India adds thousands of new businesses every day, yet access to early-stage funding remains one of the toughest challenges for first-time founders. According to RBI and Ministry of MSME data, a significant share of micro and early-stage businesses rely on personal savings or informal borrowing in their first year due to limited credit history and lack of assets. For many entrepreneurs, the absence of property or fixed assets makes traditional secured business loans unrealistic.

A loan for starting a new business without security offers an alternative route. These loans do not require collateral and instead focus on the founder’s credit behaviour, business intent, and repayment ability. They can help cover setup costs, compliance expenses, early marketing, or short-term operational needs. However, unsecured loans also come with higher costs and require stronger financial discipline.

This guide explains how unsecured startup loans work in India, the options available, eligibility requirements, risks to consider, and how digital platforms like Pocketly can responsibly support short-term funding needs.

Quick Glance

- A loan for starting a new business without security helps founders access capital without pledging property or fixed assets, making it suitable for early-stage startups with limited credit history.

- Unsecured startup loans in India are available through government schemes, NBFCs, fintech lenders, and short-term digital platforms, each serving different funding needs and timelines.

- These loans work best when used for defined purposes such as setup costs, early hiring, validated marketing, or fulfilling confirmed demand, rather than covering ongoing losses.

- Interest rates on unsecured loans are higher, and repayment structure, tenure alignment, and hidden charges have a direct impact on cash flow and founder credit health.

- Choosing the right loan requires matching funding size to business stage, prioritising transparent terms, and avoiding over-borrowing that can strain future growth.

- For short-term operational gaps, platforms like Pocketly can support startups with small, fast, and transparent digital loans—helping founders maintain continuity without long-term debt pressure.

Loan for Starting a New Business Without Security

Before looking at lenders and schemes, it is important to understand what unsecured startup loans actually mean in practice.

A loan for starting a new business without security is a financing option that does not require the borrower to pledge property, land, or fixed business assets as collateral. Instead, lenders assess risk based on the founder’s personal credit history, income stability, business registration status, and intended use of funds.

These loans are commonly used by sole proprietors, partnerships, LLPs, and early-stage private limited companies that lack asset backing but need capital to begin operations. Because lenders take on higher risk, unsecured loans usually have lower limits, shorter tenures, and higher interest rates than secured business loans.

Understanding this trade-off helps founders decide whether unsecured borrowing fits their stage and goals.

Why New Businesses Look for Loans Without Collateral

Most early-stage founders actively search for unsecured options because collateral requirements do not align with startup realities.

Most early-stage founders actively search for unsecured options because collateral requirements do not align with startup realities.

Asset constraints for first-time founders

Many new entrepreneurs do not own property or assets that qualify as acceptable collateral. Even when family assets exist, founders are often reluctant to risk them for an untested business idea.

Speed and flexibility needs

Early business expenses such as registration, licences, software tools, marketing campaigns, or vendor payments often need immediate funding. Traditional bank loans may take weeks or months, while unsecured options offer faster access.

Reducing personal asset risk

Unsecured loans allow founders to separate business risk from family or personal property. This psychological and financial separation matters, especially during the experimentation phase.

With these motivations clear, the next step is understanding the types of unsecured startup loans available in India.

Also Read: Short-Term Business Loans: Understanding Tenure, Interest Rates, and Benefits

Types of Loans for Starting a New Business Without Security in India

Unsecured startup loans come from different sources, each suited to specific needs and stages.

1. Government-backed unsecured loan schemes

Government initiatives aim to improve credit access for small and new businesses.

- Mudra Loans (PMMY): Offered under Shishu, Kishore, and Tarun categories, Mudra loans support micro and small businesses without collateral, subject to limits and eligibility.

- CGTMSE-backed loans: Banks can offer collateral-free loans under credit guarantee coverage, reducing lender risk.

- Startup India-linked lending programmes: Some public sector banks extend unsecured credit aligned with recognised startups.

While these schemes offer lower borrowing costs, application processes can be time-consuming and approval timelines unpredictable.

2. NBFC and fintech startup loans

NBFCs and digital lenders focus on speed and accessibility. These loans often have:

- Simpler documentation

- Faster approvals

- Digital onboarding

Interest rates are usually higher than banks, reflecting early-stage risk, but access is quicker.

3. Short-term digital loans for early cash needs

Some founders do not need long-term funding but face timing gaps, such as delayed payments or upfront expenses. Short-tenure digital loans address these needs without locking the business into multi-year obligations.

If your requirement is short-term and operational rather than long-term expansion, platforms like Pocketly can help manage urgent expenses without collateral commitments.

Understanding loan types is only half the picture; eligibility determines what you can realistically access.

Eligibility Criteria for Unsecured Startup Loans

Without collateral, lenders rely more heavily on founder credibility and repayment behaviour.

Without collateral, lenders rely more heavily on founder credibility and repayment behaviour.

Founder profile and credit history

In the absence of business credit records, personal credit scores play a major role. Clean repayment history, low defaults, and disciplined usage significantly improve approval chances.

Business registration and structure

Most lenders require formal registration, whether as a proprietorship, partnership, LLP, or private limited company. Registered entities signal seriousness and accountability.

Business intent and repayment visibility

Lenders expect clarity on how funds will be used and repaid. Realistic projections and clear expense mapping matter more than aggressive growth claims.

Meeting eligibility does not automatically mean borrowing is the right choice. Timing matters just as much.

Also Read: How to Build Business Credit Fast in Simple Steps

When Does an Unsecured Startup Loan Make Sense?

A loan for starting a new business without security works best when it supports momentum rather than masks uncertainty.

Situations where unsecured loans help

Unsecured borrowing makes sense when it removes a specific operational bottleneck.

- Covering setup or registration costs:

- Legal registration, licences, or compliance filings often require upfront payment.

- Hiring early team members:

- Bringing in a first sales or operations hire can unlock growth capacity.

- Marketing and customer acquisition:

- Borrowing supports reach when the offering is already validated.

- Inventory or essential equipment:

- Funding confirmed demand rather than speculative stocking.

In these cases, borrowing acts as a bridge between opportunity and execution.

Situations where caution is needed

Unsecured loans become risky when used to delay hard decisions.

- Covering ongoing losses without revenue clarity

- Funding personal expenses through business loans

- Using long-term debt for short-term problems

- Once timing is right, founders must understand costs before committing.

Interest Rates, Repayment, and Risks of Unsecured Startup Loans

The real cost of an unsecured startup loan is shaped by how interest is charged, how repayments are structured, and how errors affect cash flow and credit. Founders should evaluate these elements together, not in isolation.

The real cost of an unsecured startup loan is shaped by how interest is charged, how repayments are structured, and how errors affect cash flow and credit. Founders should evaluate these elements together, not in isolation.

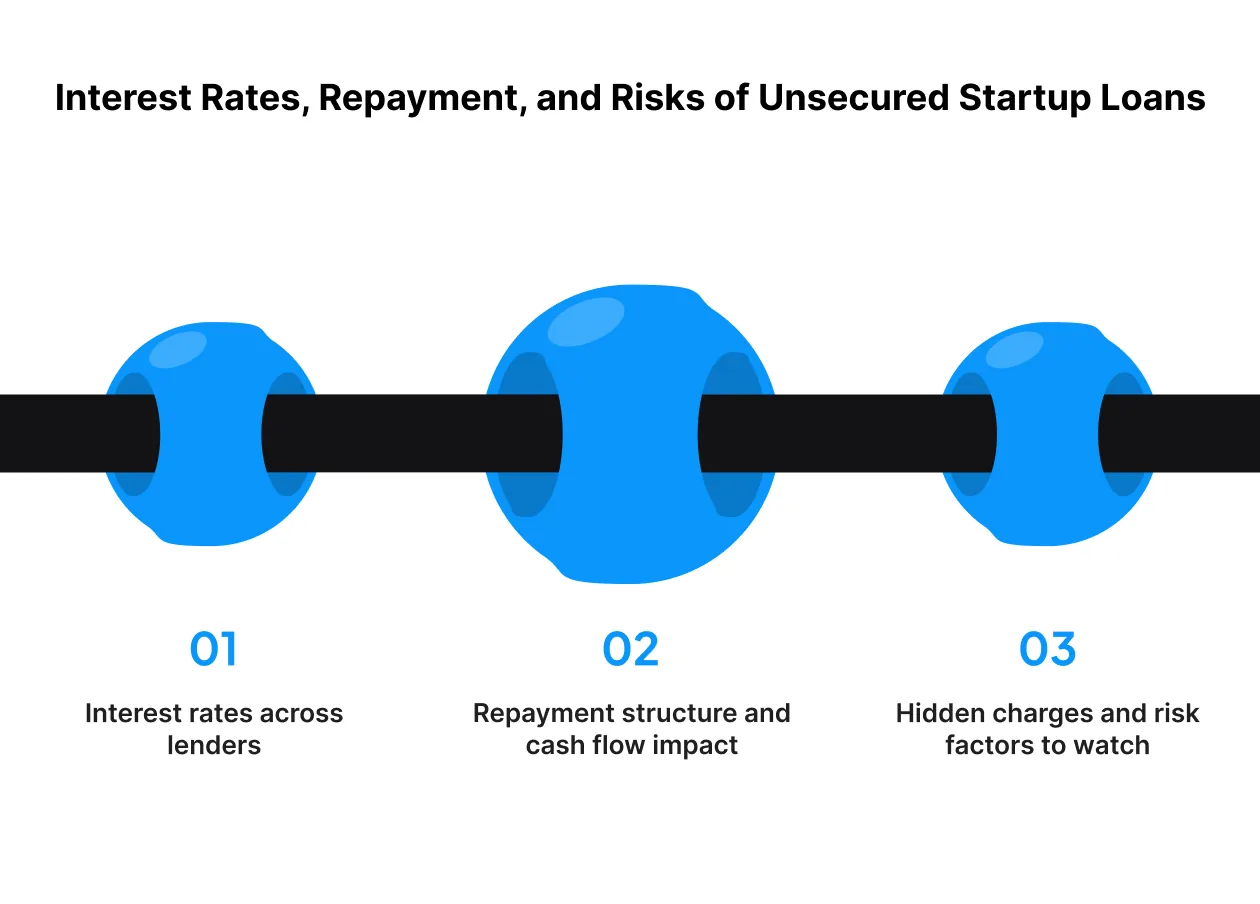

Interest rates across lenders

Unsecured startup loans carry different pricing models depending on the lender and risk appetite.

- Banks generally offer the lowest interest rates, but approvals are harder to secure. Strict documentation, credit thresholds, and longer processing timelines make banks less accessible for very early-stage startups without revenue history.

- NBFCs and fintech lenders charge higher interest rates to offset early-stage risk. In return, founders gain faster approvals, simpler onboarding, and more flexible eligibility criteria. This trade-off suits startups that prioritise speed and access over cost.

- Short-term digital loans often use monthly pricing instead of annualised interest rates. While the monthly rate may appear small, it can translate into a high annual cost if the loan is rolled over or repaid late.

Comparing loans purely on headline rates can be misleading. Founders should always assess total repayment amount over the full tenure, not just the stated percentage.

Repayment structure and cash flow impact

Repayment terms directly affect operational stability, especially in businesses with uneven cash inflows.

- Short tenures work best for temporary cash gaps, delayed receivables, or predictable short-term needs. They reduce interest exposure but demand disciplined repayment planning.

- Longer tenures are more suitable for expansion-related borrowing where returns take time to materialise, such as scaling operations or entering new markets.

Problems arise when tenure does not match cash flow reality. Even a small unsecured loan can strain working capital if repayments fall due before revenue arrives, forcing founders into reactive borrowing cycles.

Hidden charges and risk factors to watch

Beyond interest, unsecured loans often include additional costs that increase financial pressure if overlooked.

- Processing and onboarding fees are deducted upfront, reducing usable capital

- Late payment penalties that compound quickly

- Prepayment or foreclosure clauses that limit early repayment flexibility

More importantly, unsecured loans are tied directly to the founder’s personal credit profile. Missed payments or rollovers can damage credit scores, affecting future funding, partnerships, and even personal borrowing capacity.

In practice, clear terms and predictable rules matter more than the lowest advertised rate. Transparency reduces risk, especially during uncertain early stages.

With a clear understanding of cost and risk, founders are better positioned to evaluate which lender truly fits their business.

Also Read: Strategies and Tips to Improve Your Business Cash Flow

How to Choose the Right Loan Without Security for Your Startup

Selecting an unsecured startup loan should be treated as a financial strategy decision, not just a funding solution. The goal is to support execution without creating long-term pressure.

Match the loan to your business stage

Not all startups need the same type or size of loan.

- Early-stage startups benefit from smaller, flexible loans that help cover defined expenses without locking the business into long-term obligations.

- Expansion-stage businesses with revenue visibility may justify larger loans tied to specific growth milestones, provided repayment timelines align with expected inflows.

Borrowing ahead of readiness often increases stress rather than speed. Loans should follow progress, not attempt to create it prematurely.

Prioritise transparency and flexibility

The safest unsecured loans are the ones founders fully understand before accepting.

Look for:

- Clearly defined repayment schedules

- Upfront disclosure of all fees and charges

- Digital access to loan status, dues, and timelines

These factors reduce uncertainty and allow founders to plan operations without financial surprises.

Avoid over-borrowing and protect your credit health

More capital does not automatically mean more runway.

- Borrow only what the business can service comfortably under conservative assumptions

- Avoid stacking multiple unsecured loans to cover previous repayments

- Treat founder credit health as a long-term asset

Strong credit discipline preserves future funding options and negotiating power.

Even with careful planning, startups often experience short-term financial friction caused by timing mismatches, not poor decision-making. This is where limited, responsible short-term tools can act as a support layer without replacing the core funding strategy.

How Pocketly Supports Startups Without Collateral

Traditional startup loans focus on long-term financing, but early-stage founders often face short-term cash challenges outside formal funding cycles.

Pocketly supports this gap by offering short-term digital credit designed for continuity rather than long-term dependency.

How Pocketly fits in

- Short-term digital loans from ₹1,000 to ₹25,000 for urgent needs

- Fast, fully online access for time-sensitive expenses

- Transparent pricing and repayment terms with no ambiguity

- Useful for operational gaps, tools, subscriptions, or vendor payments

Download the Pocketly App to manage short-term business expenses without collateral or long-term debt pressure.

Conclusion

A loan for starting a new business without security can be a valuable tool when used intentionally and at the right stage. Understanding loan options, eligibility, costs, and repayment impact helps founders avoid unnecessary pressure during the most fragile phase of their journey.

Unsecured loans should support execution, not compensate for unclear fundamentals. When borrowing decisions are aligned with real needs and timelines, credit becomes a support system rather than a burden.

When short-term cash gaps arise, responsible digital lending platforms can help founders stay on track without risking personal assets.

Use Pocketly to handle urgent startup expenses while keeping your long-term finances stable. Download the App today.

FAQs

1. Can I get a loan for starting a new business without security in India?

Yes. Government schemes, NBFCs, and fintech lenders offer unsecured options based on founder profile and credit behaviour.

2. What is the maximum unsecured loan amount for startups?

Limits vary by lender and scheme, ranging from small short-term amounts to several lakhs.

3. Do unsecured startup loans require business income?

Not always. Many lenders assess personal credit history and business intent instead of existing revenue.

4. Are unsecured startup loans risky?

They can be if taken without repayment planning, as interest rates are higher and the credit impact is direct.

5. Can Pocketly be used for startup expenses?

Pocketly offers short-term digital loans that founders can use for urgent expenses when managed responsibly.