Planning a personal loan, but not sure which credit bureau to trust? It’s a common worry, especially when each platform shows a different score. You might check one report and feel confident, then open another and wonder if lenders will see you the same way.

That confusion makes it harder when you’re handling tight monthly budgets, emergency expenses, or trying to build a stable credit record. And with names like CIBIL, Experian, Equifax, and Highmark everywhere, it’s natural to question which one truly captures your credit behaviour.

This blog breaks everything down in simple terms. You’ll learn how these bureaus work, why your scores don’t always match, and how to decide which report matters most for your next loan. By the end, you’ll know exactly what to check before you apply.

Quick Look:

- CIBIL, Experian, Equifax, and Highmark provide credit reports that lenders use to assess trustworthiness.

- Scores differ because each bureau uses its own algorithm and reporting timelines for your credit data.

- CIBIL suits traditional loans, Experian supports new borrowers, while Equifax and Highmark fit diverse profiles.

- Checking all reports yearly helps spot errors and maintain a strong overall credit profile.

- Improve your score by paying on time, keeping utilisation low, and avoiding frequent loan applications.

Why Do Credit Bureaus Matter When You Apply For Loans?

Whenever you apply for a loan or credit card, lenders want to know how reliable you are as a borrower. They use your credit report to judge this, and that report is created by credit bureaus. These bureaus track your past repayments, active loans, missed EMIs, and overall credit behaviour.

India has four major bureaus: CIBIL, Experian, Equifax, and Highmark. Each one collects your data differently, so understanding how they work helps you prepare for smoother approvals.

Also Read: 7 Smart Tips to Increase Your CIBIL Score Immediately

How Do CIBIL, Experian, Equifax, and Highmark Compare?

Before choosing which score to monitor more actively, you should know how these bureaus operate. Each one follows its own scoring model, update cycles, and data interpretation rules. These differences can influence how lenders judge your creditworthiness.

Here’s a quick comparison:

| Credit Bureau | Common Users | Score Band | Free Annual Report | Key Advantage |

| CIBIL | Traditional banks | 300–900 | Yes | Strong lender acceptance |

| Experian | Fintech lenders | 300–900 | Yes | Clear dashboard and easier disputes |

| Equifax | NBFCs and small businesses | 300–900 | Yes | Detailed commercial analytics |

| Highmark | Microfinance and the gig sector | 300–900 | Yes | Strong coverage of alternate data |

CIBIL

CIBIL is the bureau most banks check first, especially for traditional loans. It maintains extensive historical data, giving lenders a clear view of long-term repayment patterns. Because of its wide adoption, your CIBIL score often influences approval speed and interest rates.

- Strong visibility across almost every major bank

- Detailed repayment timelines that help lenders judge consistency

- Higher scores often unlock smoother approvals

Experian

Experian offers reports that are easier to read and resolve, which suits young and digital-first borrowers. Many app-based lenders rely on Experian, so your activity here matters if you prefer short-term or instant loans.

- Simple layout that highlights key credit factors clearly

- Faster handling of disputes and corrections

- Supports newer credit profiles without harsh scoring dips

Equifax

Equifax is widely used for commercial lending, which makes it valuable if you juggle both personal and business credit. Its reports often highlight business-related enquiries, secured loans, and repayment discipline in a structured way that lenders appreciate.

- Strong business credit data for self-employed borrowers

- Trusted by NBFCs that serve SMEs and small entrepreneurs

- Well-balanced reports for mixed personal and business use

CRIF Highmark

CRIF Highmark stands out by tracking credit activity outside the typical salaried segment. It covers microfinance loans, small-ticket borrowing, and alternate income patterns, making it helpful for students, freelancers, and first-jobbers who may not have regular income proofs.

- Better tracking of microfinance and small loans

- Useful for gig workers and early earners

- Accurate insights for borrowers with limited formal credit

Why Do Your Credit Scores Differ Across Bureaus?

If you’ve ever checked your score across CIBIL, Experian, Equifax, and Highmark, you’ve probably noticed four different numbers staring back at you. It can feel confusing, especially when you expect one fixed score, but each bureau treats your data slightly differently, so variation is completely normal.

Before we get into why the mismatch happens, let's see what each bureau considers a healthy credit score:

- CIBIL: 750+ is usually seen as strong

- Experian: 700+ is generally considered good

- Equifax: 670+ is acceptable for most lenders

- Highmark: 700+ is preferred for smooth approvals

Now, here’s why your scores never match perfectly:

- Lenders may report your loan information to one bureau earlier than others.

- Each bureau has a slightly unique scoring formula, which rates behaviour differently.

- Errors or outdated entries may appear on one report but not another.

- Some lenders only report to selected bureaus, leading to incomplete data on the rest.

- Recent changes, such as closing a loan, may take time to sync across systems.

Fortunately, lenders know these differences exist. They usually check one bureau based on their internal policy, so minor variations don’t affect your chances. What matters is keeping all reports accurate, consistent, and updated.

If score variations leave you unsure about approvals, Pocketly can help with short-term funds with easy EMIs during urgent situations.

Key Similarities Across India’s Credit Bureaus

When you first compare CIBIL, Experian, Equifax, and Highmark, it’s easy to assume they’re completely different. But once you dig a little deeper, you’ll realise they actually follow many of the same credit-reporting rules in India.

Here’s what they share:

- All four agencies receive the same borrower information from banks, NBFCs, and lenders, as per RBI requirements.

- Each bureau checks similar factors: repayment history, type of credit, total loan exposure, credit age, and recent inquiries.

- Every bureau issues a valid credit report and score that lenders recognise.

- All are licensed credit information companies in India operating under the same regulations.

Even though their scores may look slightly different, the building blocks remain the same everywhere.

Which Credit Bureau Gives The Best Report?

If you’re comparing CIBIL, Experian, Equifax, and Highmark for the “best” credit report, the answer depends on who you are and how you plan to borrow. Instead of claiming one clear winner, it’s better to look at how each bureau stands out for different types of customers.

| Feature Area | CIBIL | Experian | Highmark | Equifax |

| Major bank preference | Strong | Strong | Moderate | Low |

| Score friendliness for new users | Low | High | High | Low |

| Coverage of informal or gig income | Limited | Good | Strong | Good |

| Commercial credit tracking | Not available | Not available | Not available | Very strong |

| Reporting trend for fintech lenders | High | High | High | Medium |

Also Read: Meaning and Differences between CRIF and CIBIL Score

Which Credit Bureau Should You Rely On?

Every borrower’s situation differs, and the best bureau for you usually depends on your financial journey. This is why the same report will not suit everyone.

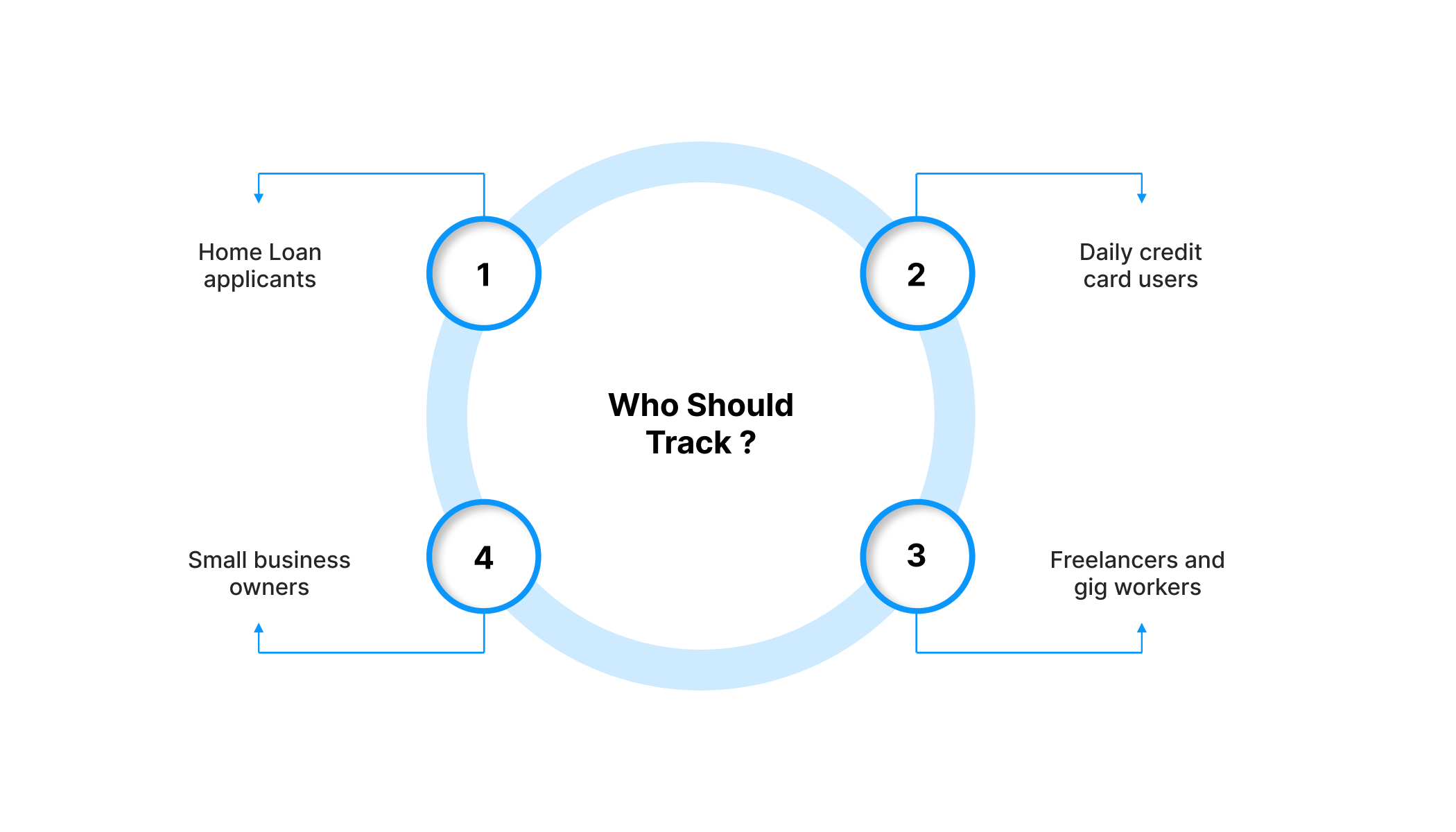

Who Should Track What?

- Home Loan applicants often rely on CIBIL because banks use it most frequently.

- Daily credit card users may find Experian more up-to-date because several issuers report changes here quickly.

- Freelancers and gig workers usually see more accurate data on Highmark.

- Small business owners often benefit from checking Equifax because it tracks both personal and business credit.

But should you depend on only one? Not really. All four reports are valid, and many lenders cross-check more than one bureau for large-ticket loans. It’s smarter to keep track of at least two to stay prepared.

Tips To Improve Your Credit Profile Across Bureaus

No matter which bureau you follow, CIBIL, Experian, Equifax, or Highmark, the basics of building a stable credit score remain the same. A lender might see slightly different numbers, but your habits shape all of them over time.

Steps you can start applying today:

- Review all four reports once a year to catch errors, outdated information, or mismatched loan details.

- Raise disputes quickly if something doesn’t look right. Incorrect data can affect scores differently across bureaus.

- Pay all EMIs on time, even if it means setting reminders or auto-payments. One missed due date can show up differently depending on the bureau’s update cycle.

- Keep your credit card usage under 30% to show responsible spending behaviour.

- Avoid applying for too many loans at once, as multiple hard inquiries reduce your score.

- Maintain a balanced mix of long-term (secured) and short-term (unsecured) credit.

Also Read: Overdue Payment Record and its Impact on CIBIL Score

How Pocketly Helps When Credit Scores Slow You Down

Credit score differences can sometimes delay approvals, especially when you’re dealing with tight timelines or sudden expenses. That’s where Pocketly steps in as a helpful solution for urgent cash needs.

Pocketly is a digital lending platform (not an NFBC) for short-term needs. You can get loans anywhere between ₹1,000-₹25,000 with interest starting at 2% per month, processing fees of 1-8%, without any hidden charges.

There is no collateral or physical paperwork, and the entire journey is suitable for urgent needs faced by students, gig workers, and young earners.

How to Apply on Pocketly:

- Sign up using your mobile number.

- Upload Aadhaar, PAN, and complete your digital KYC.

- Finish verification (including video KYC if required).

- Add bank details for secure transfers.

- Choose the loan amount and tenure.

- Receive the funds directly in your bank account within minutes.

Pocketly’s quick disbursal, flexible EMIs, and 24/7 support help you cover short-term expenses while staying consistent with your CIBIL, Experian, Equifax, and Highmark scores.

Wrapping Up

Understanding how your credit profile works across CIBIL, Experian, Equifax, and Highmark helps you read reports with more clarity. Each bureau collects data differently, so variations in your score are normal and nothing to stress about. What matters most is keeping healthy habits like timely payments, controlled credit usage, and regular monitoring.

Knowing this makes it easier to plan your borrowing, compare lenders, and choose the right products for short-term or long-term needs. And if you’re ever in a situation where you need quick support while maintaining steady credit behaviour, Pocketly can be a helpful option.

Pocketly offers small, fast personal loans designed for real-life expenses without heavy paperwork or long waits. Download Pocketly on iOS or Android to manage short-term needs smartly while staying consistent with your long-term credit goals.

FAQ’s

What is the difference between a CIBIL score and a Highmark score?

CIBIL and Highmark both measure creditworthiness, but they use different scoring models and data sources. CIBIL is widely used by banks, while Highmark covers more alternate credit histories, like rural loans and gig workers.

Which credit bureau credit score is valuable in India?

All four CIBIL, Experian, Equifax, and Highmark are valid in India. Lenders may prefer one over another depending on loan type or institution, but all scores carry regulatory approval.

Which is better, CIBIL or Experian?

Neither is strictly better as it depends on your borrowing profile. CIBIL is preferred by traditional banks, whereas Experian can be more helpful for first-time borrowers or fintech-based loans.

How many apps are providing us a free Credit score, which is powered by TransUnion CIBIL only?

Several apps in India offer free access to TransUnion CIBIL scores, typically once a year. These include CIBIL’s official website and select fintech platforms.