You earn regularly, pay your bills, and try to stay financially responsible. Yet when you apply for a loan or credit card, the decision does not depend only on your income. It depends on your credit history. And if you are not sure what credit history means, you may be risking approvals without even realising it.

The real issue is that credit history silently records every borrowing decision you make. A single missed EMI, high credit card usage, or too many loan applications can weaken your profile over time. By the time you need credit urgently, the damage may already be visible to lenders.

The solution starts with clarity. Once you understand what credit history is and how it is evaluated in India, you can manage it strategically. This blog breaks it down simply and shows you how to build a strong credit foundation for better financial access.

TL;DR

- Credit history means the complete record of how you’ve borrowed and repaid money, and lenders rely on it for more than just your income.

- Missed EMIs, high credit card usage, frequent loan applications, and loan settlements can quietly reduce your approval chances over time.

- A strong credit history improves loan approvals, helps you secure lower interest rates, increases credit limits, and speeds up processing.

- You can build or improve your credit history by paying on time, keeping utilisation below 30 to 40 percent, limiting hard enquiries, and checking your credit report regularly.

- If you are new to credit, starting small and repaying responsibly helps build a positive track record for better financial access in the future.

What Does Credit History Mean?

Credit history is the complete record of how you have managed borrowed money over time. It reflects your financial behaviour, especially when it comes to loans and credit products.

Your credit history typically includes:

- Personal, home, education, or vehicle loans

- Credit card usage and repayment patterns

- EMI payment history

- Late payments or defaults

- Credit enquiries made by lenders

- Active and closed credit accounts

While many people confuse credit history with a credit score, they are not the same. Your credit history is a detailed report. Your credit score is a three-digit number calculated from that report.

For borrowers in India, this record becomes a financial reference point. Banks and NBFCs review it to decide whether to approve your application, how much to lend, and at what interest rate.

Note: Understanding your credit history is the first step toward protecting it and improving your access to future credit.

Why Credit History Is Important in India?

Your credit history plays a direct role in shaping your financial opportunities. It is one of the first things lenders evaluate before approving any form of credit.

| Area | Impact of Strong Credit History | Impact of Weak Credit History |

| Loan Approval | Higher approval probability | Increased rejection risk |

| Interest Rates | Lower interest rates | Higher borrowing cost |

| Credit Limit | Higher sanctioned limits | Lower limits or restrictions |

| Loan Processing | Faster approvals | Additional checks and delays |

| Emergency Access | Easier access to quick credit | Limited or costly options |

| Financial Credibility | Seen as a low-risk borrower | Viewed as a high-risk borrower |

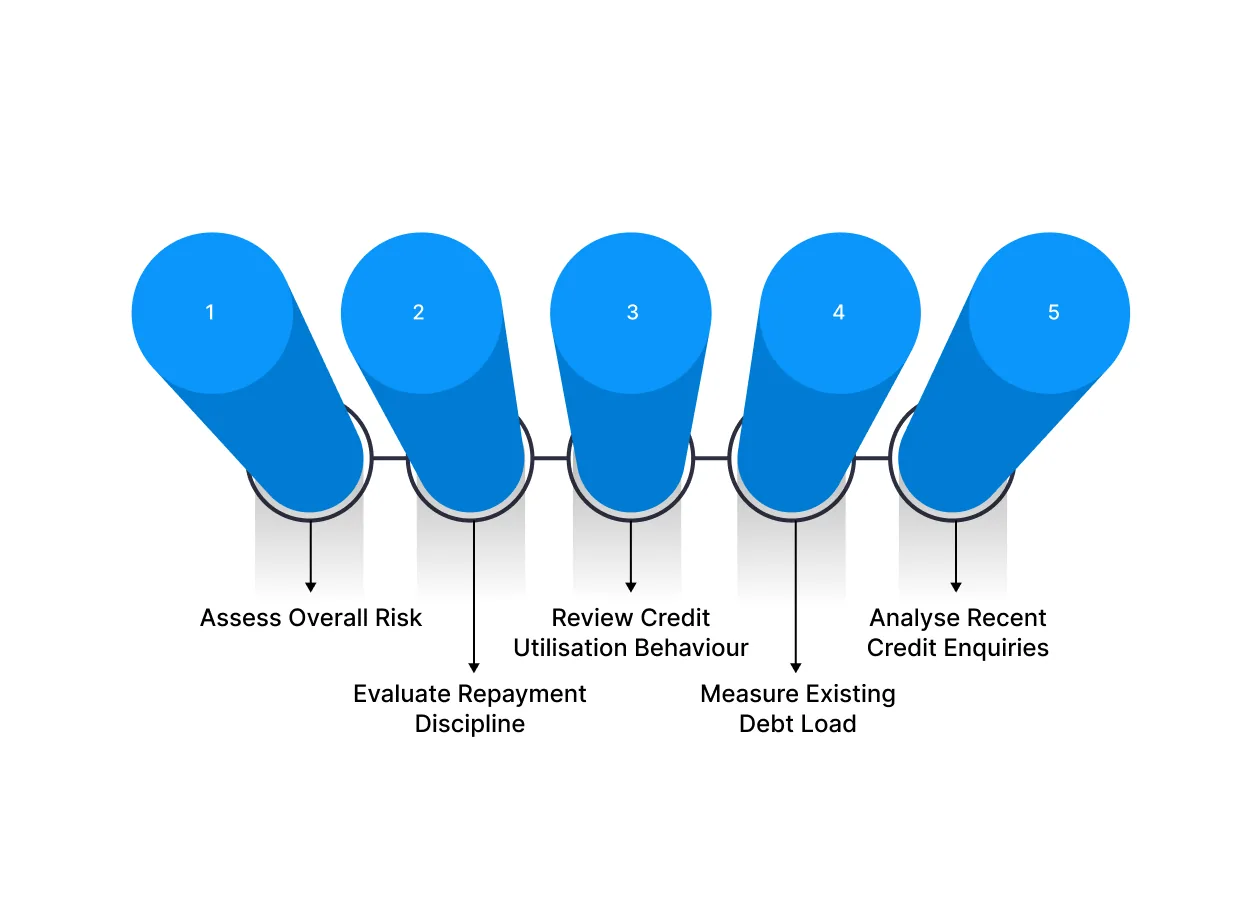

How Do Lenders Use Your Credit History?

When you apply for credit, lenders go beyond your salary and examine how you have handled borrowing in the past. Your credit history helps them evaluate reliability, financial pressure, and repayment intent.

1. Assess Overall Risk

Lenders analyse your past repayment behaviour to estimate the likelihood of default. A long record of timely payments signals stability, while repeated delays or defaults increase perceived risk.

For example, if you have consistently paid EMIs on time for several years, lenders view you as dependable. However, multiple late payments within the last 12 months may make them cautious, even if your income is high.

2. Evaluate Repayment Discipline

Beyond isolated delays, lenders look for patterns. They check whether missed payments are occasional or frequent and whether accounts were ever marked as overdue or settled.

For instance, a single delayed credit card payment may not heavily impact your application. But if your report shows a recurring pattern of minimum payments or skipped EMIs, lenders may interpret this as weak repayment discipline.

3. Review Credit Utilisation Behaviour

Credit utilisation reflects how much of your available credit you regularly use. High usage can indicate financial strain, while moderate usage suggests control.

For example, consistently using 80 to 90 per cent of your credit card limit may raise concerns. In contrast, keeping utilisation below 30 to 40 per cent demonstrates healthier credit management.

4. Measure Existing Debt Load

Lenders calculate how much of your income is already committed to current EMIs. If a large portion of your earnings is tied up in debt repayments, approving additional credit becomes riskier.

For example, if half your monthly income goes toward ongoing EMIs, lenders may either reduce your eligible loan amount or reject the application to prevent overleveraging.

5. Analyse Recent Credit Enquiries

Each time you apply for a loan or credit card, a hard enquiry is recorded. Multiple enquiries within a short period can signal urgency or financial stress.

For instance, applying for four different credit cards within two months may create the impression that you are actively seeking funds, which could lower lender confidence.

Ultimately, lenders use your credit history to form a complete picture of your financial behaviour. The more consistent and disciplined your record, the stronger your approval chances become.

What Is Defined as a Good vs Bad Credit History?

Lenders do not judge your profile on one single factor. They look at patterns across multiple areas. Below is a clear comparison to help you understand what strengthens or weakens your credit profile.

| Factor | Healthy Credit History | Risky Credit History |

| Payment Record | Consistent on-time EMIs and credit card payments | Frequent delays, missed payments, or defaults |

| Credit Utilization | Uses a small portion of available credit | Regularly maxes out credit limits |

| Credit Mix | Balanced mix of secured and unsecured loans | Only high-interest or short-term loans |

| Credit Enquiries | Limited and spaced-out applications | Multiple recent applications in a short period |

| Account Age | Older active accounts showing a long history | Only new accounts with a short track record |

| Account Status | Closed properly or active and well managed | Settled, written off, or overdue accounts |

Common Mistakes That Damage Your Credit History

A strong credit history is built slowly but can weaken quickly through repeated financial missteps. Many people do not realise the long term impact of certain habits until they apply for credit and face rejection.

Here are the most common mistakes and how to manage them effectively.

1. Delaying or Missing Payments

Risk: Your repayment history is the most critical factor in your credit profile. Even one missed EMI or credit card bill can stay on your record for years. Repeated delays create a pattern that lenders interpret as high-risk behaviour.

Mitigation: Activate auto debit for EMIs and at least the total amount due on credit cards. If cash flow is tight, communicate with the lender before the due date rather than missing the payment.

2. Maintaining High Credit Utilisation

Risk: Regularly using a large percentage of your credit limit signals dependency on borrowed money. This reduces lender confidence, even if you pay on time.

Mitigation: Aim to use less than 30 to 40 per cent of your total available credit. If needed, request a higher limit instead of maxing out existing cards.

3. Frequent Credit Applications

Risk: Multiple hard enquiries within a short period can indicate financial urgency. This may reduce your approval chances for future loans.

Mitigation: Compare options carefully before applying. Space out applications and avoid applying simply to check eligibility.

4. Loan Settlements Instead of Full Closure

Risk: When a loan is marked as settled instead of closed, it means you paid less than the full amount due. This negatively affects your creditworthiness and may limit future approvals.

Mitigation: Whenever possible, clear the full outstanding balance. After repayment, confirm that the account status is updated as closed in your credit report.

5. Ignoring Small Outstanding Dues

Risk: Minor unpaid balances on old credit cards or forgotten accounts can escalate into negative remarks on your report.

Mitigation: Periodically review your credit report to ensure no hidden or inactive accounts show pending dues.

6. Closing Old Credit Accounts Abruptly

Risk: Older accounts contribute to the length of your credit history. Closing them unnecessarily can shorten your credit age and slightly reduce your credit strength.

Mitigation: Keep older accounts active with minimal usage unless there is a valid reason to close them.

Credit history is not damaged overnight. It usually weakens through patterns. Being proactive, disciplined, and informed ensures that your financial track record remains strong and reliable over time.

Also Read: Effective Debt Management Strategies and Tips

How to Build or Improve Your Credit History?

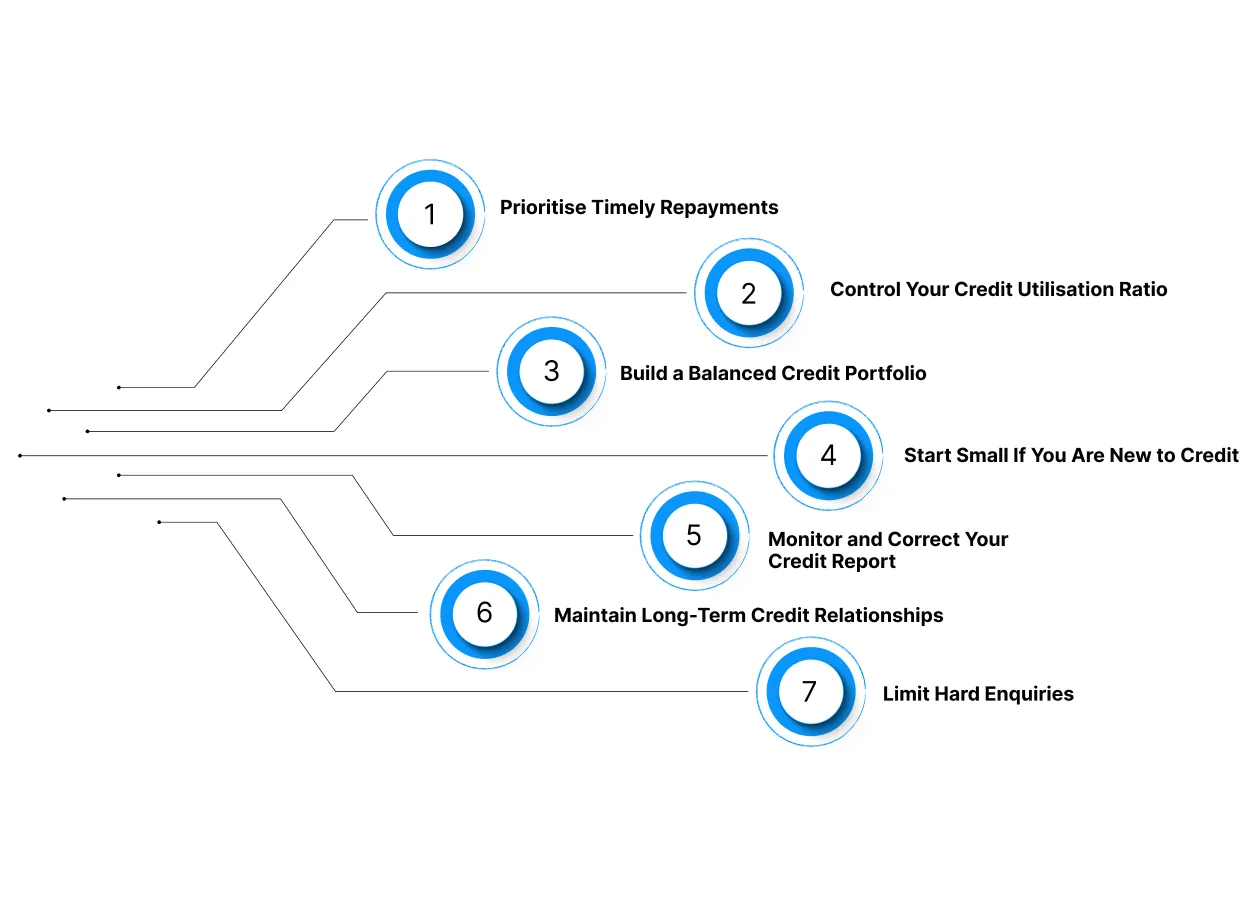

Strengthening your credit history is a gradual process built on consistency, not shortcuts. Lenders look for stable, predictable behaviour over time. The following strategies help you build credibility in a structured and sustainable way.

Strengthening your credit history is a gradual process built on consistency, not shortcuts. Lenders look for stable, predictable behaviour over time. The following strategies help you build credibility in a structured and sustainable way.

1. Prioritise Timely Repayments

Your payment history carries the highest weight in your credit profile. Even a single missed EMI can remain visible for years and affect lender confidence.

Create a repayment system that reduces human error. Use auto debit for fixed EMIs and set alerts at least three days before credit card due dates. If you ever anticipate difficulty in paying on time, inform the lender early. Proactive communication is viewed more positively than silence followed by default.

2. Control Your Credit Utilisation Ratio

Credit utilisation measures how much of your available credit you are using. High utilisation suggests financial pressure, even if payments are timely.

For example, if your total credit limit is 1,00,000 and you consistently use 80,000, lenders may perceive risk. Keeping balances below 30 to 40 per cent demonstrates financial discipline and repayment capacity.

If your spending naturally stays higher, consider requesting a credit limit increase rather than maxing out your existing limit.

3. Build a Balanced Credit Portfolio

A healthy mix of secured and unsecured credit strengthens your profile. Secured loans, such as home or vehicle loans, are generally viewed as lower risk. Unsecured credit, like personal loans or credit cards, carries a higher risk.

Avoid relying excessively on high-interest short-term loans. A diversified credit portfolio, managed responsibly, signals stability and long-term planning.

4. Start Small If You Are New to Credit

If you have no credit history, lenders have no data to assess you. In this case, begin with a secured credit card or a low-limit card. Use it for small expenses and repay the full amount each month.

This creates a positive repayment trail without increasing financial burden. Over time, this track record strengthens your eligibility for larger credit products.

5. Monitor and Correct Your Credit Report

Errors in credit reports are not uncommon. Incorrect personal details, outdated loan statuses, or wrongly reported delays can affect your credibility.

Review your report periodically and dispute inaccuracies immediately. Keeping your record clean ensures lenders evaluate you based on accurate information.

6. Maintain Long-Term Credit Relationships

Length of credit history matters. Older accounts demonstrate sustained financial responsibility.

Avoid closing old credit cards unless necessary. Even if you use them minimally, keeping them active contributes to a longer, stronger credit profile.

7. Limit Hard Enquiries

Each loan or credit card application results in a hard enquiry. Too many enquiries in a short period can reduce lender confidence.

Apply strategically and only when required. Research eligibility criteria beforehand to minimise unnecessary applications.

Also Read: Understanding Unsecured Loans: Meaning and Benefits

New to Credit? Pocketly Helps You Build Your Credit History Smartly

If you have little or no credit history, lenders may hesitate to approve larger loans or premium credit cards. Without a repayment track record, your financial profile appears untested. The way forward is not avoiding credit altogether but starting small and building consistency.

Pocketly lets you access short-term credit in a controlled, manageable way.

- Borrow within a safe range: Loan amounts between ₹1,000 and ₹25,000 help you begin with low exposure. Smaller loans are easier to repay on time, which supports disciplined credit usage.

- No collateral required: You do not need property, gold, or a guarantor. This makes it accessible for students and young professionals building their financial foundation.

- Quick digital process: A simple KYC verification enables fast approvals without paperwork or branch visits, reducing delays when funds are needed.

- Direct bank transfer: Once approved, the loan amount is credited directly to your bank account, making it practical for urgent expenses.

- Flexible repayment options: Choose a tenure that fits your monthly income, so repayments remain manageable and consistent.

- Transparent pricing: Interest rates start from 2% per month, with processing fees typically between 1% and 8%, depending on your profile and loan amount.

When repayments are made on time, responsible borrowing can contribute positively to your credit record. Over time, this helps strengthen your financial profile and improves your access to future credit opportunities.

Conclusion

Building a strong credit history is one of the smartest financial moves you can make in 2026. By paying dues on time, limiting unnecessary credit applications, and monitoring your report regularly, you strengthen your financial credibility step by step.

Credit management is not about borrowing more. It is about borrowing wisely, staying consistent, and proving reliability over time. A healthy credit history opens doors to better loan approvals, lower interest rates, and greater financial flexibility when you truly need it.

If you are just starting out or facing a temporary shortfall, responsible short-term borrowing through platforms like Pocketly can help you build or maintain a positive repayment record without long-term strain.

Ready to strengthen your financial profile? Download the Pocketly app today on [Android] or [iOS] and take a confident step toward building a stronger credit history today.

FAQs

1. What does 'credit history' mean in simple words?

Credit history is a detailed record of how you have borrowed and repaid money over time. It includes your loans, credit cards, repayment behaviour, and whether you paid on time or missed payments.

2. Is credit history the same as credit score?

No. Credit history is the complete record of your borrowing activity, while a credit score is a three-digit number calculated based on that history. The score summarises your creditworthiness, but the history shows the detailed breakdown.

3. How long does a credit history stay on your record in India?

Most repayment records, late payments, and credit enquiries remain on your credit report for several years. Serious defaults can impact your record for up to seven years.

4. Why is credit history important for loan approval?

Lenders review your credit history to assess how responsibly you have handled debt in the past. A consistent repayment track record increases your chances of approval and may help you secure better interest rates.

5. Can I improve a bad credit history?

Yes. You can improve it by paying all EMIs and credit card bills on time, reducing outstanding balances, limiting new credit applications, and correcting any errors in your credit report.