Ever feel like your money disappears before you even realise it? Pay cheques come and go, bills stack up, and goals like saving or investing seem out of reach. Financial uncertainty can leave you stressed, anxious, and unsure of your next move.

A financial checklist changes all that. It’s a simple, organised way to track income, monitor expenses, plan for goals, and prepare for unexpected costs. By having a clear roadmap, you no longer react to your finances; you control them.

In this blog, we will break down the essential steps to create a financial checklist, show you how to prioritise your money, and guide you toward managing debt, saving smartly, and planning for future goals. With this approach, financial decisions become intentional, stress is reduced, and progress toward your goals becomes measurable and achievable.

TL;DR

- Gain Full Control of Your Money: Track income, expenses, savings, debts, and goals to make intentional financial decisions instead of reacting to surprises.

- Prevent Missed Payments & Stress: Organise bills, EMIs, subscriptions, and insurance deadlines to avoid penalties and reduce financial anxiety.

- Prioritise Savings & Goals: Allocate funds for short-term needs and long-term objectives, ensuring consistent progress toward personal and family goals.

- Spot Overspending & Optimise Cash Flow: Monitor variable expenses, identify wasteful spending, and make smarter financial choices without sacrificing essentials.

- Stay Ready for Emergencies: Regularly review your checklist and use tools like Pocketly for short-term financial support to maintain stability.

What Is a Financial Checklist?

A financial checklist is a structured list of tasks and reminders designed to help you manage your money efficiently. It covers all critical areas of personal finance, ensuring nothing important is overlooked, from bills and budgeting to savings, investments, and debt management.

Key features

- Covers income, expenses, savings, and investments

- Includes debt tracking and upcoming financial obligations

- Can be monthly, quarterly, or yearly, depending on your needs

- Helps identify gaps or missed tasks in your financial planning

- Encourages proactive rather than reactive money management

Example: If you’re planning for a family vacation, a financial checklist can remind you to track your monthly savings, pay pending bills, review your travel budget, and adjust other expenses to stay on track.

Note: A checklist is a planning tool, not a magic solution; it works best when reviewed and updated regularly.

Why You Need a Financial Checklist?

A financial checklist is more than just a list; it’s your roadmap to smarter money management. It helps you stay organised, track progress, and make intentional financial decisions instead of scrambling at the last minute.

1. Avoid Missed Payments and Penalties

- Keep all recurring bills, EMIs, subscriptions, and insurance payments in one place.

- Stay on top of due dates to protect your credit score and avoid late fees.

- Example: Tracking rent, phone bills, and Netflix subscriptions ensures nothing slips through unnoticed.

2. Achieve Your Financial Goals Consistently

- Allocate funds for short-term needs (groceries, monthly savings) and long-term objectives (investments, emergency fund, retirement).

- Monitor whether your planned contributions match your goals month over month.

- Example: A professional in Mumbai uses the checklist to ensure SIPs, vacation savings, and emergency fund contributions are met every month.

3. Track Spending Patterns and Spot Opportunities

- Analyse where your money goes, identify overspending areas, and find room to save more.

- Helps create a realistic picture of your cash flow for better decision-making.

- Example: Noticing high dining-out expenses prompts adjustments, freeing money for investments.

4. Reduce Financial Stress and Gain Control

- Gives clarity about your financial position at a glance, reducing uncertainty and anxiety.

- Helps you plan for emergencies without panicking.

- Example: Knowing all bills are accounted for allows you to focus on career or personal goals without money worries.

5. Build Disciplined Financial Habits

- Encourages intentional spending instead of impulsive purchases.

- Makes saving a consistent, non-negotiable part of your routine.

- Example: Weekly reviews of the checklist ensure discretionary spending stays within budget and savings targets are met.

Core Components of a Financial Checklist

A complete financial checklist covers all areas of your money life, from income tracking to planning for future goals. Including these components ensures nothing important is overlooked.

A complete financial checklist covers all areas of your money life, from income tracking to planning for future goals. Including these components ensures nothing important is overlooked.

1. Income and Cash Flow

Knowing exactly how much money comes in each month is the foundation of financial control. Include salary, freelance work, dividends, or any side income. Mapping inflows against outflows helps you see where your money goes and plan more effectively.

For example, a young professional in Mumbai earning ₹50,000 from salary and ₹5,000 from freelance work can allocate ₹20,000 for fixed expenses, ₹15,000 for variable spending, and the remaining ₹20,000 toward savings and investments. This gives a clear snapshot of cash flow and prevents overspending.

2. Fixed and Recurring Expenses

Fixed expenses like rent, EMIs, insurance premiums, and subscriptions can quietly eat up a big chunk of your income. Recording them ensures no bill is missed and helps prioritise essentials.

For example, if rent is ₹15,000, EMI ₹3,500, and a streaming subscription ₹299, noting these expenses in your checklist prevents late fees and clarifies how much you have left for discretionary spending.

3. Variable Expenses

Variable expenses like groceries, transport, dining out, or shopping can fluctuate significantly. Tracking them highlights patterns, uncovers hidden overspending, and helps you adjust without feeling restricted.

For instance, if groceries cost ₹6,000 instead of the planned ₹4,500, you can cut back slightly on eating out or entertainment for that month, staying within your overall budget without sacrificing essentials.

4. Savings and Investment Goals

Allocating money toward savings and investments ensures you stay on track for both short-term needs and long-term security. Include emergency funds, retirement contributions, SIPs, and any planned goals.

For example, setting aside ₹5,000 per month for an emergency fund and ₹3,000 for a vacation ensures consistent progress toward financial goals while still covering regular expenses.

5. Debt and Liability Management

Tracking debts like personal loans, credit cards, or EMIs prevents missed payments, high interest, and unnecessary stress. Include amounts due, interest rates, and payment dates.

For example, noting a personal loan EMI of ₹3,500 due on the 10th and a credit card bill of ₹7,000 due on the 25th keeps payments on time and avoids late fees.

6. Insurance and Contingency Planning

Insurance protects you against unexpected costs, so keep a record of all policies and renewal dates. Include health, life, and property insurance to avoid coverage gaps.

For instance, if your health insurance premium is ₹1,200 annually, marking the renewal date in your checklist ensures timely payment and uninterrupted protection, preventing financial strain during emergencies.

7. Regular Review and Adjustment

A financial checklist is only effective if reviewed regularly. Check your finances monthly or quarterly to track progress, adjust allocations, and stay flexible as needs change.

For example, if an unexpected medical expense of ₹4,000 comes up, you can temporarily reduce entertainment or shopping for the month while keeping savings contributions on track. This keeps your finances balanced without stress.

Also Read: Effective Debt Management Strategies and Tips

How to Build Your Personalised Financial Checklist?

Creating a financial checklist isn’t just about writing down numbers. It’s about building clarity, reducing stress, and giving your money a purposeful direction. Here’s a structured step-by-step process to create one that works in real life.

Step 1: Capture Every Source of Income

Document all money coming in, including salary, freelance work, dividends, or side hustles. This gives you a full picture of resources available for spending, saving, and investing.

Example: A professional in Mumbai earns ₹50,000 monthly from a job and ₹5,000 from freelance writing. Recording both streams ensures accurate allocation for bills, lifestyle, and savings.

Outcome: Prevents underestimation, helps realistic budgeting, and reduces month-end surprises.

Step 2: List Fixed Monthly Expenses

Include non-negotiable costs like rent, EMIs, subscriptions, and insurance. Note due dates to avoid late fees and plan cash flow in advance.

Example: Rent ₹18,000, EMI ₹4,000, internet ₹800, gym ₹1,000. Knowing these commitments shows exactly how much of your income is already spoken for.

Outcome: Provides visibility into essential spending and sets the baseline for discretionary allocations.

Step 3: Track Variable and Lifestyle Expenses

Estimate costs that fluctuate each month, such as groceries, transport, dining, and entertainment. Review bank statements, UPI history, or expense tracker apps to get accurate numbers.

Example: Groceries ₹6,000, transport ₹2,500, dining out ₹4,000.

Outcome: Prevents overspending, encourages mindful discretionary choices, and keeps lifestyle spending within control.

Step 4: Allocate Savings and Investments

Decide in advance how much to save or invest each month. Include emergency funds, retirement, or travel goals. Treat these allocations like non-negotiable bills.

Example: Save ₹5,000 for an emergency fund and ₹3,000 for a vacation.

Outcome: Builds long-term financial security and ensures consistent progress toward personal goals.

Step 5: Include Debts and Liabilities

Record all outstanding debts, credit card balances, personal loans, or EMIs. Include principal, interest rates, and due dates. Prioritise higher-interest debts first, but never skip smaller mandatory payments.

Example: Credit card bill of ₹7,000 due on the 25th with 2.5% interest, personal loan EMI of ₹3,500 due on the 10th.

Outcome: Avoids missed payments, reduces interest costs, and improves credit health.

Step 6: Record Insurance Policies and Contingencies

List all policies: health, life, vehicle, property, and even travel insurance. Include premiums, renewal dates, and coverage details.

Example: Health insurance premium of ₹1,200 due in September, vehicle insurance of ₹3,500 due in November.

Outcome: Protects against unexpected financial shocks and ensures continuous coverage.

Step 7: Schedule Regular Reviews

Review your checklist monthly or quarterly. Adjust allocations for changes in income, unexpected expenses, or evolving goals.

Example: A medical expense of ₹4,000 arises mid-month. Adjust dining out or discretionary spending to maintain balance.

Outcome: Turns a static checklist into a dynamic tool that adapts to real-life changes, keeping finances on track.

Common Mistakes to Avoid With a Financial Checklist

A financial checklist can simplify money management, keep you organised, and guide smarter decisions. But even the best checklist loses its impact if common mistakes creep in. Knowing these pitfalls ensures your checklist stays accurate, up-to-date, and truly effective in achieving your financial goals.

A financial checklist can simplify money management, keep you organised, and guide smarter decisions. But even the best checklist loses its impact if common mistakes creep in. Knowing these pitfalls ensures your checklist stays accurate, up-to-date, and truly effective in achieving your financial goals.

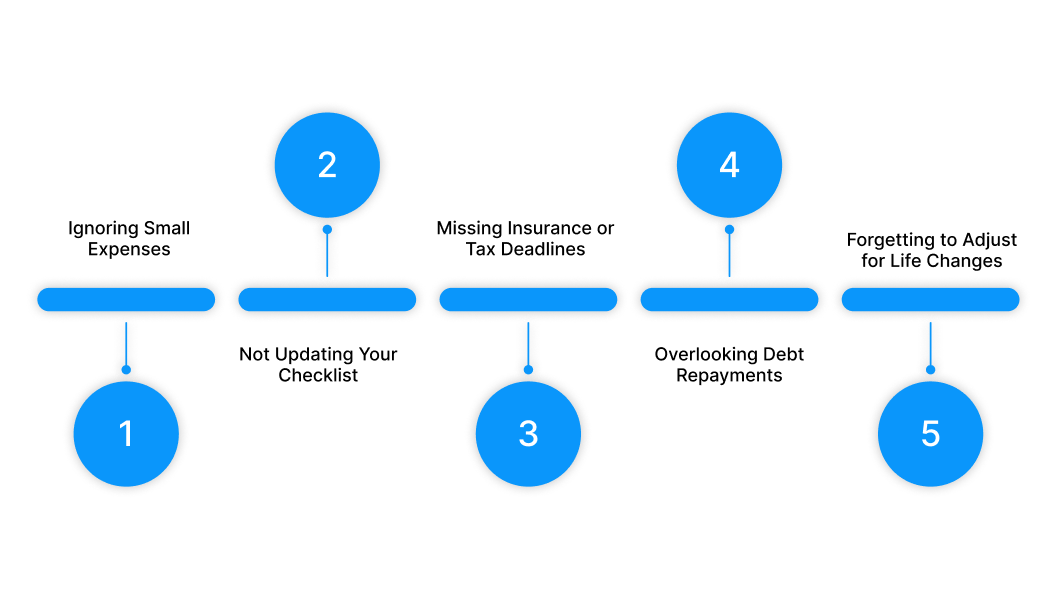

1. Ignoring Small Expenses

Small, everyday purchases like coffee, snacks, or online subscriptions may seem insignificant, but they can quietly add up and distort your budget. Ignoring them can create a false sense of financial stability and lead to gaps in your planning.

How to avoid it: Include all minor recurring and one-off expenses in your checklist. Track them using an app, spreadsheet, or a simple notes section. Over time, this gives you a realistic picture of where your money goes and prevents surprises at month-end.

Example: Spending ₹200 daily on coffee might seem small, but over a month, it totals ₹6,000. Recording it ensures you account for it in your budget and avoid overspending.

2. Not Updating Your Checklist Regularly

A checklist is only useful if it reflects your current financial situation. Failing to update it regularly can lead to missed payments, misaligned savings goals, and inaccurate projections.

How to avoid it: Set a recurring schedule weekly, bi-weekly, or monthly to review and update your checklist. Adjust for any new expenses, income changes, or completed goals.

Example: If your mobile plan changes from ₹500 to ₹800 per month, failing to update your checklist could make you under budget for essentials, forcing adjustments later.

3. Missing Insurance or Tax Deadlines

Forgetting insurance renewals, tax filing dates, or premium payments can result in penalties, lapses in coverage, or extra costs. This is one of the biggest risks that a financial checklist is designed to prevent.

How to avoid it: Add all deadlines to your checklist with reminders a week or two in advance. Consider syncing them with your calendar or phone alerts for timely action.

Example: Annual health insurance renewal missed by a week could cost a late fee or loss of benefits. A well-maintained checklist ensures you never skip these critical deadlines.

4. Overlooking Debt Repayments

Untracked EMIs, credit card dues, or personal loans can quickly accumulate penalties and damage your credit score if missed.

How to avoid it: List all debts in your checklist with due dates, amounts, and payment methods. Regularly check off payments once done to maintain clarity and accountability.

Example: Forgetting a credit card payment of ₹10,000 could lead to ₹500 late fees and interest, plus a drop in your credit score. A checklist keeps these obligations visible and manageable.

5. Forgetting to Adjust for Life Changes

Major changes like a salary increase, relocation, marriage, or new family responsibilities affect your financial landscape. Not updating your checklist accordingly can render it ineffective.

How to avoid it: Reassess your checklist whenever your financial situation changes. Adjust allocations for savings, lifestyle expenses, and financial goals.

Example: After a salary hike, your checklist should reflect higher savings contributions or investments, instead of letting extra income get absorbed by unnecessary spending.

Also Read: Should You Save for an Emergency Fund or Pay Off Debt?

Cover Unexpected Expenses Instantly With Pocketly

No financial checklist can predict every surprise expense. From urgent medical bills to sudden travel or home repairs, Pocketly provides fast, hassle-free support to keep your budget on track.

Here’s how Pocketly helps you stay prepared:

- Borrow only what you need: Loans range from ₹1,000 to ₹25,000, so you take just the right amount.

- No collateral or guarantor required: Quick approval without assets or co-signers.

- Instant approval and transfer: KYC-based verification ensures funds reach your bank in minutes.

- Flexible repayment options: Choose a plan that aligns with your monthly budget.

- Transparent pricing: Interest starts at 2% per month with 1–8% processing fees and no hidden charges.

- Available anytime, anywhere: Manage loans 24/7 through the Pocketly app.

With Pocketly, your financial checklist isn’t just a plan; it’s actionable. Handle emergencies confidently, maintain your financial stability, and keep your long-term goals intact.

Conclusion

Using a financial checklist is one of the simplest yet most effective ways to stay on top of your money in 2026. By tracking income, expenses, debts, and savings in one place, you can make intentional decisions instead of reacting to surprises.

A checklist isn’t about restriction; it’s about clarity, control, and aligning your finances with your goals. It reduces stress, prevents missed payments, and keeps your long-term plans on track.

When urgent expenses come up, tools like Pocketly can provide quick, responsible support, helping you bridge short-term gaps without disrupting your broader financial strategy.

Take charge of your money today, start your financial checklist, and download the Pocketly app today on [Android] or [iOS] to manage your finances smarter and stress-free.

FAQs

1. What is a financial checklist?

A financial checklist is a structured list of all your income, expenses, savings, debts, insurance, taxes, and financial goals. It helps you track your money, avoid missed payments, and stay aligned with your short- and long-term plans.

2. Why do I need a financial checklist?

Even if you earn well, money can slip away without proper tracking. A checklist gives clarity, prevents missed deadlines, helps prioritise spending, and ensures you’re saving and investing consistently.

3. How often should I update my financial checklist?

Ideally, review it weekly or at least once a month. Update it whenever there’s a change in income, expenses, or financial goals. Regular updates ensure your checklist stays accurate and actionable.

4. Can I use a financial checklist if I have multiple income sources?

Yes. List all income streams separately, including salary, freelance work, side hustles, or business income. This helps you understand total cash flow and plan your expenses and savings more effectively.

5. Should I track small daily expenses in my checklist?

Absolutely. Small expenses like coffee, transport, or online subscriptions can add up and derail your budget if ignored. Tracking every rupee gives a complete picture of your finances and helps prevent overspending.