A CIBIL score of 750 or more in India is excellent and can enhance your borrowing power. Your credit score plays a crucial role in your financial health, impacting everything from loan approvals to interest rates. Yet, millions of people still struggle with poor credit scores, due to simple mistakes or a lack of awareness about how credit works.

Fortunately, improving your credit score is not only possible but achievable with the right strategies. In this blog, we'll walk you through how to build a credit score, so you can get better financial opportunities and enjoy long-term savings.

Key Takeaways

- Timely Payments Matter Most: Timely payments account for 35% of your credit score, making them the most important factor in building and maintaining a strong score.

- Credit Utilisation Affects Your Score: Keep your credit utilisation ratio below 30% to positively impact your score. Lower utilisation shows that you’re managing debt responsibly.

- Hard Inquiries Can Harm Your Score: Frequent credit applications result in hard inquiries that lower your score. Apply only when necessary and space out applications to minimise impact.

- Dispute Errors: Regularly review your report for inaccuracies. Disputing errors can result in score improvements, sometimes within a short period.

- Longer Loan Tenures Offer Flexibility: Opting for longer loan tenures can ease debt management with smaller monthly payments and help diversify your credit mix, benefiting your overall score.

Top 10 Ways to Build and Improve Your Credit Score

A healthy credit score is important for better financial opportunities, such as loans, credit cards, and favourable interest rates. Various factors, like payment history and the length of your credit history, influence your credit score. Let’s take a look at ways to strengthen your score and ensure financial stability.

1. Make On-Time Payments

Paying on time is the most important factor influencing 35% of your credit score, which is calculated by your payment history, making it the largest single factor. When you make on-time payments for bills, personal loans, or credit cards, it reflects your ability to manage debt responsibly, which boosts your creditworthiness.

How Timely Payments Impact Your Credit Score

- Lenders see a history of on-time payments as an indication of reliability, which directly influences how much credit they are willing to extend.

- Missing a payment, even by just a few days, can cause a dip in your score, with more significant drops for payments that are overdue for 30, 60, or 90+ days.

- Consistent late payments over time can prevent you from achieving an excellent credit score, making it difficult to access affordable loans, housing, or even jobs (where credit checks are common).

Tools and Strategies for Staying on Track:

- Set Reminders: Use tools like Google Calendar, Apple Reminders, or your bank’s app to set up payment alerts well in advance of due dates.

- Automated Bill Payments: Many banks and credit card companies will help you set up automatic payments, so that your bills are paid on time, even if you forget.

- Consolidation Apps: Use personal finance apps like Mint to track all your due dates and set up alerts.

Also Read: Overdue Payment in Loan: Meaning, Consequences, and How to Clear It

2. Keep Credit Card Balances Low

Your credit utilisation ratio basically indicates how much of your available credit you are using. This ratio is crucial for your credit score as it makes up about 30% of your total score. A lower credit utilisation rate (below 30%) signals that you're not overly reliant on credit, which is seen as a positive trait by credit scoring models. For example, if you have a credit limit of ₹50,000 and you carry a balance of ₹15,000, your credit utilisation is 30%.

Why the Credit Utilisation Ratio Matters

- If you're using a large portion of your credit limit (e.g., above 50%), it may signal to lenders that you are financially stretched, making you a higher risk.

- Maintaining a lower balance relative to your credit limit shows lenders that you can manage your finances responsibly. This can help improve your credit utilisation.

- Aim to keep your ratio under 30%. The lower, the better; ideally, staying under 10% can maximise your credit score potential.

Benefits of Balance Transfer Offers

If you're carrying pending balances on multiple credit cards, a balance transfer offer can be a lifesaver. There are credit card companies that offer 0% interest on balance transfers at the starting phase(usually 6–12 months). This allows you to reduce your debt faster without accruing high-interest charges.

Common Mistakes to Avoid

- Maxing Out Your Credit Cards: One of the most detrimental mistakes is using your credit cards up to their limit. When your utilisation is at or near 100%, your credit score can take a hit.

- Carrying High Balances: Even if you don’t max out your cards, consistently carrying high balances (above 30%) will harm your credit score.

- Opening Too Many New Accounts: Opening new accounts or credit cards to increase your available credit can cause problems. It increases your overall available credit but can also raise your credit inquiries and reduce the average age of your credit accounts.

Avoid Opening Too Many Accounts at Once

When you apply for new credit, lenders perform a hard inquiry (also known as a hard pull) to assess your creditworthiness. Each hard inquiry can cause a small, short-term dip in your credit score. While a single hard inquiry may not affect your score, too many in a short period can raise a red flag to potential lenders.

Best Practices

To minimise the impact of hard inquiries, it’s important to manage how and when you apply for credit. Here are some tips:

- Space Out Your Applications: Avoid applying for multiple credit cards, loans, or mortgages within a short period. Space your applications out over several months to reduce the negative impact on your score.

- Only Apply When Necessary: Be selective about when you apply for new credit. Consider whether you truly need the credit or if it's a luxury purchase. Always assess your financial situation and eligibility before applying.

- Use Prequalification Tools: Many lenders offer soft inquiries for prequalification, which won’t affect your credit score. This is a great way to check your chances of approval before formally applying.

Note: Multiple hard inquiries in a short time can reduce your credit score. For example, a 10-point drop is common if you have several hard inquiries within a six-month period.

4. Keep Older Accounts Open

The length of your credit history is a major factor in computing your credit score, accounting for about 15% of your overall score. A longer credit history is a sign of reliability, showing lenders that you have experience managing credit responsibly. When you keep older accounts open, your average credit history length increases, which can have a positive impact on your score. On the other hand, closing older accounts shortens your credit history, which may cause your score to drop.

Tips for Credit Account Management

While it’s important to keep older accounts open, managing them properly is equally crucial. Here are some tips to keep old accounts active without unnecessary fees:

- Set Recurring Payments: If you're not using an old account frequently, set up a small recurring payment (like a subscription or utility bill) to ensure the account remains active.

- Avoid Annual Fees: Some older credit cards may have high annual fees. If this is the case, consider calling the issuer to ask for a fee waiver or to switch to a no-fee version, keeping the account open but reducing costs.

- Minimal Use: If you don’t want to carry a balance on an old credit card, use it for minor purchases and pay it off in full each month to avoid interest.

Avoiding Account Closures

Closing old accounts, although it seems like a way to simplify your financial life, may hurt your credit score. Here’s why:

- Reduced Credit History Length: Closing old accounts shortens your credit history, further affecting your score.

- Higher Credit Utilisation: Closing accounts can reduce your overall available credit, which may increase your credit utilisation ratio, thereby lowering your score.

- Credit Mix Impact: Keeping a variety of credit types (credit cards, loans, etc.) helps improve your credit score. Closing old accounts can limit your credit mix, especially if it’s a type of credit you no longer actively use.

5. Diversify Your Credit Types

There are various types of credit that contribute to your overall credit score. The main categories include:

- Credit Cards: Revolving credit allows you to borrow up to a limit and pay back over time.

- Loans: Personal loans, auto and student loans are types of installment credit where you borrow a fixed amount and repay it over time with interest.

- Mortgages: A long-term loan used to buy property, which is typically secured by the home itself.

Having a mix of credit types portrays to the lenders that you can manage different kinds of debt responsibly. This further impacts your credit score, contributing to a better credit mix and providing a fuller picture of your ability to handle various payment obligations.

Appropriate Loan Choices

While credit cards are common, taking out a small personal loan or an auto loan (if financially feasible) can help diversify your credit profile. For example:

- Personal Loans: These can be an effective way to improve your credit mix while providing funds for an important purchase or emergency. They also help show your ability to handle non-revolving credit. With Pocketly, you can access personal loans ranging from ₹1,000 to ₹25,000 with good interest rates and flexible repayment terms

- Auto Loans: Financing a car through an auto loan can be a good way to add an installment loan to your credit mix, improving your credit diversity.

6. Dispute Any Inaccuracies on Your Credit Report

Your credit report is a summary of your credit history, including credit card accounts, loans, payment history, and outstanding debts. Here’s how to break it down:

- Personal Information: This section includes your name, address, date of birth, and social security number. Check for any incorrect details, such as misspelt names or outdated addresses.

- Credit Accounts: This lists all credit cards, loans, and mortgages you've held, including the balance and payment history. Look for unfamiliar accounts or accounts that have wrong payment statuses.

- Credit Inquiries: Hard inquiries made by lenders when you apply for credit. Make sure no unauthorised inquiries are listed here.

- Public Records: This section may include bankruptcies, judgments, or liens. Ensure these are accurate and reflect your actual financial history.

- Discrepancies: Common errors include late payments that were made on time, incorrect account balances, or accounts listed as “open” when they were actually closed.

Steps to Report a Dispute

If you find inaccuracies, follow these steps:

1. Obtain Your Credit Report: Get your free credit report from major bureaus such as Equifax, Experian, or TransUnion.

2. Identify the Errors: Carefully review your report to find any discrepancies.

3. Contact the Credit Bureau: File a dispute with the bureau online or via mail. Provide evidence to support your claim, like bank statements or payment receipts.

4. Wait for Resolution: Credit bureaus typically investigate disputes within 30 days. If the information is found to be incorrect, they will remove or correct it.

5. Follow-up: After the investigation, you’ll receive a report on the findings. Ensure that the inaccuracies have been resolved and that your score reflects the corrections.

The Importance of Accuracy

A mistakenly reported late payment, an incorrectly high balance, or an account marked as delinquent can lower your score, increase the interest, and reduce your chances of securing credit. It’s important to check your credit report regularly for inaccuracies and dispute them promptly to maintain a healthy credit score.

7. Settle Any Outstanding Collections

An account that goes into collections is one of the most damaging things to your credit score. Once a debt is handed over to an agency, it stays on your credit report for 7 years. Collections accounts can significantly lower your score, making it difficult to qualify for secure housing or even get certain jobs (where credit checks are part of the hiring process).

- Impact on Score: Collection accounts can cause a sharp drop in your credit score, often by 50–100 points or more, depending on the other aspects of your credit report.

- Delayed Recovery: Even after paying off the collection, it can take years for your score to recover fully, although settling the account will improve your score slightly by showing the account as "paid."

Negotiation Strategies

Here are some strategies to help you settle collections:

- Pay for Deletion: One common negotiation tactic is to offer the complete payment in exchange for the collection account being deleted from your credit report. This is known as a "pay-for-delete" agreement. Although not all creditors will agree to this, it’s worth trying.

- Settle for Less: If you can't afford the full amount, negotiate to settle the debt for less than what you owe. Some collectors will accept a reduced payment as full satisfaction of the debt.

- Get Everything in Writing: Before making any payments, ensure that the agreement is documented in writing. This ensures that the creditor or collection agency will honour their commitment to report the debt as settled or deleted

8. Use a Credit Builder Loan

A credit builder loan is for those who have little to no credit history to build or improve their credit score. Unlike traditional loans, where you receive funds upfront, in this type of loan, it goes directly into a savings account or a certificate of deposit, which you cannot access until you pay off the loan. Your repayments are reported to bureaus as you repay through various loan repayment modes.

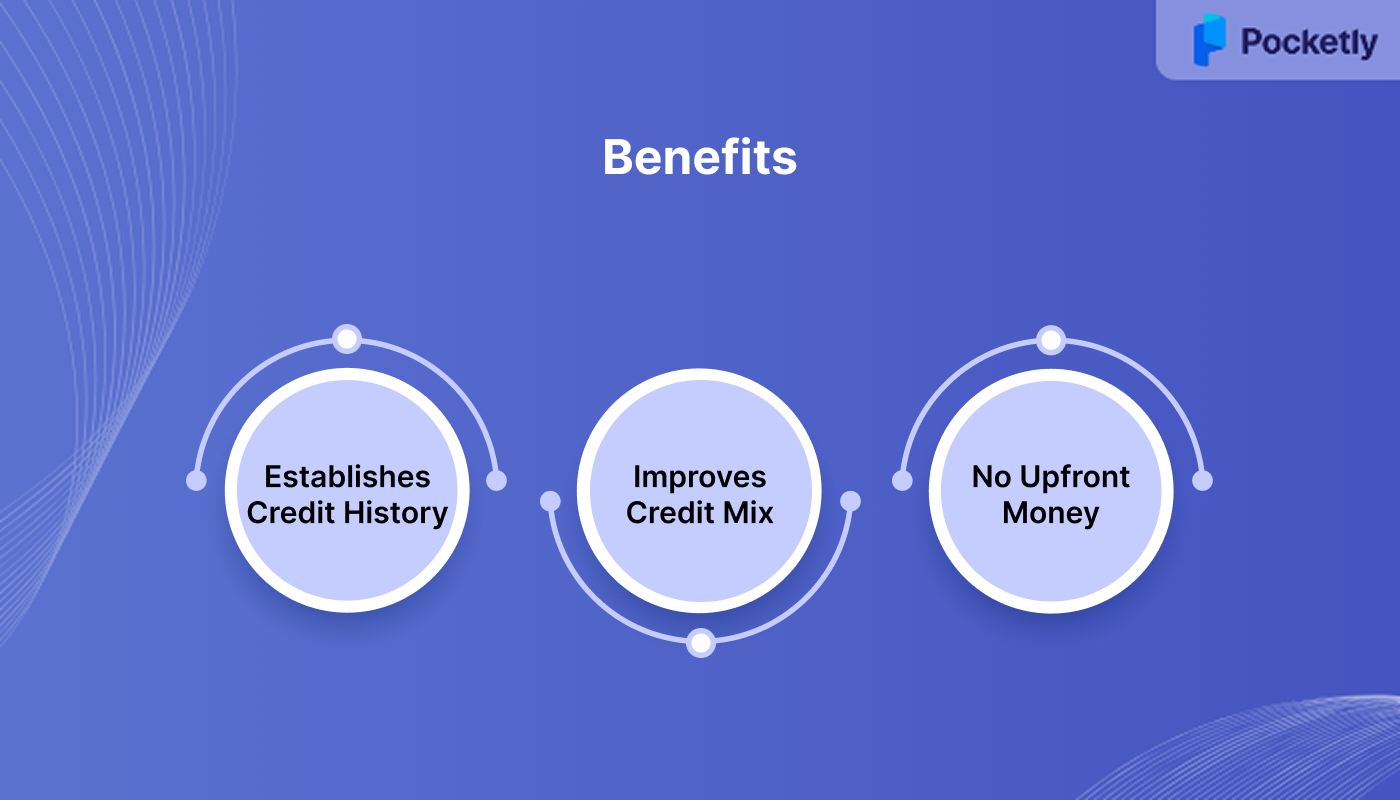

Benefits

A credit builder loan can be a powerful tool for improving your credit score, especially for people who are just starting out or recovering from past credit issues. Here are some key benefits:

- Establishes Credit History: For individuals with little or no credit, this loan is a great way to establish a credit history.

- Improves Credit Mix: It adds an installment loan to your credit mix, which can positively affect your credit score.

- No Upfront Money: Since the loan amount is held in a savings account or CD until the loan is paid off, you don't need any initial funds, making it accessible for those who may not have extra cash.

Alternatives to Loans

If you’re unable to qualify for a credit builder loan, there are other options to help build credit:

- Secured Credit Cards: They require a deposit as collateral, which acts as your credit limit. Correct usage of a secured card can help improve your credit score over time.

- Credit-Builder Apps: Some apps offer services that help you build credit by reporting your rent and utility payments to credit bureaus. These can be a good alternative if you don't qualify for a loan or card.

- Store Cards: Many stores offer credit cards with lower approval standards. While their limits are usually low, using them responsibly can help build your credit.

9. Opt for Longer Loan Tenures

Choosing a longer loan tenure can be beneficial for your credit score, especially when it comes to installment loans (like personal loans or auto loans). A longer tenure usually means smaller monthly payments, which can make it easier to manage your debt, especially if you're on a tight budget. It shows lenders that you’re capable of handling larger amounts of debt over a longer period, demonstrating creditworthiness.

Benefits of Longer Loan Tenures

While opting for a longer tenure can be an effective way to manage your debt, it also has benefits in terms of your credit profile:

- Credit Mix Diversification: A mix of different types of credit (e.g., credit cards, short-term loans, and long-term loans) can boost your credit score by showing that you can handle various kinds of debt.

- Improved Payment History: With a long-term loan, you have more opportunities to show lenders your ability to make consistent, timely payments, which boosts your credit score.

10. Pay Down Revolving Account Balances

Revolving accounts, such as credit cards and lines of credit, allow you to borrow up to a limit and carry a balance from month to month. Unlike installment loans, revolving credit doesn’t have fixed repayment terms, so it’s crucial to manage your balances carefully.

Credit Utilisation Ratio: Ideally, you should aim to keep your credit utilisation ratio below 30% further showing the lender that you're not overly reliant on credit and can manage your finances properly.

How Paying Down Balances Improves Your Score

Paying down your revolving account balances can have an instant effect on your credit score:

- Lower Credit Utilisation: Reducing the amount you owe decreases your credit utilisation ratio, which directly boosts your score.

- Interest Savings: Paying off revolving balances reduces the interest you pay on your debt, freeing up more money for other financial goals.

Tips for Managing Revolving Accounts

- Make Small Payments Regularly: If you can’t pay off the balance in full, make regular payments that reduce your balance over time. This can help lower your utilisation and keep your score moving upward.

- Pay Before the Statement Date: If possible, pay down your credit card balances before your statement date to minimise reported utilisation and boost your score.

- Avoid Maxing Out Credit Cards: Avoid carrying balances close to your credit limit, as this increases your credit utilisation ratio and can lower your score.

Why Choose Pocketly for Your Personal Loan Needs?

When it comes to managing your finances and building your credit score, Pocketly’s instant personal loan approval offers a convenient and flexible solution with a quick and transparent process. Whether you're looking to cover emergency expenses, consolidate debt, or make a big purchase, Pocketly makes it easy to access the funds you need.

Here’s why Pocketly stands out:

- Loan Amounts: Access loans ranging from ₹1,000 to ₹25,000 to meet various personal needs.

- Affordable Interest Rates: Starting at 2% ensuring manageable payments.

- Flexible Processing Fees: Processing fees range from 1% to 8% on the loan amount and repayment terms.

- EMI Options: Choose flexible repayment options with easy EMIs to suit your budget.

- Hassle-Free Application: Enjoy a simple, digital loan application process with minimal documentation and an easy KYC verification.

- No Hidden Charges: Transparent terms with no hidden fees, ensuring a smooth borrowing experience.

Conclusion

Improving your credit score is a vital step towards gaining financial freedom, securing loans, and achieving better interest rates. The strategies outlined in this blog, from making timely payments to managing revolving credit balances, can help you steadily build a healthier credit profile. While these steps may take time, consistency and smart financial practices will lead to long-term benefits in your credit health.

Pocketly, as a digital lending platform, offers flexible loan amounts, making it easier for you to manage your finances and build your credit score. Download Pocketly now on iOS or Android and take the next step in improving your financial future!

FAQs

1. What is the 15 3 rule for credit?

The 15/3 rule suggests paying off your credit card balance twice a month—once when it hits 15% of the credit limit and again just before the due date. This can lower your credit ratio and improve your score.

2. Is 3 months enough to build credit?

While 3 months is a short period, it can help establish a positive credit history, especially if you're using a credit-builder loan or a secured card and making timely payments.

3. How to build a CIBIL score from 0?

To build your CIBIL score from 0, start by applying for a secured credit card or a credit-builder loan, and make on-time payments to establish a positive payment history.

4. Why is my credit score going down when I pay on time?

Even if you pay on time, your credit score can drop due to factors like high credit utilisation, frequent credit inquiries, or errors on your credit report. Regularly check your report for discrepancies.

5. What is a bad credit score?

A bad credit score typically falls below 600. Scores in this range make it difficult to qualify for loans or cards, and if approved, they often come with higher interest rates.