Your CIBIL score plays an important role in loan approvals, credit card eligibility, and even the interest rates lenders offer you. As digital lending grows rapidly in India, maintaining a healthy credit profile is becoming more important than ever.

According to an RBI-backed industry survey, many banks expect digital lending to account for a major share of future credit growth, making credit awareness increasingly essential.

Despite this, many borrowers still believe that factors like salary, savings balance, debit card usage, or checking their own credit score can lower their CIBIL score. In reality, several of these assumptions are simply myths.

Understanding what truly affects your CIBIL score can help you avoid common mistakes, build stronger financial habits, and improve your chances of accessing credit when you need it. In this guide, we'll break down the myths, explain the real scoring factors, and highlight the habits that matter most for maintaining a healthy credit profile.

TL;DR

-

Your salary, savings balance, debit card usage, and marital status do not directly affect your CIBIL score.

-

CIBIL scores are mainly based on repayment history, credit utilisation, credit enquiries, credit mix, and loan history.

-

Checking your own CIBIL score is a soft enquiry and does not lower your score.

-

Common mistakes like late payments, maxing out credit cards, and multiple loan applications can hurt your credit profile.

-

Responsible borrowing, timely repayments, and regular credit report checks help maintain a healthy CIBIL score.

Why People Get Confused About What Affects a CIBIL Score

Many people assume that anything influencing loan approval must also affect their CIBIL score. In reality, lenders assess far more information than what is used to calculate a score.

A CIBIL score is generated from credit history like loan repayments, credit card usage, debt, and credit enquiries. However, lenders also evaluate factors outside this calculation, including income, employment stability, and financial obligations like rent and household expenses. These don't affect your score but influence lending decisions.

A simpler way to understand the difference between CIBIL score and loan approval is to think of your CIBIL score as a record of how you have handled borrowed credit in the past. Loan approval, on the other hand, combines that credit history with additional information about your current financial situation.

This is why someone with a strong CIBIL score may still face challenges if their income is insufficient for a particular loan, while someone with a moderate income can maintain an excellent score through responsible credit behaviour.

Next, let's look at the common factors people worry about and why they do not actually affect your CIBIL score.

Factors That Do Not Affect Your CIBIL Score and Why

Income and Salary

Your CIBIL score measures how responsibly you manage borrowed credit, not how much you earn. Credit bureaus assess repayment history, credit utilisation, length of credit history, credit mix, and recent enquiries. Your salary is not included in this calculation.

A high earner with frequent late payments or high credit card balances will have a lower score than a modest earner who pays bills on time. Income doesn't influence your score, though lenders do consider it when assessing repayment capacity and deciding loan amounts.

Key distinction:

-

CIBIL score measures credit behaviour

-

Income measures repayment capacity

-

Lenders evaluate both separately

Understanding this helps you focus on credit management rather than worrying about salary levels alone.

Savings Account Balance and Investments

Many people believe that maintaining a large savings account balance or investing regularly will automatically improve their CIBIL score. This assumption often comes from the idea that having more money makes you financially stronger and therefore more creditworthy. While strong savings and investments can support your overall financial health, they do not directly influence your CIBIL score.

Your CIBIL score is based on credit history, not assets. Credit bureaus track loan repayments, credit card usage, outstanding balances, and enquiries. They do not consider savings account balances, fixed deposits, mutual funds, stocks, or other investments.

Debit Card Transactions

Debit card activity does not affect your CIBIL score because no borrowing is involved. Debit cards use your own money and are not reported to credit bureaus. Credit cards, by contrast, involve borrowed funds that must be repaid, and this repayment behaviour forms part of your credit history.

The confusion arises because debit and credit transactions look similar from a user perspective, but credit bureaus treat them very differently. Making hundreds of debit transactions monthly reflects active banking, but does not contribute to your CIBIL score.

Key distinction:

-

Debit card = spending your own money (no credit history impact)

-

Credit card = borrowing money (affects CIBIL score based on repayment)

Someone using only a debit card will not build a credit history. If your goal is to build creditworthiness, focus on responsible credit use and timely repayment rather than debit card spending.

Marriage and Personal Demographics

Your CIBIL score is linked to your individual credit profile based on your own borrowing and repayment history. Getting married does not merge credit records, combine scores, or transfer a spouse's credit history to your report. Personal demographics such as marital status, gender, religion, caste, or residence also do not affect your CIBIL score.

A person with a strong credit history will not see their score change simply by marrying someone with poor credit. Each person's score remains independent and reflects only their own credit behaviour.

One exception: Joint credit products

If both partners apply for a joint loan or become co-borrowers, repayment activity appears on both records. Missed payments on jointly held accounts affect both credit profiles because both are responsible for repayment. This impact comes from shared borrowing responsibility, not from marriage itself.

Checking Your Own CIBIL Score

Checking your own CIBIL score does not lower it. The confusion comes from credit enquiries: lender checks (hard enquiries) may have a small impact on your score, but checking your own score (soft enquiry) does not affect calculations.

Soft enquiries are visible only to you and are not used in score calculations. Many borrowers avoid checking for months or years, only to discover errors, outdated information, or missed payments when applying for loans. Identifying issues early gives you time to correct them and improve your profile before seeking new credit.

A simple comparison makes the distinction clearer:

|

Type of Enquiry |

Who Initiates It? |

Impact on CIBIL Score |

|

Soft Enquiry |

You checking your own score |

No impact |

|

Hard Enquiry |

Lender reviewing your profile for a credit application |

May have a minor impact if repeated frequently |

Benefits of regular checks:

-

Track your credit standing

-

Spot discrepancies early

-

Make informed borrowing decisions

-

Maintain a healthier credit profile

Periodic self-checks help you understand your position and make better financial decisions rather than harming your score.

Also read: Steps for CIBIL Consumer Member Login and Score Check

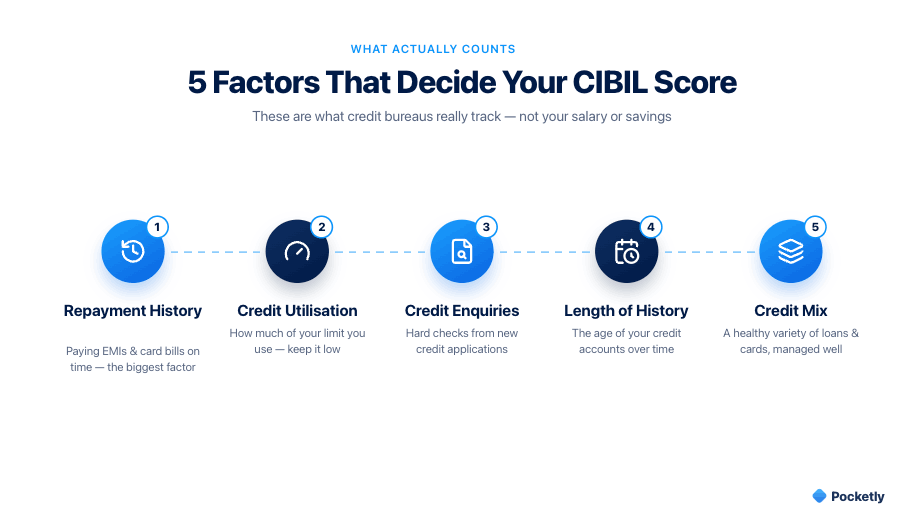

What Actually Impacts Your CIBIL Score

Now that we've covered the factors that do not affect your CIBIL score, it's equally important to understand what actually does.

Repayment History

Your repayment history is generally considered the most important factor influencing your CIBIL score. It reflects how consistently you have repaid borrowed credit, including loan EMIs and credit card bills.

Missing payments, paying after the due date, or defaulting on a loan can negatively affect your score because it signals potential repayment risk. Even a few late payments can remain visible on your credit report for years.

Setting up payment reminders or auto-debit instructions can reduce the chances of missing due dates.

Credit Utilisation Ratio

Credit utilisation refers to the percentage of your available credit limit that you are currently using. It is particularly relevant for credit card users.

For example, if your credit card limit is ₹1 lakh and your outstanding balance is ₹30,000, your credit utilisation ratio is 30%.

A high utilisation ratio may indicate that you rely heavily on borrowed credit, which lenders could view as a potential risk. In contrast, maintaining moderate utilisation levels suggests better financial management.

Some common habits that can increase credit utilisation include:

-

Frequently maxing out credit cards

-

Carrying large outstanding balances month after month

-

Using most of the available credit limit even when payments are made on time

Keeping credit card balances under control and paying outstanding amounts regularly can support a healthier credit profile.

Multiple Credit Applications

Every time you apply for a loan or credit card, the lender may conduct a hard enquiry on your credit report. While a single enquiry is generally not a cause for concern, submitting several applications within a short period can have an impact.

Multiple hard enquiries may indicate that a borrower is actively seeking credit from multiple sources. As a result, lenders may perceive higher borrowing risk.

Before applying for new credit, it is often helpful to review eligibility requirements and compare options carefully rather than submitting multiple applications at once.

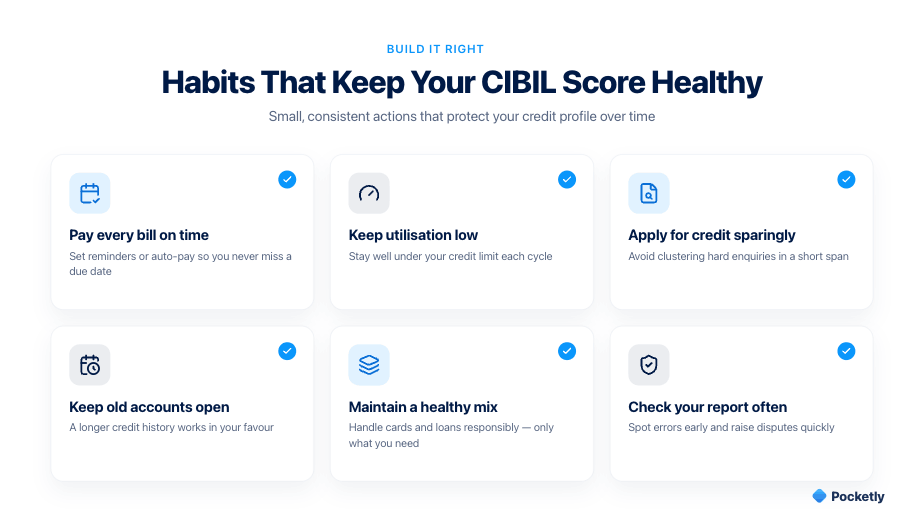

Length of Credit History

The age of your credit accounts also contributes to your CIBIL score. A longer credit history provides lenders with more information about your borrowing and repayment behaviour over time.

Older, well-managed accounts can demonstrate stability and responsible credit usage. This is one reason why maintaining long-standing credit accounts in good standing can be beneficial.

While you cannot instantly increase the length of your credit history, maintaining older accounts responsibly can contribute positively over time.

Also read: Credit History Meaning: The Ultimate 2026 Guide for Young Indians

Credit Mix

Credit mix refers to the variety of credit products you manage. Credit bureaus may view experience with different types of credit as an indicator of responsible borrowing behaviour.

Common credit products include:

-

Credit cards

-

Personal loans

-

Auto loans

-

Home loans

-

Consumer durable loans

A balanced credit profile often demonstrates that a borrower can handle different forms of credit responsibly. However, this does not mean you should take additional loans solely to improve your credit mix. The focus should always remain on borrowing based on genuine needs and managing existing obligations responsibly.

Quick Comparison: What Affects vs What Does Not Affect Your CIBIL Score

Common Mistakes That Can Lower Your Score Without You Realising

Many borrowers focus on improving their CIBIL score but overlook everyday habits that can gradually damage it. Some of these mistakes may seem minor at first, yet they can create negative signals on your credit report over time. Knowing what to avoid is just as important as understanding the factors that improve your score.

Missing Minimum Payments or Paying Late

One of the quickest ways to hurt your CIBIL score is by missing payment due dates. This applies to both loan EMIs and credit card bills.

Even if you eventually clear the outstanding amount, late payments can be reported to credit bureaus and remain visible on your credit history. Repeated delays may make lenders view you as a higher-risk borrower.

To avoid this:

-

Set payment reminders before due dates

-

Enable auto-pay where possible

-

Track all active loans and credit cards in one place

Paying on time consistently is one of the most effective ways to maintain a healthy credit profile.

Maxing Out Your Credit Cards

Using most or all of your available credit limit can negatively affect your credit utilisation ratio, even when payments are made on time.

For example, if your credit card has a limit of ₹50,000 and your outstanding balance regularly stays close to that amount, lenders may interpret this as heavy dependence on credit.

Common warning signs include:

-

Frequently reaching the credit limit

-

Carrying high balances month after month

-

Using multiple cards to cover regular expenses

Keeping credit utilisation under control can help demonstrate responsible credit management.

Applying for Multiple Loans at the Same Time

When faced with an urgent financial need, some borrowers submit applications to several lenders simultaneously in the hope of increasing approval chances. However, each application can trigger a hard enquiry on the credit report.

A cluster of hard enquiries within a short period may indicate aggressive credit-seeking behaviour. This can raise concerns among lenders and potentially affect your score.

Instead of applying everywhere at once:

-

Review eligibility criteria beforehand

-

Compare options carefully

-

Apply only to lenders that are a good fit for your profile

A more targeted approach can reduce unnecessary credit enquiries.

Ignoring Errors in Your Credit Report

Credit reports are not immune to mistakes. Incorrect personal details, duplicate loan entries, inaccurate payment records, or loans that do not belong to you can sometimes appear on a report.

Many people only discover these issues when applying for a loan or credit card, by which point the error may already have affected lending decisions.

Regularly reviewing your credit report helps you:

-

Identify inaccuracies early

-

Raise disputes with the relevant credit bureau

-

Ensure your credit history accurately reflects your repayment behaviour

Monitoring your report periodically is a simple habit that can prevent avoidable credit problems.

Settling a Loan Instead of Fully Repaying It

When borrowers face repayment difficulties, lenders may occasionally offer a settlement option for less than the total amount owed. While this can help resolve an immediate financial challenge, it is important to understand the potential impact on your credit profile.

A loan marked as "settled" indicates that the debt was not repaid in full according to the original agreement. Future lenders may view this differently from a loan marked as "closed" after complete repayment.

Before accepting a settlement:

-

Understand the long-term implications

-

Discuss available repayment alternatives with the lender

-

Consider whether full repayment is possible

Whenever feasible, closing a loan through complete repayment generally reflects more positively on your credit history.

A Small Mistake Today Can Affect Future Borrowing

Many credit score problems do not result from major financial mistakes but from small, repeated habits that go unnoticed. Missing a payment, ignoring a reporting error, or repeatedly applying for new credit can gradually weaken an otherwise healthy profile.

The good news is that most of these issues are preventable. By understanding the common pitfalls and managing credit responsibly, you can protect your CIBIL score and improve your chances of accessing credit when you genuinely need it.

In the next section, we'll look at practical steps you can take to build and maintain a healthy CIBIL score over the long term.

Manage Short-Term Cash Needs With Pocketly

Even borrowers with a good CIBIL score can occasionally face unexpected expenses. A medical bill, urgent travel requirement, insurance premium, exam fee, household repair, or month-end cash shortfall can create temporary financial pressure. In such situations, borrowing may help bridge the gap, but it's important to approach credit responsibly.

One of the most effective ways to protect your credit health is to borrow only what you genuinely need. Taking a larger loan than necessary can increase repayment obligations and put unnecessary strain on your monthly budget. Before applying, assess the exact amount required and ensure that the repayment schedule fits comfortably within your finances.

Equally important is making repayments on time. Regardless of the loan amount, timely EMI payments contribute positively to your credit history, while missed or delayed payments can negatively affect your credit profile. Responsible borrowing and consistent repayment habits work together to support long-term credit health.

For individuals looking for a small-ticket loan to manage a short-term cash shortage, Pocketly offers a fully digital borrowing experience. Pocketly is a digital lending platform working with RBI-registered NBFCs, designed to help eligible users access funds quickly and conveniently.

About Pocketly

-

Loan amounts ranging from ₹1,000 to ₹25,000

-

Interest rates starting from 2% per month

-

Processing fee between 1% and 8%

-

No collateral required

-

Fast digital application process

-

Quick digital KYC verification

-

Eligibility and visible loan limits vary based on individual profiles

How the Process Works

-

Download the app or visit the website

-

Complete the digital KYC process

-

Select the required loan amount

-

Receive approval and funds, subject to eligibility and verification

While access to short-term credit can be helpful during temporary financial gaps, the goal should always be to borrow responsibly and repay according to the agreed schedule. This helps address immediate needs while supporting a healthy credit profile for future borrowing opportunities.

Conclusion

A healthy CIBIL score is not built through income level, savings balance, or frequent banking activity. It comes from consistent financial discipline like paying dues on time, managing credit responsibly, and avoiding unnecessary borrowing mistakes. The more clearly you understand what truly impacts your score, the easier it becomes to protect your credit profile and improve your future borrowing opportunities.

And when temporary cash needs arise, borrowing carefully matters just as much as borrowing quickly. If you're looking for a convenient way to manage short-term expenses responsibly, you can download the Pocketly app to explore small-ticket loan options with a fully digital application process.

Frequently Asked Questions

1. Which of the following does not impact your CIBIL score?

Several commonly believed factors do not directly affect your CIBIL score, including your salary, savings account balance, fixed deposits, mutual fund investments, debit card transactions, marital status, and checking your own credit report. CIBIL scores are primarily based on your credit behaviour, such as repayment history, credit utilisation, credit enquiries, and existing debt obligations.

2. Does checking my own CIBIL score reduce it?

No. When you check your own CIBIL score, it is recorded as a soft enquiry, which does not affect your score. Soft enquiries are visible only to you and are not considered during credit score calculations. Only lender-initiated hard enquiries, typically made when you apply for credit, may have a minor impact if they occur frequently.

3. Does salary affect my CIBIL score?

No, your salary does not directly influence your CIBIL score. Credit bureaus do not use income information when calculating scores. However, lenders may consider your salary separately when assessing your loan eligibility, repayment capacity, and approved loan amount.

4. Do debit card transactions affect CIBIL score?

No. Debit card transactions use money from your own bank account and do not involve borrowing. Since credit bureaus track how you manage borrowed credit rather than personal spending, debit card usage has no direct impact on your CIBIL score.

5. Does changing jobs affect my CIBIL score?

No, changing jobs does not directly affect your CIBIL score. Your score is based on your credit history and repayment behaviour, not your employment status. However, some lenders may consider employment stability when reviewing a loan application, which is separate from credit score calculation.

6. Can a low bank balance reduce my CIBIL score?

No. The amount of money in your savings account is not used to calculate your CIBIL score. A low bank balance alone will not affect your credit profile. However, if insufficient funds cause missed EMI payments or failed auto-debits, those missed payments could negatively impact your score because repayment history is a key scoring factor.