Have you ever needed money urgently and wondered how a cash advance actually works in real life? It often sounds simple, quick access to funds, but the details can be confusing, especially when you're unsure about the cost and repayment.

In India today, as per CRIF High Mark, nearly 90% of small personal loans under ₹1 lakh are originated by digital-first fintech NBFCs, while credit card cash advances are expanding rapidly across ATM, online, and over-the-counter channels. This surge reflects how millions turn to quick cash solutions for urgent needs, but the real cost and repayment impact often remain unclear.

A cash advance is commonly used for short-term needs, whether through a credit card withdrawal or a small digital loan. But understanding the real impact requires more than just a definition.

In this blog, you will learn the cash advance meaning, how it works in India, and see real-life examples that break down the actual cost, repayment, and decision-making involved.

Key Takeaways

-

A cash advance gives quick access to funds through credit cards or short-term loans, but this convenience often comes with higher immediate costs.

-

Interest and charges usually begin immediately, which can increase the total repayment amount faster than expected.

-

Real examples help you understand how repayment and costs build up in practical situations.

-

Credit card cash advances often lack structured repayment, while short-term options with clear terms are easier to plan and manage.

What Is a Cash Advance?

A cash advance provides immediate access to funds, either by withdrawing cash from your credit card or by taking a short-term loan through a digital platform. For many young Indian students, salaried professionals managing monthly expenses, and self-employed individuals dealing with irregular income, cash advances often become a quick way to handle urgent financial needs.

In simple terms, the cash advance's meaning is immediate access to funds that you repay over a short period, usually with added charges.

There are two common types in India:

-

Credit card cash advance: Withdraw money from an ATM using your credit card.

-

Short-term digital loan: Borrow a small amount through an app with defined repayment terms.

To understand this better, it helps to look at how a cash advance actually works in real situations.

How a Cash Advance Works in India

Cash advances are designed for speed, but the process and repayment experience can vary depending on how you access the funds.

-

You can withdraw money instantly from an ATM using your credit card, with the amount added to your outstanding balance.

-

Or apply for a small loan through a digital platform, where the amount is transferred directly to your bank account after approval.

-

Interest often starts accruing immediately, especially for credit card withdrawals, with no interest-free period.

-

Repayment timelines are shorter and may not follow a fixed EMI structure, making planning more important.

For example, if you withdraw ₹5,000 using your credit card, the amount starts attracting interest from the same day and must be repaid along with your bill, which can feel more expensive than expected.

Because of this, what feels like a quick solution can become difficult to manage if not planned carefully. Once you see how cash advances function, it becomes easier to understand how they differ from traditional loans.

Also Read: Applying for an Instant Personal Credit Line Online

Is a Cash Advance a Loan or Something Different?

A common question is whether a cash advance is a loan. Technically, yes, it involves borrowing money. But it works differently from a traditional loan.

-

A loan usually comes with EMIs and a clear repayment structure.

-

A cash advance (credit card) has no EMI and starts accruing interest immediately.

-

A digital short-term loan sits somewhere in between, offering structure but shorter tenure.

This difference is important because it directly affects how easy or difficult repayment becomes.

Cash Advance Example in India (Real Scenarios)

Understanding how a cash advance works becomes much easier when you look at real-life situations.

Example 1: ₹4,000 Credit Card Cash Advance

You withdraw ₹4,000 using your credit card from an ATM to handle an urgent expense.

Here's what typically happens:

-

Interest starts immediately from the day of withdrawal.

-

There is no interest-free period.

-

Additional withdrawal fees may apply.

-

You need to repay it along with your credit card bill.

Even though ₹4,000 seems manageable, the lack of structure means the amount can feel heavier during repayment, especially if other expenses are due at the same time.

Note: Unlike regular purchases that may have a grace period, cash advances start accruing interest immediately because they are treated as cash withdrawals by the issuer.

Example 2: ₹10,000 Short-Term Digital Loan

You take a ₹10,000 short-term loan through a digital platform for a medical expense.

In this case:

-

You are shown the total repayment amount upfront.

-

A fixed repayment timeline is provided.

-

You may repay in one go or in structured instalments.

-

Costs are clearer before you borrow.

This makes it easier to plan compared to a credit card cash advance, even if the purpose is the same.

Example 3: Emergency Timing Gap

When deciding, consider factors such as cost, repayment flexibility, and urgency of the need to select the most manageable option. If your salary is due in 5 days but you need ₹5,000 today for a repair, it creates a short-term gap.

You have two options:

-

Withdraw using a credit card, which is quick but expensive and unstructured.

-

Take a short-term loan, which has slightly more steps, but clearer repayment.

The decision here is not just about speed, but about how manageable the repayment will feel after the emergency is resolved.

Cost Breakdown: What You Actually Pay

A cash advance is not just about the amount you withdraw; it's about the total cost that builds up quickly, often in ways that are easy to overlook.

Here's what typically adds up:

-

Interest charges: In many cases, interest starts from the day you withdraw the money, especially with credit card cash advances. There is usually no interest-free period.

-

Withdrawal or processing fees: A percentage of the amount withdrawn may be charged upfront, increasing the effective cost immediately.

-

Short repayment window: Since repayment is expected within a billing cycle or short tenure, the pressure to repay quickly can make the cost feel heavier.

Example: How Costs Add Up

Suppose you withdraw ₹5,000 using a credit card cash advance:

-

Withdrawal or processing fees typically range from 2% to 3% of the amount withdrawn, increasing the upfront cost (₹100-₹150).

-

Interest starts immediately.

-

The full amount is added to your next bill.

If not repaid quickly, the total payable increases faster than expected, even for a small amount.

Unlike traditional loans, cash advance monthly payments are often not structured, especially for credit card withdrawals. This lack of clarity makes it harder to plan and increases the risk of carrying forward the balance.

Cash Advance vs Short-Term Loan: What's the Difference?

Although both options solve short-term needs, the experience can be very different.

|

Factor |

Cash Advance (Credit Card) |

Short-Term Loan |

|

Structure |

No fixed repayment plan |

Defined repayment timeline |

|

Interest |

Starts immediately |

Usually disclosed upfront |

|

Cost clarity |

Can feel unclear |

More transparent |

|

Financial control |

Harder to manage |

Easier to plan |

|

Usage behaviour |

Often impulsive |

More intentional |

Understanding this difference helps you make better borrowing decisions.

Also Read: The Ultimate Guide to Small Business Loans in India (2026)

When a Cash Advance May or May Not Make Sense

A cash advance may be beneficial in certain scenarios, but the outcome depends on how clearly the need and repayment are planned. It works best as a short-term solution for immediate needs, not as a regular way to manage expenses.

Quick Decision Guide

|

Situation |

Should You Use a Cash Advance? |

Why It Matters |

|

Urgent, unavoidable expense |

Yes (with planning) |

Helps address immediate need without delay |

|

Salary or payment due soon |

Yes (short duration) |

Easier to repay quickly and limit cost |

|

Non-essential spending |

No |

Adds unnecessary cost without real need |

|

Already managing multiple payments |

No |

Increases financial pressure and risk |

|

No clear repayment plan |

No |

Higher chance of delayed repayment |

The difference often comes down to planning. A one-time, well-managed use is very different from repeated or unplanned borrowing.

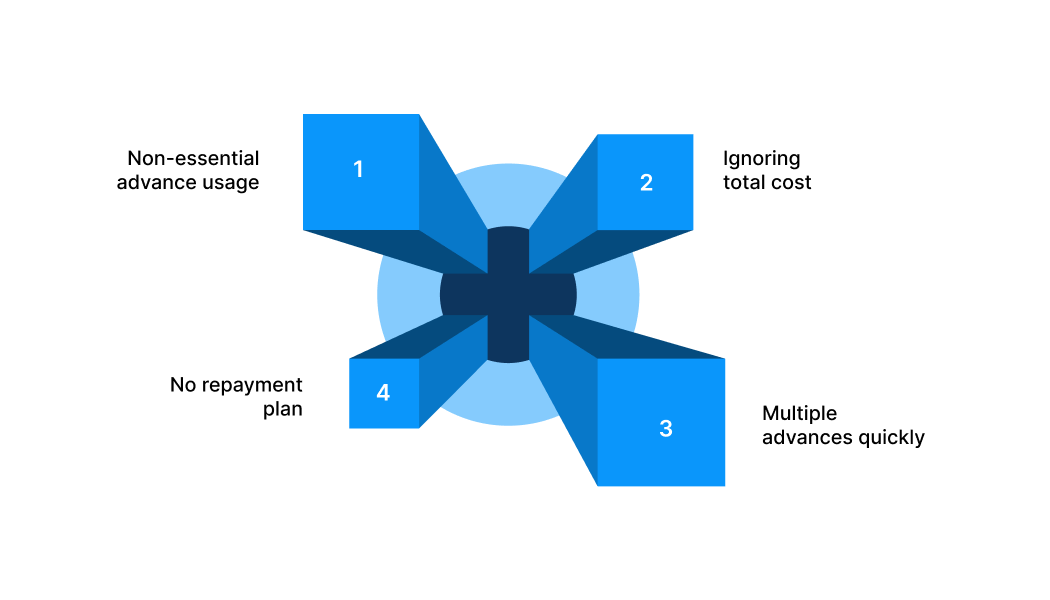

Common Mistakes That Increase Financial Pressure

Even small decisions can create long-term impact when they turn into repeated habits, especially with short-term borrowing.

-

Using cash advances for non-essential spending: This often turns a temporary solution into a recurring expense. Keeping it limited to urgent needs helps avoid unnecessary dependency.

-

Ignoring the total cost involved: Looking only at the amount borrowed can be misleading. Taking a moment to check the full repayment amount makes it easier to plan ahead.

-

Taking multiple advances in a short time: Frequent borrowing can quickly increase financial pressure. Spacing out usage and relying on income where possible improves control.

-

Not planning repayment in advance: Without a clear repayment plan, delays become more likely. Knowing how you will repay before borrowing reduces last-minute stress.

Over time, these patterns reduce financial flexibility and make borrowing harder to manage. Avoiding them is not just about discipline, but about making more deliberate choices when handling short-term financial needs.

If you are dealing with a short-term cash need, choosing a more structured option with clear repayment terms can make it easier to stay in control.

Managing Short-Term Cash Needs with Pocketly

Not every short-term financial need requires a long-term commitment. The goal is to manage it in a way that keeps your finances stable.

Pocketly, not an NBFC itself, is a fintech platform designed for young Indians, offering simple and transparent access to small, short-term credit. It operates as a digital lending platform, working with RBI-registered NBFCs (Fairassets Technologies India Private Limited, NDX Financial Services Private Limited and Speel Finance Company Private Limited) to provide structured borrowing options without collateral, along with 24/7 support and clear, upfront pricing.

Here's how Pocketly supports better short-term borrowing:

-

Borrow between ₹1,000 and ₹25,000 based on your need.

-

No collateral or guarantor required.

-

Quick digital KYC process.

-

Direct transfer to your bank account.

-

Flexible repayment options.

-

Transparent pricing with no hidden charges.

-

Interest starts from 2% per month, with processing fees between 1% and 8%.

-

24/7 access through the app.

How to Apply

-

Step 1: Visit the website or download the app.

-

Step 2: Complete a quick digital KYC.

-

Step 3: Select your loan amount.

-

Step 4: Receive approval and funds.

What to Keep in Mind Before Taking a Cash Advance

Before borrowing, it helps to look at the full picture:

-

Understand the total cost.

-

Check if repayment fits your income cycle.

-

Borrow only what you need.

-

Plan repayment in advance.

Taking a few minutes to review these can prevent unnecessary financial stress later.

Check your eligibility on Pocketly in a few minutes, manage urgent needs like medical expenses, rent gaps, or repairs without long-term commitments.

Conclusion

Looking at a cash advance example in India makes one thing clear: the decision is not just about accessing money quickly, but about understanding the cost, timing, and repayment behind it.

As short-term borrowing becomes more accessible, the real difference lies in how clearly you evaluate your options before taking one. A small gap in timing or an urgent need can be managed effectively when the repayment is planned and the terms are transparent.

Over time, building this clarity helps you handle similar situations with more confidence and less financial pressure.

Exploring structured options like Pocketly can give you a clearer view of your borrowing choices, helping you manage short-term needs with more control and predictability. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. What is a cash advance loan?

A cash advance loan is a short-term way to access funds instantly, either through a credit card withdrawal or a small digital loan with a short repayment period.

2. Is a cash advance a loan?

Yes, it involves borrowing money, but it differs from traditional loans because repayment is faster and, in some cases, less structured.

3. Do cash advances have monthly payments?

Not always. Credit card cash advances usually do not follow fixed monthly payments, while digital short-term loans may offer defined repayment schedules.

4. Is a cash advance more expensive than regular credit card use?

In most cases, yes. Cash advances often start accruing interest immediately and may include additional fees, making them costlier than normal card transactions.

5. Does a cash advance show in your credit card statement?

Yes, it appears as a separate transaction and is added to your outstanding balance, which you need to repay.

6. When should you avoid taking a cash advance?

It is best avoided for non-essential expenses or when you are unsure about repayment, as the cost and short timeline can create additional pressure.