Many borrowers focus only on paying their monthly EMI on time, without realising that making an occasional extra payment towards the loan principal can significantly reduce future interest costs. Even a small lump-sum payment from a bonus, tax refund, or freelance income can help lower the outstanding balance and potentially shorten the repayment journey.

This matters even more as personal borrowing continues to rise in India. According to RBI data, personal loans recorded 14.2% year-on-year growth in January 2025, showing how strongly borrowers continue to rely on credit for everyday financial needs and larger expenses.

In such a scenario, understanding how part payment works can help borrowers manage debt more strategically, reduce borrowing costs over time, and make better use of surplus funds whenever they become available.

TL;DR

-

Part payment means paying an extra amount towards your loan principal apart from your regular EMI, without closing the loan completely.

-

Reducing the principal early can lower future interest costs and may either reduce your EMI or shorten the loan tenure.

-

Borrowers often use bonuses, tax refunds, freelance income, or surplus savings to make part payments during the loan tenure.

-

Before making a part payment, check for lock-in periods, minimum payment requirements, processing charges, GST, and lender restrictions.

-

Part payment is different from foreclosure because the loan continues after the payment instead of being fully closed.

What Is Part Payment in a Loan?

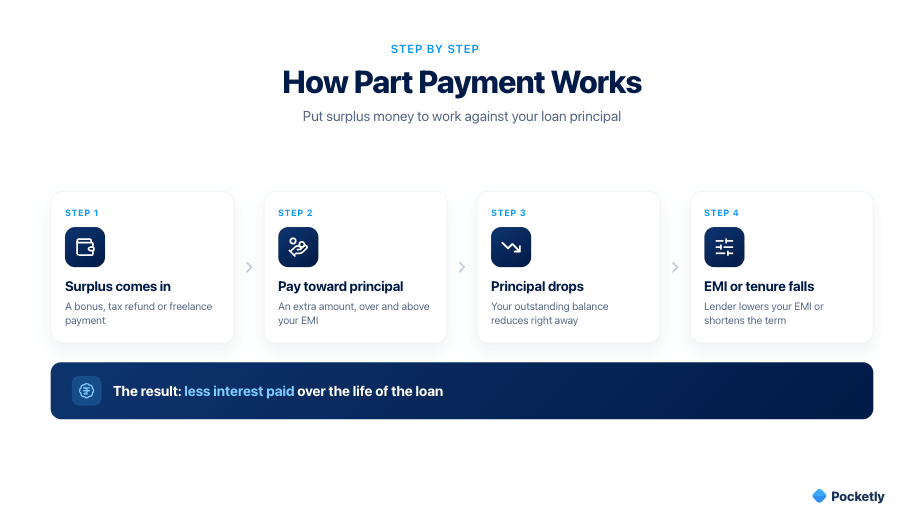

Part payment in a loan refers to making an additional payment towards the outstanding loan amount before the loan tenure ends, without closing the loan completely. The extra amount is typically adjusted against the principal, which is the original amount borrowed from the lender.

This is different from a regular EMI. Your EMI is a scheduled monthly payment that covers both principal and interest according to the repayment plan. A part payment, on the other hand, is an optional payment made over and above your EMI whenever you have surplus funds available.

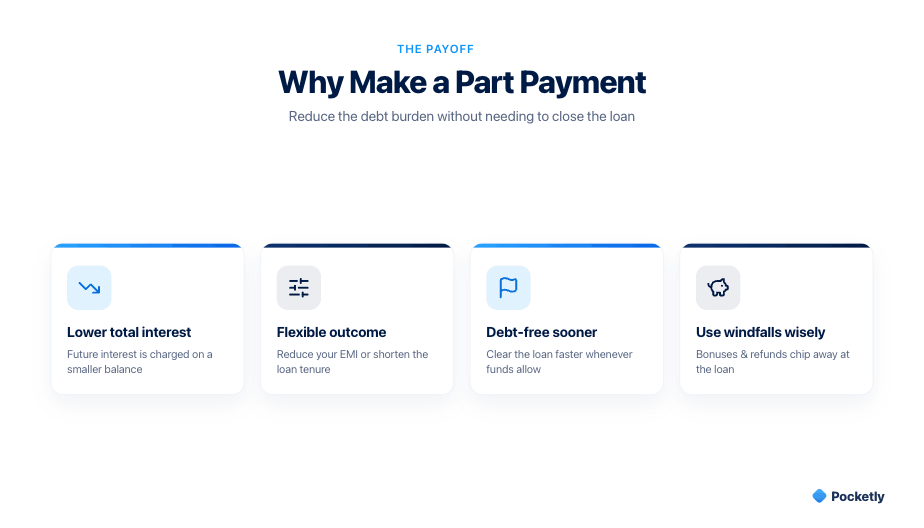

When the principal balance reduces, future interest is generally calculated on a lower outstanding amount. As a result, borrowers may save on total interest costs over the remaining tenure. Depending on the lender's terms, the loan may continue with a lower EMI or a shorter repayment period.

For example, if you receive a bonus, tax refund, or freelance payment, you can use a portion of it to make a part payment instead of waiting for the loan to be repaid solely through monthly EMIs. The loan remains active, but the outstanding balance becomes smaller.

Why Borrowers Make Part Payments Instead of Closing the Entire Loan

Borrowers can receive extra money during the loan tenure, such as a performance bonus, tax refund, festival incentive, or payment from a freelance project. However, the amount may not be enough to repay the entire outstanding loan. In such situations, continuing with only regular EMIs means the loan principal reduces gradually, and interest keeps accruing on the remaining balance.

This is where part payment becomes useful. Instead of waiting until enough funds are available for full foreclosure, borrowers can use a portion of their surplus money to reduce the outstanding principal immediately. A lower principal generally means lower future interest costs and can potentially shorten the repayment period, depending on the lender's terms.

The goal is simple: lower the debt burden without needing enough money to close the loan completely. But how exactly does part payment affect your loan balance, EMI, and repayment schedule? Let's look at how the process works.

How Does Part Payment Work in a Personal Loan?

Depending on the lender's policy, you may be given one of two options:

Reduce the EMI Amount

Some lenders keep the original loan tenure unchanged and lower your monthly EMI. This can improve monthly cash flow and make repayments easier to manage.

Reduce the Loan Tenure

Others keep the EMI amount the same but shorten the repayment period. This option often helps borrowers become debt-free sooner and may lead to greater overall interest savings.

The exact impact depends on the lender's terms, which is why understanding the potential savings from part payment is the next important step.

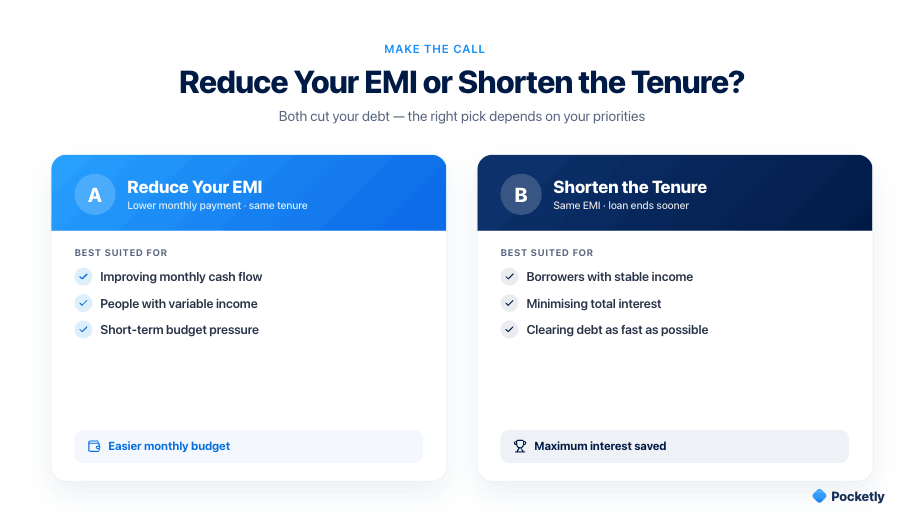

Should You Reduce EMI or Shorten the Loan Tenure?

Both options lower the outstanding debt, but the right choice depends on your financial priorities.

Option A: Reduce Your EMI

Reducing the EMI lowers your monthly repayment burden while keeping the loan tenure largely unchanged. This option can be useful if you're managing multiple expenses or expect temporary pressure on your budget.

Best suited for:

-

Borrowers looking to improve monthly cash flow

-

Individuals with variable income

-

Those expecting short-term financial commitments

A salaried employee dealing with rising household costs or a small entrepreneur facing uneven monthly income may prefer lower EMIs to improve cash flow. The extra breathing room can make it easier to manage regular expenses without missing repayments.

Option B: Shorten the Loan Tenure

With this option, the EMI remains the same, but the repayment period becomes shorter. Since the loan is repaid faster, interest is charged for a shorter duration, which can lead to greater overall savings.

Best suited for:

-

Borrowers with stable income

-

Individuals focused on reducing total interest paid

-

Those aiming to clear debt as quickly as possible

A professional who receives a substantial annual bonus or a freelancer with consistent income may choose tenure reduction to become debt-free sooner and minimise total borrowing costs.

Also read: Maximum and Minimum Tenure for Personal Loans

What Charges, Conditions or Restrictions Should You Check First?

Making a part payment can help reduce your loan burden, but the benefits may be smaller than expected if you overlook the lender's terms and charges. Some borrowers assume they can make part payments at any time without restrictions, only to discover fees or eligibility conditions later.

Before making a part payment, carefully review the lender's policy and repayment terms. Understanding these details can help you calculate whether the savings outweigh any associated costs.

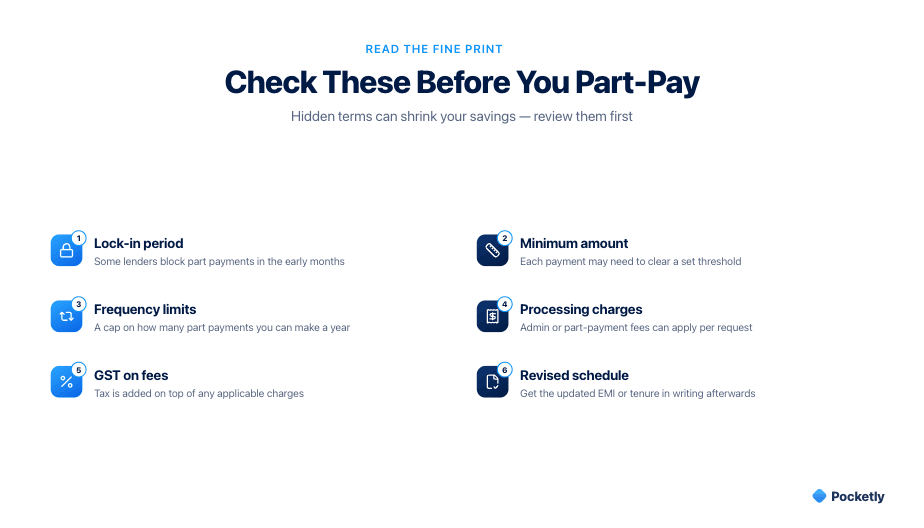

Key Things to Check Before Making a Part Payment

Lock-In Period

Some lenders do not allow part payments during the initial months of the loan. This restriction, known as a lock-in period, may prevent borrowers from reducing the principal immediately after taking the loan.

Minimum Part-Payment Amount

Lenders may require a minimum amount for each part payment. If your surplus funds are below this threshold, you may need to wait until you can make a larger payment.

Frequency Limits

Certain lenders restrict how often borrowers can make part payments during a year or throughout the loan tenure. Knowing these limits can help you plan repayments more effectively.

Processing Charges

Part-payment requests may attract processing or administrative charges. These fees can reduce the overall benefit of making an early repayment, so it is important to understand the applicable costs beforehand.

GST on Applicable Fees

If the lender charges a processing fee or other service-related charges, GST may also apply. Reviewing the total cost helps you assess the true savings from the part payment.

Revised Repayment Schedule

After the payment is processed, ask for an updated repayment schedule. This document will show whether your EMI has changed, the tenure has reduced, or both. It also helps verify that the payment has been adjusted correctly against the outstanding principal.

Taking a few minutes to review these conditions can help you avoid surprises and maximise the value of your part payment.

Also read: 7 Checks in the Bank Loan Verification Process That Decide Approval

Part Payment vs Prepayment vs Foreclosure

The terms part payment, prepayment, and foreclosure are often used interchangeably, but they do not mean the same thing. Understanding the difference can help you choose the right repayment strategy based on your financial situation and available funds.

A part payment involves paying an additional amount towards the outstanding principal while continuing the loan. The loan remains active, and you continue repaying the remaining balance through revised EMIs or a shortened tenure.

Prepayment is a broader term that refers to repaying a loan before its scheduled end date. Part payment is one form of prepayment because you are paying a portion of the loan early.

Foreclosure, on the other hand, occurs when you repay the entire outstanding loan amount and close the loan account before the original tenure ends.

Key Differences at a Glance

|

Feature |

Part Payment |

Prepayment / Foreclosure |

|

Loan continues |

Yes |

No |

|

Principal reduced |

Yes |

Yes |

|

Future EMIs remain |

Yes |

No |

|

Full loan closure |

No |

Yes |

When Is Each Option Suitable?

-

Part payment is suitable when you have surplus funds but not enough to clear the entire loan.

-

Foreclosure may be considered when you have sufficient funds to repay the complete outstanding balance and want to eliminate future interest obligations altogether.

-

Both options can reduce interest costs, but the eligibility criteria, charges, and conditions vary between lenders.

Managing Short-Term Cash Needs Responsibly With Pocketly

While part payments can help reduce existing loan obligations, unexpected expenses can sometimes create temporary cash shortages. An urgent medical bill, exam fee, rent payment, insurance premium, or a business-related expense can be simplified by having access to short-term funds. It can help you manage essential costs without disrupting your financial commitments.

Pocketly is a digital lending platform working with RBI-registered NBFCs, designed to help students, salaried professionals, and small entrepreneurs bridge short-term liquidity gaps. Eligible users can apply for unsecured personal loans ranging from ₹1,000 to ₹25,000, with interest rates starting from 2% per month and processing fees ranging from 1% to 8%. No collateral is required, and the application process is fully digital.

How to Apply Through Pocketly

-

Download the Pocketly app or visit the website

-

Complete the digital KYC process

-

Select the required loan amount based on your eligibility

-

Receive approval and disbursal if your application is approved

The platform is designed to provide a quick and convenient borrowing experience, although eligibility, approval, and visible loan limits may vary based on an individual's profile and verification results.

If a temporary expense creates a cash gap before your next salary, stipend, client payment, or business receipt, consider exploring a small-ticket digital loan solution that matches your needs and repayment capacity.

Conclusion

Managing a loan is not only about paying EMIs on time. Small financial decisions made during the repayment journey can shape how comfortably you handle future expenses and opportunities. Using surplus income wisely, staying aware of lender terms, and planning repayments strategically can help you maintain stronger financial control over time.

If you ever need quick support for short-term expenses between salaries, client payments, or monthly cash inflows, download the Pocketly app to explore fast and convenient digital loan options designed for everyday financial needs.

Frequently Asked Questions

1. What is part payment in a personal loan?

Part payment is an additional payment made towards your outstanding loan principal before the loan tenure ends. It is separate from your regular EMI and helps reduce the remaining loan balance without closing the loan completely.

2. Does part payment reduce EMI or loan tenure?

It can do either, depending on your lender's policy. Some lenders reduce the EMI while keeping the tenure unchanged, whereas others keep the EMI the same and shorten the repayment period. In some cases, borrowers may be allowed to choose between the two options.

3. Are there any charges for making a part payment?

Some lenders may levy part-payment or processing charges, and applicable taxes such as GST may also apply. There could also be restrictions such as lock-in periods or minimum payment requirements. Always review the lender's terms before making a part payment.

4. Can I make multiple part payments during the loan tenure?

Many lenders allow multiple part payments, but the frequency and conditions vary. Some may limit the number of part payments permitted each year or specify a minimum amount for every payment. Check your loan agreement or contact the lender for exact details.

5. Is part payment better than foreclosure?

Neither option is universally better. Part payment is useful when you have some surplus funds but not enough to repay the entire loan. Foreclosure may be suitable if you can comfortably clear the full outstanding balance and want to eliminate future interest obligations completely.

6. When is the best time to make a part payment on a loan?

Part payments often have the greatest impact when made earlier in the loan tenure because a larger principal balance is still outstanding. Reducing the principal sooner can lower the amount on which future interest is calculated, potentially increasing overall savings.