The message arrives late in the evening: Payment due tomorrow. Rent, a medical bill, or a sudden travel expense refuses to wait patiently. Moments like these quietly push many of us to start searching online for quick loan options.

Banks often appear as the safest route for borrowing, but the process can stretch across days of forms and approvals. Direct lenders, especially digital platforms, promise faster access to smaller loans with far fewer steps involved. The real challenge is figuring out which option actually suits the situation without creating more financial pressure later.

Borrowing today is no longer limited to visiting a bank branch and waiting endlessly for approval. Understanding how these two options differ can help avoid delays, confusion, and unnecessary borrowing costs.

Key Takeaways

-

Direct lender instalment loans usually offer fully online applications, quick approvals, and faster disbursals, while traditional bank loans often involve manual checks and longer processing times.

-

Banks typically provide higher loan amounts with longer repayment tenures, whereas direct lenders focus on smaller personal loans repaid through short-term instalments.

-

The true cost of a loan includes interest rates, processing fees, repayment terms, and late payment charges, not just the advertised rate.

-

Choosing the right loan depends on approval speed, eligibility requirements, loan size needed, and repayment flexibility for the borrower’s situation.

What are Installment Loans From Direct Lenders?

Instalment loans from direct lenders are short-term personal loans offered by lending platforms that deal with borrowers without routing applications through traditional banks. The entire process usually happens online, where identity verification, eligibility checks, and approvals are completed digitally within minutes.

Once approved, the borrowed amount is repaid through fixed instalments over a defined period, making it easier to manage smaller financial gaps without long approval cycles.

What Traditional Bank Loans Usually Offer People Taking Loans?

Bank loans are often the first option people think about when planning to borrow money for bigger or planned expenses.

Here are some common things people usually experience when applying for a traditional bank loan in India.

-

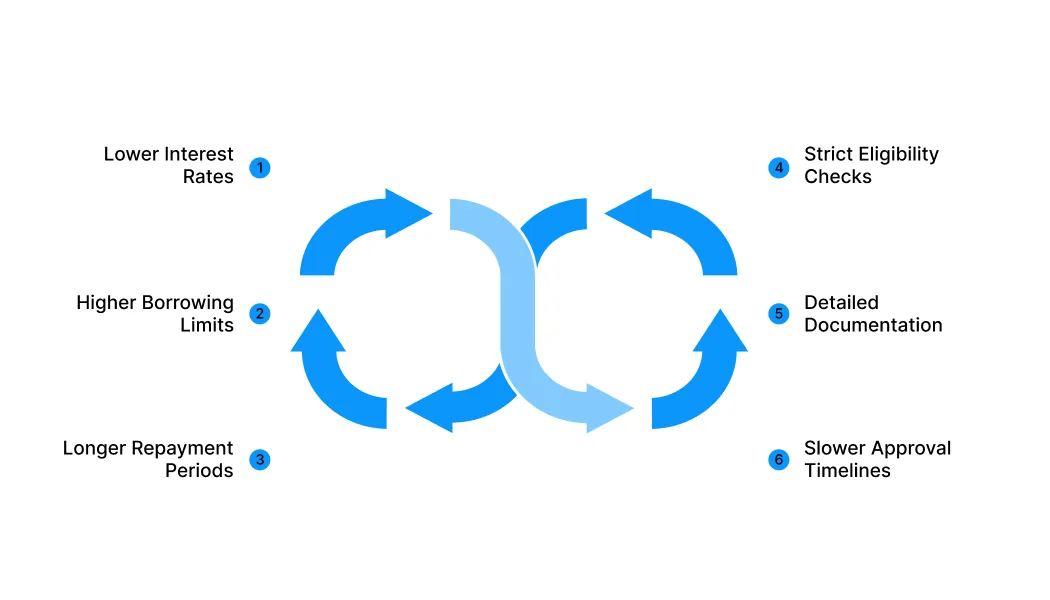

Lower interest rates: Banks often provide comparatively lower interest rates, especially for applicants with strong credit scores and stable income history.

-

Higher borrowing limits: Traditional banks usually allow larger loan amounts, which makes them suitable for planned expenses like education, weddings, or home improvements.

-

Longer repayment periods: Loan tenures from banks typically stretch across several years, helping reduce monthly instalment pressure for bigger financial commitments.

-

Strict eligibility checks: Banks carefully review credit scores, employment stability, income proof, and existing debts before approving most loan applications.

-

Detailed documentation: Applicants are generally required to submit identity proof, address proof, income records, and sometimes additional verification documents.

-

Slower approval timelines: Because banks follow multiple verification steps, approvals and disbursements can sometimes take several days or even weeks.

Also read: Interest Rates in India 2026: How They Affect Loans & Savings

With both loan types explained individually, it becomes easier to see how their application process and borrowing experience actually differ.

Direct Lender Instalment Loans vs Traditional Bank Loans

Both loan options promise quick financial help, but the real experience often feels very different once applications begin.

Here is how each loan type usually works when someone in India actually tries to borrow money.

1. Direct Lender instalment Loans

These loans are often chosen when money is needed quickly for urgent expenses without waiting days for approvals.

Here are some practical ways these loans usually work for people applying through digital lending platforms.

-

Fast online applications: Most direct lenders allow applications through mobile apps, where details, KYC, and bank verification are completed within minutes.

-

Same-day loan approvals: Automated systems review credit score, bank transactions, and income patterns to approve many loans quickly.

-

Quick bank transfers: Once approved, money is often credited within hours, making them useful for emergencies or short-term expenses.

-

Smaller borrowing amounts: These loans usually range between smaller limits, commonly used for bills, travel bookings, or urgent household costs.

-

Short repayment schedules: Borrowers repay the loan through fixed instalments spread across a few weeks or months.

2. Traditional Bank Loans

Many people consider banks first when planning larger loans, especially for expenses that are not extremely urgent.

Here are some things people usually experience when applying for a loan through a traditional bank.

-

Longer application steps: Banks often require salary slips, bank statements, and employment verification before processing most loan requests.

-

Slower approval timelines: Credit teams review documents manually, which often means waiting several working days for final approval.

-

Higher loan limits: Banks typically approve larger loan amounts suited for expenses like education fees, weddings, or home renovations.

-

Long repayment tenures: Repayment periods may stretch across several years, depending on the loan type and approved amount.

-

Lower interest rates: Borrowers with strong credit scores often qualify for lower interest rates compared with many short-term lenders.

To make the differences clearer at a glance, here is a simple side-by-side comparison of both loan options.

|

Factor |

Direct Lender instalment Loans |

Traditional Bank Loans |

|

Application process |

Mobile app / online form |

Branch visit/bank portal |

|

Approval speed |

Minutes to hours |

Several days |

|

KYC process |

Digital verification |

Physical or extended checks |

|

Loan size |

Small short-term loans |

Larger loans |

|

Repayment period |

Weeks to months |

Months to years |

|

Credit checks |

Flexible/digital |

Strict credit assessment |

Beyond the basic comparison, approval speed is often the factor that matters most when money is needed quickly.

Approval Speed: Why Direct Lenders Often Disburse Funds Faster?

When money is needed urgently, the biggest concern usually becomes how quickly the loan actually reaches the bank account.

Here are a few reasons why direct lenders are often able to approve and disburse loans much faster.

-

Automated credit checks: Digital lenders use automated systems that analyse credit scores, bank transactions, and income patterns within minutes.

-

Instant digital KYC verification: Aadhaar-based verification and PAN validation allow identity checks to be completed quickly without manual paperwork.

-

No branch visits required: Applications, document uploads, and verification steps are completed online instead of visiting physical bank branches.

-

Technology-driven approvals: Algorithms review financial data instantly, reducing the waiting time usually involved in manual credit reviews.

-

Fewer approval layers: Direct lenders often operate with streamlined processes, avoiding multiple internal approvals common in traditional banks.

-

Faster fund transfers: Once approved, many lenders transfer the loan amount directly to the borrower’s bank account within hours.

Also read: Credit vs Loan in India: Key Differences & Smart Choice (2026)

Speed is only one part of the decision, though, because the total borrowing cost can vary depending on several loan charges.

Interest Rates and Total Borrowing Costs

Interest rates usually grab attention first, but the real cost of borrowing depends on several factors beyond the headline rate.

Here are a few cost elements worth comparing before choosing between direct lender instalment loans and traditional bank loans.

-

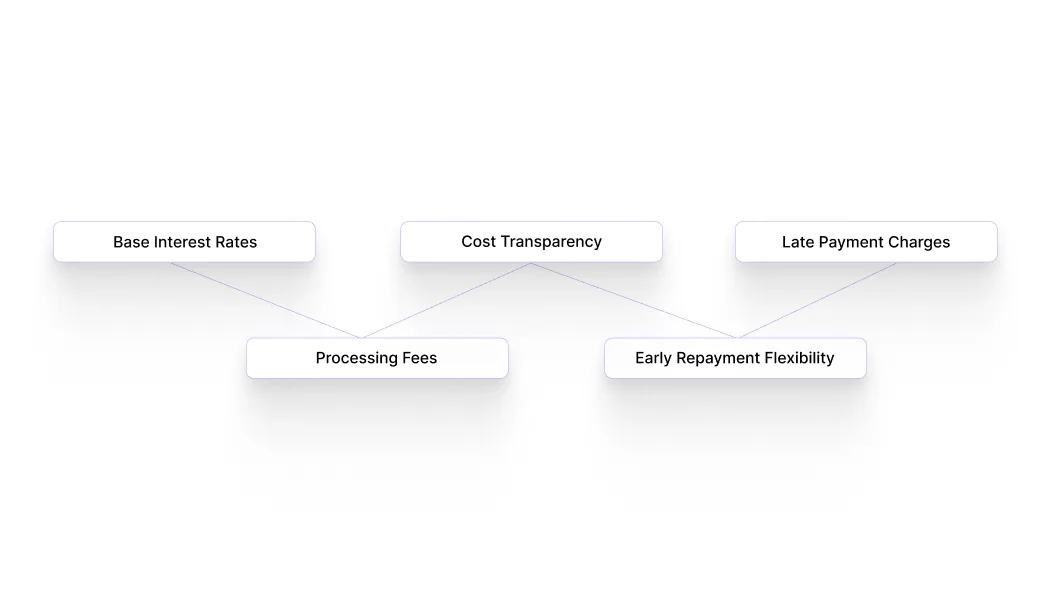

Base interest rates: Banks often advertise lower annual rates for larger loans, while direct lenders price loans based on speed and accessibility.

-

Processing fees: Banks typically charge structured processing fees, while digital lenders often include simplified service charges within the loan setup.

-

Cost transparency: Digital lending platforms usually display repayment schedules upfront, helping applicants understand instalments before confirming the loan.

-

Early repayment flexibility: Many direct lenders allow borrowers to close smaller loans earlier once repayments are manageable.

-

Late payment charges: Both banks and direct lenders apply penalties for missed instalments, encouraging borrowers to stay consistent with repayments.

Looking only at the interest rate rarely tells the full story, because loan speed, flexibility, and repayment structure also influence total borrowing cost.

Loan Eligibility: Which Option Is Easier to Get Approved For?

Many people only realise how strict loan eligibility rules are after a bank application gets rejected.

Here are a few important differences in how banks and direct lenders usually evaluate loan applications.

-

Credit score expectations: Banks often prioritise applicants with strong credit history, which can make approval difficult for first-time borrowers.

-

Income verification rules: Stable salary records and long employment history usually influence whether bank loan applications move forward.

-

Documentation requirements: Banks typically ask for salary slips, bank statements, employment proof, and identity verification during approval checks.

-

Alternative financial checks: Direct lenders often review bank transactions and financial activity to understand repayment ability.

-

Technology-based underwriting: Automated systems analyse financial behaviour quickly instead of relying only on traditional credit history.

-

Accessibility for younger applicants: People with limited credit history may still qualify when lenders assess broader financial activity.

Key note: Banks often prioritise strong financial records, while digital lenders focus on faster, more accessible eligibility checks.

Once eligibility is clear, the next question most people ask is how much they can actually borrow and how repayments will work.

How Much Can You Borrow and How Flexible Are Repayments?

Loan size and repayment flexibility often influence which option feels practical for different financial situations.

Here are a few important differences people usually notice when comparing loan amounts and repayment options.

-

Loan size availability: Banks usually approve larger loan amounts suited for planned expenses like education fees, weddings, or home improvements.

-

Smaller quick loans: Direct lenders usually focus on smaller amounts designed for urgent needs such as bills, repairs, or short-term expenses.

-

Repayment duration: Bank loans often stretch across several years, helping reduce monthly instalments for bigger borrowing amounts.

-

Shorter repayment timelines: Instalment loans from direct lenders are usually repaid within a few months through fixed instalments.

-

Flexible loan selection: Many digital lending platforms allow borrowers to choose smaller loan amounts instead of committing to large, long-term loans.

-

Manageable repayment planning: Shorter repayment schedules can help close financial gaps quickly without long financial commitments.

Even after comparing these details, small mistakes during loan comparison can still lead to unnecessary borrowing costs.

Common Mistakes to Avoid When Comparing Loan Options

Comparing loans quickly can sometimes lead to choices that do not match the actual need or repayment comfort.

Here are a few common mistakes people make while deciding between direct lender instalment loans and traditional bank loans.

-

Comparing only interest rates: Looking only at the interest rate may miss other factors like repayment period, loan size, and approval speed.

-

Ignoring how quickly funds are needed: Some situations require immediate funds, while others allow time for longer bank approval processes.

-

Choosing larger loans unnecessarily: Borrowing more than required can increase repayment pressure even when the expense itself is smaller.

-

Not checking repayment comfort: Understanding instalment amounts helps ensure the loan fits comfortably within monthly income.

-

Skipping eligibility checks beforehand: Knowing basic eligibility requirements can save time and avoid unnecessary application attempts.

-

Overlooking convenience factors: Application speed, digital access, and repayment flexibility often influence the borrowing experience as much as costs.

Also read: Personal Loan Rejection Reasons: 7 Common Causes & Fixes in 2026

Avoiding common mistakes can prevent unnecessary delays and costs, but the bigger question is which option actually helps you save more overall.

Direct Lender vs Bank Loan: Which Saves More in 2026?

Choosing between a direct lender and a bank often comes down to total cost, not just how quickly the money arrives.

To understand where you actually spend less over time, here is how both options compare across key cost factors.

Direct Lender Costs

Direct lenders offer quick access to funds, but the overall cost can vary depending on how the loan is structured.

-

Interest Rates: Often higher than banks, especially for short-term or small-ticket loans.

-

Processing Fees: Usually low or clearly stated upfront, with fewer hidden charges.

-

Flexibility Charges: Some lenders allow flexible repayment, though late fees can apply if deadlines are missed.

-

Total Cost Impact: Works out better for short-term needs where the loan is repaid quickly.

Bank Loan Costs

Bank loans are generally structured for lower interest rates over longer periods, making them suitable for planned borrowing.

-

Interest Rates: Typically lower compared with direct lenders, especially for high-credit-score applicants.

-

Processing Fees: May include documentation, processing, or administrative charges.

-

Prepayment Charges: Some banks charge fees for early repayment, affecting total savings.

-

Total Cost Impact: More cost-effective for larger loans repaid over longer durations.

What Actually Saves You More

-

Short-term borrowing: Direct lenders may cost less overall if repaid quickly despite slightly higher rates.

-

Long-term borrowing: Banks usually offer better savings due to lower interest rates spread over time.

-

Urgency vs planning: Faster access may come at a higher cost, while planned loans tend to reduce total expenses.

Saving more depends less on the lender type and more on how long the loan stays unpaid and how well it fits your financial situation.

Even after comparing costs and timelines, many people still look for a simpler option that avoids lengthy steps and gets things done quickly.

Need a Small Loan Quickly Without the Usual Hassle? Pocketly Might Be the Easier Option

Sometimes the real problem is not finding a loan, but finding one that is quick, simple, and fits smaller financial needs.

Here is how Pocketly helps people access small personal loans without complicated bank procedures.

Why Many People Choose Pocketly for Quick Loans:

-

Fast approvals: Eligible loan requests can receive approval in as little as seven minutes.

-

Loans up to ₹25,000: Borrow smaller amounts that suit urgent needs instead of committing to large, long-term loans.

-

100% digital process: Apply directly from your phone without paperwork, branch visits, or lengthy application steps.

-

Minimal KYC requirements: Only basic verification such as PAN, Aadhaar details, and video KYC is required.

-

Flexible EMI options: Choose instalment plans that comfortably match your monthly budget and repayment capacity.

-

Quick disbursal: Approved loan amounts are transferred directly to your bank account within minutes.

-

Available for different earners: Pocketly offers personal loan options for both salaried individuals and self-employed applicants.

Basic Requirements to Apply:

-

Age: 18 to 40 years

-

Identity proof: PAN card number

-

Address proof: Aadhaar-based verification

-

Verification: Video KYC and verified email ID

Pocketly keeps borrowing simple, so smaller financial needs never turn into bigger worries.

For smaller, urgent financial gaps, Pocketly makes borrowing simple with quick approvals, minimal paperwork, and a fully digital loan process.

Explore how Pocketly can help you access a quick personal loan today. Download the app and get started in minutes.

FAQs

1. Can you get a loan directly from a lender without going through a bank?

Yes, some lenders provide loans directly to borrowers without intermediaries, meaning the application, approval, and funding all happen with the same lender.

2. Are online loan applications safe to use?

Online loans can be safe when offered by legitimate and regulated lenders, but it is important to verify the lender’s credentials before applying.

3. Why do some loan applications get rejected?

Applications may be rejected due to factors like low credit scores, insufficient income, or a high debt-to-income ratio.

4. What questions should you ask before taking a personal loan?

Common questions include the purpose of the loan, the repayment period, the interest rate, and any additional fees involved.

5. Do online lenders check credit scores before approving loans?

Many online lenders still check credit scores, but they may also consider alternative financial data when evaluating applications.

6. Can you apply for multiple personal loans at the same time?

Yes, it is possible to hold multiple personal loans, but lenders will review existing debts before approving a new one.