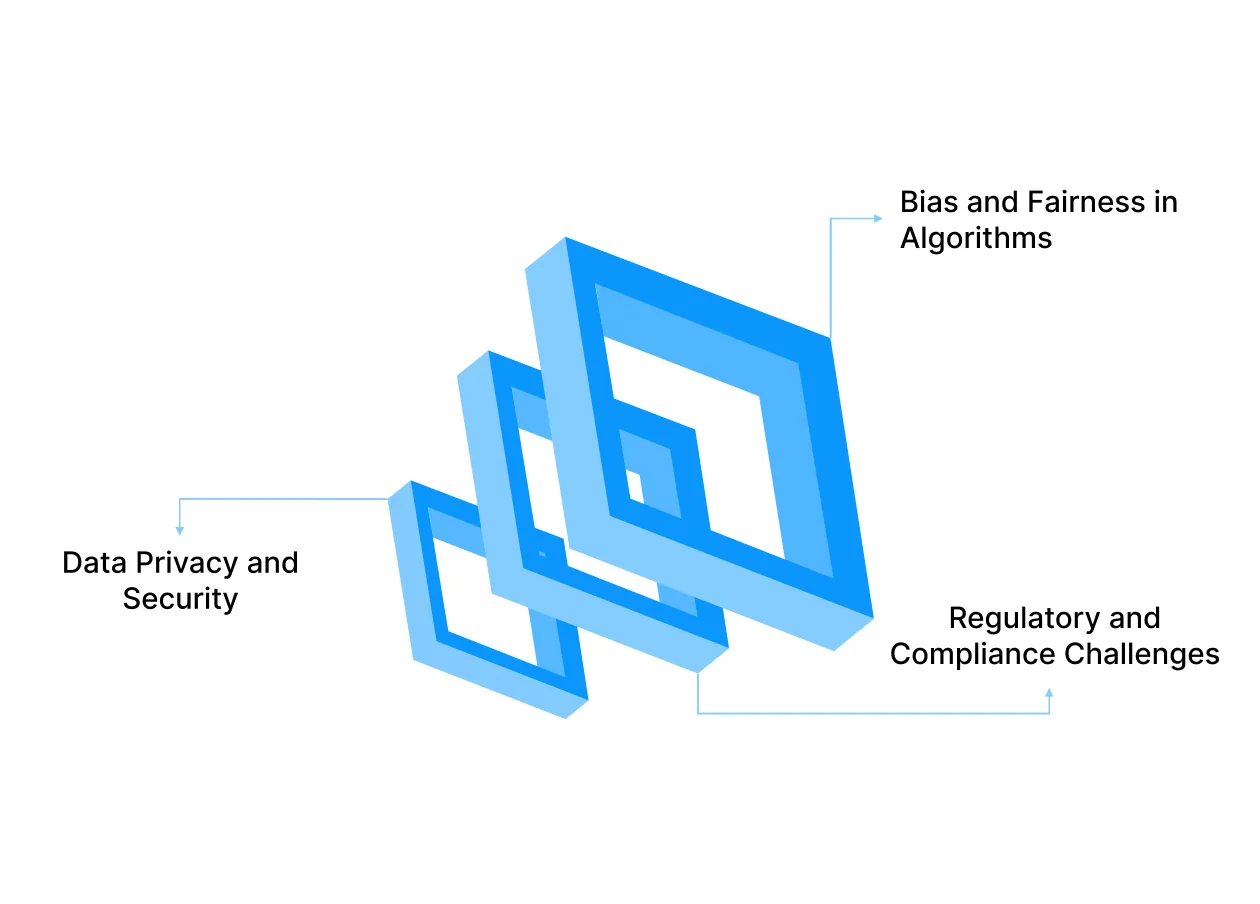

Data Privacy and Security

AI in lending requires access to vast amounts of personal, financial, and behavioural data to make accurate predictions. However, this reliance on data brings significant concerns regarding data privacy and security.

- Protecting User Privacy: Given the sensitive nature of the information involved, ensuring user privacy is paramount. Lenders must take stringent measures to protect data, with secure encryption, anonymisation, and safe data storage practices.

- Security Risks: The more data AI systems process, the higher the risk of breaches or misuse. Lenders must ensure that their systems comply with data protection regulations, like India’s Personal Data Protection Bill (currently being debated), and implement strong security protocols to prevent leaks.

AI can only be truly effective if it operates on secure, ethical data-handling practices. In an era where data breaches are becoming more common, financial services must prioritise user consent, transparency, and data protection to build trust with customers.

Bias and Fairness in Algorithms

AI-driven lending platforms have the potential to create more inclusive and accurate credit decisions. However, AI systems can inherit biases from the data they’re trained on, which could result in unfair outcomes.

- Bias in Training Data: If AI models are trained on historical data that includes biases (e.g., socio-economic disparities or gender biases), the models could unintentionally perpetuate those biases, leading to discrimination against certain groups.

- Amplifying Bias: Even slight biases in AI models can be amplified when used at scale, affecting large groups of borrowers. For example, if an algorithm is not calibrated to account for diverse financial behaviours, it could reject eligible borrowers from underrepresented communities.

Responsible lenders must regularly audit and tune AI models for fairness and transparency. Ensuring that algorithms reflect diverse financial situations and are free from discriminatory biases is key to maintaining fairness in the lending process.

Regulatory and Compliance Challenges

AI’s growing role in financial services, particularly in lending, raises several regulatory and compliance challenges. Lenders must ensure that AI models comply with existing laws and frameworks set by regulators like the RBI, SEBI, and IRDAI.

- Adhering to Financial Regulations: While AI can make lending more efficient, it must still adhere to traditional financial regulations. For example, interest rates, data collection practices, and customer protection laws must be respected even in an AI-driven environment.

- Explainability and Audit Trails: AI models are often referred to as “black boxes,” meaning it’s not always clear how they arrive at their decisions. This lack of transparency can be a problem for regulatory authorities that require an explainable AI. Lenders must ensure that their AI systems provide clear audit trails, documenting how credit decisions are made and ensuring that they align with regulatory standards.

Despite risks, responsible AI deployment can significantly strengthen both business efficiency and borrower protection.

Also Read: RBI Guidelines For Personal Loan Lending In India

What is The Future of AI in Lending?

AI is not static, its role in lending will continue to evolve rapidly.

1. Explainable and Ethical AI Models

As AI becomes increasingly embedded in lending, regulators and borrowers alike are demanding more transparency. In response to this, the development of explainable AI models is gaining traction. These models allow both borrowers and lenders to understand how decisions are made, ensuring fairness and accountability.

Regulatory pressure will only continue to grow, pushing lenders to build AI systems that are not only effective but also ethical and transparent.

2. Integration with Digital Identity and Open Banking

In the coming years, digital identity verification and open banking systems will play a key role in transforming how AI-driven lending operates. By securely sharing data between banks, lenders, and third-party providers, financial institutions will be able to offer faster, more secure, and convenient lending solutions.

These shared data ecosystems will ensure a more seamless, transparent process for borrowers while also improving fraud detection and credit risk assessments.

3. Wider Use Across Financial Products

AI's potential extends beyond just lending. In the future, AI is expected to improve savings products, insurance pricing, and investment advice by providing more tailored, data-driven solutions. For example, AI-powered models could help insurers better assess risk and personalise premiums or enable investors to receive real-time, AI-generated financial advice based on their risk profiles and goals.

How Pocketly Uses Modern Technology to Support Responsible Lending

AI tools can help people understand their spending and plan their monthly budgets. However, even with good planning, unexpected situations can create short-term money gaps.

In such moments, responsible access to small credit can help users manage essential expenses without long delays.

This is where Pocketly becomes useful for young Indians facing real emergencies.

Pocketly is a digital lending platform that leverages modern digital technology and streamlined data processing to help users access short‑term credit quickly and responsibly.

Here’s how Pocketly’s technology supports better lending outcomes:

- Digital, 100 % Online Process: From application to repayment, everything happens through the app, reducing paperwork and waiting times.

- Quick Eligibility Checks and Fast Approvals: Once you complete your KYC and provide basic details, Pocketly’s systems verify information quickly, often delivering approvals and disbursals within minutes.

- Instant Disbursal of Funds: After verification, approved loans are transferred directly to your bank account in seconds, helping you manage urgent needs without delay.

- Flexible Loan Options: Pocketly offers short‑term personal loans from as little as ₹1,000 up to ₹25,000, with repayment tenures you can choose to suit your budget (typically from 60 to 180 days).

- Transparent Costs & Terms: Interest rates start from about 2%–3% per month (APR varies), and there are no hidden charges. All fees and repayment details are shown clearly before you apply.

Download the Pocketly App to access quick, digital personal loans that fit real‑life cash needs with clear terms and minimal hassles.

Conclusion

AI in lending is transforming access to credit and operational efficiency, especially in markets like India, where digital adoption is high, and traditional credit histories are limited. By using diverse data sources, automating decisions, and enhancing risk models, AI is helping lenders deliver fairer, faster, and more inclusive lending solutions.

For borrowers, this means faster approvals, personalised credit options, and access where traditional models might fail. For platforms, AI enhances precision and scalability, but it also requires responsible deployment and strong data safeguards to protect users and ensure fairness.

In this evolving landscape, Pocketly offers a reliable solution for those needing fast, transparent credit. Whether it's covering unexpected expenses or managing cash flow,

Pocketly ensures that you stay on track with flexible lending options tailored to your needs. Download Pocketly today.

FAQs

1. What does AI in lending mean?

AI in lending refers to systems that use machine learning and data analytics to automate credit decisions, risk assessment, and fraud detection.

2. How does AI improve loan approvals?

AI speeds up credit decisions by analysing multiple data sources instantly and reducing manual processing time.

3. Can AI make lending fairer?

Yes, when designed responsibly, AI can reduce human bias and consider alternative data for more inclusive credit decisions.

4. Is AI safe for financial data?

Data security depends on the platform. Reputable lenders use encryption and strict protocols to protect data privacy.

5. Will AI replace human lenders?

AI enhances efficiency and automation, but human oversight remains important for ethical decisions and complex cases.