Many young Indians earn regularly yet still feel unsure about where their money goes each month. Rising living costs, multiple digital subscriptions, EMIs, and irregular cash inflows often make budgeting feel overwhelming. Even with a steady salary, it’s common to face month-end cash pressure or depend on short-term fixes.

According to surveys, only 27% of India’s population is financially literate, meaning the vast majority struggle with basic money management skills such as budgeting and planning.

These surveys and lender reports consistently highlight a clear pattern: people who actively track and plan their spending are far less likely to miss payments and far more likely to build savings buffers. Budgeting is no longer optional. It is a basic survival skill in a cost-heavy, credit-driven economy.

This guide explains budget management, the most effective budgeting methods, and the real benefits of managing money intentionally, especially for those navigating tight monthly cash flow and unpredictable expenses.

Key Takeaways

- Budget management means deciding where your money goes before it gets spent, helping you control cash flow instead of reacting to expenses.

- Choosing the right budgeting method matters—options like 50-30-20, zero-based, category budgeting, or flexible budgeting suit different income patterns.

- Effective budgeting reduces financial stress by making expenses predictable, cutting down missed payments, and improving monthly stability.

- Intentional budgeting strengthens savings and emergency readiness, reducing panic borrowing during unexpected costs.

- Common challenges like irregular income, overspending, and inconsistent tracking can be managed with flexible planning and weekly reviews.

- Short-term support tools like Pocketly help protect your budget during cash gaps, allowing you to meet obligations without derailing your financial plan.

What Is Budget Management and Why It Matters

Budget management is the process of deciding where your money should go before it gets spent. It involves planning how income is divided across essentials, lifestyle expenses, savings, and future needs.

At its core, budget management helps you:

- Track how much money comes in each month.

- Control how much goes out across different categories.

- Ensure spending aligns with your priorities, not impulses.

Importantly, budgeting is not about cutting enjoyment or living rigidly. It’s about creating awareness and control, so your money supports your goals instead of causing stress.

For young earners and students, budget management acts as a financial compass. It helps you understand whether your spending habits are sustainable and where small changes can create long-term stability.

Why Budget Management Is Important for Young Indians

Budget management matters more today because financial pressure no longer comes only from low income. It comes from poor cash flow visibility.

For many young Indians:

- Income may be steady, but expenses are scattered.

- EMIs, subscriptions, and lifestyle costs grow quietly.

- Emergency expenses arrive without warning.

Effective budget management helps you:

- Handle irregular income and rising living costs without panic.

- Reduce dependence on last-minute borrowing for routine expenses.

- Build financial confidence, making decisions with clarity instead of guesswork.

When you know exactly how much you can spend and save, money stops feeling unpredictable. Budgeting gives you control, not limits.

Once you understand why budget management matters, the next step is choosing a budgeting method that fits your income pattern and lifestyle.

Also Read: How to Manage Budget vs Expenses Without Stress in 2026

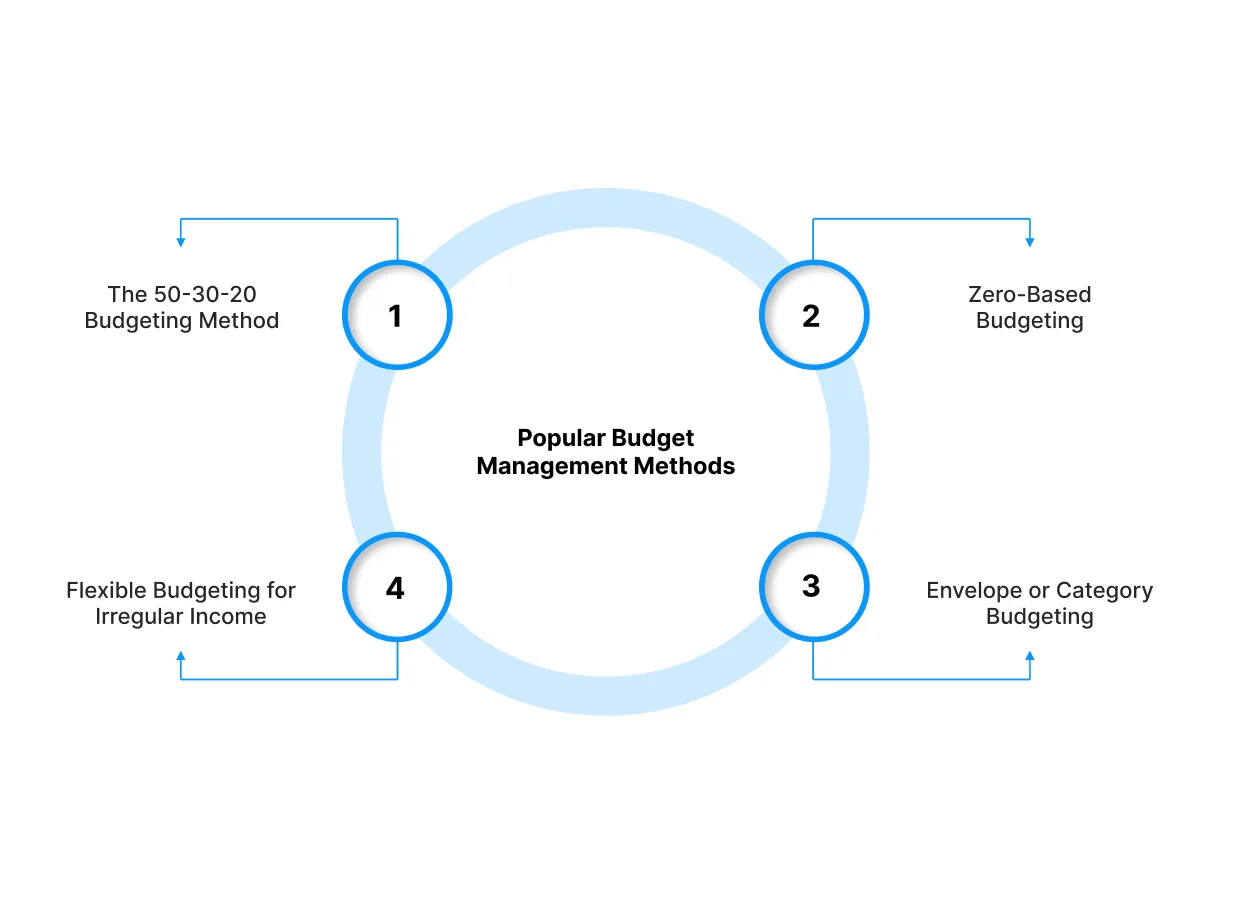

Popular Budget Management Methods You Can Use

Different budgeting methods work for different income patterns, spending habits, and levels of financial discipline.

Different budgeting methods work for different income patterns, spending habits, and levels of financial discipline.

The 50-30-20 Budgeting Method

The 50-30-20 method is one of the simplest ways to manage money, especially for people with a steady monthly income. It divides your income into three clear buckets.

- 50% for needs: Rent, groceries, transport, utilities, EMIs.

- 30% for wants: Dining out, subscriptions, shopping, travel.

- 20% for savings: Emergency funds, investments, or long-term goals.

This method works well for salaried professionals because income is predictable and expenses are relatively stable. It provides structure without feeling restrictive, making it easier to follow consistently.

However, it may feel limiting if fixed expenses already exceed 50%, which is common in metro cities.

Zero-Based Budgeting

Zero-based budgeting follows a simple rule: every rupee must have a job.

Instead of broadly dividing income, you assign exact amounts to every expense category until your remaining balance reaches zero. This does not mean spending everything, but deliberately allocating money to savings as well.

This method is ideal if:

- You tend to overspend without noticing.

- You want tighter control over where money goes.

- You are trying to correct poor spending habits.

It requires regular tracking and updates, but it is highly effective for people who want maximum visibility and discipline.

Envelope or Category Budgeting

Envelope budgeting divides money into spending categories, such as food, travel, subscriptions, and personal expenses. Once a category runs out, spending stops for that area.

Traditionally done with cash envelopes, it now works well with digital budgeting apps that track categories automatically.

This method helps:

- Control discretionary spending.

- Avoid impulse purchases.

- Stick to limits without complex calculations.

It suits people who struggle with lifestyle spending and want clear boundaries without heavy planning.

Flexible Budgeting for Irregular Income

For freelancers, gig workers, and self-employed individuals, fixed budgets often fail. Flexible budgeting adapts month by month based on actual income.

This method focuses on:

- Prioritising essentials first.

- Adjusting savings and discretionary spending based on income flow.

- Preparing for low-income months in advance.

Flexible budgeting recognises income reality rather than forcing rigid rules. It works best when paired with conservative estimates and emergency buffers.

Choosing a method is useful, but the real value lies in the benefits budget management delivers over time.

Also Read: Student Expenses in India: Living Costs And Budgeting

Key Benefits of Budget Management

Effective budget management delivers both short-term relief and long-term stability.

Better Control Over Monthly Expenses

Budgeting gives you clarity. You know exactly where money goes and why.

With proper budget management:

- Spending patterns become visible.

- Unnecessary expenses are easier to spot.

- Sudden shortfalls become less frequent.

Instead of reacting to expenses, you start anticipating them.

Reduced Financial Stress

Uncertainty causes stress, not spending itself. Budgeting reduces that uncertainty.

When you manage your budget well:

- Bills and payments feel manageable.

- Missed or delayed obligations reduce.

- Cash flow becomes predictable.

This mental relief is one of the biggest, yet most overlooked, benefits of budgeting.

Improved Savings and Emergency Readiness

Without a budget, savings happen only if money is left over. With a budget, savings become intentional.

Budget management helps you:

- Set aside money regularly.

- Build buffers for medical, travel, or urgent expenses.

- Avoid panic borrowing during cash gaps.

Even small, consistent savings create long-term security.

Stronger Financial Discipline

Budgeting builds habits that compound over time.

It encourages:

- Mindful spending decisions.

- Better handling of credit and EMIs.

- Progress toward long-term goals like education, travel, or asset purchases.

Discipline grows naturally when money decisions are planned, not rushed.

Even with a budget in place, challenges can still arise, especially when income timing and expenses don’t align perfectly.

Common Budgeting Challenges and How to Handle Them

Understanding common roadblocks helps you avoid abandoning your budget halfway through the month.

Understanding common roadblocks helps you avoid abandoning your budget halfway through the month.

Irregular Income and Unexpected Costs

Irregular income is one of the biggest challenges for students, freelancers, and gig workers. Monthly earnings may change, while expenses like rent, subscriptions, and utilities stay fixed.

Unexpected costs such as medical bills, travel, or urgent repairs can quickly disrupt even a well-planned budget. The solution lies in flexible planning rather than rigid rules.

- Plan your budget around a minimum guaranteed income, not your best month.

- Prioritise essentials first before allocating money to lifestyle spending.

- Build a small emergency buffer, even if it starts with modest amounts.

Flexibility allows your budget to adapt instead of breaking under pressure.

Over-Reliance on Credit

When cash runs short, credit often feels like an easy fix. However, repeated borrowing without a plan can create long-term stress.

Using credit to cover routine expenses increases repayment pressure and can lead to missed payments. This cycle often worsens financial stability rather than improving it.

A structured budget helps:

- Identify avoidable spending.

- Reduce dependence on last-minute borrowing.

- Use credit only for genuine short-term gaps.

The goal is not to avoid credit entirely, but to use it consciously.

Inconsistent Tracking

Many budgets fail not because they are unrealistic, but because they are not tracked consistently.

Skipping expense tracking for even a few days can create blind spots. Monthly reviews often come too late to correct overspending.

- Weekly check-ins work better than monthly reviews.

- Short, regular tracking keeps spending visible.

- Simple tools or apps are enough; complexity is unnecessary.

Consistency matters more than perfection when it comes to tracking.

This is where short-term financial support can help you stay on track without breaking your budget. And Pocketly helps you with that. Download Pocketly today!

Practical Tips to Improve Your Budget Management

Small changes often make the biggest difference. Here are some practical tips to improve your budget management.

Track Weekly, Not Just Monthly

Monthly reviews often arrive too late to fix overspending. Weekly check-ins help you stay aware of where your money is going while you still have time to adjust.

- Catch budget leaks early.

- Prevent small daily expenses from adding up unnoticed.

- Stay in control without feeling overwhelmed.

Short, regular reviews keep your budget realistic and flexible.

Separate Needs from Lifestyle Spending

Blending essentials with lifestyle spending makes budgets harder to manage. Separating them keeps priorities clear.

- Protect fixed essentials like rent, food, and utilities.

- Make discretionary cuts without impacting necessities.

- Adjust lifestyle spending during tighter months.

This separation gives you room to adapt without stress.

Plan for Irregular Expenses

Many budgets fail because irregular expenses get ignored. Annual fees, travel, or medical costs can disrupt monthly plans if unprepared.

- List known irregular expenses in advance.

- Spread their cost across months.

- Avoid sudden pressure on your monthly cash flow.

Planning ahead reduces financial surprises.

Also Read: Managing Income and Expenses: A Simple Beginner’s Guide

How Pocketly Supports Smarter Budget Management

Even the most carefully planned budget can struggle when expenses arrive before income. A delayed salary, sudden bill, or urgent subscription payment can throw plans off balance. Missing payments not only adds stress but can also undo budgeting progress.

Pocketly helps bridge these short-term gaps so your budget stays intact.

How Pocketly Helps You Stay Consistent

- Short-term support for real cash gaps: Access loans from ₹1,000 to ₹25,000 to manage urgent expenses without disrupting your monthly plan.

- Fast and fully digital process: Complete quick KYC and receive approval without paperwork or delays.

- Clear and upfront costs: Interest starts at 2% per month, with processing fees between 1% and 8%, so you always know what you’re paying.

- Helps avoid missed payments: Cover EMIs, bills, or subscriptions on time while staying aligned with your budget.

As a digital lending platform, Pocketly is designed to support responsible money management, not replace budgeting habits.

Download the Pocketly app to manage short-term cash gaps without derailing your budget.

Conclusion

Budget management is not about cutting joy. It’s about creating clarity and control. By choosing a method that fits your income, tracking expenses consistently, and planning for irregular costs, you build a system that supports daily life.

Unexpected expenses may still happen, but a strong budget helps you respond calmly instead of reacting under pressure. When cash gaps arise, having responsible short-term support can protect your plan rather than break it.

Use Pocketly’s short-term loans responsibly to protect your budget and stay financially balanced. Download the app today!

FAQs

1. What is budget management in simple terms?

Budget management means planning how you spend, save, and allocate income to avoid overspending and financial stress.

2. Which budgeting method is best for beginners?

The 50-30-20 method works well for beginners with stable income due to its simple structure.

3. How often should I review my budget?

Weekly reviews work better than monthly checks because they catch issues early.

4. Can budget management help reduce debt?

Yes, budgeting controls spending and supports timely repayments, reducing reliance on credit.

5. What should I do if expenses exceed my budget temporarily?

Short-term financial support, paired with disciplined repayment, can bridge gaps without breaking your budget.