Lending plays a central role in modern finance, allowing individuals and businesses to access funds when needed and repay them over time. From everyday expenses to larger financial commitments, borrowing has become an essential part of managing money.

Over the years, lending and finance have moved beyond traditional systems. What once required lengthy paperwork and approvals is now increasingly handled through faster, digital processes. This shift is making credit more accessible while also changing how borrowers evaluate their options.

Understanding how lending works, the different types available, and how modern platforms fit into the system is key to making informed financial decisions. This guide breaks down the fundamentals of lending and finance, along with how evolving solutions are shaping access to credit today.

At a Glance

-

Lending is a core part of finance that helps individuals and businesses access funds and manage financial needs more effectively.

-

The lending process is shaped by factors such as borrower profile, repayment capacity, credit assessment, and loan terms.

-

Digital lending is changing finance by making credit faster to access, easier to apply for, and more flexible for different borrower needs.

-

Choosing the right lending platform depends not just on speed, but on cost, transparency, repayment fit, and overall borrowing context.

-

For short-term cash gaps, digital platforms can offer a more practical way to access limited credit without moving into long-term debt.

What Is Lending in Finance

Lending in finance refers to the process of providing money to an individual or business with the expectation that it will be repaid over time, usually with interest. It is a core function of the financial system that allows funds to move from those who have surplus capital to those who need it.

At a basic level, lending involves three key components:

-

Borrower: The individual or business that requires funds

-

Lender: The bank, financial institution, or platform that provides the loan

-

Repayment terms: The conditions under which the borrowed amount is returned, including interest, tenure, and schedule

Lending plays a significant role in both personal and economic activity. For individuals, it helps manage expenses, handle emergencies, or fund major purchases. For businesses, it supports operations, expansion, and investment.

Within the broader financial system, lending helps maintain liquidity and enables continuous economic movement. Understanding this foundation makes it easier to explore different types of lending and how modern financial solutions are evolving.

Also Read: AI in Lending: Transforming Credit Access, Speed, And Efficiency

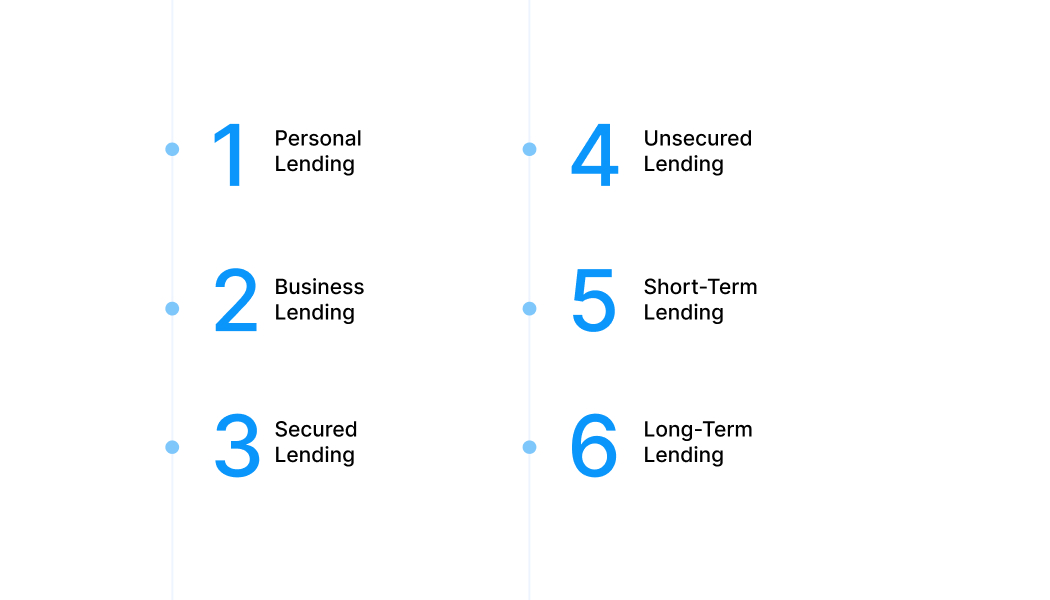

Types of Lending in Finance

Lending in finance exists in multiple forms, each designed to serve a specific purpose based on the borrower’s needs, risk profile, and repayment capacity. Understanding these types helps in identifying the most suitable form of credit for a given situation.

Here are the main types of lending:

-

Personal lending: Loans taken by individuals for expenses such as medical needs, education, travel, or general consumption. These are usually unsecured and depend on income and credit profile.

-

Business lending: Loans provided to businesses for working capital, operations, or expansion. These can be secured or unsecured, depending on the scale and requirement.

-

Secured lending: Requires collateral such as property, gold, or other assets. Since the lender’s risk is lower, these loans often come with relatively lower interest rates.

-

Unsecured lending: Does not require collateral. Approval is based on creditworthiness, income stability, and repayment history, which usually results in higher interest rates.

-

Short-term lending: Designed for immediate financial needs with shorter repayment cycles. These loans focus on quick access and faster closure.

-

Long-term lending: Used for larger financial commitments such as home loans or business investments, with extended repayment periods.

Each type serves a different financial need, and the right choice depends on factors such as urgency, loan amount, and repayment ability. Understanding these categories provides a clearer view of how lending fits into the broader financial system.

Also Read: AI in Finance: How It Is Changing Your Money?

How the Lending Process Works

The lending process in finance follows a structured flow that helps lenders assess risk while ensuring borrowers understand their obligations. Although the exact steps may vary across institutions, the overall process remains consistent.

Here is how it typically works:

-

Application: The borrower applies for a loan by providing basic details such as identity, income, and the required loan amount through a bank or digital platform.

-

Credit Assessment: The lender evaluates the borrower’s profile using factors like credit score, income stability, repayment history, and in some cases, transaction behaviour.

-

Approval Decision: Based on this assessment, the lender approves or rejects the application. If approved, the loan amount, interest rate, and repayment terms are defined.

-

Disbursal: The approved amount is transferred to the borrower’s bank account. Traditional lenders may take longer, while digital platforms often complete this step faster.

-

Repayment: The borrower repays the loan according to the agreed schedule, which may involve EMIs or a short-term repayment cycle depending on the loan type.

Each stage is designed to balance accessibility with risk management. Understanding this process helps borrowers make better decisions when selecting a lending option.

How Digital Lending Is Changing Finance

Lending is no longer limited to traditional banks and long approval cycles. Digital platforms are reshaping how credit is accessed by making the process faster, more flexible, and easier to navigate.

With the rise of fintech solutions, borrowers can now complete most of the lending journey online. From application to disbursal, the process is designed to reduce delays and simplify access to funds.

Key changes include:

-

Faster access to credit: Digital platforms significantly reduce approval and disbursal time, allowing borrowers to access funds when timing is critical.

-

Simplified application process: Minimal documentation and basic KYC requirements replace lengthy paperwork.

-

Data-driven credit assessment: Lenders use alternative data such as transaction history and income patterns, in addition to traditional credit scores.

-

Improved accessibility: More individuals, including those with limited credit history, can access lending options through digital platforms.

This shift is expanding how lending fits into everyday financial decisions. Borrowers now have more flexibility in how and when they access credit, making it important to evaluate these options carefully within the broader financial system.

Explore how digital lending works in practice. Download Pocketly to access short-term credit quickly when you need it.

Also Read: Digital Lending In India: Future Trends And Insights

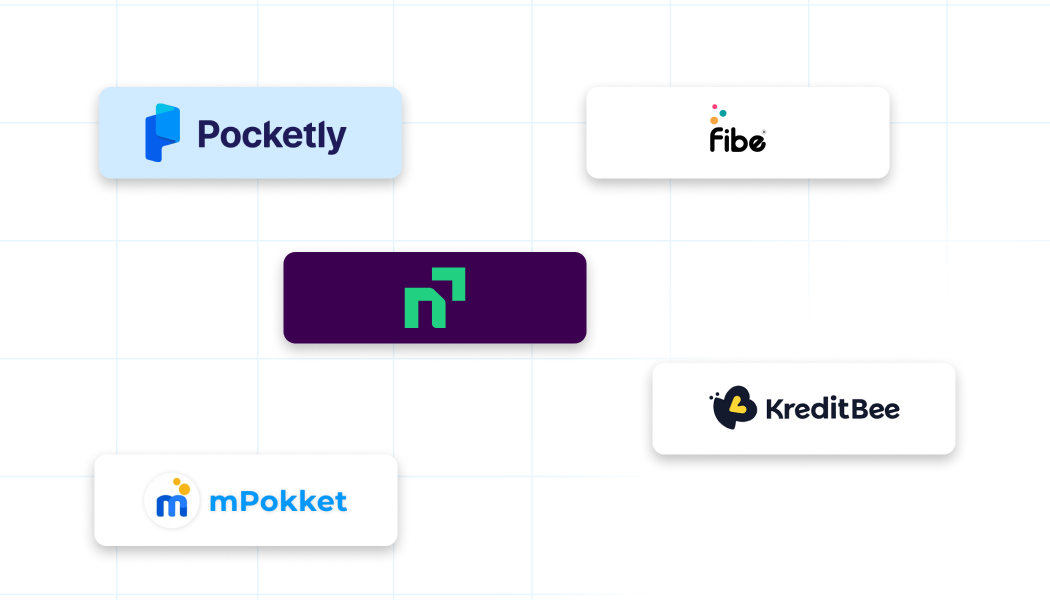

Examples of Digital Lending Platforms in India

As digital lending becomes a more visible part of the financial ecosystem, several platforms in India are making credit access faster and more convenient through app-based and fully online processes. These platforms reduce dependence on branch visits, simplify documentation, and offer different borrowing formats based on user needs.

Some commonly used digital lending platforms include:

Pocketly

Pocketly is designed for smaller, short-term borrowing needs and is often positioned for users who want a quick and simple digital experience. It is more suited to situations where the requirement is immediate and limited in amount, rather than a large, long-term credit need. The platform focuses on ease of access, minimal friction in the application process, and repayment structures that align better with short-term borrowing behaviour.

KreditBee

KreditBee offers digital personal loan solutions with a wider borrowing range and more structured repayment options. It is often considered by borrowers who need more than a small-ticket loan and want the convenience of a digital process. Compared to platforms focused only on short-term borrowing, KreditBee can appeal to users looking for greater flexibility in loan size and tenure.

If you need quick access to small-ticket credit, download Pocketly to check your eligibility and apply within minutes.

mPokket

mPokket is commonly associated with students and young earners who may be accessing credit for the first time. Its model is built around smaller loan amounts, relatively simpler onboarding, and quick processing. This makes it more accessible for users who may not have an extensive credit history but still need a short-term borrowing option for immediate expenses.

Fibe (EarlySalary)

Fibe offers digital lending solutions with an emphasis on speed and flexibility, particularly for salaried users. It is often used by borrowers looking for instant access to funds without going through a traditional loan process. Its positioning within digital lending reflects the shift toward faster approvals and more user-friendly repayment structures in the consumer finance space.

Navi

Navi provides fully digital personal loans and is known for offering a streamlined user journey from application to disbursal. It is typically more relevant for users who value a simple interface, quick digital processing, and competitive loan terms based on eligibility. As part of the digital lending landscape, Navi reflects how financial products are being redesigned for convenience and scale.

Together, these platforms show how lending in India is moving toward faster, technology-driven access to credit. At the same time, they also highlight an important reality: digital convenience does not make every option suitable for every borrower. The right platform depends on the loan amount required, repayment capacity, urgency, and overall borrowing context.

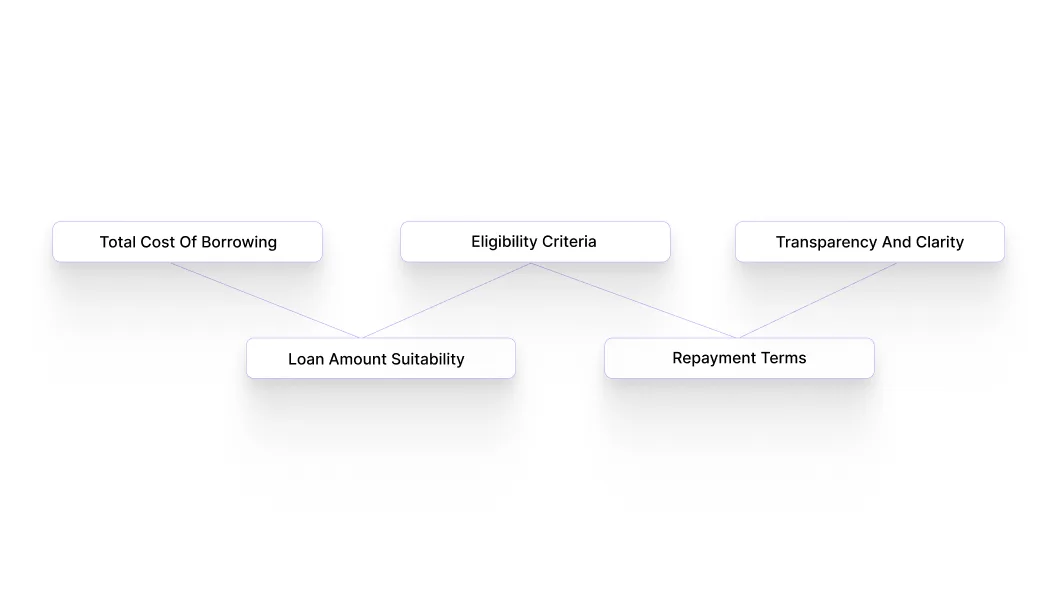

How to Choose the Right Lending Platform

With multiple digital options available, choosing a lending platform requires more than just looking at how quickly funds are disbursed. The right choice depends on how well the loan fits your financial needs and how manageable it is to repay.

Here are the key factors to consider:

-

Total cost of borrowing: Interest rates alone do not reflect the full cost. Processing fees, platform charges, and penalties can significantly increase the final repayment amount.

-

Loan amount suitability: Borrowing more than required can increase financial pressure, while borrowing too little may not solve the problem. The loan amount should match the immediate need.

-

Eligibility criteria: Different platforms use different evaluation methods. Some rely heavily on credit scores, while others also consider income flow or transaction behaviour.

-

Repayment terms: It is important to understand the repayment timeline, due dates, and any penalties for delays. Short-term loans require clear repayment planning.

-

Transparency and clarity: A reliable platform clearly communicates all terms, including costs, repayment structure, and conditions, before the loan is accepted.

Choosing a lending platform is ultimately about balance. The goal is to access credit when needed while ensuring that the repayment remains practical and does not create additional financial strain.

Also Read: RBI Guidelines For Personal Loan Lending In India

Manage Short-Term Cash Needs More Efficiently with Pocketly

Even with proper financial planning, short-term cash gaps can still occur. A bill may be due before your salary arrives, or an unexpected expense may need immediate attention. In such situations, access to small, timely credit can help maintain financial stability without disrupting your overall budget.

This is where platforms like Pocketly fit into the modern lending ecosystem. Instead of pushing large loans or long commitments, it focuses on quick access to smaller amounts that are easier to manage within a short repayment cycle.

Here is how it supports short-term borrowing needs:

-

Loan amounts suited for small needs: Borrow between ₹1,000 and ₹25,000 based on your requirement

-

Fast digital process: Complete your application and KYC online with minimal documentation

-

Quick disbursal: Once approved, funds can be transferred within minutes to your bank account

-

Flexible repayment options: Choose repayment periods typically ranging from 60 to 180 days

-

Accessible to wider users: Available for students, salaried, and self-employed individuals with a steady income

-

Transparent cost structure: Interest generally starts around 2% per month, with clearly defined fees

This approach allows borrowers to handle immediate expenses without committing to larger, long-term debt. The focus remains on controlled borrowing, where the amount and repayment cycle stay aligned with short-term cash flow.

Used responsibly, digital lending solutions like Pocketly can act as a practical financial bridge during temporary gaps, helping you stay on track without added financial strain.

Make informed borrowing decisions and download Pocketly on iOS or Android to manage short-term financial needs with a faster, digital process.

FAQs

Q: What is lending in finance?

Lending in finance is the process of giving money to a borrower with the expectation that it will be repaid over time, usually with interest. It is a core part of the financial system that helps individuals and businesses access funds when needed.

Q: What is the difference between finance and lending?

Finance is a broader concept that includes managing money, investments, savings, and credit. Lending is one part of finance that specifically deals with providing loans and recovering them through structured repayment.

Q: What are the 4 pillars of lending?

The four pillars of lending are creditworthiness, capacity, collateral, and conditions. These factors help lenders assess whether a borrower is reliable and whether the loan can be repaid responsibly.

Q: What is short-term lending in finance?

Short-term lending refers to borrowing for a shorter repayment period, usually to manage urgent or temporary financial needs. It is commonly used for smaller amounts and works best when repayment visibility is clear.

Q: How do you choose the right digital lending platform?

The right digital lending platform should offer transparent charges, suitable loan amounts, and repayment terms that are easy to manage. For smaller and short-term borrowing needs, platforms like Pocketly can be relevant because they are designed for quick access and limited loan requirements.