Managing financial services has become a daily responsibility for individuals, not just institutions. From bank accounts and insurance policies to credit cards, digital lending apps, and investment platforms, most Indians now interact with multiple financial services every month.

India has over 2.2 billion bank accounts, rapid growth in NBFC and fintech lending, and one of the world’s largest digital payments ecosystems. Yet, many users access financial products without a clear plan for managing them together.

Poor coordination between credit, savings, insurance, and payments often leads to missed dues, cash stress, and over-reliance on short-term borrowing.

This guide explains the management of financial services, why it matters at an individual level, and how smarter management leads to better financial control and stability.

Key Takeaways

- Managing financial services means coordinating banking, credit, insurance, savings, and investments so money flows smoothly without stress.

- Poor coordination, not low income, is a major cause of missed payments, cash gaps, and over-reliance on short-term borrowing.

- Key services that need active management include bank accounts, credit products, insurance policies, and savings or investment tools.

- Simple systems work best, such as centralising visibility, aligning each product with a clear purpose, and reviewing cash flow weekly.

- Common challenges include scattered financial apps, irregular income with fixed expenses, and short-term timing gaps between bills and salary.

- Responsible tools like Pocketly can support financial management by bridging temporary cash gaps without disrupting long-term stability.

A Brief Look Into The Management of Financial Services

Management of financial services refers to how individuals plan, use, monitor, and coordinate different financial products in daily life. This includes banking accounts, credit products, insurance policies, and investment tools.

The focus is not on using more financial products, but on using the right ones at the right time. Proper management ensures your money flows smoothly, costs stay controlled, and financial decisions remain aligned with your needs.

When financial services are managed well, they support stability and flexibility. When they are unmanaged, they often lead to confusion, missed payments, or unnecessary borrowing.

Financial Services vs Financial Management

It’s easy to confuse financial services with financial management, but they serve different purposes.

- Financial services are the products offered by institutions, such as bank accounts, loans, insurance policies, and finance apps.

- Financial services management is how you organise, track, and control those products in real life.

Good management helps prevent overlap between services, avoids hidden costs, and ensures each product serves a clear purpose instead of adding complexity.

Once the concept is clear, the next step is understanding which services actually need active management.

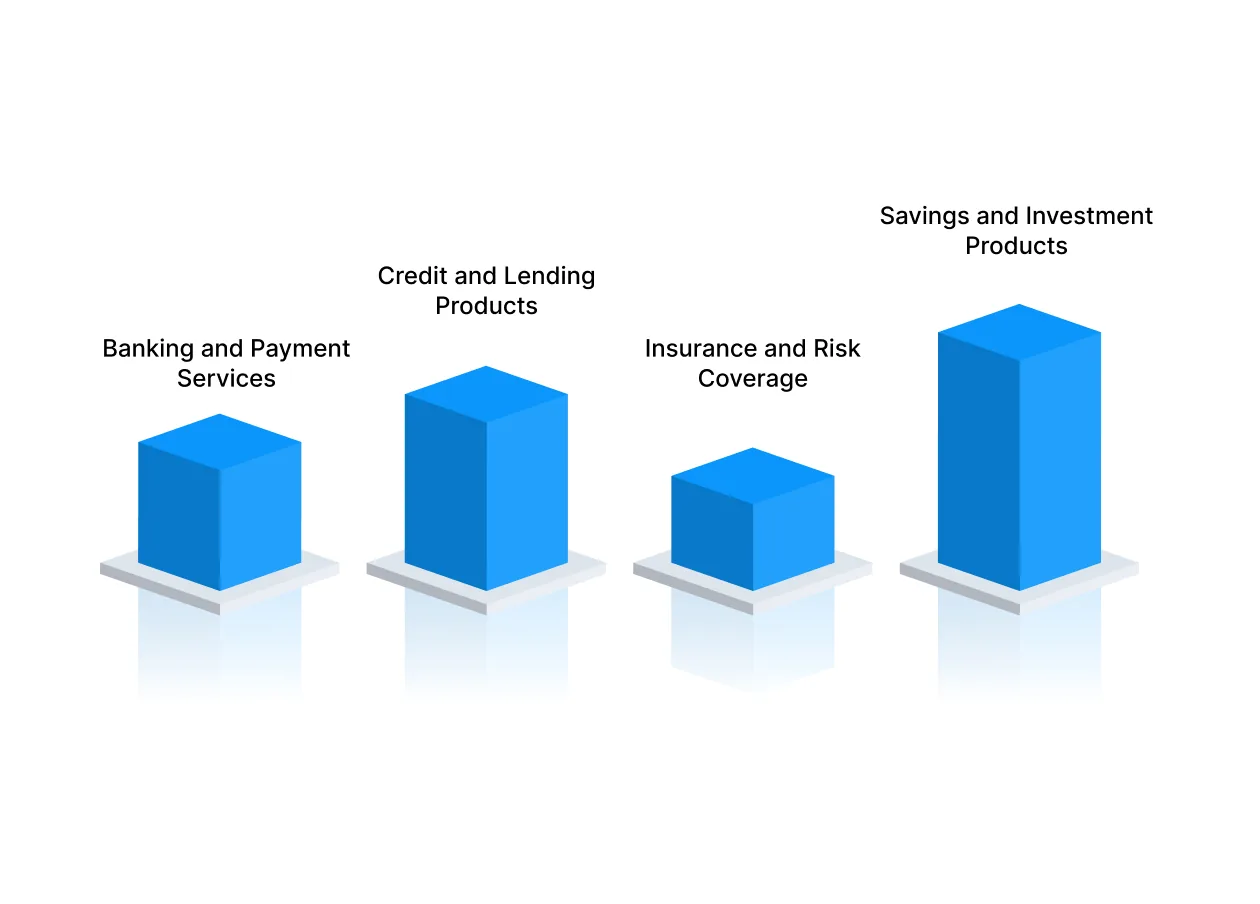

Key Financial Services That Require Active Management

Effective management starts with knowing where attention is actually required. Not all financial services demand the same level of involvement, but ignoring the critical ones can quietly create stress, penalties, and long-term instability.

Banking and Payment Services

Banking sits at the centre of everyday financial activity, which makes it easy to overlook problems until they compound. Active oversight ensures that money flows smoothly without friction.

This includes:

- Savings and current accounts used for salary credits, routine spending, and bill payments

- Digital payments and UPI links, including merchant mandates and recurring auto-debits

- Salary credits, bill settlements, and balance monitoring to avoid overdrafts or declined payments

Without regular checks, small inefficiencies creep in. Duplicate subscriptions, inactive accounts holding idle balances, or forgotten auto-debits can slowly erode financial efficiency. Over time, these leaks reduce usable cash and increase mental load without offering any real value.

Credit and Lending Products

Credit products demand the highest level of attention because mistakes carry both immediate costs and long-term consequences.

This category includes:

- Credit cards, EMIs, BNPL plans, and short-term loans

- Interest rates, repayment schedules, minimum dues, and utilisation limits

Poor credit management often starts with minor oversights, missing a due date by a day, carrying high utilisation for too long, or stacking short-term credit without a repayment plan. These quickly translate into late fees, rising interest costs, and unnecessary pressure.

Structured tracking keeps borrowing intentional. When credit is monitored properly, it serves a clear purpose, such as bridging timing gaps or funding planned expenses, rather than becoming a default solution for cash shortfalls.

Insurance and Risk Coverage

Insurance exists to protect against financial shocks, but it only works when policies are kept current and aligned with real needs.

Active management includes:

- Health, life, and asset insurance policies

- Premium schedules, renewal dates, and policy terms

- Periodic coverage reviews as income, dependents, or assets change

Unmanaged insurance can be as risky as having no insurance at all. Lapsed premiums, outdated coverage amounts, or missing riders often surface only during emergencies. Regular review ensures protection remains relevant and prevents expensive gaps during critical moments.

Savings and Investment Products

Savings and investments are designed for the future, but they still require periodic alignment and oversight.

This includes:

- Fixed deposits, mutual funds, SIPs, and other investment instruments

- Liquidity planning for emergencies and near-term needs

- Matching investments with time horizons and risk tolerance

Without management, money can become either too locked in or too exposed. Over-investing without liquidity creates stress during emergencies, while excess idle savings lose value over time. Active oversight ensures funds remain accessible when needed while still supporting long-term growth.

Managing these services well requires a structured approach rather than reactive decisions, which is where clear strategies become essential.

Why Management of Financial Services Matters Today

Managing financial services has become harder because money now moves across multiple platforms at once. Salaries arrive in one account, expenses flow through cards and UPI, subscriptions run silently in the background, and credit repayments follow fixed dates. Without coordination, even people with stable incomes can feel constant cash pressure.

Effective management brings these moving parts into one clear system, reducing stress and uncertainty.

1. Prevents cash flow mismatches

When income and expenses are not aligned, short-term stress builds quickly.

- Aligns income timing with expenses and repayments: Ensures bills and EMIs match when money actually comes in.

- Reduces last-minute financial stress: Fewer urgent scrambles to cover routine payments.

Managing timing is often more important than increasing income.

2. Reduces over-reliance on credit

Credit becomes risky when it is used out of habit rather than need.

- Helps distinguish genuine needs from convenience borrowing: Prevents using credit for avoidable lifestyle expenses.

- Supports disciplined credit usage: Keeps borrowing intentional and controlled.

Good management keeps credit as a support tool, not a dependency.

3. Improves financial confidence

Clarity changes how money decisions feel.

- Clear view of obligations and available funds: You know what is due and what remains at any point.

- Fewer surprises and missed payments: Predictability replaces anxiety.

Confidence grows when finances stop feeling reactive.

With the importance of financial services management clear, let’s look at practical methods to manage them effectively.

Also Read: 10 Essential Financial Habits For Success

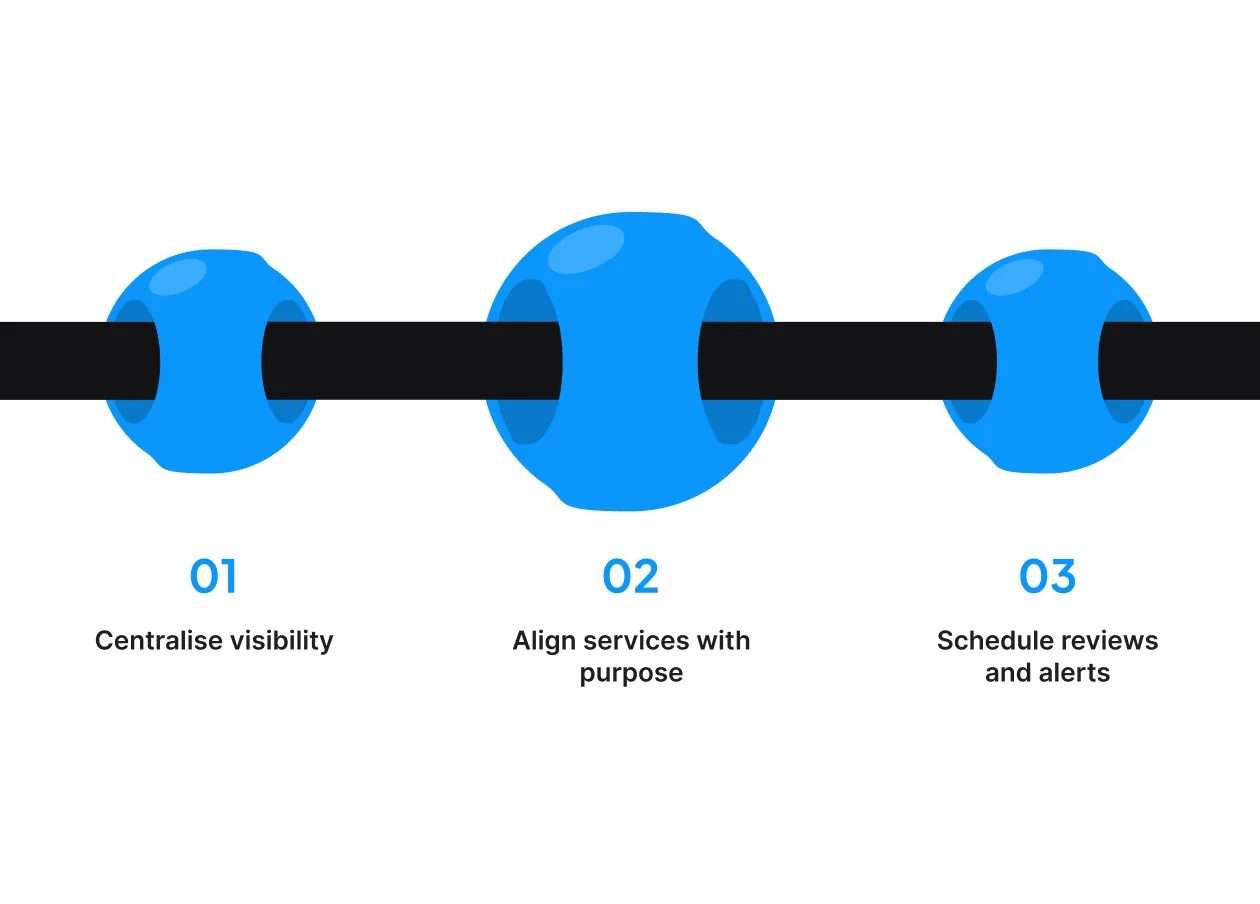

3 Practical Strategies for Managing Financial Services Effectively

Managing financial services does not require complicated spreadsheets or constant monitoring. Simple, repeatable systems create better control and reduce mental load.

1. Centralise visibility

Fragmentation creates confusion. Centralisation creates clarity.

- Track all accounts, loans, and subscriptions in one place: A single view prevents overlooked payments or idle balances.

- Know total monthly obligations at a glance: Helps plan spending without guesswork.

Visibility is the foundation of good financial control.

2. Align services with purpose

Each financial product should serve a clear role.

- Use savings for buffers, not daily spending: Protects emergency funds from erosion.

- Use credit only for timing gaps or planned needs: Prevents long-term pressure from short-term borrowing.

Purpose-driven usage reduces overlap and unnecessary costs.

3. Schedule reviews and alerts

Consistency matters more than intensity.

- Weekly cash flow checks: Catch issues early, before they grow.

- Auto-alerts for dues and low balances: Reduce reliance on memory and manual tracking.

Automation supports discipline without constant effort.

Even with planning, gaps can still occur when income and expenses don’t align.

Also Read: 10 Smart Spending Tips For Financial Wellness

Common Challenges in Managing Financial Services

Even with the right intent, managing multiple financial services can become overwhelming. Most challenges do not come from lack of income, but from poor coordination between products, timing, and obligations.

Too many products, no coordination

Modern finance offers convenience, but it also creates clutter.

- Multiple apps and lenders create confusion: Accounts, cards, loans, and subscriptions sit across platforms with no single view.

- Missed dues despite sufficient income: Payments slip simply because reminders and tracking are scattered.

Without coordination, money management becomes reactive instead of planned.

Irregular income and fixed commitments

This challenge is common among students, freelancers, and gig workers.

- Income varies, but expenses stay fixed: Rent, subscriptions, and EMIs do not adjust to low-income months.

- Requires flexible cash flow planning: Budgets must adapt to minimum guaranteed income, not best-case scenarios.

Rigid systems often fail where income is unpredictable.

Short-term cash gaps

Timing mismatches are one of the most common financial stress points.

- Bills arrive before salary: Even a few days’ delay can disrupt planned payments.

- Emergencies disrupt planned budgets: Medical needs or urgent repairs break otherwise balanced systems.

These gaps do not reflect poor habits, just timing issues.

This is where responsible short-term financial tools like Pocketly play a supporting role.

If you need a quick buffer for essentials, Pocketly offers short-term loans from ₹1,000 to ₹25,000 through a fully digital process, so you can cover urgent bills and stay on schedule. Download the Pocketly App today.

Also Read: Different NBFC Types in India: A Guide For 2026

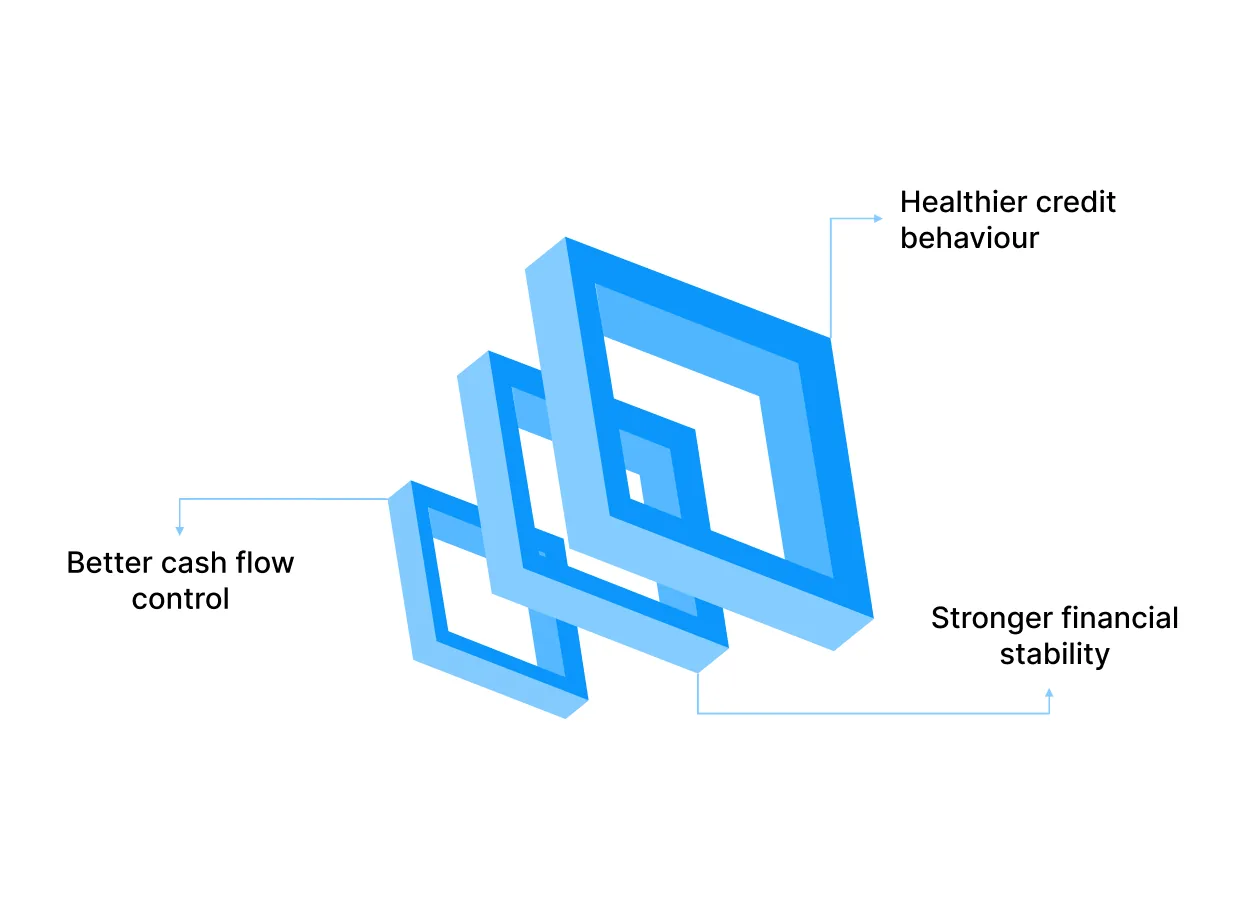

Long-Term Benefits of Managing Financial Services Well

Consistent management compounds into stability.

When financial services are managed intentionally over time, the benefits go beyond short-term relief. Small, disciplined actions gradually create stronger control, confidence, and resilience.

Better cash flow control

Good management reduces uncertainty in day-to-day finances.

- Fewer surprises: Bills, repayments, and subscriptions are anticipated instead of reacting at the last moment.

- Predictable monthly planning: Income and expenses align more closely, making planning calmer and more reliable.

Clear visibility helps money move with purpose rather than urgency.

Healthier credit behaviour

Credit works best when it supports flexibility, not pressure.

- Timely repayments: Clear tracking of dues reduces missed or delayed payments.

- Lower stress around borrowing: Credit is used intentionally for timing gaps, not routine dependence.

Over time, this builds confidence and steadier credit habits.

Stronger financial stability

Long-term stability comes from separating needs by time horizon.

- Emergency readiness: Savings and buffers reduce panic during unexpected situations.

- Clear separation between short-term needs and long-term goals: Daily expenses no longer interfere with future plans like education or asset building.

This balance keeps financial systems steady even during disruptions.

How Pocketly Supports Better Management of Financial Services

Short-term liquidity is a practical part of managing financial services effectively. Even well-structured systems can strain when expenses arrive before income. Missing payments can undo careful planning and create unnecessary stress.

Pocketly is a digital lending platform that supports financial service management by helping users handle timing gaps without breaking their overall system.

How Pocketly helps

- Short-term loans from ₹1,000 to ₹25,000: Designed for genuine cash gaps, not long-term borrowing.

- Fast, fully digital access: Quick KYC and approvals reduce friction during urgent needs.

- Transparent pricing: Interest starts at 2% per month, with clearly defined costs upfront.

- Prevents service disruptions: Helps cover EMIs, bills, or essential payments on time.

Pocketly works best as a support layer, not a replacement for budgeting or planning. Used responsibly, it helps maintain stability when timing goes off.

Download the Pocketly app to manage short-term needs without breaking your financial system.

Conclusion

Managing financial services is no longer optional. With multiple products influencing daily cash flow, credit health, and security, individuals must actively coordinate how financial services are used.

By understanding your services, aligning them with purpose, and planning for timing gaps, you gain control instead of reacting under pressure. While unexpected expenses may still arise, responsible short-term support can protect your system rather than disrupt it.

Use Pocketly to support short-term needs while keeping your overall financial management intact. Download the App today.

FAQs

1. Why is managing financial services important for individuals?

It helps prevent cash stress, missed payments, and unnecessary borrowing.

2. What are some common mistakes in financial services management?

Using too many products without tracking, ignoring repayment schedules, and relying on credit for routine expenses.

3. How can short-term loans fit into financial services management?

They help bridge temporary cash gaps when used responsibly and repaid on time.

4. Is Fintech part of financial services management?

Yes. Fintech tools help track, access, and manage financial services more efficiently.