Building business credit is crucial for small business entrepreneurs and professionals seeking to expand their financial opportunities. Whether you're running a side business or managing a growing company, having strong business credit can help you secure loans, negotiate better terms, and keep your personal finances separate from your business expenses.

In this blog, we'll walk you through simple, effective steps to quickly build your business credit, empowering you to take your business to the next level.

Key Takeaways

- Business Credit is Essential: A strong business credit profile opens doors to better financing options, lower interest rates, and improved supplier relationships.

- Legal Structure Matters: Choosing the right business structure, like LLCs or corporations, is crucial for separating personal and business finances, laying the foundation for credit-building.

- Monitor Your Business Credit: Regularly check your business credit report to track progress and catch errors that could impact your credit score.

- Supplier Relationships Are Key: Establishing credit terms with suppliers and ensuring they report payments to credit bureaus is a critical step in building business credit.

What is Business Credit?

Business credit refers to a company's capacity to obtain loans or purchase goods and services on credit, based on its own creditworthiness rather than the personal credit of its owners. This credit is extended by vendors, suppliers, financial institutions, and lenders through various means such as loans, business credit cards, or trade credit.

A business credit score assesses the risk associated with lending to a company, taking into account factors like payment history, credit utilization, and outstanding debts. Establishing and maintaining good business credit is quintessential for securing financing terms, building relationships with suppliers, and supporting long-term business growth.

Importance of Business Credit

Business credit is vital for the long-term growth of your business, providing financial flexibility, protection, and credibility to thrive in the competitive market. Here are some important reasons for building and maintaining strong business credit.

- Access to Capital & Financing: Good business credit improves your chances of loan approval, provides access to higher credit limits, and offers financing options such as business loans, line of credit, and trade credit

- Financial Cost Benefits: Strong business credit attracts lower interest rates, reducing overall borrowing costs. It may also secure better insurance premiums and improved credit terms with suppliers.

- Operational Advantages: Business credit helps in better cash flow management, particularly during seasonal fluctuations. It also helps control employee spending with tracking capabilities and simplifies accounting.

- Business Growth & Credibility: A strong credit profile enhances your business reputation, builds investor confidence, and thus secures larger contracts and partnerships.

- Strategic Business Benefits: Business credit cards often offer rewards on business expenses, including travel and office supplies, along with interest-free periods that improve cash flow.

- Long-term Financial Planning: Building business credit creates a strong financial record for securing future financing. It also provides scalability for growth and tax advantages through deductible business expenses.

Many business owners recognize the value of strong credit but feel overwhelmed by where to begin. The process, however, can be broken down into manageable, sequential steps that any business can execute effectively.

How to Build a Business Credit Fast in Simple Steps

Building business credit is a very important step for entrepreneurs and small business owners, especially in India, where access to financial resources can be competitive. A strong credit profile opens doors to better financing options, lower interest rates, and improves your credibility with lenders and suppliers.

Here’s a more detailed look at the top ways to build business credit:

1. Register Your Business

Begin by officially registering your business as a legal entity and choosing the right business structure, like LLCs, corporations, or partnerships, which provide legal separation between personal and business finances, allowing your business to establish its own credit profile. An LLC or corporation not only protects your personal assets but also influences how lenders and creditors view your business’s financial health.

2. Obtain a Federal Tax ID Number (EIN)

In India, obtaining a Permanent Account Number (PAN) and GST (Goods and Services) registration is important for your business. Similarly, a Federal Tax Identification Number (EIN) in the U.S. plays a quintessential role in separating personal and business finances. The EIN, like a Social Security number for businesses, is required for tax filings, credit applications, and opening a business bank account.

3. Open a Business Bank Account

Set up a dedicated business bank account to manage your finances. This helps maintain clarity in transactions and is crucial when applying for credit or loans. Indian banks like HDFC, SBI, and ICICI offer business accounts with features tailored to small businesses, making it easier to manage finances while building your credit profile.

4. Establish Credit with Suppliers

Negotiate credit terms (such as net-30 or net-60) with your suppliers. Ensure that these vendors report your payments to credit bureaus like CIBIL or Equifax India, which will help build your business credit score. This helps create a solid business credit profile over time.

5. Apply for a Business Credit Card

Business credit cards are one of the quickest ways to build credit. Timely payments on this card will help you build a positive credit history. Make sure the card issuer submits your payment details to credit bureaus to have a direct impact on your business credit.

6. Regularly Monitor Your Business Credit Report

Review your business credit reports from agencies like CIBIL, Equifax, or CRIF High Mark. Regular reviewing of your credit report can help in catching any errors or discrepancies early. This also helps you understand how lenders and suppliers are perceiving your business. Keeping track of your credit score will allow you to take corrective action and maintain credit health.

Building robust business credit through these systematic steps helps in long-term financial health. However, businesses occasionally face immediate cash flow and other challenges.

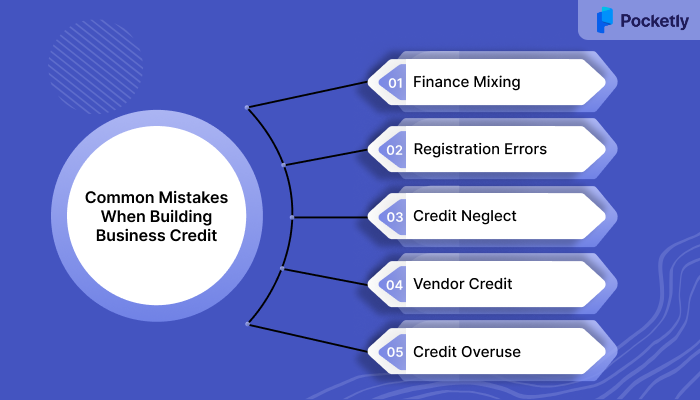

Common Mistakes When Building Business Credit

While building business credit, there are some common mistakes that can hinder progress, such as ignoring credit reports and overusing credit. Avoiding these pitfalls ensures a healthier credit profile and smoother financial growth.

- Mixing Personal and Business Finances: Using personal accounts for business transactions can jeopardize both your personal and business credit scores. So, maintain separate accounts for clarity and protection.

- Failing to Register the Business Properly: Not registering your business as a legal entity can prevent you from establishing credit independently of your personal finances. A formal business structure, such as an LLC or Corporation, is necessary for building business credit.

- Ignoring Your Business Credit Reports: Neglecting to check your credit reports can result in overlooking errors or fraudulent activities that could negatively impact your credit score. Regularly monitor your business credit reports.

- Not Building Credit with Vendors: Failing to establish credit relationships with suppliers can slow down your credit-building process. Work with vendors who report to credit bureaus to accelerate your business credit growth.

- Overextending Credit Utilization: Relying too much on credit can lead to high utilization rates, which negatively impact your business credit score. Aim to use no more than 30% of your available credit to maintain a healthy credit profile.

These mistakes often stem from confusion about how business credit differs from personal credit management. Let’s take a look and understand the key differences.

Difference Between Business Credit and Personal Credit

Business credit and personal credit are distinct in terms of financial management. Business credit is tied to the financial health of a business, impacting its ability to secure financing, while personal credit focuses on an individual's financial history. Both report to credit agencies like TransUnion, CIBIL, Experian, Equifax, and CRIF High Mark.

| Aspect | Business Credit | Personal Credit |

| Ownership | Linked to the business entity, not individual owners. | Tied to an individual's financial history. |

| Credit Score Factors | Based on business payment history, debt levels, and credit utilization. | Based on personal payment history, debt levels, and credit utilization. |

| Impact of Missed Payments | Affects business credit score and ability to get business loans or vendor credit. | Affects personal credit score, making it harder to get personal loans or mortgages. |

| Application Process | Requires business-related documents like tax ID, financial statements, and business history. | Requires personal financial details, such as income and employment history. |

| Liability | Business is responsible for the credit; personal assets are typically protected (unless a personal guarantee is made). | An individual is personally liable for debts. |

| Usage | Used for business expenses such as equipment, supplies, and business loans. | Used for personal expenses such as housing, cars, and personal loans. |

| Building Credit | It can be built by establishing credit with suppliers, vendors, and business credit cards. | Built through personal loans, credit cards, and paying bills on time. |

Understanding these distinctions is crucial, but managing them effectively requires the right set of tools and resources. The good news is that technology has made credit management more accessible than ever before.

Tools to Build and Manage Your Business Credit Effectively

In order to manage and build your business credit effectively, there are several tools and resources in the market that can help you track progress, ensure timely payments, and improve your credit score.

- Credit Monitoring Services: Tools like Nav and CreditSignal allow you to monitor your business credit score and reports from agencies like Experian and Equifax. These services help you stay on top of your credit health and identify any errors.

- Accounting Software: Software like QuickBooks or Xero helps you track expenses, income, and cash flow. Keeping accurate financial records ensures you have the necessary data when applying for credit and can help you manage your payments on time.

- Business Credit Cards: A business credit card, such as one from American Express or Chase Ink, helps you build credit while offering rewards for business expenses.

- Vendor Credit Management Tools: Platforms like Plastiq or Fundbox can manage your payments with vendors and report to credit agencies. Setting up vendor accounts with favorable payment terms (net-30, net-60) is crucial to build your credit.

- Business Loan Platforms: Websites like Lendio or Fundera allow you to compare different business loan options and find lenders that match your credit profile. These platforms will help you get the best terms based on your current credit situation.

While these tools help build and monitor business credit, running a business often requires quick financial solutions. Cash flow gaps, unexpected expenses, and growth opportunities need fast funding to maintain momentum as your credit profile develops.

How Pocketly Can Help You Manage Business Finances

While building business credit is crucial for your long-term growth, managing your day-to-day business finances can be just as important. Pocketly provides an easy solution for small business owners and professionals to handle short-term financial needs, such as managing cash flow or covering unexpected expenses.

- Fast Loan Approval: Pocketly offers quick approval and disbursal of loans, helping you manage urgent cash flow issues without delay.

- Interest Rates Starting at 2% Per Month: Affordable interest rates that make it easier to manage repayments.

- Processing Fees: Ranges from 1-8% of the loan amount, with transparency in loan costs.

- No Collateral Required: Get access to funds without putting your personal or business assets at risk.

- Flexible Loan Repayment Modes: Tailored repayment options that suit your business's financial capacity.

- Secure and Reliable: ISO 27001 certified platform, ensuring your personal and business data is protected.

Conclusion

Building strong business credit is essential for unlocking better financial opportunities, reducing borrowing costs, and establishing your business’s credibility. By following the simple steps outlined in this blog, you can quickly strengthen your credit profile, which will enable your business to thrive in a competitive market. In addition to managing your business credit, having access to fast and flexible financial solutions is just as important.

Pocketly provides an easy way for small business owners to handle short-term financial needs with fast approval and flexible repayment options, helping you stay on top of your business expenses. Download Pocketly today on Android or iOS.

FAQ’s

1. How can I raise my credit score to 700 in 30 days?

You can get a 700 credit score in 30 days by reducing credit card balances, fixing credit report errors, and becoming an authorized user can boost your score.

2. Is it possible to build business credit within 30 days?

Building a strong business credit profile takes time, but you can start the process within 30 days. This involves registering your business, obtaining required licenses, opening a business account, and applying for a business card.

3. How long does it take to get business credit?

The timeline for acquiring business credit varies depending on your business's financial history and the creditworthiness of its owners. Typically, it can take anywhere from weeks to months to establish and access business credit, based on the actions you take and the type of credit products you apply for.

4. What is the 15-3 strategy for improving a credit score?

The 15-3 strategy involves making two credit card payments each month: one 15 days before the due date and the second three days before. This technique helps lower your credit utilization rate by reducing the balance reported to credit bureaus, potentially improving your credit score.

5. How many credit bureaus are there?

In India, there are four main credit bureaus: CIBIL (TransUnion CIBIL), Experian, Equifax, and CRIF High Mark. These bureaus gather and report credit information, which lenders use to assess your creditworthiness. While there are additional specialized agencies, these four are the most widely used by financial institutions for evaluating credit.