You may have heard this often: when interest rates go up, bond prices fall. The statement is simple, but the reasoning behind it is not always clear.

If bonds offer fixed returns, their value should stay constant. But in reality, their price keeps changing as interest rates move.

Here is the key idea: bond prices fall because fixed returns become less valuable when interest rates rise.

When new bonds start offering higher returns, older bonds with lower fixed payouts become less attractive. To adjust for this difference, their price drops so that their overall return remains competitive in the market.

Understanding this relationship is important, especially when interest rates are rising. It affects not just investments, but also how borrowing costs, EMIs, and financial decisions change over time.

This blog explains how bond pricing works when interest rates go up, the calculation behind it, and what it means in real-world financial situations.

Key Takeaways

-

Bond prices and interest rates move in opposite directions. When market rates rise, existing bonds with lower fixed returns become less attractive.

-

Bond pricing is based on present value. Future coupon payments and face value are discounted using the new market interest rate.

-

Longer-term and lower-coupon bonds usually see bigger price drops. Their future cash flows are more exposed to changes in discounting.

-

Understanding bond pricing builds broader financial clarity. The same rate logic also affects EMIs, borrowing costs, and repayment decisions.

-

When rates are rising, cost awareness matters more. Whether you are investing or borrowing, the right decision depends on total value, not just headline numbers.

What Happens to Bond Prices When Interest Rates Rise

When interest rates rise, new bonds enter the market offering higher returns. This creates an immediate comparison for investors.

The issue is that existing bonds continue to pay the same fixed interest. Their returns do not adjust to match the new, higher rates available.

As a result, these older bonds become less attractive. Investors are not willing to pay the same price for a bond that offers lower returns than what is currently available.

To balance this difference, the price of existing bonds falls.

For example, if a bond offers a fixed return and newer bonds start offering higher returns, the only way for the older bond to stay relevant is for its price to drop. This adjustment ensures that the effective return for a new buyer aligns more closely with current market rates.

This is why bond prices and interest rates move in opposite directions.

Why Bond Prices Fall When Interest Rates Rise

The reason bond prices fall comes down to comparison. Investors always look for the best return available for the same level of risk.

When interest rates rise, new bonds start offering higher returns. Existing bonds, however, continue to pay the same fixed interest.

This creates a gap.

-

Existing bonds have fixed returns: Their coupon payments do not change even when market rates increase

-

New bonds reflect current market rates: They offer higher returns for similar risk

-

Investors shift toward better returns: No one will pay full price for a bond that pays less than what is available in the market

-

Prices adjust to stay competitive: The only way older bonds attract buyers is by becoming cheaper

For example, if your bond pays a lower return compared to new bonds, a buyer will only consider it if the price drops enough to make the overall return competitive.

This adjustment is automatic in the market. Even though the bond’s payments remain fixed, its price changes to match current interest rate expectations.

How Bond Pricing Actually Works in the Market

To understand how bond prices change, you need to look at three basic components. These determine how a bond is valued in the market at any point.

-

Face value: This is the amount the bond pays back at maturity. It remains fixed and does not change with market conditions.

-

Coupon rate: This is the fixed interest the bond pays, based on its face value. It stays constant throughout the life of the bond.

-

Market interest rate: This is the return investors currently expect from similar bonds. It keeps changing based on economic conditions.

The key issue arises when these three do not align.

-

If the market rate goes higher than the coupon rate, the bond becomes less attractive

-

If the market rate goes lower than the coupon rate, the bond becomes more valuable

This is where price adjustment happens. The bond’s interest payment does not change, but its market price moves so that the overall return matches current expectations.

For example, if a bond pays a fixed return and market rates increase, its price will fall to offer a competitive yield. If rates decrease, its price may rise because its fixed return becomes more attractive compared to new bonds.

This dynamic is the foundation of how bond pricing works.

Also Read: Legal Interest Rates in India: What Professionals Should Know Before Borrowing

How Bonds Are Priced When Interest Rates Rise (step-by-step)

When interest rates rise, the bond’s cash flows do not change. What changes is how those future payments are valued in today’s terms.

The calculation works by adjusting the bond’s price so that its return matches the new, higher market rate.

Here is the step-by-step approach:

Step 1: Identify all future cash flows

A bond provides two types of payments:

-

Regular interest payments (coupon)

-

Final repayment of the face value at maturity

Step 2: Use the new market interest rate as the discount rate

When rates go up, investors expect higher returns. This new rate becomes the benchmark for valuation.

Step 3: Discount each future payment to present value

Each future cash flow is adjusted using the higher market rate.

-

The further the payment is in the future, the lower its present value

-

A higher rate reduces these values more sharply

Step 4: Add all discounted values

The total of all discounted coupon payments and the face value gives the bond’s new price.

New Bond Price = Present Value of Coupons + Present Value of Face Value

The key outcome is straightforward:

-

Higher interest rates → higher discounting → lower present value → lower bond price

For example, if a bond pays fixed annual interest and market rates increase, each of those payments becomes less valuable in today’s terms. To compensate, the bond’s price falls so that a new buyer earns a return aligned with current market rates.

This is why bond pricing always adjusts when interest rates change, even though the bond’s payments remain fixed.

The same rate logic applies to borrowing too. If rising interest rates are making short-term credit decisions harder, a smaller option like Pocketly can help you manage urgent needs without taking on a larger loan.

Also Read: The Ultimate Guide to Small Business Loans in India (2026)

Simple Example of Bond Price Falling with Rising Rates

The calculation becomes clearer when you look at a simple example. Instead of focusing on formulas, it helps to see how price adjusts in a real situation.

Let’s break it down:

Bond details

-

Face value: ₹1,000

-

Coupon rate: 5%

-

Annual interest payment: ₹50

Market condition changes

-

New bonds are now offering a higher return

-

Investors can earn more from similar investments

What this means for the existing bond

-

The ₹50 annual return is now lower compared to the market

-

Buyers will not pay ₹1,000 for a bond offering a lower return

Price adjustment happens

-

The bond’s price drops below ₹1,000

-

This lower price increases the effective return for a new buyer

The bond becomes cheaper so that its fixed ₹50 return feels competitive in a higher interest rate environment.

For example, if the price drops enough, the return calculated on the new, lower price becomes closer to what new bonds are offering. This is how the market balances fixed returns with changing interest rates.

This example shows that the bond’s payments stay the same, but its price adjusts to reflect current market expectations.

What Decides How Much a Bond Price Falls

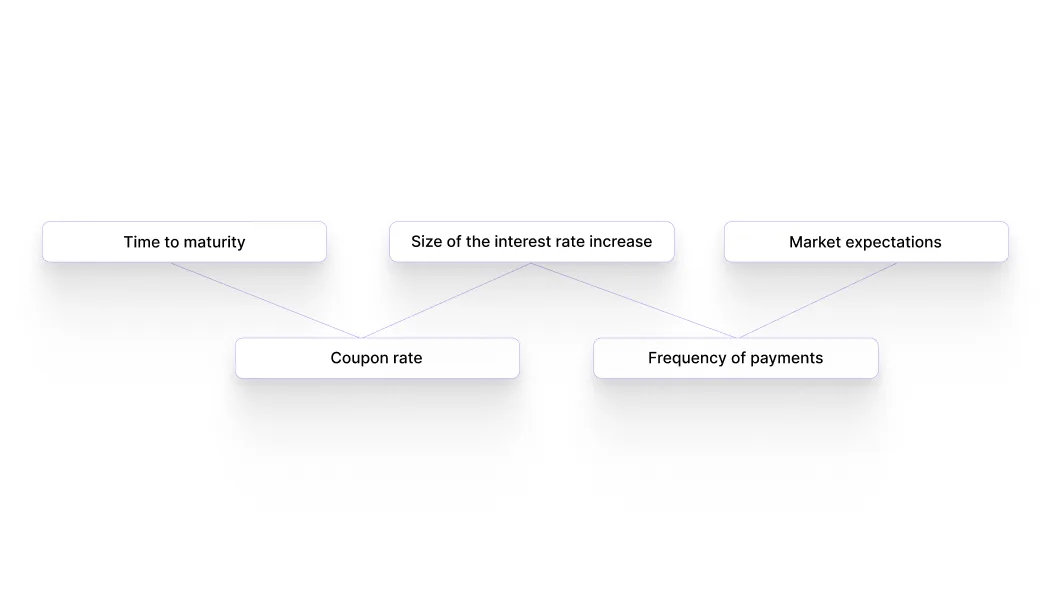

Not all bonds react the same way when interest rates rise. Some may see a sharp drop in price, while others move only slightly.

The difference depends on a few key factors:

-

Time to maturity: Bonds with a longer time remaining are more affected because more future payments are discounted at the higher rate.

-

Coupon rate: Bonds with lower interest payments tend to fall more in price since they already offer less return compared to the market.

-

Size of the interest rate increase: A small increase may cause limited price movement, while a larger jump can lead to a sharper drop.

-

Frequency of payments: Bonds that pay interest more frequently may adjust differently compared to those with annual payments.

-

Market expectations: If investors expect rates to rise further, bond prices may fall more in advance.

For example, a long-term bond with a low coupon rate will typically see a bigger price drop than a short-term bond with a higher coupon. This is because more of its value depends on future payments, which are now discounted more heavily.

Understanding these factors helps explain why bond prices do not move uniformly when interest rates change.

Why Long-Term Bonds Fall More When Rates Rise

The impact of rising interest rates is not the same for all bonds. Long-term bonds usually see a larger change in price compared to short-term ones.

The reason comes down to how future payments are affected over time.

-

More future payments are involved: Long-term bonds have many interest payments spread across years. Each of these gets discounted at the new, higher rate.

-

Greater impact of discounting: The further a payment is in the future, the more its present value reduces when rates increase.

-

Money is locked in for longer: Investors compare long-term bonds with newer options offering better returns over the same period. This makes older bonds less attractive.

-

Higher sensitivity to rate changes: Even a small increase in interest rates can significantly reduce the present value of long-term cash flows.

For example, a bond maturing in ten years will be affected more than one maturing in one year. The longer duration means more future payments are adjusted downward, leading to a larger drop in price.

This is why long-term bonds are considered more sensitive to interest rate changes.

What Rising Interest Rates Mean for Everyday Money Decisions

Interest rate changes do not affect only bonds. They influence how money behaves across savings, investments, and borrowing decisions.

If you understand how pricing adjusts in bonds, you can apply the same thinking to everyday financial choices.

Here is how rising rates show up in real situations:

-

Borrowing becomes more expensive: Loans may carry higher interest costs, which increases the total amount you repay over time.

-

EMIs and repayment pressure can increase: For variable-rate loans, monthly payments may rise when interest rates move up.

-

Delaying decisions can change costs: Waiting during rising rate cycles can result in higher borrowing costs later.

-

Returns on savings and fixed-income options improve: Higher interest rates may benefit new investments, but older ones may become less attractive.

-

Cost awareness becomes more important: Just like bond prices adjust, borrowing decisions should also factor in total cost, not just speed or convenience.

For example, when interest rates increase, even a small borrowing decision can become more expensive if not planned properly. Understanding how interest affects value helps you make clearer financial choices, whether you are investing or managing short-term expenses.

When borrowing costs start rising, keeping the amount small and repayment short becomes more important. Pocketly can be a practical option for limited, short-term needs where speed and cost clarity matter.

Also Read: Fixed vs Floating Interest Rate in India (2026): Which Is Best for You?

Manage Small Borrowing Needs Better with Pocketly

The same logic that affects bond prices applies to everyday borrowing as well. When interest rates rise, the cost of money increases. Even small borrowing decisions can become more expensive if they are not structured carefully.

This makes one thing clear: the amount you borrow and how long you hold it matter as much as the rate itself.

In situations like a sudden bill, travel expense, or short-term cash gap, the goal is not to take out a large loan. It is to solve the need without carrying interest for longer than necessary.

This is where Pocketly fits in.

Pocketly is a digital lending platform working with RBI-registered NBFCs, designed for short-term borrowing needs where speed and cost clarity matter.

Here is how it supports better borrowing decisions:

-

Small-ticket borrowing only: Loan amounts range from ₹1,000 to ₹25,000, so the borrowing stays aligned with the actual need.

-

No collateral required: You do not need to pledge any asset or arrange a guarantor to apply.

-

Fast digital process: The application, KYC, and approval process happen online, which makes it easier to act when the need is immediate.

-

Transparent pricing: Interest starts from 2% per month, and processing fees range from 1% to 8%, depending on profile and loan amount.

-

Funds sent directly to your account: Once approved, the amount is transferred to your bank account so you can handle the expense without delay.

Getting started is simple:

-

Download the app or visit the website

-

Complete quick digital KYC

-

Select the loan amount

-

Review the terms and receive funds upon approval

Note: The maximum loan amount of ₹25,000 depends on profile and eligibility. Some users may see lower limits initially.

If you need to manage a small short-term expense during a rising rate cycle, check your eligibility on Pocketly and review the total cost before choosing a larger borrowing option.

FAQs

Q: Why do bond prices fall when interest rates go up?

Bond prices fall because existing bonds offer fixed returns, while new bonds start offering higher returns when rates rise. To stay competitive, older bonds must drop in price so their yield matches the market.

Q: How are bonds priced when interest rates increase?

Bond pricing is based on the present value of future cash flows. When interest rates increase, those cash flows are discounted at a higher rate, which lowers the bond’s current price.

Q: What is the formula used to calculate bond prices?

The bond price is calculated as the present value of all future coupon payments plus the present value of the face value at maturity. These are discounted using the current market interest rate.

Q: Do all bonds fall equally when interest rates rise?

No, bonds react differently based on their maturity, coupon rate, and structure. Longer-term and lower-coupon bonds typically see larger price drops compared to short-term or higher-coupon bonds.

Q: Why are long-term bonds more affected by rising interest rates?

Long-term bonds have more future payments that are impacted by higher discounting. The longer the duration, the greater the reduction in present value when interest rates increase.

Q: How do rising interest rates affect investors?

Investors holding existing bonds may see a decline in market value. However, new investments can offer higher returns, which may improve future earning potential.